|

市場調查報告書

商品編碼

1708214

醫藥冷鏈包裝市場機會、成長動力、產業趨勢分析及2025-2034年預測Pharmaceutical Cold Chain Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

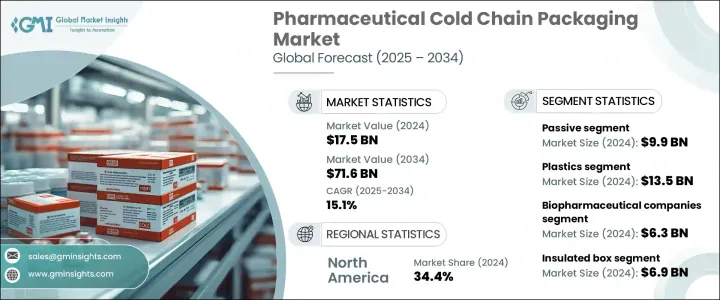

2024 年全球醫藥冷鏈包裝市場規模達 175 億美元,預估 2025 年至 2034 年期間的複合年成長率為 15.1%。這一成長主要得益於先進療法的日益普及,例如基於 mRNA 的治療、細胞療法和基因療法,這些療法需要在整個供應鏈中進行嚴格的溫度控制。隨著製藥公司增加產量以滿足對這些創新療法日益成長的需求,對可靠的冷鏈包裝解決方案的需求變得更加重要。冷鏈包裝確保對溫度敏感的藥物(包括生物製劑和疫苗)在從生產地運輸到最終用戶的過程中的安全性、穩定性和有效性。

此外,慢性病的增加和個人化醫療的日益成長趨勢也增加了對專門包裝解決方案的需求,以維持複雜生物製劑的效力。人們越來越重視在儲存和運輸過程中保持對溫度敏感的藥品的品質和合規性,這進一步促進了市場的擴張。監管審查的加強和遵守嚴格分銷協議的需要促使製造商投資先進的冷鏈包裝技術,確保產品安全和合規性。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 175億美元 |

| 預測值 | 716億美元 |

| 複合年成長率 | 15.1% |

醫藥冷鏈包裝市場按材料細分,主要類別為塑膠、金屬和紙張。 2024 年,塑膠產業的產值達到 135 億美元。塑膠的主導地位可以歸因於其優異的隔熱性能,這對於在運輸過程中維持所需的溫度至關重要。其重量輕且具有成本效益,使其成為旨在降低運輸成本同時保持產品完整性的製藥公司的理想選擇。塑膠材料以其耐用性和可擴展性而聞名,為確保生物製劑和其他敏感藥物的安全運輸提供了實用的解決方案。隨著對生物製劑的需求增加,對能夠在整個供應鏈中保持精確溫度控制的塑膠包裝的需求預計將成長,從而加強該領域在市場上的地位。

市場進一步依最終用戶分類,包括物流和配送中心、生物製藥公司、醫院、臨床研究組織、研究機構等。 2024 年生物製藥公司的收入為 63 億美元,反映了該領域的快速擴張。基因和 mRNA 療法的日益普及推動了對能夠保持敏感藥物的穩定性和功效的專用包裝解決方案的需求。嚴格的監管準則在推動對先進冷鏈包裝解決方案的需求方面發揮著至關重要的作用,這些解決方案可確保整個分銷過程符合安全標準。隨著生物製藥公司擴大生產能力,對可靠、高品質的冷鏈包裝的需求預計將上升,從而加強市場的上升趨勢。

2024 年,北美醫藥冷鏈包裝市場佔有 34.4% 的佔有率。該地區強勁的市場地位主要歸因於對生物製劑和細胞療法日益成長的需求,這些產品需要在儲存和運輸過程中進行嚴格的溫度管理。包括 FDA 在內的監管機構執行嚴格的指導方針,推動採用冷鏈包裝解決方案,確保藥品在整個供應鏈中保持其安全性、有效性和合規性。北美對精準醫療的日益重視和生物製劑產品組合的不斷擴大,增強了該地區在全球醫藥冷鏈包裝市場的地位。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 產業衝擊力

- 成長動力

- 生物製劑和特種藥物的需求不斷成長

- mRNA 和細胞/基因療法的擴展

- 嚴格的監管要求

- 電子商務和網路藥局的成長

- 製藥業的擴張

- 產業陷阱與挑戰

- 冷鏈基礎設施成本高

- 溫度超標和產品變質的風險

- 成長動力

- 成長潛力分析

- 監管格局

- 技術格局

- 未來市場趨勢

- 差距分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 策略儀表板

第5章:市場估計與預測:按材料,2021 - 2034 年

- 主要趨勢

- 塑膠

- 聚乙烯(PE)

- 聚丙烯(PP)

- 聚對苯二甲酸乙二酯(PET)

- 聚氨酯(PU)

- 其他

- 金屬

- 紙

第6章:市場估計與預測:按類型,2021 - 2034 年

- 主要趨勢

- 積極的

- 被動的

第7章:市場估計與預測:按產品,2021 - 2034 年

- 主要趨勢

- 保溫箱

- 容器

- 冷卻劑

- 托盤

- 其他

第8章:市場估計與預測:按最終用途產業,2021 - 2034 年

- 主要趨勢

- 生物製藥公司

- 臨床研究組織

- 醫院

- 研究機構

- 物流配送公司

- 其他

第9章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

第10章:公司簡介

- Chill-Pak

- Cold Chain Technologies

- CoolPac

- Cryopak

- CSafe

- Envirotainer

- Haier Biomedical

- Insulated Products Corporation

- Intelsius

- Nordic Cold Chain Solutions

- Sealed Air

- Smurfit Kappa

- Sofrigam Group

- Sonoco ThermoSafe

- Tessol

- Va-Q-Tec Thermal Solutions

- Vericool

The Global Pharmaceutical Cold Chain Packaging Market generated USD 17.5 billion in 2024 and is projected to grow at a CAGR of 15.1% between 2025 and 2034. This growth is primarily driven by the increasing adoption of advanced therapies, such as mRNA-based treatments, cell therapies, and gene therapies, which require strict temperature control throughout the supply chain. As pharmaceutical companies ramp up production to meet the rising demand for these innovative treatments, the need for reliable cold chain packaging solutions becomes more critical. Cold chain packaging ensures the safety, stability, and efficacy of temperature-sensitive drugs, including biologics and vaccines, during transportation from manufacturing sites to end users.

Additionally, the rise in chronic diseases and the growing trend of personalized medicine have heightened the need for specialized packaging solutions to maintain the potency of complex biologics. The growing focus on maintaining the quality and compliance of temperature-sensitive pharmaceutical products during storage and transit further contributes to the market's expansion. Increased regulatory scrutiny and the need to adhere to strict distribution protocols push manufacturers to invest in advanced cold chain packaging technologies, ensuring product safety and compliance.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $17.5 Billion |

| Forecast Value | $71.6 Billion |

| CAGR | 15.1% |

The pharmaceutical cold chain packaging market is segmented by material, with plastic, metal, and paper being the primary categories. The plastic segment generated USD 13.5 billion in 2024. Plastic's dominance can be attributed to its superior thermal insulation properties, which are essential for maintaining the required temperatures during transit. Its lightweight nature and cost-effectiveness make it an ideal choice for pharmaceutical companies aiming to reduce shipping costs while preserving product integrity. Plastic materials, known for their durability and scalability, provide a practical solution for ensuring the safe transportation of biologics and other sensitive drugs. As the demand for biologics increases, the need for plastic packaging that can maintain precise temperature control throughout the supply chain is expected to grow, strengthening the segment's position in the market.

The market is further categorized by end users, including logistics and distribution centers, biopharmaceutical companies, hospitals, clinical research organizations, research institutes, and others. Biopharmaceutical companies generated USD 6.3 billion in 2024, reflecting the rapid expansion of this segment. The growing adoption of gene and mRNA therapies has fueled the demand for specialized packaging solutions capable of preserving the stability and efficacy of sensitive pharmaceuticals. Strict regulatory guidelines play a crucial role in driving the need for advanced cold chain packaging solutions that ensure compliance with safety standards throughout the distribution process. As biopharmaceutical companies expand their production capabilities, the demand for reliable and high-quality cold chain packaging is expected to rise, reinforcing the market's upward trajectory.

North America's pharmaceutical cold chain packaging market held a 34.4% share in 2024. The region's strong market presence is largely attributed to the growing demand for biologics and cell therapies, which require stringent temperature management during storage and transportation. Regulatory authorities, including the FDA, enforce strict guidelines that drive the adoption of cold chain packaging solutions, ensuring that pharmaceutical products maintain their safety, efficacy, and compliance throughout the supply chain. The increasing emphasis on precision medicine and the expanding portfolio of biologics in North America contribute to the region's stronghold in the global pharmaceutical cold chain packaging market.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for biologics & specialty drugs

- 3.2.1.2 Expansion of mRNA & cell/gene therapies

- 3.2.1.3 Stringent regulatory requirement

- 3.2.1.4 Growth of e-commerce and online pharmacies

- 3.2.1.5 Expansion of the pharmaceutical industry

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High costs of cold chain infrastructure

- 3.2.2.2 Risk of temperature excursions & product spoilage

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Material, 2021 - 2034 (USD Billion & Kilo Tons)

- 5.1 Key trends

- 5.2 Plastics

- 5.2.1 Polyethylene (PE)

- 5.2.2 Polypropylene (PP)

- 5.2.3 Polyethylene Terephthalate (PET)

- 5.2.4 Polyurethane (PU)

- 5.2.5 Others

- 5.3 Metal

- 5.4 Paper

Chapter 6 Market Estimates and Forecast, By Type, 2021 - 2034 (USD Billion & Kilo Tons)

- 6.1 Key trends

- 6.2 Active

- 6.3 Passive

Chapter 7 Market Estimates and Forecast, By Product, 2021 - 2034 (USD Billion & Kilo Tons)

- 7.1 Key trends

- 7.2 Insulated box

- 7.3 Containers

- 7.4 Coolants

- 7.5 Pallets

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By End Use Industry, 2021 - 2034 (USD Billion & Kilo Tons)

- 8.1 Key trends

- 8.2 Biopharmaceutical companies

- 8.3 Clinical research organizations

- 8.4 Hospitals

- 8.5 Research institutes

- 8.6 Logistics and distribution companies

- 8.7 Others

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion & Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Chill-Pak

- 10.2 Cold Chain Technologies

- 10.3 CoolPac

- 10.4 Cryopak

- 10.5 CSafe

- 10.6 Envirotainer

- 10.7 Haier Biomedical

- 10.8 Insulated Products Corporation

- 10.9 Intelsius

- 10.10 Nordic Cold Chain Solutions

- 10.11 Sealed Air

- 10.12 Smurfit Kappa

- 10.13 Sofrigam Group

- 10.14 Sonoco ThermoSafe

- 10.15 Tessol

- 10.16 Va-Q-Tec Thermal Solutions

- 10.17 Vericool

低溫運輸包裝市場規模、佔有率、成長分析(按產品、材料類型、應用和地區)-2025-2032 年產業預測低溫運輸包裝市場:按產品類型、應用和地區

低溫運輸包裝市場規模、佔有率、成長分析(按產品、材料類型、應用和地區)-2025-2032 年產業預測低溫運輸包裝市場:按產品類型、應用和地區 2025 年低溫運輸包裝全球市場報告

2025 年低溫運輸包裝全球市場報告 美國低溫運輸包裝市場規模、佔有率、趨勢分析報告:按產品、材料、應用和細分市場預測,2025-2030

美國低溫運輸包裝市場規模、佔有率、趨勢分析報告:按產品、材料、應用和細分市場預測,2025-2030 低溫運輸包裝市場:依產品類型、最終用途產業、材料類型、技術 - 2025-2030 年全球預測2024-2032年冷鏈包裝市場機會、成長動力、產業趨勢分析與預測低溫運輸包裝市場規模、佔有率和趨勢分析報告:按材料、按類型、按產品類型、按最終用途、按地區、按細分市場、預測,2024-2030 年2024-2032 年按產品(隔熱容器和盒子、板條箱、冷包裝、標籤、溫控托盤托運商)、最終用戶(食品、乳製品、藥品等)和地區分類的冷鏈包裝市場報告2030 年低溫運輸包裝市場預測:按產品、材料、應用和地區分類的全球分析

低溫運輸包裝市場:依產品類型、最終用途產業、材料類型、技術 - 2025-2030 年全球預測2024-2032年冷鏈包裝市場機會、成長動力、產業趨勢分析與預測低溫運輸包裝市場規模、佔有率和趨勢分析報告:按材料、按類型、按產品類型、按最終用途、按地區、按細分市場、預測,2024-2030 年2024-2032 年按產品(隔熱容器和盒子、板條箱、冷包裝、標籤、溫控托盤托運商)、最終用戶(食品、乳製品、藥品等)和地區分類的冷鏈包裝市場報告2030 年低溫運輸包裝市場預測:按產品、材料、應用和地區分類的全球分析 全球藥品冷鏈包裝市場研究報告 - 2024 年至 2032 年產業分析、規模、佔有率、成長、趨勢與預測

全球藥品冷鏈包裝市場研究報告 - 2024 年至 2032 年產業分析、規模、佔有率、成長、趨勢與預測