|

市場調查報告書

商品編碼

1699345

皮下注射器及針頭市場機會、成長動力、產業趨勢分析及 2025-2034 年預測Hypodermic Syringes and Needles Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

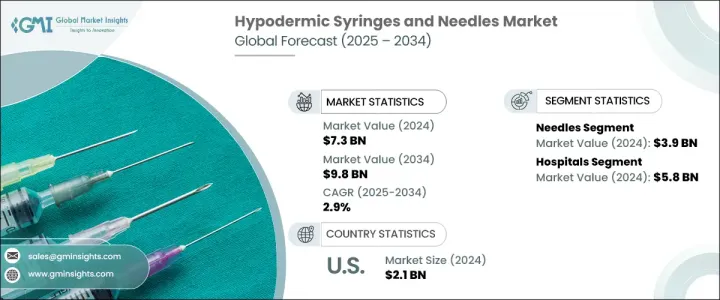

2024 年全球皮下注射器和針頭市場價值為 73 億美元,預計 2025 年至 2034 年期間的複合年成長率為 2.9%。這一成長受到多種因素的推動,包括慢性病患病率上升、外科手術數量增加以及注射器和針頭在採血中的使用率不斷提高。隨著醫療保健的進步不斷影響現代醫療方法,預計未來十年對高效、精確注射設備的需求將激增。此外,藥物管理技術的進步、對安全注射器的推動以及需要定期注射的老年人口的增加,進一步加強了市場擴張。

慢性病負擔的惡化是導致注射器和針頭需求增加的重要因素。全球數百萬人需要頻繁注射藥物來治療糖尿病、關節炎和心血管疾病等疾病,這更凸顯了對可靠、精確的針頭系統的需求。對預防保健的日益關注,加上對疫苗接種計劃的認知不斷提高,預計也將推動市場成長。政府推動免疫接種的舉措和對家庭醫療保健解決方案日益成長的偏好進一步推動了採用率。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 73億美元 |

| 預測值 | 98億美元 |

| 複合年成長率 | 2.9% |

市場分為兩個主要部分:注射器和針頭。針頭市場預計將成為整體市場擴張的主要貢獻者,預計複合年成長率為 3.1%,到 2034 年將達到 54 億美元。慢性病治療的需求日益成長,特別是對於需要定期注射的患者而言,這推動了對先進針頭技術的需求。隨著自行注射數量的穩定成長以及對感染預防的日益重視,製造商正致力於創新針頭設計,以提高患者的舒適度和安全性。

在應用方面,皮下注射器和針頭市場涵蓋多個類別,包括採血、藥物輸送、疫苗接種、胰島素給藥等。藥物傳輸領域預計將經歷顯著成長,到 2034 年將達到 48 億美元,複合年成長率為 2.8%。隨著管理慢性病的人數不斷增加,對有效的藥物管理解決方案的需求也越來越大。該行業正在見證無針注射系統、智慧注射器和預充式注射器技術的進步,這些技術在提高藥物輸送效率和患者依從性方面發揮著至關重要的作用。

2024 年美國皮下注射器和針頭市場價值為 21.3 億美元,預計在 2025 年至 2034 年期間將以 1.8% 的速度成長。該國完善的醫療保健基礎設施,加上慢性病的高發生率,繼續推動對這些設備的需求。由於相當一部分人口需要注射治療,對精確、高品質的注射器和針頭的需求仍然強勁。此外,對醫療保健創新的投資不斷增加以及確保產品安全和效率的嚴格監管政策正在進一步塑造美國的市場動態。隨著對注射解決方案的需求不斷成長,製造商正專注於永續且方便用戶使用的注射器和針頭技術,以滿足不斷變化的醫療保健需求。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 產業衝擊力

- 成長動力

- 慢性病發生率上升

- 手術數量增加

- 技術進步與產品創新

- 注射器和針頭採血使用量激增

- 產業陷阱與挑戰

- 針刺傷和感染的風險

- 成長動力

- 成長潛力分析

- 監管格局

- 技術格局

- 新興替代品

- 差距分析

- 波特的分析

- PESTEL分析

- 未來市場趨勢

第4章:競爭格局

- 介紹

- 公司矩陣分析

- 公司市佔率分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 策略儀表板

第5章:市場估計與預測:按類型,2021 - 2034 年

- 主要趨勢

- 注射器

- 針

第6章:市場估計與預測:按可用性,2021 - 2034 年

- 主要趨勢

- 一次性的

- 可重複使用的

第7章:市場估計與預測:按應用,2021 - 2034 年

- 主要趨勢

- 血液收集

- 藥物輸送

- 疫苗接種

- 胰島素給藥

- 其他應用

第8章:市場估計與預測:依最終用途,2021 - 2034 年

- 主要趨勢

- 醫院

- 門診手術中心

- 診斷中心

- 其他最終用途

第9章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- Abbott

- B. Braun

- BD (Becton, Dickinson and Company)

- Cardinal Health

- Catalent

- Connecticut Hypodermics

- DeRoyal

- EXEl

- HI-TECH MEDICS

- ICU medical

- Lifelong MEDITECH

- McKESSON

- Medline

- NIPRO

- RETRACTABLE TECHNOLOGIES

- TERUMO

- VITA NEEDLE

- VMG

The Global Hypodermic Syringes And Needles Market was valued at USD 7.3 billion in 2024 and is set to grow at a CAGR of 2.9% from 2025 to 2034. This growth is fueled by multiple factors, including the rising prevalence of chronic diseases, an increasing number of surgical procedures, and the expanding utilization of syringes and needles for blood collection. As healthcare advancements continue to shape modern medical treatments, the demand for efficient and precise injection devices is expected to surge over the next decade. Additionally, technological advancements in drug administration, the push for safety-engineered syringes, and the rising geriatric population requiring routine injections are further strengthening market expansion.

The growing burden of chronic illnesses is a significant driver behind the increasing demand for hypodermic syringes and needles. Millions of people worldwide require frequent injectable medications for conditions such as diabetes, arthritis, and cardiovascular diseases, amplifying the need for reliable and accurate needle systems. The increasing focus on preventive care, coupled with rising awareness of vaccination programs, is also expected to propel market growth. Government initiatives promoting immunization and the increasing preference for home healthcare solutions are further driving adoption rates.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $7.3 Billion |

| Forecast Value | $9.8 Billion |

| CAGR | 2.9% |

The market is divided into two key segments: syringes and needles. The needle segment is poised to be the primary contributor to overall market expansion, with a projected CAGR of 3.1%, reaching USD 5.4 billion by 2034. The growing necessity for chronic care treatments, particularly for patients who require regular injections, is fueling the demand for advanced needle technologies. With the steady increase in the number of self-administered injections and the growing emphasis on infection prevention, manufacturers are focusing on innovative needle designs that enhance patient comfort and safety.

In terms of application, the hypodermic syringes and needles market spans various categories, including blood collection, drug delivery, vaccinations, insulin administration, and more. The drug delivery segment is projected to experience notable growth, reaching USD 4.8 billion by 2034 at a CAGR of 2.8%. As the number of individuals managing chronic diseases rises, there is a greater need for effective medication administration solutions. The industry is witnessing advancements in needle-free injection systems, smart syringes, and prefilled syringe technology, all of which are playing a crucial role in enhancing drug delivery efficiency and patient compliance.

The U.S. Hypodermic Syringes and Needles Market was valued at USD 2.13 billion in 2024 and is set to grow at a rate of 1.8% between 2025 and 2034. The country's well-established healthcare infrastructure, combined with a high prevalence of chronic diseases, continues to drive demand for these devices. With a significant portion of the population requiring injectable treatments, the need for precise and high-quality syringes and needles remains strong. Moreover, increasing investments in healthcare innovation and stringent regulatory policies ensuring product safety and efficiency are further shaping the market dynamics in the United States. As the demand for injectable solutions grows, manufacturers are focusing on sustainable and user-friendly syringe and needle technologies to cater to evolving healthcare needs.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising incidence of chronic disorders

- 3.2.1.2 Increase in the number of surgeries

- 3.2.1.3 Technological advancements and product innovation

- 3.2.1.4 Surged adoption of syringes and needles for blood collection

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Risk of needlestick injuries and infection

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Emerging alternatives

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Future market trends

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Syringes

- 5.3 Needles

Chapter 6 Market Estimates and Forecast, By Usability, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Disposable

- 6.3 Reusable

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Blood collection

- 7.3 Drug delivery

- 7.4 Vaccination

- 7.5 Insulin administration

- 7.6 Other applications

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals

- 8.3 Ambulatory surgical centers

- 8.4 Diagnostic centers

- 8.5 Other end use

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Abbott

- 10.2 B. Braun

- 10.3 BD (Becton, Dickinson and Company)

- 10.4 Cardinal Health

- 10.5 Catalent

- 10.6 Connecticut Hypodermics

- 10.7 DeRoyal

- 10.8 EXEl

- 10.9 HI-TECH MEDICS

- 10.10 ICU medical

- 10.11 Lifelong MEDITECH

- 10.12 McKESSON

- 10.13 Medline

- 10.14 NIPRO

- 10.15 RETRACTABLE TECHNOLOGIES

- 10.16 TERUMO

- 10.17 VITA NEEDLE

- 10.18 VMG

2025 年全球注射器與針頭市場報告

2025 年全球注射器與針頭市場報告 針市場:各設計型針類型,各目的型針類型,各交付方式,各材料類型,各終端用戶,各地區,與主要企業:2035年前的產業趨勢與全球預測

針市場:各設計型針類型,各目的型針類型,各交付方式,各材料類型,各終端用戶,各地區,與主要企業:2035年前的產業趨勢與全球預測 全球過濾針市場 - 2025-2033

全球過濾針市場 - 2025-2033 可操縱針市場,按產品類型、應用、最終用途、國家和地區 - 2024-2032 年行業分析、市場規模、市場佔有率和預測高流量針頭套件市場,按容量、類型、最終用途、材料、國家和地區 - 2024-2032 年行業分析、市場規模、市場佔有率和預測過濾針市場,按原料、最終用戶、國家和地區 - 2024-2032 年行業分析、市場規模、市場佔有率和預測

可操縱針市場,按產品類型、應用、最終用途、國家和地區 - 2024-2032 年行業分析、市場規模、市場佔有率和預測高流量針頭套件市場,按容量、類型、最終用途、材料、國家和地區 - 2024-2032 年行業分析、市場規模、市場佔有率和預測過濾針市場,按原料、最終用戶、國家和地區 - 2024-2032 年行業分析、市場規模、市場佔有率和預測 注射器和針頭的全球市場 2024-2028

注射器和針頭的全球市場 2024-2028 注射器針頭市場:按產品類型、最終用戶分類 - 全球預測 2025-2030靜脈針市場:按規格、最終用戶分類 - 2025-2030 年全球預測脊椎針市場:按產品類型、應用、最終用戶、年齡層、應用、材料、手術類型 - 2025-2030 年全球預測

注射器針頭市場:按產品類型、最終用戶分類 - 全球預測 2025-2030靜脈針市場:按規格、最終用戶分類 - 2025-2030 年全球預測脊椎針市場:按產品類型、應用、最終用戶、年齡層、應用、材料、手術類型 - 2025-2030 年全球預測