|

市場調查報告書

商品編碼

1699438

內視鏡市場機會、成長動力、產業趨勢分析及 2025-2034 年預測Endoscopy Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

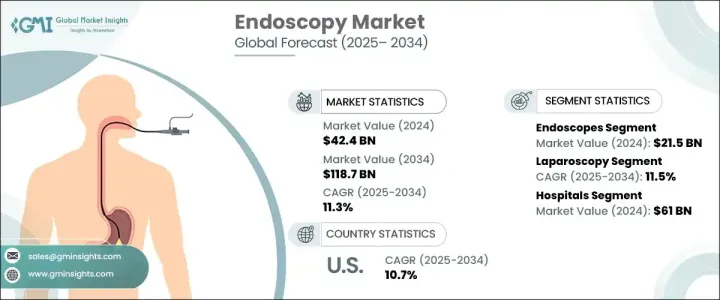

2024 年全球內視鏡市場價值為 424 億美元,預計 2025 年至 2034 年的複合年成長率為 11.3%。這一擴張是由醫學影像的快速進步、報銷框架的改善、慢性病患病率的上升以及對具有成本效益的診斷解決方案的需求不斷成長所推動的。內視鏡技術已經取得了顯著的發展,高清 (HD) 成像、3D 視覺化和窄帶成像 (NBI) 等創新技術提高了診斷的準確性。機器人、人工智慧(AI)和無線通訊的整合進一步提高了程式效率。此外,採用輕量、靈活和一次性使用的內視鏡可降低感染風險,同時提高可及性和可負擔性。多個醫療領域對微創技術的需求日益成長,使得內視鏡檢查成為首選的診斷和治療方法。

產品範圍包括內視鏡、視覺化系統、內視鏡超音波、充氣器和其他設備。內視鏡佔據市場主導地位,2024 年市場規模達 215 億美元。在應用方面,市場涵蓋腹腔鏡檢查、胃腸 (GI) 內視鏡檢查、關節鏡檢查、耳鼻喉內視鏡檢查、肺內視鏡檢查、婦產科和其他程序。 2024 年腹腔鏡手術市場規模將達到 112 億美元,到 2034 年的複合年成長率將達到 11.5%。人們對微創手術的偏好日益成長,推動了這一領域的發展,因為透過小切口進行的手術可以減少恢復時間和術後併發症。腹腔鏡手術的需求正在加速成長,特別是膽囊切除術、疝氣修補術和減肥手術。隨著肥胖人數的增加,越來越多的人選擇減重手術,進一步推動了市場的成長。腹腔鏡培訓計畫的日益普及確保了更多的外科醫生能夠採用這些技術,從而促進了更廣泛的應用。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 424億美元 |

| 預測值 | 1187億美元 |

| 複合年成長率 | 11.3% |

醫院仍然是最大的終端用戶群體,預計到 2034 年市場價值將達到 610 億美元。醫療機構依靠內視鏡進行常規篩檢、早期疾病檢測和外科手術干預,尤其是在腫瘤學領域。優惠的報銷政策和內視鏡檢查保險覆蓋範圍鼓勵醫院投資先進的設備和培訓項目。透過擴展內視鏡檢查能力,醫院可以改善病患的治療效果,同時最佳化醫療成本。對高品質、具成本效益程序的需求繼續推動醫療機構的技術進步和基礎設施投資。

北美佔了相當大的市場佔有率,其中美國位居榜首,2024 年的市佔率將達到 165 億美元。慢性疾病(尤其是胃腸道疾病和肥胖症)的負擔日益加重,增加了對內視鏡手術的需求。先進的醫療保健基礎設施和持續的技術創新(例如人工智慧輔助內視鏡和機器人系統)增強了市場擴張。此外,支持診斷和治療內視鏡手術的報銷政策改善了患者的就診機會,進一步刺激了需求。對早期疾病檢測和預防性醫療保健的持續重視鞏固了該地區在全球內視鏡市場的主導地位。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 產業衝擊力

- 成長動力

- 全球老年人口不斷成長

- 引進技術先進的內視鏡

- 胃腸道疾病、癌症和其他慢性疾病發生率上升

- 微創手術的需求不斷增加

- 產業陷阱與挑戰

- 發展中國家缺乏熟練的醫生和內視鏡醫師

- 成長動力

- 成長潛力分析

- 監管格局

- 美國

- 歐洲

- 技術格局

- 報銷場景

- 波特的分析

- PESTEL分析

- 差距分析

- 價值鏈分析

第4章:競爭格局

- 介紹

- 公司矩陣分析

- 公司市佔率分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 策略儀表板

第5章:市場估計與預測:按產品,2021 - 2034 年

- 主要趨勢

- 內視鏡

- 硬內視鏡

- 軟性內視鏡

- 機器人輔助內視鏡

- 膠囊內視鏡

- 可視化系統

- 內視鏡超音波

- 氣腹機

- 其他產品

第6章:市場估計與預測:按應用,2021 - 2034 年

- 主要趨勢

- 腹腔鏡檢查

- 胃腸內視鏡檢查

- 胃鏡

- 大腸鏡檢查

- 乙狀結腸鏡檢查

- 十二指腸鏡檢查

- 其他胃腸內視鏡檢查

- 關節鏡檢查

- 耳鼻喉內視鏡檢查

- 肺內視鏡檢查

- 婦產科

- 其他應用

第7章:市場估計與預測:依最終用途,2021 - 2034 年

- 主要趨勢

- 醫院

- 門診手術中心

- 其他最終用途

第8章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第9章:公司簡介

- B Braun

- Boston Scientific

- CONMED

- COOK MEDICAL

- FUJIFILM

- HOYA

- INTUITIVE

- Johnson & Johnson

- KARL STORZ

- Medtronic

- OLYMPUS

- RICHARD WOLF

- Smith & Nephew

- Stryker

The Global Endoscopy Market, valued at USD 42.4 billion in 2024, is projected to grow at a CAGR of 11.3% from 2025 to 2034. This expansion is driven by rapid advancements in medical imaging, improved reimbursement frameworks, a rising prevalence of chronic diseases, and an increasing demand for cost-effective diagnostic solutions. Endoscopic technology has evolved significantly with innovations like high-definition (HD) imaging, 3D visualization, and Narrow-Band Imaging (NBI), enhancing diagnostic accuracy. The integration of robotics, artificial intelligence (AI), and wireless communication further improves procedural efficiency. Additionally, the adoption of lightweight, flexible, and single-use endoscopes reduces infection risks while improving accessibility and affordability. The growing need for minimally invasive techniques across multiple medical fields has solidified endoscopy as a preferred diagnostic and treatment method.

The product landscape includes endoscopes, visualization systems, endoscopic ultrasound, insufflators, and other devices. Endoscopes dominated the market, generating USD 21.5 billion in 2024. On the application front, the market spans laparoscopy, gastrointestinal (GI) endoscopy, arthroscopy, ENT endoscopy, pulmonary endoscopy, obstetrics/gynecology, and other procedures. Laparoscopy accounted for USD 11.2 billion in 2024, expanding at an 11.5% CAGR through 2034. The rising preference for minimally invasive surgeries has fueled this segment, as procedures performed through small incisions reduce recovery time and postoperative complications. Demand for laparoscopic surgeries is accelerating, particularly for gallbladder removal, hernia repair, and bariatric procedures. With obesity on the rise, more individuals are opting for weight-loss surgeries, further propelling market growth. The increasing availability of laparoscopic training programs ensures more surgeons can adopt these techniques, promoting wider adoption.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $42.4 Billion |

| Forecast Value | $118.7 Billion |

| CAGR | 11.3% |

Hospitals remain the largest end-user segment, with projections indicating a market value of USD 61 billion by 2034. Healthcare institutions rely on endoscopy for routine screenings, early disease detection, and surgical interventions, particularly in oncology. Favorable reimbursement policies and insurance coverage for endoscopic procedures encourage hospitals to invest in advanced equipment and training programs. By expanding their endoscopic capabilities, hospitals improve patient outcomes while optimizing healthcare costs. The demand for high-quality, cost-effective procedures continues to drive technological advancements and infrastructure investments in healthcare facilities.

North America holds a significant share of the market, with the US leading at USD 16.5 billion in 2024. The rising burden of chronic diseases, particularly gastrointestinal disorders and obesity, has heightened the demand for endoscopic procedures. The presence of advanced healthcare infrastructure and ongoing technological innovations, such as AI-assisted endoscopy and robotic systems, strengthens market expansion. Additionally, reimbursement policies supporting diagnostic and therapeutic endoscopic procedures have improved patient access, further fueling demand. The continued emphasis on early disease detection and preventive healthcare solidifies the region's dominance in the global endoscopy market.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing geriatric population globally

- 3.2.1.2 Introduction of technologically advanced endoscopes

- 3.2.1.3 Rising incidences of gastrointestinal disorders, cancer, and other chronic conditions

- 3.2.1.4 Increasing demand for minimally invasive procedures

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Dearth of skilled physicians and endoscopists in developing countries

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 U.S.

- 3.4.2 Europe

- 3.5 Technology landscape

- 3.6 Reimbursement scenario

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Gap analysis

- 3.10 Value chain analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Endoscopes

- 5.2.1 Rigid endoscopes

- 5.2.2 Flexible endoscopes

- 5.2.3 Robot-assisted endoscopes

- 5.2.4 Capsule endoscopes

- 5.3 Visualization systems

- 5.4 Endoscopic ultrasound

- 5.5 Insufflator

- 5.6 Other products

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Laparoscopy

- 6.3 GI endoscopy

- 6.3.1 Gastroscopy

- 6.3.2 Colonoscopy

- 6.3.3 Sigmoidoscopy

- 6.3.4 Duodenoscopy

- 6.3.5 Other GI endoscopies

- 6.4 Arthroscopy

- 6.5 ENT endoscopy

- 6.6 Pulmonary endoscopy

- 6.7 Obstetrics/Gynecology

- 6.8 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgical centers

- 7.4 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 B Braun

- 9.2 Boston Scientific

- 9.3 CONMED

- 9.4 COOK MEDICAL

- 9.5 FUJIFILM

- 9.6 HOYA

- 9.7 INTUITIVE

- 9.8 Johnson & Johnson

- 9.9 KARL STORZ

- 9.10 Medtronic

- 9.11 OLYMPUS

- 9.12 RICHARD WOLF

- 9.13 Smith & Nephew

- 9.14 Stryker

醫療內視鏡影像處理器市場-全球產業規模、佔有率、趨勢、機會和預測(按類型、應用、地區和競爭細分,2020-2030 年)

醫療內視鏡影像處理器市場-全球產業規模、佔有率、趨勢、機會和預測(按類型、應用、地區和競爭細分,2020-2030 年) 2025年全球內視鏡視訊系統市場報告

2025年全球內視鏡視訊系統市場報告 全球內視鏡人工智慧市場研究報告-產業分析、規模、佔有率、成長、趨勢和預測 2025 年至 2033 年

全球內視鏡人工智慧市場研究報告-產業分析、規模、佔有率、成長、趨勢和預測 2025 年至 2033 年 全球內視鏡治療設備市場:2025 年

全球內視鏡治療設備市場:2025 年 2025 年去除異物全球市場報告

2025 年去除異物全球市場報告 內視鏡設備市場:依產品類型、應用、最終用戶和地區分類

內視鏡設備市場:依產品類型、應用、最終用戶和地區分類 內視鏡封閉系統市場,按應用、按產品、按最終用途、按國家和地區 - 2025 年至 2032 年全球行業分析、市場規模、市場佔有率和預測

內視鏡封閉系統市場,按應用、按產品、按最終用途、按國家和地區 - 2025 年至 2032 年全球行業分析、市場規模、市場佔有率和預測 內視鏡設備市場分析及預測(截至 2033 年),按類型、產品、服務、技術、組件、應用、最終用戶、設備、安裝類型和解決方案分類

內視鏡設備市場分析及預測(截至 2033 年),按類型、產品、服務、技術、組件、應用、最終用戶、設備、安裝類型和解決方案分類 內視鏡設備和軟體市場規模、佔有率、成長分析(按產品、應用、最終用戶、地區)- 產業預測,2025 年至 2032 年

內視鏡設備和軟體市場規模、佔有率、成長分析(按產品、應用、最終用戶、地區)- 產業預測,2025 年至 2032 年 單側雙通道內視鏡市場:依產品類型、適應症、最終用戶和地區

單側雙通道內視鏡市場:依產品類型、適應症、最終用戶和地區