|

市場調查報告書

商品編碼

1272700

血粉市場——增長、趨勢和預測 (2023-2028)Blood Meal Market - Growth, Trends, and Forecasts (2023 - 2028) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

在預測期內,血粉市場的複合年增長率預計為 3.1%。

主要亮點

- 由於含氮量高,血粉是製作全價動物飼料的重要成分。 它還用作有機肥料,為植物提供礦物質和養分。 血粉是動物飼料和有機肥料的蛋白質來源,全球市場預計在未來幾年將出現適度增長。 隨著新興國家城市化進程的推進,對動物產品的需求不斷增加,市場有望進一步活躍起來。

- 血粉作為飼料和肥料在農業中的多方面用途預計將在預測期內略微提振需求。 然而,嚴格的監管框架是影響全球血粉市場增長的一個因素。 隨著對動物福利和環境可持續性的日益關注,預計監管環境將變得更加嚴格。

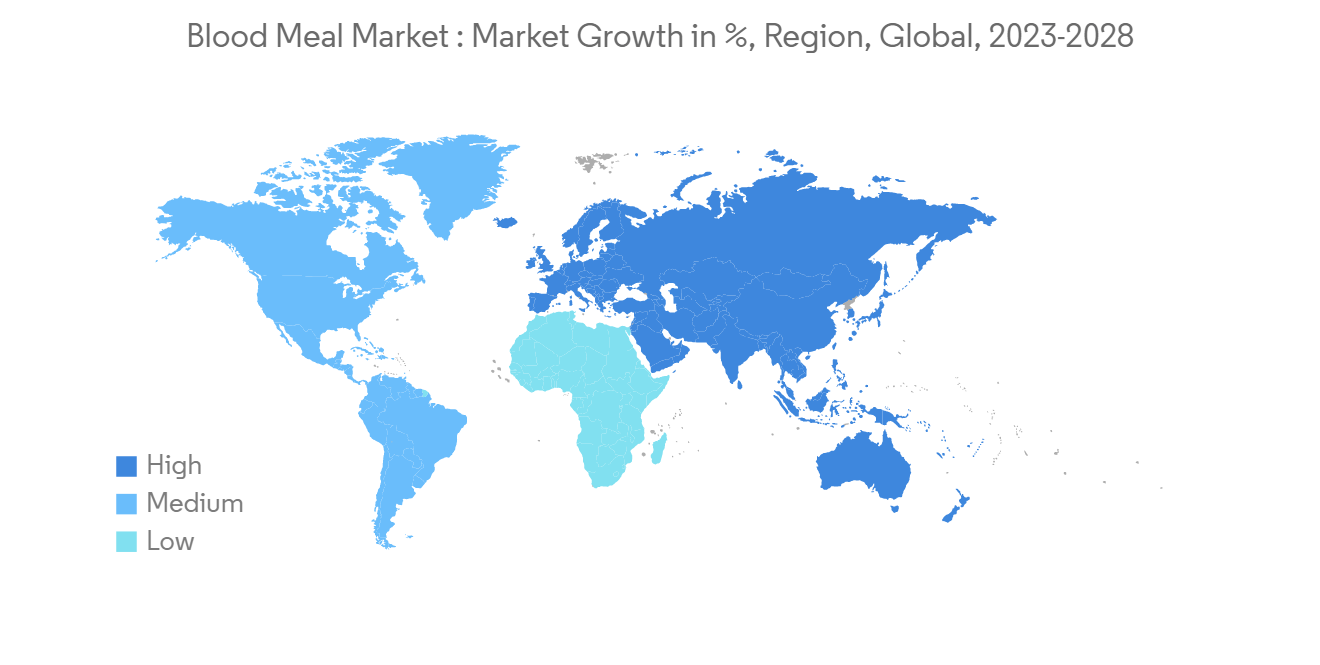

- 亞太地區擁有大量牲畜和廣闊的農業區,因此該市場有望快速增長。 此外,該地區的高產能使其成為對血粉製造商具有吸引力的市場。 隨著對動物產品的需求增加,該地區的新興國家正在大力投資農業以滿足不斷增長的需求。

血粉市場趨勢

不斷增長的動物肉類需求創造了市場機會

- 血液被認為是一種液體蛋白質,富含賴氨酸等氨基酸,因此比賴氨酸含量較低的植物蛋白更具優勢。 推動血粉市場增長的主要因素是可支配收入增加、城市化和對動物蛋白的需求增加。 根據全球飼料調查,2018-2022 年飼料產量增長了 15.4%。 水產養殖業和水產養殖產品的增長也增加了對營養飼料的需求。

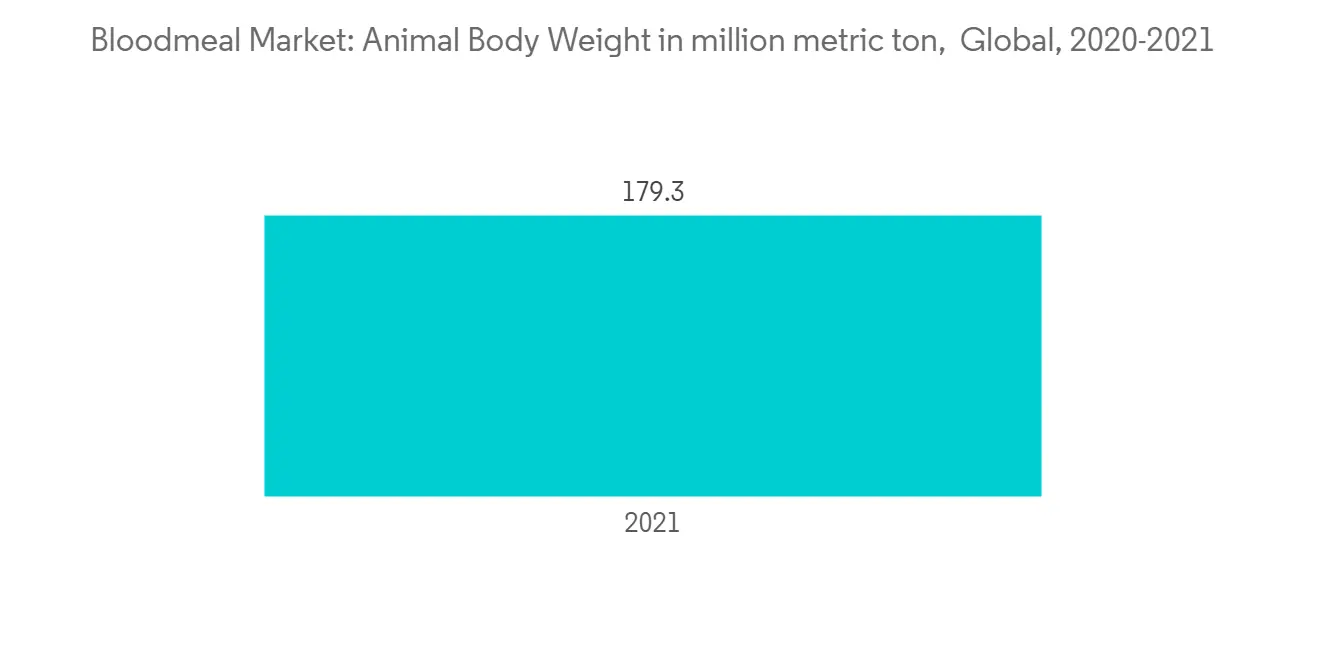

- 根據聯合國糧食及農業組織 (FAO) 的數據,2021 年全球捕撈魚類產量將達到 1.793 億噸,比 2019 年到 2021 年增長 1.9%。 隨著對動物衍生產品(不僅僅是動物肉)的需求增加,動物屠宰量增加,為血粉製造商提供了機會。

- 根據糧農組織的數據,從 2018 年到 2020 年,屠宰的動物數量增加了 2.8%,到 2020 年達到 732 億頭。 這些飲食是優質蛋白質和其他營養素的天然來源,並且由於對天然飼料成分的需求不斷增加,預計將獲得牽引力。

亞太地區是增長最快的市場

- 亞太地區預計將成為血粉市場增長最快的地區。 由於牛肉和豬肉等動物產品的生產和消費不斷增加,該地區被認為是一個有吸引力的市場。 據糧農組織稱,該地區的牛肉產量將從 2018 年的 1780 萬噸增加到 2021 年的 1950 萬噸。 中國和越南豬肉等主要肉類消費國的存在也是支持該地區目標市場增長的一個因素。

- 根據經濟合作與發展組織 (OECD) 的數據,中國人均豬肉消費量為 24 公斤/人。 而在越南,豬肉佔肉類消費量的 70%,估計為每人 25 公斤。 印度和中國等國家的城市化進程加快和人口增長也是推動亞太地區血粉市場增長的因素。

- 到 2022 年,印度將成為最大的反芻動物飼料生產國,產量將達到 5.309 億噸。 這是由於畜牧業基礎設施發展基金 (AHIDF) 等計劃的實施,該基金鼓勵建立動物飼料製造廠並加強現有工廠。 對複合飼料的需求不斷增長,以及通過改善營養來提高農場生產力和盈利能力,預計將在預測期內推動該地區的血粉市場。

血粉行業概況

隨著國內外參與者進入市場,全球骨粉市場適度整合。 市場上的主要參與者是 Boyer Valley Company LLC、The Fertrell Company、Darling Ingredients 等。 由於機會越來越多,許多公司有興趣投資血粉市場。 廠商投資研發,收購競爭對手,推廣血粉。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 三個月的分析師支持

內容

第一章介紹

- 調查假設和市場定義

- 本次調查的範圍

第二章研究方法論

第 3 章執行摘要

第四章市場動態

- 市場概覽

- 市場驅動因素

- 市場製約因素

- 波特的五力分析

- 新進入者的威脅

- 買方/消費者議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭公司之間的敵對關係

第 5 章市場細分

- 的由來

- 豬血

- 家禽血

- 反芻動物血液

- 用法

- 家禽飼料

- 豬肉飼料

- 反芻動物飼料

- 水產飼料

- 天然害蟲防治劑

- 有機肥

- 地區

- 北美

- 美國

- 加拿大

- 墨西哥

- 其他北美地區

- 歐洲

- 德國

- 英國

- 法國

- 俄羅斯

- 西班牙

- 其他歐洲

- 亞太地區

- 印度

- 中國

- 日本

- 其他亞太地區

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中東和非洲

- 阿拉伯聯合酋長國

- 沙特阿拉伯

- 其他中東和非洲地區

- 北美

第六章競爭格局

- 最常採用的策略

- 市場份額分析

- 公司簡介

- Boyer Valley Company, LLC.

- The Fetrell Company

- Terramar Chile

- Darling Ingredients

- West Coast Reduction Ltd

- Agro-industrial Complex Backa Topola LTD

- Valley Proteins Inc.

- Sanimax

- Allanasons Pvt Ltd

第7章 市場機會未來動向

簡介目錄

Product Code: 67624

The blood meal market is estimated to register a CAGR of 3.1% during the forecast period.

Key Highlights

- Blood meal is a crucial ingredient in formulating complete feed for animals, owing to its high nitrogen content. It is also used as an organic fertilizer, providing minerals and nutrients for plants. The global market for blood meal, a protein source for animal feed and organic fertilizer, is projected to experience moderate growth in the coming years. The growing demand for animal-based products in emerging countries, driven by increasing urbanization, is expected to further fuel the market.

- The multifaceted applications of blood meal in agriculture as both feed and fertilizer are expected to drive demand slightly during the forecast period. However, the stringent regulatory framework is a factor that may affect the growth of the global blood meal market. The regulatory landscape is expected to become more stringent, with an increasing focus on animal welfare and environmental sustainability.

- The Asia-Pacific region is expected to witness the fastest growth in the market, owing to its high population of livestock and a larger area under agriculture. Additionally, the region's high production capabilities make it an attractive market for blood meal manufacturers. With the growing demand for animal-based products, emerging economies in the region are investing heavily in agriculture to meet the growing demand.

Blood Meal Market Trends

Growing Demand for Animal Meat is creating Market Opportunities

- Blood is considered a liquid protein and is rich in amino acids like Lysine, and has an advantage over plant-based protein with low lysine content. The major factors behind the growth of the blood meal market are the rise in disposable incomes, urbanization, and increased demand for animal proteins. According to the Global Feed survey, feed production increased by 15.4% in 2018-2022. The growth in aquaculture and aquaculture products also increases the demand for nutritional feed.

- According to Food and Agriculture Organization (FAO), the global capture fisheries production in 2021 reached a record of 179.3 million metric tons, an increase of 1.9% between 2019 and 2021. With the increasing demand for animal meat as well as animal-based products, there is an increase in the slaughter of animals leading to the opening of various opportunities for manufacturers of blood meal.

- According to FAO, the number of animals slaughtered increased by 2.8% in 2018-2020 and reached 73.2 billion in 2020. These meals are a natural source of high-quality protein as well as other nutrients and are expected to gain traction owing to the increasing demand for natural feed ingredients.

Asia Pacific is the Fastest Growing Market

- Asia-Pacific is anticipated to record the fastest growth in the blood meals market. The region seems to be an attractive market owing to increasing production as well as consumption of various animal-based products such as beef meat and pork meat. According to FAO, cattle meat production in the region increased from 17.8 million metric ton in 2018 to 19.5 million metric ton in 2021. The presence of major meat-consuming countries such as pork in China and Vietnam is another factor supporting the growth of the target market in this region.

- According to Organisation for Economic Co-operation and Development (OECD), the average pork consumption in China is 24 kg per person. Also, in Vietnam, pork accounts for 70% of the meat consumption and is anticipated as 25 kg per person. In countries like India and China, growing urbanization and increasing population are also factors propelling the growth of the blood meal market in the Asia Pacific region.

- India is the largest ruminant feed producer, with 530.9 million metric tons in 2022. This is due to implementing schemes such as the Animal Husbandry Infrastructure Development Fund (AHIDF), which encourages establishing animal feed manufacturing plants and strengthening existing ones. Increasing demand for compound feed and a focus on farm productivity and profitability through improved nutrition are expected to drive the blood meal market in the region during the forecast period.

Blood Meal Industry Overview

The global bone meal market is moderately consolidated with domestic players and international players in the market. The major players in the market include Boyer Valley Company LLC, The Fertrell Company, and Darling Ingredients. Many companies are taking an interest in investing in the blood meal market owing to increasing opportunities. Manufacturers are investing in R&D, acquiring their competitors, and promoting blood meal products.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Source

- 5.1.1 Porcine Blood

- 5.1.2 Poultry Blood

- 5.1.3 Ruminant Blood

- 5.2 Application

- 5.2.1 Poultry Feed

- 5.2.2 Porcine Feed

- 5.2.3 Ruminant Feed

- 5.2.4 Aqua Feed

- 5.2.5 Natural Pest Deterrent

- 5.2.6 Organic Fertilizer

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.1.4 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Russia

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia Pacific

- 5.3.3.1 India

- 5.3.3.2 China

- 5.3.3.3 Japan

- 5.3.3.4 Rest of the Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East & Africa

- 5.3.5.1 United Arab Emirates

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 Rest of the Middle East & Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Most Adopted Strategies

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 Boyer Valley Company, LLC.

- 6.3.2 The Fetrell Company

- 6.3.3 Terramar Chile

- 6.3.4 Darling Ingredients

- 6.3.5 West Coast Reduction Ltd

- 6.3.6 Agro-industrial Complex Backa Topola LTD

- 6.3.7 Valley Proteins Inc.

- 6.3.8 Sanimax

- 6.3.9 Allanasons Pvt Ltd