|

市場調查報告書

商品編碼

1851339

穿戴式健康感測器:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)Wearable Health Sensors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

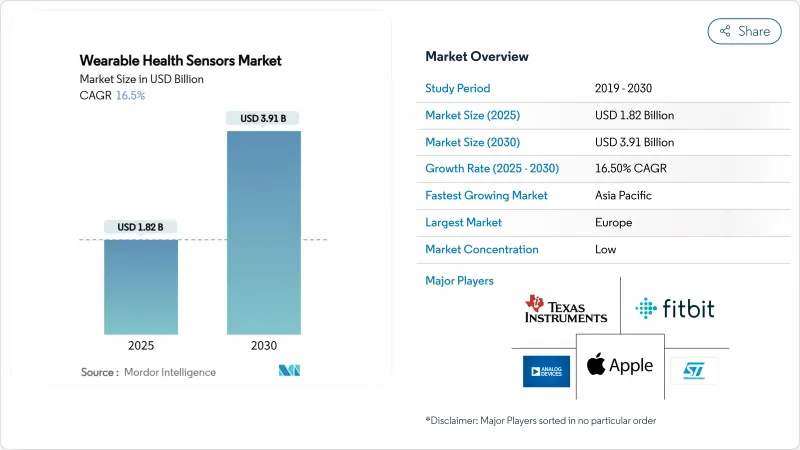

預計到 2025 年,穿戴式健康感測器市場規模將達到 18.2 億美元,到 2030 年將達到 39.1 億美元,年複合成長率為 16.5%。

隨著支付方和醫療服務提供者看到早期療育帶來的顯著成本節約,需求正從間歇性照護轉向持續監測。小型感測器結合低功耗藍牙、LTE-M 和 NB-IoT 技術,在將臨床級資料傳輸到安全雲平台的同時,保持了低功耗。北美地區受惠於遠端患者監護(RPM) 的報銷政策,推動了相關技術的應用;而印刷生物貼片的成本創新則拓展了其在歐洲和亞洲的應用。競爭的焦點在於非侵入式血糖檢測、與膚色無關的光學感測以及能夠在不影響電池壽命的前提下提高精度的混合 MEMS-光學堆疊。晶片供應商和設備品牌之間的夥伴關係正在加速多參數穿戴式裝置在消費、臨床和工業領域的上市。

全球穿戴式健康感測器市場趨勢與洞察

獲得FDA批准的遠端患者監護線纜加速了美國處方箋級穿戴設備的發展

簡化遠端患者監護 (RPM) 計費流程已將強制性的 30 天週期從 16 天縮短至 12 天,從而釋放了每年 51 億美元的設備資金。現在,醫療服務提供者每年每位患者最多可獲得 1,400 美元,用於購買企業級感測器平台,而非零售設備。一家大型醫療系統已組建專門的 RPM 團隊,並擴大了智慧型手錶可與相關貼片和電子病歷 (EHR) 控制面板配合使用。慢性病患者的再入院率下降了 30%,這增強了支付方的支持力道。

亞洲各國強制推行慢性病篩檢,推動了連續血壓監測儀和動態血糖監測套件的普及。

中國在最新的五年規劃中累計87億美元用於糖尿病和高血壓篩檢,設備需求年增率達22.3%。日本強制要求40歲以上公民每年進行心血管疾病篩檢,並將穿戴式感測器納入全民醫療保險。這些項目將產生用於人工智慧決策支援的縱向資料集,同時在全部區域推廣居家診斷。

歐盟醫療器材法規 (EU MDR) IIa 類軟體即醫療器材上市後監管的延誤

分析型穿戴裝置的平均核准時間從7個月增加到19個月,新興企業的遵循成本增加了280%。許多公司推遲了在歐盟的上市計劃,或轉向健康標籤,這延緩了臨床級穿戴式設備在各地區的上市時間;而規模較小的公司則尋求擴大規模以分攤監管成本,從而推動了行業整合。

細分市場分析

到2024年,加速計和慣性MEMS感測器將佔據32.4%的市場佔有率,憑藉其在追蹤身體多個部位運動模式方面的多功能性,它們將成為穿戴式健康感測器生態系統的基礎。這些感測器的功能正在從簡單的步數計數發展到能夠進行高級步態分析和跌倒檢測,這在老年護理應用中尤其重要。光學/光電容積脈搏波描記法(PPG)感測器預計將在2025年至2030年間以13.4%的最快速度成長,這主要得益於其功能不斷擴展,從心率監測擴展到血氧飽和度、血壓估算,甚至早期血糖監測應用。溫度感測器在連續發熱監測系統中重新煥發活力,而壓力感測器則擴大應用於智慧鞋類,以預防糖尿病足潰瘍。

將多種感測器整合到單一裝置中代表著市場發展的重大變革,其中混合磁感測器感測器和光學感測器的組合在改善心血管監測方面展現出尤為廣闊的應用前景。越南國家大學的最新研究表明,結合這些感測器可以克服光學感測器在檢測細微心血管異常方面的局限性,從而有望實現對諸如房顫等疾病的早期療育。電化學生物感測器在汗液分析等特定應用中日益普及,例如用於水合狀態監測。同時,位置感測器和接近感測器能夠提供情境感知訊息,透過校正身體姿勢和運動的影響,提高其他感測器讀數的準確性。

腕戴式設備憑藉其消費者熟悉度高、外形規格成熟以及能夠在一個易於取用的位置整合多種感測器等優勢,將在2024年繼續保持45%的市場佔有率。這種部署方式的戰略優勢在於平衡用戶接受度和感測器精度,蘋果和三星等領先公司正利用其智慧型手錶平台推出日益複雜的健康監測功能。智慧服飾和紡織品將以15.2%的複合年成長率(2025-2030年)實現最快成長,因為軟性電子和導電材料的創新使得感測器能夠無縫整合到日常服裝中,而不會影響舒適度或耐洗性。

胸貼和皮膚穿戴式感測器在臨床應用中日益普及,它們能夠為慢性病患者提供持續監測功能,同時保持隱藏。不列顛哥倫比亞大學開發了一種低成本的壓阻式感測器,可嵌入紡織品中,用於監測人體運動,包括心率和體溫。穿戴式頭戴裝置和眼鏡產品在神經監測和擴增實境(AR)健康介面等領域找到了專門的應用。同時,鞋類感測器能夠提供關於步態模式和體重分佈的獨特見解,使其在糖尿病治療和運動表現分析方面具有特別重要的價值。植入式和可攝入式感測器的興起代表著市場前沿,它們能夠提供前所未有的監測精度,但在監管和使用者接受度方面面臨著巨大的挑戰。

穿戴式健康感測器市場按感測器類型(壓力感測器、溫度感測器及其他)、配戴方式/外形規格(腕帶、胸貼及其他)、應用領域(生命徵象監測及其他)、最終用戶(醫療服務提供者及其他)、連接方式(藍牙、Wi-Fi及其他)和地區(北美及其他)進行細分。市場規模和預測均以美元計價。

區域分析

預計到2024年,北美將以38.71%的營收佔有率引領穿戴式健康感測器市場。遠距病患監護(RPM)報銷的廣泛普及、人均醫療保健成本的不斷上漲以及日益完善的生態系統正在刺激醫療機構的需求。美國醫療保險和醫療補助服務中心(CMS)允許醫療機構每年向每位接受監測的慢性病患者收取約1400美元的費用,這使得此類設備從消費級新奇產品轉變為臨床醫療資產。加拿大正在將遠端醫療擴展到偏遠省份,而墨西哥的社會安全體係正在試行為糖尿病持續監測(CGM)提供補貼。

到2030年,亞太地區將以13.8%的複合年成長率實現最快成長速度。中國的國家健康篩檢預算推動了連續血壓監測儀和血糖感測器的批量採購,同時本土半導體製造商也在擴大光晶片組的生產規模。日本的超老化社會將防跌倒和心律不整套件納入社區診所。印度的中產階級開始使用中階健身手環,而政府基層醫療中心則在測試穿戴式生命徵象監測亭。韓國利用其代工技術,為全球品牌提供MEMS和ASIC核心。

歐洲的貢獻舉足輕重,但卻面臨醫療器材法規 (MDR) 的阻力。德國和法國正在為透過其 DiGA 或 PACTe 門戶網站提交的數位療法提供報銷,鼓勵進行心臟衰竭和慢性阻塞性肺病 (COPD) 監測的臨床試驗。德國、荷蘭和英國的印刷電子中心正在降低貼片的成本,並幫助醫院證明一次性感測器的合理性。然而,MDR 的上市後限制正在減緩 IIa 類軟體的推廣,導致一些新興企業優先考慮在美國發布產品。在中東的油氣產業勞動力計畫中,該技術的應用正在加速推進;而在非洲,其應用能否成功取決於能否解決膚色較深人群在光電容積脈搏波描記法 (PPG) 的準確性和連接性方面存在的不足。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 獲得FDA批准的遠端患者監護線纜加速了美國處方箋級穿戴裝置的普及

- 亞洲強制慢性病篩檢推動了持續血壓/動態血壓監測套件的使用

- 在歐洲擴大印刷軟性生物貼片的生產規模,可將單位成本降低至1美元以下。

- 精英運動聯盟採用人工智慧驅動的傷病預防穿戴設備

- 海灣合作理事會油氣作業中的工人安全防熱疲勞計劃

- 非侵入式光學血糖感測器的創業融資激增

- 市場限制

- 歐盟醫療器材法規 (EU MDR) IIa 類軟體即醫療器材上市後監管的延誤

- 超小型貼片電池能量密度的限制

- PPG在非洲/加勒比海國家的召回:膚色差異導致準確性差距

- 巴西和哥倫比亞資料主權合規的成本

- 價值/供應鏈分析

- 監理與技術展望

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 技術概覽(感測器小型化、印刷及軟性電子產品)

第5章 市場規模與成長預測

- 依感測器類型

- 壓力感測器

- 溫度感測器

- 加速計/慣性MEMS

- 光學/PPG感測器

- 生物感測器(電化學)

- 陀螺儀和磁力計

- 位置和接近感測器

- 其他

- 透過佩戴位置/外形規格

- 腕錶

- 頭飾和眼鏡產品

- 胸部貼片和皮膚黏合劑

- 鞋類和鞋墊

- 智慧服飾/紡織品

- 植入式和可攝入式感測器

- 透過使用

- 生命徵象監測

- 慢性病管理(糖尿病、心血管疾病)

- 運動與健身表現

- 遠端患者監護和老年護理

- 心理健康與壓力追蹤

- 工人安全和環境暴露

- 最終用戶

- 醫療保健提供者和醫院

- 消費性電子品牌

- 運動隊伍/健身中心

- 軍人和初期應變人員

- 家庭護理服務提供者

- 透過連接技術

- Bluetooth/BLE

- Wi-Fi

- NFC/RFID

- 蜂窩網路(LTE-M/NB-IoT)

- 超寬頻(UWB)

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 歐洲

- 北歐國家

- 瑞典

- 挪威

- 丹麥

- 芬蘭

- 西歐

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 荷蘭

- 東歐

- 波蘭

- 俄羅斯

- 其他歐洲

- 中東

- 海灣合作理事會(沙烏地阿拉伯、阿拉伯聯合大公國、卡達、科威特、巴林、阿曼)

- 土耳其

- 其他中東地區

- 非洲

- 南非

- 奈及利亞

- 肯亞

- 其他非洲地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 東協(印尼、馬來西亞、泰國、越南、菲律賓、新加坡)

- 亞太其他地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略性舉措(併購、資金籌措、夥伴關係)

- 市佔率分析

- 公司簡介

- Apple Inc.

- Alphabet Inc.(Fitbit)

- TE Connectivity Ltd.

- STMicroelectronics NV

- Texas Instruments Inc.

- Analog Devices Inc.

- TDK Corporation

- Infineon Technologies AG

- NXP Semiconductors NV

- Maxim Integrated Products Inc.

- Abbott Laboratories

- Medtronic plc

- Dexcom Inc.

- Garmin Ltd.

- Omron Corporation

- Masimo Corporation

- Huawei Technologies Co. Ltd.

- Samsung Electronics Co. Ltd.

- Robert Bosch GmbH

- Valencell Inc.

第7章 市場機會與未來展望

The wearable health sensors market is valued at USD 1.82 billion in 2025 and is forecast to reach USD 3.91 billion by 2030, advancing at a 16.5% CAGR.

Demand is shifting from episodic care toward continuous monitoring as payers and providers see clear cost savings from early intervention. Miniaturized sensors paired with Bluetooth Low Energy, LTE-M, and NB-IoT keep power draw low while moving clinical-grade data into secure cloud platforms. North American adoption benefits from Remote Patient Monitoring (RPM) reimbursements, while cost breakthroughs in printed bio-patches expand use in Europe and Asia. Competitive activity centers on non-invasive glucose detection, skin-tone agnostic optical sensing, and hybrid MEMS-optical stacks that raise accuracy without harming battery life. Partnerships between silicon vendors and device brands are accelerating time-to-market for multi-parameter wearables across consumer, clinical, and industrial settings.

Global Wearable Health Sensors Market Trends and Insights

FDA-reimbursed Remote Patient Monitoring codes accelerating U.S. prescription-grade wearables

RPM billing simplification that cut mandatory capture from 16 to 12 days per 30-day cycle unlocked a USD 5.1 billion annual device pool. Providers now receive up to USD 1,400 per patient yearly, funding enterprise-grade sensor platforms over retail gadgets. Major health systems formed dedicated RPM teams, expanding procurement pipelines for validated patches and smartwatches that feed EHR dashboards. Hospital readmission rates for chronic patients have fallen 30%, reinforcing payer support.

National chronic-disease screening mandates in Asia driving continuous BP and CGM kits

China earmarked USD 8.7 billion for diabetes and hypertension screening under its latest Five-Year Plan and posts 22.3% annual device demand growth. Japan mandates yearly cardiovascular checks for citizens older than 40, embedding wearable sensors into universal coverage. These programs create long-run datasets for AI decision support while normalizing at-home diagnostics across the region.

EU MDR Class IIa SaMD post-market surveillance delays

Average clearance for analytical wearables rose from 7 to 19 months, lifting compliance expense 280% for startups. Many postpone EU launches or pivot to wellness labeling, slowing regional access to clinical-grade wearables and prompting consolidation as small firms seek scale to absorb regulatory overhead.

Other drivers and restraints analyzed in the detailed report include:

- Scale-up of printed flexible bio-patches in the EU cutting unit cost below USD 1

- AI-enabled injury-prevention wearables adopted by elite sports leagues

- Battery energy-density limits in ultra-miniature patches

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Accelerometers and inertial MEMS sensors command 32.4% of the market share in 2024, establishing themselves as the foundation of the wearable health sensors ecosystem due to their versatility in tracking movement patterns across multiple body locations. These sensors have evolved beyond simple step counting to enable sophisticated gait analysis and fall detection algorithms that are particularly valuable in elderly care applications. Optical/PPG sensors are projected to grow at the fastest rate of 13.4% from 2025-2030, driven by their expanding capabilities beyond heart rate monitoring to include blood oxygen saturation, blood pressure estimation, and even early-stage glucose monitoring applications. Temperature sensors have found renewed importance in continuous fever monitoring systems, while pressure sensors are increasingly deployed in smart footwear for diabetic foot ulcer prevention.

The integration of multiple sensor types within single devices represents a significant market evolution, with hybrid magnetic and optical sensor combinations showing particular promise for improved cardiovascular monitoring. Recent research from Vietnam National University demonstrates that combining these sensor types can overcome the limitations of optical sensors in detecting subtle cardiovascular abnormalities, potentially enabling earlier intervention for conditions like atrial fibrillation. Biosensors (electrochemical) are gaining traction in specialized applications like sweat analysis for hydration monitoring, while position and proximity sensors enable contextual awareness that improves the accuracy of other sensor readings by accounting for body position and movement artifacts.

Wrist-worn devices maintain their market leadership with 45% share in 2024, benefiting from consumer familiarity, established form factors, and the ability to house multiple sensor types in a single accessible location. The strategic advantage of this placement lies in its balance between user acceptance and sensor accuracy, with major players like Apple and Samsung leveraging their smartwatch platforms to introduce increasingly sophisticated health monitoring capabilities. Smart clothing and textiles are experiencing the fastest growth at 15.2% CAGR (2025-2030), as innovations in flexible electronics and conductive materials enable seamless integration of sensors into everyday garments without compromising comfort or washability.

Chest patches and skin-adhesive sensors are gaining prominence in clinical applications, offering continuous monitoring capabilities for patients with chronic conditions while maintaining a discreet profile. The University of British Columbia has developed a low-cost piezo-resistive sensor that can be embedded in textiles to monitor human movements, including heart rates and temperatures, with the added benefit of being washable and durable SCI. Headgear and eyewear placements are finding specialized applications in neurological monitoring and augmented reality health interfaces, while footwear sensors provide unique insights into gait patterns and weight distribution that are particularly valuable for diabetic care and athletic performance analysis. The emerging category of implantable and ingestible sensors represents the frontier of the market, offering unprecedented monitoring precision but facing significant regulatory and user acceptance challenges.

Wearable Medical Sensors Market is Segmented by Sensor Type (Pressure Sensors, Temperature Sensors and More), Body Placement/Form Factor (Wrist-Wear, Chest Patches and More), Application (Vital-Signs Monitoring, and More), End User (Healthcare Providers, and More), Connectivity (Bluetooth, Wi-Fi and More), and Geography (North America, and More). The Market Sizes and Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America led the wearable health sensors market with 38.71% revenue share in 2024. Widespread RPM reimbursement, high per-capita health spending, and ecosystem depth spur institutional demand. CMS allows providers to bill roughly USD 1,400 each year per monitored chronic patient, turning devices from consumer novelties into clinical assets. Canada expands telehealth to remote provinces, while Mexico's social security system pilots diabetes CGM subsidies.

Asia-Pacific records the fastest 13.8% CAGR through 2030. China's national screening budgets drive bulk procurement of continuous BP cuffs and glucose sensors, while local semiconductor fabricators scale optical chipsets. Japan's super-aged society integrates fall and arrhythmia patch kits into community clinics. India's middle class adopts mid-range fitness bands, and government primary-care centers test wearable vitals kiosks. South Korea leverages foundry expertise to supply MEMS and ASIC cores for global brands.

Europe contributes a significant slice yet faces MDR headwinds. Germany and France reimburse digital therapeutics that pass DiGA or PACTe portals, encouraging heart failure and COPD monitoring pilots. Printed-electronics hubs in Germany, the Netherlands, and the UK reduce patch cost, helping hospitals justify disposable sensors. However, MDR post-market rules slow Class IIa software deployments, leading several startups to prioritize United States release first. The Middle East accelerates adoption within oil and gas labor programs, while African uptake depends on addressing PPG accuracy in darker skin populations and connectivity gaps.

- Apple Inc.

- Alphabet Inc. (Fitbit)

- TE Connectivity Ltd.

- STMicroelectronics N.V.

- Texas Instruments Inc.

- Analog Devices Inc.

- TDK Corporation

- Infineon Technologies AG

- NXP Semiconductors N.V.

- Maxim Integrated Products Inc.

- Abbott Laboratories

- Medtronic plc

- Dexcom Inc.

- Garmin Ltd.

- Omron Corporation

- Masimo Corporation

- Huawei Technologies Co. Ltd.

- Samsung Electronics Co. Ltd.

- Robert Bosch GmbH

- Valencell Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 FDA-Reimbursed Remote Patient Monitoring Codes Accelerating U.S. Prescription-Grade Wearables

- 4.2.2 National Chronic-Disease Screening Mandates in Asia Driving Continuous BP / CGM Kits

- 4.2.3 Scale-up of Printed Flexible Bio-Patches in EU Cutting Unit Cost Below US$1

- 4.2.4 AI-Enabled Injury-Prevention Wearables Adopted by Elite Sports Leagues

- 4.2.5 Worker-Safety Heat-Strain Programs in GCC Oil and Gas Operations

- 4.2.6 Venture Funding Surge in Non-invasive Glucose Optical Sensors

- 4.3 Market Restraints

- 4.3.1 EU MDR Class IIa SaMD Post-Market Surveillance Delays

- 4.3.2 Battery Energy-Density Limits in Ultra-Miniature Patches

- 4.3.3 PPG Accuracy Gaps on Dark Skin Tones Recalls in Africa/Caribbean

- 4.3.4 Data-Sovereignty Compliance Costs in Brazil and Colombia

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory and Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

- 4.7 Technology Snapshot (Sensor Miniaturization, Printed and Flexible Electronics)

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Sensor Type

- 5.1.1 Pressure Sensors

- 5.1.2 Temperature Sensors

- 5.1.3 Accelerometers / Inertial MEMS

- 5.1.4 Optical / PPG Sensors

- 5.1.5 Biosensors (Electro-chemical)

- 5.1.6 Gyroscopes and Magnetometers

- 5.1.7 Position and Proximity Sensors

- 5.1.8 Others

- 5.2 By Body Placement / Form Factor

- 5.2.1 Wrist-wear

- 5.2.2 Headgear and Eyewear

- 5.2.3 Chest Patches and Skin-Adhesive

- 5.2.4 Footwear and In-Shoe

- 5.2.5 Smart Clothing / Textiles

- 5.2.6 Implantable and Ingestible Sensors

- 5.3 By Application

- 5.3.1 Vital-Signs Monitoring

- 5.3.2 Chronic-Disease Management (Diabetes, CVD)

- 5.3.3 Sports and Fitness Performance

- 5.3.4 Remote Patient Monitoring and Elderly Care

- 5.3.5 Mental-Health and Stress Tracking

- 5.3.6 Worker Safety and Environmental Exposure

- 5.4 By End User

- 5.4.1 Healthcare Providers and Hospitals

- 5.4.2 Consumers and Consumer-Electronics Brands

- 5.4.3 Sports Teams / Fitness Centers

- 5.4.4 Military and First Responders

- 5.4.5 Home-care Agencies

- 5.5 By Connectivity Technology

- 5.5.1 Bluetooth / BLE

- 5.5.2 Wi-Fi

- 5.5.3 NFC / RFID

- 5.5.4 Cellular (LTE-M / NB-IoT)

- 5.5.5 Ultra-Wideband (UWB)

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Nordics

- 5.6.3.1.1 Sweden

- 5.6.3.1.2 Norway

- 5.6.3.1.3 Denmark

- 5.6.3.1.4 Finland

- 5.6.3.2 Western Europe

- 5.6.3.2.1 Germany

- 5.6.3.2.2 United Kingdom

- 5.6.3.2.3 France

- 5.6.3.2.4 Italy

- 5.6.3.2.5 Spain

- 5.6.3.2.6 Netherlands

- 5.6.3.3 Eastern Europe

- 5.6.3.3.1 Poland

- 5.6.3.3.2 Russia

- 5.6.3.3.3 Rest of Eastern Europe

- 5.6.4 Middle East

- 5.6.4.1 GCC (Saudi Arabia, UAE, Qatar, Kuwait, Bahrain, Oman)

- 5.6.4.2 Turkey

- 5.6.4.3 Rest of Middle East

- 5.6.5 Africa

- 5.6.5.1 South Africa

- 5.6.5.2 Nigeria

- 5.6.5.3 Kenya

- 5.6.5.4 Rest of Africa

- 5.6.6 Asia-Pacific

- 5.6.6.1 China

- 5.6.6.2 Japan

- 5.6.6.3 India

- 5.6.6.4 South Korea

- 5.6.6.5 ASEAN (Indonesia, Malaysia, Thailand, Vietnam, Philippines, Singapore)

- 5.6.6.6 Rest of Asia-Pacific

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves (MandA, Funding, Partnerships)

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)}

- 6.4.1 Apple Inc.

- 6.4.2 Alphabet Inc. (Fitbit)

- 6.4.3 TE Connectivity Ltd.

- 6.4.4 STMicroelectronics N.V.

- 6.4.5 Texas Instruments Inc.

- 6.4.6 Analog Devices Inc.

- 6.4.7 TDK Corporation

- 6.4.8 Infineon Technologies AG

- 6.4.9 NXP Semiconductors N.V.

- 6.4.10 Maxim Integrated Products Inc.

- 6.4.11 Abbott Laboratories

- 6.4.12 Medtronic plc

- 6.4.13 Dexcom Inc.

- 6.4.14 Garmin Ltd.

- 6.4.15 Omron Corporation

- 6.4.16 Masimo Corporation

- 6.4.17 Huawei Technologies Co. Ltd.

- 6.4.18 Samsung Electronics Co. Ltd.

- 6.4.19 Robert Bosch GmbH

- 6.4.20 Valencell Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

健康感測器市場按感測器類型、應用、產品類型、最終用戶、連接方式和分銷管道分類-2025-2032年全球預測

健康感測器市場按感測器類型、應用、產品類型、最終用戶、連接方式和分銷管道分類-2025-2032年全球預測 2025年全球健康感測器市場報告

2025年全球健康感測器市場報告 穿戴式健康感測器市場:2025-2030 年全球預測

穿戴式健康感測器市場:2025-2030 年全球預測 穿戴式健康感測器的全球市場(2024-2028)

穿戴式健康感測器的全球市場(2024-2028) 美國健康感測器市場規模、佔有率和趨勢分析報告:2024-2030 年按產品、應用、地區和細分市場預測

美國健康感測器市場規模、佔有率和趨勢分析報告:2024-2030 年按產品、應用、地區和細分市場預測 全球健康感測器市場規模研究與預測,按類型、按產品、按應用、按最終用途和區域分析,2023-2030 年健康感測器市場規模、佔有率、趨勢分析報告:材料類型、應用、最終用途、地區和細分市場預測,2024-2030 年

全球健康感測器市場規模研究與預測,按類型、按產品、按應用、按最終用途和區域分析,2023-2030 年健康感測器市場規模、佔有率、趨勢分析報告:材料類型、應用、最終用途、地區和細分市場預測,2024-2030 年