|

市場調查報告書

商品編碼

1524118

量子點(QD):市場佔有率分析、產業趨勢/統計、成長預測(2024-2029)Quantum Dots - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

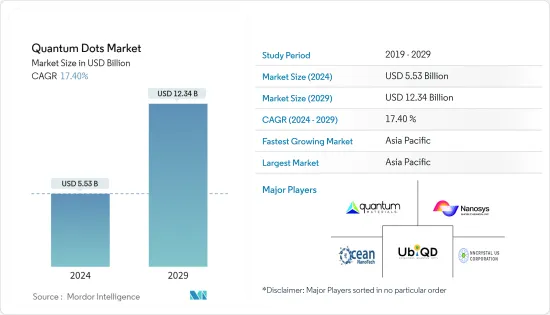

量子點(QD)市場規模預計到 2024 年為 55.3 億美元,預計到 2029 年將達到 123.4 億美元,在預測期內(2024-2029 年)複合年成長率為 17.40%。

量子點(QD)是具有動態特性的奈米級半導體顆粒。這些微結構通常由硒化鎘等材料製成,可以吸收和發射特定波長的光,這使得它們在電子、醫學影像處理和顯示器等應用中具有價值。量子點 (QD) 的尺寸依賴性電子特性使得能夠精確控制其光學和電子特性。

*量子點 (QD) 表現出獨特的光學特性,包括尺寸依賴性螢光和在特定波長下發光的能力。這使得它們在需要精確色彩控制的應用中非常有用,例如顯示器和照明。此外,這些半導體量子點 (QD) 的獨特成分、可調特性和尺寸為其在各種應用和新技術中的應用帶來了巨大的希望。

*在農業領域,可以製造光轉換塗層,預計將提高溫室果樹的產量和成熟速度。荷蘭農民擴大採用室內種植,先進的溫室使用 LED 照明,可以在更小的空間內更快地種植更多作物。

*量子點(QD)輔助顯示是最新技術之一。它能夠產生更鮮豔的色彩並為現代顯示器帶來靈活性,預計將推動更多的採用。量子點獨特的與尺寸相關的光學、電子、化學和光電特性使其非常適合現代顯示器,因為它們具有更高的功率效率、更寬的色域和更低的屏障保護要求。

*然而,由於照明解決方案成本高昂,量子點 (QD) 技術的成長僅限於高階應用。量子點 (QD) 技術無法與 LED 等其他更便宜的技術競爭。此外,與 OLED 相比,對比度較低和視角較差等技術限制也阻礙了研究市場的成長。

*COVID-19疫情對電子產業的成長產生了重大影響。疫情爆發初期,擾亂了產業供應鏈,部分地區製造商難以業務永續營運。疫情引發的消費性電子和運算產品的激增推動了對顯示產品和 LED 的需求,這在量子點 (QD) 市場上也很明顯。隨著數位解決方案的採用預計將繼續成長,預測期內接受調查的市場也預計將出現向上成長。

量子點(QD)市場趨勢

光電子和光學元件顯著成長

- 量子點 (QD) 顯示器已成為傳統液晶顯示器 (LCD) 的有前途的替代品。透過採用量子點作為顏色轉換材料,這些顯示器可以實現寬色域、更高的亮度和更高的能源效率。採用量子點 (QD) 增強的 LCD 可提供更明亮、更準確的色彩,適合電視、顯示器和行動裝置中的高品質成像。

- 量子點 (QD) 也徹底改變了照明領域,主要是在下一代發光二極體(LED) 的開發方面。透過利用量子點作為降壓轉換器,白光 LED 可以獲得更高的顯色指數 (CRI) 值和更好的色彩品質。與傳統磷光體LED 相比,量子點 (QD) LED 具有更寬的色域、更高的效率和更長的使用壽命。這些進步為家庭、辦公室和城市環境中的節能照明解決方案鋪平了道路。

- 根據IEA統計,LED在國際照明市場的滲透率正顯著提高,預計2025年將達到76%,2030年將達到87.4%。 LED 也是透過光纖通訊系統傳輸資訊的重要 IT 和通訊雷射。

- 奈米級半導體裝置有望成為下一代高度整合和高功能的技術。量子點 (QD) 由於其量子限制而表現出獨特的特性。這種獨特的特性引起了人們對量子點(QD)在光電應用中潛力的關注。人們正在對這些有利的奈米材料進行大量努力,以強調下一代光電元件(例如雷射、LED、檢測器、放大器和太陽能電池)的增強性能和功能。

亞太地區預計將佔據主要市場佔有率

- 中國對半導體製造和量子計算研究的投資為量子點(QD)提供了潛在的成長機會。量子點(QD)具有推進半導體技術並為量子電腦的發展做出貢獻的潛力。

- 中國在量子技術特別是量子通訊方面取得了長足進展。瓦查納在量子計算的某些方面落後於美國。其科學家取得了令人矚目的成果,並且正在取得快速進展。近年來,量子雷達和量子感測器的進展不斷湧現,體現了中國對量子技術的承諾。

- 量子點(QD)技術及其應用的重大進步推動了日本量子點(QD)的成長。例如,國家資訊通訊技術研究所光子網路研究所的研究人員開發了一種使用高品質量子點(QD)的新光源技術。與使用傳統方法製造的量子點(QD)相比,量子點(QD)表現出更高的穩定性和光學頻率,在各個領域開闢了潛在的應用前景。

- 日本 NITC 已完成研究,讓光纖網路在新的頻譜區域使用量子點 (QD)。透過應用量子點(QD)生長的新方法,我們成功實現了開拓頻寬的光資料傳輸,展現了擴展光纖網路能力的潛力。

量子點 (QD) 產業概覽

量子點(QD)市場正在走向半固體,應用數量也在增加,預計在預測期內市場滲透水平將會成長。主要供應商的業務遍及全球,這幫助他們獲得了可觀的市場佔有率。市場主要企業包括Nanosys Inc.(Shoei Electronic Materials Inc.)、NnCrystal US Corporation(NN-Labs)、Quantum Materials Corporation、UbiQD Inc.、Ocean NanoTech.等。每個企業都致力於透過策略合作來增加市場佔有率並增強盈利。

*2024 年 2 月 - Quantum Solutions 宣佈在 200mm 矽 ROIC(讀出積體電路)晶圓上成功展示 QDot PbS 量子點 (QD) n 型墨水的晶圓級沉積。這項突破凸顯了在 200mm 晶圓平台上製造高通量 SWIR(短波長紅外線)影像感測器的可行性,這對於大規模感測器製造至關重要。

*2023 年 11 月 - Nanoco 集團與一家領先的亞洲化學合作夥伴簽訂了兩項協議,以最佳化 Nanoco 用於紅外線感測應用的第二代量子點(QD) 材料並擴大生產規模。的年度共同開發契約(JDA)。這是該公司成為感測市場奈米材料商業性供應商的最新里程碑,並支持其 2024 會計年度的前景。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場洞察

- 市場概況

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 買方議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

- COVID-19 和其他宏觀經濟因素對市場的影響

第5章市場動態

- 市場促進因素

- 高品質顯示設備對量子點 (QD) 的需求增加

- 對節能解決方案的需求不斷成長

- 市場挑戰

- 對生物應用中細胞毒性的擔憂

第6章 市場細分

- 按類型

- III-V族半導體

- II-VI族半導體

- 矽(Si)

- 按用途

- 光電/光學元件

- 醫療保健

- 農業

- 替代能源

- 其他

- 按地區

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 其他亞太地區

- 其他地區(拉丁美洲、中東、非洲)

- 北美洲

第7章 競爭格局

- 供應商定位分析

- 公司簡介

- Nanosys Inc.(Shoei Electronic Materials Inc)

- NnCrystal US Corporation(NN-Labs)

- Quantum Materials Corporation

- UbiQD Inc.

- Ocean NanoTech

- Thermo Fisher Scientific Inc.

- Nanoco Group PLC.

- NanoOptical Materials Inc

- Merck KGaA

- Quantum Solutions Inc.

第8章投資分析

第9章 市場機會及未來趨勢

The Quantum Dots Market size is estimated at USD 5.53 billion in 2024, and is expected to reach USD 12.34 billion by 2029, growing at a CAGR of 17.40% during the forecast period (2024-2029).

Quantum dots are nanoscale semiconductor particles that exhibit quantum mechanical properties. These tiny structures, typically composed of materials like cadmium selenide, can absorb and emit light at specific wavelengths, making them valuable for applications in electronics, medical imaging, and displays. Their size-dependent electronic characteristics allow precise control over their optical and electronic properties.

* Quantum dots exhibit unique optical properties, such as size-dependent fluorescence and the ability to emit specific wavelengths of light. This makes them valuable in applications like displays and lighting, where precise color control is essential. In addition, the unique composition, tunable property, and size of these semiconducting quantum dots make them highly appealing for a wide variety of applications and new technologies.

* In agriculture, it is possible to create light-converting coatings, which are anticipated to increase yield and the speed of maturation of fruit plants in greenhouses. Dutch farmers are increasingly adopting indoor farming, and they can cultivate more crops faster and in a smaller space with advanced greenhouses using LED lights.

* Quantum dot (QD) assisted displays are among the newest technology additions. The adoption is anticipated to grow due to their ability to produce more vivid colors and bring flexibility to modern displays. The unique size-dependent optical, electronic, chemical, and optoelectronic features of QDs make them highly suitable for modern displays owing to their higher power efficiency and wide color gamut with lower barrier protection requirements.

* However, the high costs of lighting solutions have restricted the growth of quantum dot technology to be used only in high-end applications. They are unable to compete with other cheaper technologies, like LEDs. Additionally, technical limitations such as lower contrast ratio and poor viewing angle in comparison to OLEDs also continue to challenge the studied market's growth.

* The outbreak of COVID-19 has had a notable impact on the growth of the electronics industry. The initial pandemic outbreak disrupted the industry's supply chain, making it difficult for manufacturers to continue their operations in some areas. A pandemic-led growth in the adoption of consumer electronic and computing products drove the demand for display products and LEDs, which was also evident in the quantum dots market. With the adoption of digital solutions anticipated to continue to grow, the market studied will also witness upward growth during the forecast period.

Quantum Dots Market Trends

Optoelectronics and Optical Components to Witness Significant Growth

- Quantum dot displays have emerged as a promising alternative to traditional liquid crystal displays (LCDs). By incorporating QDs as color-converting materials, these displays can achieve a wider color gamut, enhanced brightness, and improved energy efficiency. Quantum dot-enhanced LCDs deliver vibrant and more accurate colors, making them suitable for high-quality imaging in televisions, monitors, and mobile devices.

- Quantum dots have also revolutionized the lighting field, mainly in developing next-generation light-emitting diodes (LEDs). By utilizing QDs as down-converters, white LEDs can achieve higher color rendering index (CRI) values and better color quality. Quantum dot LEDs offer a wider range of colors, improved efficiency, and longer lifetimes than conventional phosphor-based LEDs. These advancements have paved the way for energy-efficient lighting solutions in homes, offices, and urban environments.

- LEDs also form a crucial part of the optical fiber communication systems for transmitting data through modulated light; according to IEA, the penetration rate of LEDs into the international lighting market is rising considerably; it is expected to reach 76% by 2025 and 87.4% by 2030, and these LEDs are also telecommunication lasers, vital in transmitting information through optical communication systems.

- Nanometer-scale semiconductor devices have been predicted as next-generation technologies with high integration and functionality. Quantum dots exhibit unique properties due to their quantum confinement. These unique properties have brought to light the potential of quantum dots in optoelectronic applications. Numerous efforts have been dedicated to these favorable nanomaterials for next-generation optoelectronic components, such as lasers, LEDs, photodetectors, amplifiers, and solar cells, highlighting enhancing performance and functionality.

Asia-Pacific is Expected to Hold Significant Market Share

- China's investments in semiconductor manufacturing and quantum computing research offer potential growth opportunities for quantum dots. Quantum dots have the potential to advance semiconductor technologies and contribute to the development of quantum computers.

- China has made huge advances in quantum technologies, particularly in quantum communication. Vachana is behind the United States in some aspects of quantum computing. Its scientists have made eye-catching achievements and are progressing rapidly. In recent years, there have been reports of advancements in quantum radar and quantum sensors, showcasing China's commitment to quantum technology.

- The growth of quantum dots in Japan has been driven by significant advancements in quantum dot technology and its application. For instance, researchers at the Photonic Network Research Institute of Japan's National Institute of Information and Communication Technology have developed a new light source technology using high-quality quantum dots. These quantum dots exhibit higher stability and optical frequency than those created using conventional methods, paving the way for potential application in various fields.

- Japan's NITC completes research that could allow fiber optics networks to use quantum dots in new areas of the spectrum. Researchers have successfully transmitted optical data in an untapped frequency band by applying a new approach to quantum dot growth, showing the potential to expand fiber optic network capabilities.

Quantum Dots Industry Overview

The quantum dots market is semi-consolidated and has an increasing number of applications, and the level of market penetration is expected to grow during the forecast period. Major vendors have a global presence, which helps them to gain a substantial market share. Key players in the market include Nanosys Inc. (Shoei Electronic Materials Inc.), NnCrystal US Corporation (NN-Labs), Quantum Materials Corporation, UbiQD Inc., Ocean NanoTech., etc. The businesses are leveraging strategic collaborative actions to improve their market percentage and enhance profitability.

* February 2024 - Quantum Solutions announced the booming demonstration of wafer-level deposition of QDot PbS quantum dot n-type ink on a 200 mm silicon ROIC (read-out integrated circuit) wafer. This groundbreaking work highlights the feasibility of producing SWIR (short-wave infrared) image sensors with high throughput on 200 mm wafer platforms, which is essential for large-scale manufacturing of sensors.

* November 2023 - Nanoco Group has signed a new two-year joint development agreement (JDA) with its existing major Asian chemical partner to optimize and scale up the production of Nanoco's second-generation quantum dot materials for infrared sensing applications. This marks the company's latest milestone in becoming a commercial provider of nanomaterials to the sensing market and supports its FY24 forecasts.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Degree of Competition

- 4.3 Impact of COVID-19 Aftereffects and Other Macroeconomic Factors on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Demand for Quantum Dots in High-Quality Display Devices

- 5.1.2 Growing Demand for Energy-efficient Solutions

- 5.2 Market Challenges

- 5.2.1 Concerns Regarding the Toxicity of Cells in Biological Applications

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 III-V-Semiconductors

- 6.1.2 II-VI-Semiconductors

- 6.1.3 Silicon (Si)

- 6.2 By Application

- 6.2.1 Optoelectronics and Optical Components

- 6.2.2 Medicine

- 6.2.3 Agriculture

- 6.2.4 Alternative Energy

- 6.2.5 Other Applications

- 6.3 By Geography

- 6.3.1 North America

- 6.3.1.1 United States

- 6.3.1.2 Canada

- 6.3.2 Europe

- 6.3.2.1 United Kingdom

- 6.3.2.2 Germany

- 6.3.2.3 France

- 6.3.2.4 Rest of Europe

- 6.3.3 Asia-Pacific

- 6.3.3.1 China

- 6.3.3.2 Japan

- 6.3.3.3 India

- 6.3.3.4 Rest of Asia-Pacific

- 6.3.4 Rest of the World (Latin America and Middle East and Africa)

- 6.3.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Vendor Positioning Analysis

- 7.2 Company Profiles*

- 7.2.1 Nanosys Inc. (Shoei Electronic Materials Inc)

- 7.2.2 NnCrystal US Corporation (NN-Labs)

- 7.2.3 Quantum Materials Corporation

- 7.2.4 UbiQD Inc.

- 7.2.5 Ocean NanoTech

- 7.2.6 Thermo Fisher Scientific Inc.

- 7.2.7 Nanoco Group PLC.

- 7.2.8 NanoOptical Materials Inc

- 7.2.9 Merck KGaA

- 7.2.10 Quantum Solutions Inc.

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

量子點市場:按類型、產品、應用分類 - 2025-2030 年全球預測

量子點市場:按類型、產品、應用分類 - 2025-2030 年全球預測 量子點濃縮物市場報告:趨勢、預測和競爭分析(至 2030 年)

量子點濃縮物市場報告:趨勢、預測和競爭分析(至 2030 年) 量子點市場、佔有率、市場規模、趨勢、行業分析報告:按類型、按應用、按產品、按地區 - 2025-2034 年市場預測

量子點市場、佔有率、市場規模、趨勢、行業分析報告:按類型、按應用、按產品、按地區 - 2025-2034 年市場預測 2024 年量子點全球市場報告

2024 年量子點全球市場報告 雷射量子點市場報告:2030 年趨勢、預測與競爭分析

雷射量子點市場報告:2030 年趨勢、預測與競爭分析 量子點的全球市場規模:各材料類型,各終端用戶,各地區,範圍及預測

量子點的全球市場規模:各材料類型,各終端用戶,各地區,範圍及預測 量子點市場:按材料、產品、顯示器、生產技術、產業、地區分類 - 預測至 2029 年

量子點市場:按材料、產品、顯示器、生產技術、產業、地區分類 - 預測至 2029 年 量子點市場,依產品類型、依材料類型、依製造程序、依最終用戶、依國家和地區 - 2024-2032 年行業分析、市場規模、市場佔有率和預測

量子點市場,依產品類型、依材料類型、依製造程序、依最終用戶、依國家和地區 - 2024-2032 年行業分析、市場規模、市場佔有率和預測 2024-2032 年按加工技術、應用、材料、最終用途產業和地區分類的量子點市場報告

2024-2032 年按加工技術、應用、材料、最終用途產業和地區分類的量子點市場報告 2024-2028年全球量子點市場

2024-2028年全球量子點市場