|

市場調查報告書

商品編碼

1699434

柴油發電電信發電機市場機會、成長動力、產業趨勢分析及 2025-2034 年預測Diesel Fired Telecom Generator Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

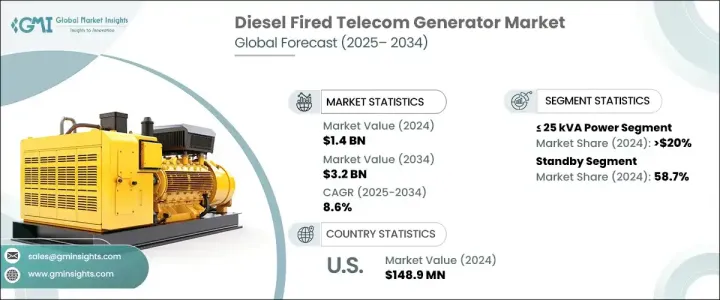

2024 年全球柴油發電電信發電機市場價值為 14 億美元,預計 2025 年至 2034 年期間將以 8.6% 的複合年成長率大幅成長。隨著 4G 和 5G 網路的快速普及,資料服務需求不斷成長,這推動了整個電信基礎設施對可靠電源解決方案的需求。隨著全球電信業的不斷擴張,電信塔數量的不斷增加,加上對不間斷供電的需求,促使電信業者投資柴油發電機以維持無縫服務。此外,發展中地區頻繁停電和缺乏可靠的電力供應為電信業者部署備用電源解決方案提供了巨大的成長機會,確保持續的服務可用性。

隨著城市化進程的加快,升級老化的電信基礎設施和擴大服務欠缺地區的網路覆蓋範圍的需求正成為當務之急。柴油發電機在確保城市和偏遠地區電信站的可靠電力方面發揮關鍵作用,在這些地區保持無縫連接至關重要。越來越依賴備用電源系統來支援不斷成長的資料流量和自動化技術,進一步凸顯了這些發電機在電信領域的重要性。此外,對提高能源效率的追求,加上先進監控系統的整合,提高了這些發電機的性能,使其成為現代電信營運中不可或缺的一部分。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 14億美元 |

| 預測值 | 32億美元 |

| 複合年成長率 | 8.6% |

柴油電信發電機市場按發電機容量和類型細分。 2024 年,額定功率 <= 25 kVA 的小型發電機佔據了 20% 的市場。這些緊湊型發電機對於為基礎設施仍在建設中的農村和低度開發地區的偏遠電信站供電特別有價值。它們的效率使其成為小規模營運的理想選擇,例如為基地台和小型蜂窩供電,這對於將網路覆蓋範圍擴大到服務不足的地區至關重要。隨著電信網路不斷擴展以滿足日益成長的連接需求,對小型高效發電機的需求預計會增加。

就發電機類型而言,備用柴油電信發電機佔據市場主導地位,到 2024 年將佔據 58.7% 的佔有率。對不間斷網路服務和最短停機時間的需求不斷成長,推動了這一領域的成長。電信營運商越來越依賴這些發電機來維持持續營運,尤其是隨著 5G 網路、行動資料服務和自動化技術的不斷普及。這些發電機在電力中斷期間提供可靠的備用電源,確保電信服務不間斷地保持活躍。

2024 年美國柴油電信發電機市場價值為 1.489 億美元,由於邊緣運算和資料中心營運對持續電力的需求不斷成長,需求激增。由於不間斷高效電力對於維持高性能網路至關重要,柴油備用發電機的作用仍然至關重要。此外,減少排放和將先進的監控系統整合到電信基礎設施的努力進一步推動了市場成長。隨著電信業適應不斷發展的技術需求,柴油備用發電機將繼續在確保可靠且有效率的服務交付方面發揮關鍵作用。

目錄

第1章:方法論與範圍

- 市場範圍和定義

- 市場估計和預測參數

- 預測計算

- 資料來源

- 基本的

- 次要

- 有薪資的

- 民眾

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 監管格局

- 產業衝擊力

- 成長動力

- 產業陷阱與挑戰

- 成長潛力分析

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 戰略展望

- 創新與永續發展格局

第5章:市場規模及預測:依功率等級,2021 年至 2034 年

- 主要趨勢

- ≤25千伏安

- > 25千伏安 - 50千伏安

- > 50千伏安 - 125千伏安

- > 125 千伏安 - 200 千伏安

- > 200 千伏安 - 330 千伏安

- > 330千伏安

第6章:市場規模及預測:依應用,2021 年至 2034 年

- 主要趨勢

- 支援

- 主/連續

第7章:市場規模及預測:依地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 俄羅斯

- 英國

- 德國

- 法國

- 西班牙

- 奧地利

- 義大利

- 亞太地區

- 中國

- 澳洲

- 印度

- 日本

- 韓國

- 印尼

- 馬來西亞

- 泰國

- 越南

- 菲律賓

- 緬甸

- 孟加拉

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 卡達

- 土耳其

- 伊朗

- 阿曼

- 非洲

- 埃及

- 奈及利亞

- 阿爾及利亞

- 南非

- 安哥拉

- 肯亞

- 莫三比克

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 智利

第8章:公司簡介

- AGG POWER TECHNOLOGY

- Aggreko

- Atlas Copco

- Caterpillar

- Cummins

- Deere & Company

- FG Wilson

- Generac Power Systems

- HIMOINSA

- Kirloskar Electric

- Kohler

- MAHINDRA POWEROL

- Perkins Engines Company

- SUPERNOVA GENSET

- Tractors and Farm Equipment

- Wärtsilä

The Global Diesel Fired Telecom Generator Market was valued at USD 1.4 billion in 2024 and is projected to grow significantly at a CAGR of 8.6% between 2025 and 2034. The increasing demand for data services, driven by the rapid adoption of 4G and 5G networks, is fueling the need for reliable power solutions across telecom infrastructure. As the global telecom industry continues to expand, the rising number of telecom towers, coupled with the need for uninterrupted power supply, is pushing telecom operators to invest in diesel-fired generators to maintain seamless service. Furthermore, frequent power outages and the lack of reliable electricity supply in developing regions present significant growth opportunities for telecom operators to deploy backup power solutions, ensuring consistent service availability.

As urbanization accelerates, the need to upgrade aging telecom infrastructure and expand network coverage in underserved regions is becoming a priority. Diesel-fired generators play a critical role in ensuring reliable power for telecom stations in both urban and remote areas, where maintaining seamless connectivity is essential. The growing reliance on backup power systems to support the growing data traffic and automation technologies further highlights the importance of these generators in the telecom sector. Additionally, the push for increased energy efficiency, coupled with the integration of advanced monitoring systems, is enhancing the performance of these generators, making them indispensable in modern telecom operations.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.4 Billion |

| Forecast Value | $3.2 Billion |

| CAGR | 8.6% |

The diesel-fired telecom generator market is segmented by generator capacity and type. Smaller units with a power rating of <= 25 kVA accounted for 20% of the market share in 2024. These compact generators are particularly valuable for powering remote telecom stations in rural and underdeveloped regions where infrastructure development is still ongoing. Their efficiency makes them ideal for smaller-scale operations such as powering base stations and small cells, which are essential for extending network coverage to underserved areas. As telecom networks continue to expand to meet the growing demand for connectivity, the need for smaller, highly efficient generators is expected to rise.

In terms of generator type, standby diesel-fired telecom generators dominated the market, holding 58.7% of the share in 2024. The rising need for uninterrupted network service and minimal downtime is driving the growth of this segment. Telecom operators increasingly depend on these generators to maintain continuous operations, especially as 5G networks, mobile data services, and automation technologies continue to proliferate. These generators provide a reliable backup during power disruptions, ensuring that telecom services remain active without interruption.

The U.S. diesel-fired telecom generator market was valued at USD 148.9 million in 2024, with demand surging due to the growing need for continuous power in edge computing and data center operations. As uninterrupted and efficient power becomes critical for maintaining high-performance networks, the role of diesel-powered backup generators remains vital. Additionally, the push to reduce emissions and integrate advanced monitoring systems into telecom infrastructure is further propelling market growth. As the telecom industry adapts to evolving technological needs, diesel-powered backup generators will continue to play a crucial role in ensuring reliable and efficient service delivery.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's Analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL Analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Strategic outlook

- 4.3 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Power Rating, 2021 – 2034 (Units & USD Million)

- 5.1 Key trends

- 5.2 ≤ 25 kVA

- 5.3 > 25 kVA - 50 kVA

- 5.4 > 50 kVA - 125 kVA

- 5.5 > 125 kVA - 200 kVA

- 5.6 > 200 kVA - 330 kVA

- 5.7 > 330 kVA

Chapter 6 Market Size and Forecast, By Application, 2021 – 2034 (Units & USD Million)

- 6.1 Key trends

- 6.2 Standby

- 6.3 Prime/continuous

Chapter 7 Market Size and Forecast, By Region, 2021 – 2034 (Units & USD Million)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Russia

- 7.3.2 UK

- 7.3.3 Germany

- 7.3.4 France

- 7.3.5 Spain

- 7.3.6 Austria

- 7.3.7 Italy

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Australia

- 7.4.3 India

- 7.4.4 Japan

- 7.4.5 South Korea

- 7.4.6 Indonesia

- 7.4.7 Malaysia

- 7.4.8 Thailand

- 7.4.9 Vietnam

- 7.4.10 Philippines

- 7.4.11 Myanmar

- 7.4.12 Bangladesh

- 7.5 Middle East

- 7.5.1 Saudi Arabia

- 7.5.2 UAE

- 7.5.3 Qatar

- 7.5.4 Turkey

- 7.5.5 Iran

- 7.5.6 Oman

- 7.6 Africa

- 7.6.1 Egypt

- 7.6.2 Nigeria

- 7.6.3 Algeria

- 7.6.4 South Africa

- 7.6.5 Angola

- 7.6.6 Kenya

- 7.6.7 Mozambique

- 7.7 Latin America

- 7.7.1 Brazil

- 7.7.2 Mexico

- 7.7.3 Argentina

- 7.7.4 Chile

Chapter 8 Company Profiles

- 8.1 AGG POWER TECHNOLOGY

- 8.2 Aggreko

- 8.3 Atlas Copco

- 8.4 Caterpillar

- 8.5 Cummins

- 8.6 Deere & Company

- 8.7 FG Wilson

- 8.8 Generac Power Systems

- 8.9 HIMOINSA

- 8.10 Kirloskar Electric

- 8.11 Kohler

- 8.12 MAHINDRA POWEROL

- 8.13 Perkins Engines Company

- 8.14 SUPERNOVA GENSET

- 8.15 Tractors and Farm Equipment

- 8.16 Wärtsilä

攜帶式逆變發電機市場 - 全球產業規模、佔有率、趨勢、機會和預測,按功率等級、電源、最終用戶、地區、競爭進行細分,2020-2030 年預測

攜帶式逆變發電機市場 - 全球產業規模、佔有率、趨勢、機會和預測,按功率等級、電源、最終用戶、地區、競爭進行細分,2020-2030 年預測 2025年全球發電機市場報告

2025年全球發電機市場報告 全球發電機市場研究報告 - 產業分析、規模、佔有率、成長、趨勢和預測 2025 年至 2033 年

全球發電機市場研究報告 - 產業分析、規模、佔有率、成長、趨勢和預測 2025 年至 2033 年 全球黑啟動發電機市場研究報告 - 產業分析、規模、佔有率、成長、趨勢和預測 2025 年至 2033 年

全球黑啟動發電機市場研究報告 - 產業分析、規模、佔有率、成長、趨勢和預測 2025 年至 2033 年 備用建築發電機組市場機會、成長動力、產業趨勢分析及 2025-2034 年預測

備用建築發電機組市場機會、成長動力、產業趨勢分析及 2025-2034 年預測 柴油攜帶式逆變發電機市場機會、成長動力、產業趨勢分析及 2025-2034 年預測

柴油攜帶式逆變發電機市場機會、成長動力、產業趨勢分析及 2025-2034 年預測 建築攜帶式逆變發電機市場機會、成長動力、產業趨勢分析及 2025-2034 年預測

建築攜帶式逆變發電機市場機會、成長動力、產業趨勢分析及 2025-2034 年預測 發電機組市場 - 成長、未來展望、競爭分析,2025 年至 2033 年

發電機組市場 - 成長、未來展望、競爭分析,2025 年至 2033 年 2025 年全球發電機銷售市場報告

2025 年全球發電機銷售市場報告 同步發電機市場:全球產業分析、規模、佔有率、成長、趨勢和預測,2025-2032 年

同步發電機市場:全球產業分析、規模、佔有率、成長、趨勢和預測,2025-2032 年