|

市場調查報告書

商品編碼

1699439

醫用 X 光市場機會、成長動力、產業趨勢分析及 2025-2034 年預測Medical X-ray Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

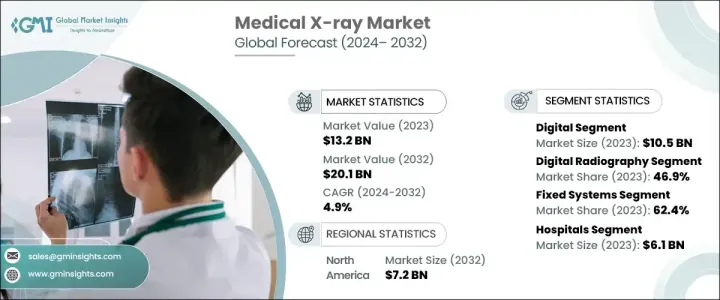

2023 年全球醫用 X 光市場規模達到約 132 億美元,預計 2024 年至 2032 年期間的複合年成長率為 4.9%。醫用 X 光是必不可少的診斷影像工具,主要用於觀察身體內部結構,包括骨骼、器官和組織。

醫療X光市場的成長主要受到醫療設施擴張和診斷能力進步的推動,尤其是在新興經濟體。這些發展中地區正在大力投資現代化醫療保健基礎設施,包括尖端的X光系統,以滿足日益成長的診斷影像服務需求。此外,人們對早期疾病檢測重要性的認知不斷提高,也促進了 X 光成像的更廣泛應用。行動和攜帶式 X 光設備的進步也促進了市場的成長,因為這些創新使得診斷成像更容易獲得。此外,人口老化增加了與年齡相關疾病的診斷服務的需求,進一步推動了市場擴張。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 132億美元 |

| 預測值 | 201億美元 |

| 複合年成長率 | 4.9% |

市場分為數位和類比 X 光類型,其中數位領域處於領先地位,2023 年的收入約為 105 億美元。數位 X 光系統與遠距醫療平台的整合增強了其實用性,促進了遠端諮詢和診斷審查。無線和攜帶式數位X光系統等技術創新正在擴大其在各種臨床環境中的應用。此外,對法規遵循和品質保證的關注推動了數位 X 光系統的採用,符合嚴格的醫療保健標準。

按技術細分,醫療X光市場包括數位射線照相術、電腦射線照相術和基於膠片的射線照相術。數位放射成像領域佔最大佔有率,2023 年營收將達到 62 億美元,預計預測期內複合年成長率為 5.1%。該領域的成長主要歸因於其能夠產生具有卓越清晰度和準確性的高解析度影像,這對於有效的醫學診斷至關重要。數位射線照相技術在捕捉和處理影像方面的效率可快速提高患者吞吐量並減少週轉時間。此外,數位放射成像與現代醫療保健 IT 系統無縫整合,改善了資料管理和可存取性。

在北美,由於完善的醫療保健基礎設施有利於先進技術的採用,預計到 2032 年醫療 X 光市場規模將達到 72 億美元。美國佔據北美市場的很大佔有率,2023 年的營收為 43 億美元。慢性病盛行率的上升顯著推動了對包括 X 光系統在內的診斷影像服務的需求,而事故和傷害的增加凸顯了對準確診斷工具的需求。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 產業衝擊力

- 成長動力

- 已開發國家診斷影像技術的進步

- 全球慢性病盛行率不斷上升

- 診斷成像程序的數量不斷增加

- 醫療 X 光檢查的報銷情況

- 產業陷阱與挑戰

- 高輻射暴露的風險

- 安裝醫學影像設備的成本高昂

- 成長動力

- 成長潛力分析

- 未來市場趨勢

- 監管格局

- 技術格局

- 2023年成交量分析(單位)

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 策略儀表板

第5章:市場估計與預測:按類型,2021 年至 2032 年

- 主要趨勢

- 數位的

- 模擬

第6章:市場估計與預測:按技術,2021 年至 2032 年

- 主要趨勢

- 底片放射照相術

- 電腦放射成像

- 數位射線照相術

第7章:市場估計與預測:按便攜性,2021 年至 2032 年

- 主要趨勢

- 固定系統

- 攜帶式系統

第 8 章:市場估計與預測:按應用,2021 年至 2032 年

- 主要趨勢

- 牙科

- 口內成像

- 口外成像

- 獸醫

- 腫瘤學

- 骨科

- 心臟病學

- 神經病學

- 其他獸醫應用

- 乳房X光檢查

- 胸部

- 心血管

- 骨科

- 其他應用

第9章:市場估計與預測:依最終用途,2021 年至 2032 年

- 主要趨勢

- 醫院

- 門診手術中心

- 專科診所

- 其他最終用途

第10章:市場估計與預測:按地區,2021 年至 2032 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 亞太地區

- 中國

- 日本

- 印度

- 越南

- 韓國

- 泰國

- 大洋洲

- 印尼

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 埃及

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第 11 章:公司簡介

- Agfa-Gevaert Group

- Allengers Medical Systems

- Canon

- Carestream Health

- Dentsply Sirona

- Fujifilm Holdings Corporation

- GE HealthCare Technologies

- Hologic

- Koninklijke Philips NV

- Konica Minolta

- Midmark

- Neusoft Medical Systems

- Perlong Medical Equipment

- Samsung Electronics

- Shimadzu

- Siemens Healthineers

- Trivitron Healthcare

The Global Medical X-Ray Market reached around USD 13.2 billion in 2023 and is projected to grow at 4.9% CAGR from 2024 to 2032. Medical X-rays are essential diagnostic imaging tools primarily used to visualize internal body structures, including bones, organs, and tissues.

Growth in the medical X-ray market is largely driven by the expansion of healthcare facilities and advancements in diagnostic capabilities, particularly in emerging economies. These developing regions are investing heavily in modern healthcare infrastructure, which includes cutting-edge X-ray systems, to meet the rising demand for diagnostic imaging services. Additionally, increased awareness of the importance of early disease detection is encouraging broader adoption of X-ray imaging. The advancement of mobile and portable X-ray devices is also contributing to market growth, as these innovations make diagnostic imaging more accessible. Moreover, the aging population is increasing the demand for diagnostic services related to age-associated conditions, further propelling market expansion.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $13.2 Billion |

| Forecast Value | $20.1 Billion |

| CAGR | 4.9% |

The market is categorized into digital and analog X-ray types, with the digital segment leading the way, generating revenues of approximately USD 10.5 billion in 2023. The integration of digital X-ray systems with telemedicine platforms enhances their utility, facilitating remote consultations and diagnostic reviews. Technological innovations, such as wireless and portable digital X-ray systems, are expanding their application across various clinical environments. Additionally, the focus on regulatory compliance and quality assurance drives the adoption of digital X-ray systems, aligning with rigorous healthcare standards.

When segmented by technology, the medical X-ray market includes digital radiography, computed radiography, and film-based radiography. The digital radiography segment captured the largest share, with revenues reaching USD 6.2 billion in 2023 and is expected to grow at a CAGR of 5.1% during the forecast period. This segment's growth is primarily attributed to its capacity to produce high-resolution images with superior clarity and accuracy, crucial for effective medical diagnoses. The efficiency of digital radiography in capturing and processing images swiftly enhances patient throughput and reduces turnaround times. Furthermore, digital radiography seamlessly integrates with modern healthcare IT systems, improving data management and accessibility.

In North America, the medical X-ray market is anticipated to reach USD 7.2 billion by 2032, supported by a well-established healthcare infrastructure that facilitates the adoption of advanced technologies. The U.S. holds a significant portion of the North American market, with revenues of USD 4.3 billion in 2023. The rising prevalence of chronic diseases is notably driving demand for diagnostic imaging services, including X-ray systems, while an increase in accidents and injuries emphasizes the need for accurate diagnostic tools.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Technological advancements in diagnostic imaging in developed countries

- 3.2.1.2 Rising prevalence of chronic diseases worldwide

- 3.2.1.3 Growing number of diagnostic imaging procedures

- 3.2.1.4 Presence of reimbursement for medical x-ray procedures

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Risk of high radiation exposure

- 3.2.2.2 High cost associated with installation of medical imaging modalities

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Regulatory landscape

- 3.6 Technological landscape

- 3.7 Volume analysis, 2023 (Units)

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2023

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Type, 2021 – 2032 ($ Mn)

- 5.1 Key trends

- 5.2 Digital

- 5.3 Analog

Chapter 6 Market Estimates and Forecast, By Technology, 2021 – 2032 ($ Mn)

- 6.1 Key trends

- 6.2 Film-based radiography

- 6.3 Computed radiography

- 6.4 Digital radiography

Chapter 7 Market Estimates and Forecast, By Portability, 2021 – 2032 ($ Mn)

- 7.1 Key trends

- 7.2 Fixed systems

- 7.3 Portable systems

Chapter 8 Market Estimates and Forecast, By Application, 2021 – 2032 ($ Mn)

- 8.1 Key trends

- 8.2 Dental

- 8.2.1 Intraoral imaging

- 8.2.2 Extraoral imaging

- 8.3 Veterinary

- 8.3.1 Oncology

- 8.3.2 Orthopedics

- 8.3.3 Cardiology

- 8.3.4 Neurology

- 8.3.5 Other veterinary applications

- 8.4 Mammography

- 8.5 Chest

- 8.6 Cardiovascular

- 8.7 Orthopedics

- 8.8 Other applications

Chapter 9 Market Estimates and Forecast, By End Use, 2021 – 2032 ($ Mn)

- 9.1 Key trends

- 9.2 Hospitals

- 9.3 Ambulatory surgical centers

- 9.4 Specialty clinics

- 9.5 Other end use

Chapter 10 Market Estimates and Forecast, By Region, 2021 – 2032 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Vietnam

- 10.4.5 South Korea

- 10.4.6 Thailand

- 10.4.7 Oceania

- 10.4.8 Indonesia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 Egypt

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Agfa-Gevaert Group

- 11.2 Allengers Medical Systems

- 11.3 Canon

- 11.4 Carestream Health

- 11.5 Dentsply Sirona

- 11.6 Fujifilm Holdings Corporation

- 11.7 GE HealthCare Technologies

- 11.8 Hologic

- 11.9 Koninklijke Philips N.V.

- 11.10 Konica Minolta

- 11.11 Midmark

- 11.12 Neusoft Medical Systems

- 11.13 Perlong Medical Equipment

- 11.14 Samsung Electronics

- 11.15 Shimadzu

- 11.16 Siemens Healthineers

- 11.17 Trivitron Healthcare

醫用 X 光市場規模、佔有率、成長分析、按類型、按技術、按便攜性、按最終用途、按地區 - 按行業預測,2024-2031 年

醫用 X 光市場規模、佔有率、成長分析、按類型、按技術、按便攜性、按最終用途、按地區 - 按行業預測,2024-2031 年 X 光和 CT 計量解決方案市場:按技術、產品類型和應用分類 – 2025-2030 年全球預測

X 光和 CT 計量解決方案市場:按技術、產品類型和應用分類 – 2025-2030 年全球預測 脊椎 X 光和電腦斷層掃描市場:按適應症、患者類型和最終用戶 - 2025-2030 年全球預測

脊椎 X 光和電腦斷層掃描市場:按適應症、患者類型和最終用戶 - 2025-2030 年全球預測 醫用 X光發生器市場:按產品和應用分類的全球預測 - 2025-2030

醫用 X光發生器市場:按產品和應用分類的全球預測 - 2025-2030 2024年至2032年醫用X光市場機會、成長動力、產業趨勢分析與預測

2024年至2032年醫用X光市場機會、成長動力、產業趨勢分析與預測 醫用 X 光影像處理器市場機會、成長促進因素、產業趨勢分析與預測 2024 - 2032 年

醫用 X 光影像處理器市場機會、成長促進因素、產業趨勢分析與預測 2024 - 2032 年 X光系統的開發平台 - 開發階段,市場區隔,地區和國家,法規途徑,主要企業(2024年版)

X光系統的開發平台 - 開發階段,市場區隔,地區和國家,法規途徑,主要企業(2024年版) 手持式 X 光市場規模、佔有率和趨勢分析報告:按應用、按最終用途、按地區、細分市場預測,2024-2030 年

手持式 X 光市場規模、佔有率和趨勢分析報告:按應用、按最終用途、按地區、細分市場預測,2024-2030 年 醫療用X光市場分析·預測 (~2033年):各類型·產品·技術·用途·終端用戶·零組件·功能·安裝類型·服務

醫療用X光市場分析·預測 (~2033年):各類型·產品·技術·用途·終端用戶·零組件·功能·安裝類型·服務 移動 X 光圍裙架市場報告:2030 年趨勢、預測與競爭分析

移動 X 光圍裙架市場報告:2030 年趨勢、預測與競爭分析