|

市場調查報告書

商品編碼

1690707

橡膠加工油:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Rubber Process Oils - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

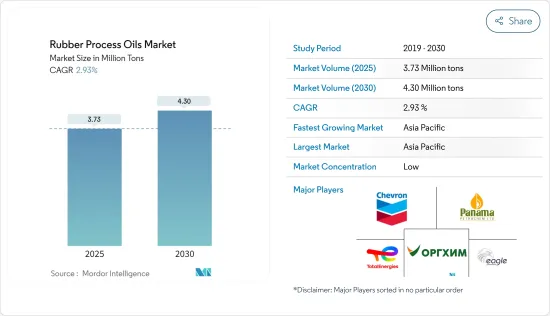

2025 年橡膠加工油市場規模預計為 373 萬噸,預計到 2030 年將達到 430 萬噸,預測期內(2025-2030 年)的複合年成長率為 2.93%。

新冠肺炎疫情為市場帶來了負面影響。這是因為製造設施和工廠由於封鎖和限制而關閉。供應鏈和運輸中斷進一步擾亂了市場。不過,2021年,產業復甦,市場需求回歸。

主要亮點

- 短期內,汽車產業對輪胎和汽車零件的需求增加是推動市場成長的主要因素之一。

- 另一方面,原料價格的波動預計會阻礙市場成長。

- 然而,預計預測期內對生物基橡膠加工油的需求不斷增加將為市場成長提供各種機會。

- 亞太地區是最大的市場,由於中國、印度和日本等國家的消費量不斷增加,預計將在預測期內成為成長最快的市場。

橡膠加工油市場趨勢

輪胎和汽車零件對橡膠加工油的需求不斷增加

- 橡膠加工油用於混合橡膠化合物。這些產品提高了填料的分散性和化合物的流動性。因此,它被認為是橡膠工業最重要的組成部分。

- 橡膠加工油用於輪胎和其他汽車零件,因為它們可以改善機械性能。此外,該產品的煞車效率和燃油經濟性提高將進一步有利於其在輪胎和汽車零件中的應用。

- 橡膠加工油可以改善用於製造輪胎的橡膠的性能。人口成長帶來的生活水準提高和消費能力增強正在推動全球對汽車的需求。例如,根據 OICA 的數據,2022 年全球整體乘用車產量將達到 6,159 萬輛,比 2021 年成長 8%,比 2020 年成長 10%。因此,預計乘用車產量的增加將在預測期內創造對橡膠加工油市場的需求上升。

- 此外,德國汽車產業也因半導體短缺和原料供應有限而受到阻礙。同樣,其他因素,例如新的全球統一輕型車輛測試程序(WLTP)的實施、美國和中國之間的貿易緊張局勢導致國際汽車需求減少,以及歐盟28國的新排放氣體標準要求汽車製造商確保新售出的汽車平均二氧化碳排放為每公里95克,也對乘用車生產產生了不利影響。

- 不過,2022年,汽車生產逐漸從半導體短缺中恢復。例如,根據 OICA 的數據,2022 年德國生產了約 3,480,357 輛乘用車,比 2021 年成長 12%。因此,預計乘用車領域產量的增加將推動橡膠加工油市場的需求上升。

- 此外,美國是世界第二大汽車銷售和生產市場。例如,根據 OICA 的數據,2022 年美國汽車產量將達到 10,063,339 輛,比 2021 年增加 10%。因此,預計汽車產量的增加將導致橡膠加工油市場的需求增加。

- 因此,預計預測期內該地區所有這些有利趨勢和投資都將推動橡膠加工油市場的需求。

亞太地區佔市場主導地位

- 預計預測期內亞太地區將主導橡膠加工油市場。中國、日本和印度等新興國家輪胎和汽車零件對橡膠加工油的需求不斷成長,預計將推動該地區對橡膠加工油的需求。

- 最大的橡膠加工油生產商位於亞太地區。橡膠加工油生產的主要企業包括道達爾、雪佛龍知識產權有限責任公司、巴拿馬石油化工有限公司、ORGKHIM生化控股和Eagle Petrochem。

- 隨著消費者對電動車的偏好日益成長,中國汽車產業正經歷動態轉變。中國汽車工業的擴張預計將使橡膠加工油市場受益。根據國際汽車工業組織(OICA)的數據,中國是世界上最大的汽車生產國,佔全球產量的近34%。 2022年汽車產量為27,020,615輛,較2021年的26,121,712輛成長24%。因此,汽車產量的增加預計將帶來橡膠加工油市場需求的上升。

- 在印度,更嚴格的汽車排放標準、車輛安全性的提高、汽車高級駕駛輔助系統 (ADAS) 的引入以及零售和電子商務領域物流的快速成長都在推動對新型和先進輕型商用車 (LCV) 的需求。例如,根據OICA的數據,印度2022年輕型商用車產量將達到617,398輛,較2021年成長27%,較2020年恢復60%。

- 此外,印度汽車產業的投資不斷增加和進步預計將增加橡膠加工油市場的消費量。例如,塔塔汽車在2022年4月宣布,計劃在未來五年內向其乘用車業務投資30.8億美元。預計此次擴建將對該國的橡膠加工油市場產生正面影響。

- 在工業和建築活動中,人們越來越意識到要保護工人免受觸電、墜落物體、有害化學物質和石油洩漏、移動機械等造成的傷害,這可能會對橡膠鞋的需求產生積極影響。橡膠鞋生產中橡膠加工油的使用量正在增加。因此,對橡膠鞋的需求不斷成長將進一步推動橡膠加工油市場的發展。

- 由於上述因素,預計研究期間亞太地區的橡膠製加工油市場將大幅成長。

橡膠加工油產業概況

橡膠加工油市場比較分散。該市場的主要企業(不分先後順序)包括道達爾能源、雪佛龍公司、巴拿馬石油化工有限公司、ORGKHIM Biochemical Holding、EaglePetrochem 等。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 調查前提條件

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場動態

- 驅動程式

- 輪胎和汽車零件需求增加

- 鞋類需求增加

- 其他

- 限制因素

- 原物料價格波動

- 其他限制因素

- 價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章 市場區隔

- 產品類型

- 芳香

- 石蠟基

- 環烷酸

- 應用

- 輪胎和汽車零件

- 鞋類

- 消費品

- 其他用途

- 地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭格局

- 併購、合資、合作與協議

- 市場佔有率(%)**/排名分析

- 主要企業策略

- 公司簡介

- APAR Industries

- Chevron Corporation

- CPC Corporation

- EaglePetrochem

- Exxon Mobil Corporation

- HF Sinclair Corporation

- LODHA Petro

- ORGKHIM Biochemical Holding

- Panama Petrochem Ltd

- Repsol

- Sterlite Lubricants

- TotalEnergies

- Witmans Industries Pvt. Ltd

第7章 市場機會與未來趨勢

- 生物基橡膠加工油的需求不斷增加

- 其他機會

The Rubber Process Oils Market size is estimated at 3.73 million tons in 2025, and is expected to reach 4.30 million tons by 2030, at a CAGR of 2.93% during the forecast period (2025-2030).

The COVID-19 pandemic negatively impacted the market. This was because of the shutdown of the manufacturing facilities and plants due to the lockdown and restrictions. Supply chain and transportation disruptions further created hindrances for the market. However, the industry witnessed a recovery in 2021, thus rebounding the demand for the market studied.

Key Highlights

- Over the short term, increasing demand for tire and automotive components from the automobile industry is one of the major factors driving the growth of the market studied.

- On the flip side, volatility in raw material prices is expected to hinder the growth of the market.

- However, the increasing demand for bio-based rubber process oil is forecasted to offer various opportunities for the growth of the market over the forecast period.

- Asia-Pacific region represents the largest market and is also expected to be the fastest-growing market over the forecast period owing to the increasing consumption from countries such as China, India, and Japan.

Rubber Process Oil Market Trends

Growing Demand of Rubber Process Oil from Tire and Automobile Components

- Rubber process oils are used while mixing the rubber compounds. These products improve the dispersion of fillers and the flow property of the compound. Hence, it is considered to be the most important ingredient for the rubber-based industry.

- Due to enhanced mechanical properties, rubber process oils are used in the tire and other automotive components. In addition, improved braking efficiency and fuel consumption of the product are likely to further benefit its usage in the tire and automotive components.

- The rubber process oils enhance the rubber properties used in the production of tires. Rising population improved living standards and increased spending power are factors likely to boost the demand for automobiles globally. For instance, according to OICA, in 2022, the total number of passenger cars produced globally was 61.59 million units, which showed an increase of 8% compared to 2021 and 10% compared to 2020. Therefore, an increase in the production of passenger cars is expected to create an upside demand for the rubber process oil market in the forecast period.

- Moreover, in Germany, the automotive industry has been hampered by the shortage of semiconductors and a limited supply of raw materials. Similarly, other factors such as the implementation of the new Worldwide Harmonized Light-Duty Vehicles Test Procedure (WLTP) and US-China trade conflicts which decreased the international automotive demand, EU-28's new emission standard which mandates carmakers to achieve average CO2 emissions of 95 grams per kilometre across newly sold vehicles had negatively affected the production of passenger cars.

- However, in 2022 the automobile production in the country recovered gradually from semiconductor shortages. For instance, according to OICA, around 34,80,357 passenger cars were produced in Germany in 2022, which shows an increase of 12% compared to 2021. Therefore, increase in the production of passeger car segment is expected to create an upside demand for the rubber process oils market.

- Furthermore, the United States is the second-largest market for vehicle sales and production globally. For instance, according to OICA, in 2022, automobile production in the United States amounted to 1,00,60,339 units, which showed an increase of 10% compared to 2021. As a result, an increase in automobile production is expected to create an upside demand for rubber process oils market.

- Therefore, all such favorable trends and investments in the region are expected to drive the demand for rubber process oils market during the forecast period.

Asia-Pacific Region to Dominate the Market

- Asia-Pacific region is expected to dominate the market for rubber process oil during the forecast period. The rising demand for rubber process oil from tire and automobile components in developing countries like China, Japan, and India is expected to drive the demand for rubber process oil in this region.

- The largest producers of rubber process oil are located in the Asia-Pacific region. Some of the leading companies in the production of rubber process oil are Total, Chevron Intellectual Property LLC, Panama Petrochem Ltd, ORGKHIM Biochemical Holding, and Eagle Petrochem among others.

- The automobile industry in China is experiencing shifting trends as consumer preference for battery-powered electric vehicles rises. The expansion of China's automotive sector is expected to benefit the rubber process oil market. According to the International Organization of Motor Vehicle Manufacturers (OICA), China is the world's largest automobile producer, accounting for nearly 34% of global volume. In 2022, the country produced 2,70,20,615 units of automobiles, registering an increase of 24% compared to 2,61,21,712 units in 2021. Therefore, increasing in the production of automobiles is expected to create an upside demand for the rubber process oil market.

- In India, increasing regulations on vehicle emissions, advancement in vehicle safety, the introduction of driver-assist systems in vehicles, and rapidly growing logistics in the retail and e-commerce sectors, have been significantly driving the demand for new and advanced Light commercial vehicles (LCVs). For instance, accroding to OICA, in 2022, light commercial vehicle production in India amounted to 6,17,398 units, which showen an increase of 27% compared to 2021 and a recovery of 60% compared to 2020.

- Furthermore, increased investments and advancements in the automobile industry in India is expected to increase the consumption of rubber process oil market. For instance, in April 2022, Tata Motors announced plans to invest USD 3.08 billion in its passenger vehicle business over the next five years. This expansion is expected to have a positive impact on the rubber process oils market in the country.

- Rising awareness about the worker's safety from injuries due to electrical contacts, falling objects, spilling of harmful chemicals and oils, moving machinery, and others during industrial or construction work is likely to benefit the demand for rubber footwear. Rubber process oil is increasingly used in manufacturing footwear using rubber. Hence, the rising demand for rubber footwear further fuels the rubber process oils market.

- Owing to the above-mentioned factors, the market for rubber process oil in the Asia-Pacific region is projected to grow significantly during the study period.

Rubber Process Oil Industry Overview

The Rubber Process Oil Market is fragmented in nature. The major players in this market (not in a particular order) include TotalEnergies, Chevron Corporation, Panama Petrochem Ltd, ORGKHIM Biochemical Holding, and EaglePetrochem, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand for Tire and Automotive Components

- 4.1.2 Growing Demand for Footwear

- 4.1.3 Others

- 4.2 Restraints

- 4.2.1 Volatility in Raw Material Price

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Product Type

- 5.1.1 Aromatic

- 5.1.2 Paraffinic

- 5.1.3 Naphthenic

- 5.2 Application

- 5.2.1 Tire and Automobile Components

- 5.2.2 Footwear

- 5.2.3 Consumer Goods

- 5.2.4 Other Applications

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 APAR Industries

- 6.4.2 Chevron Corporation

- 6.4.3 CPC Corporation

- 6.4.4 EaglePetrochem

- 6.4.5 Exxon Mobil Corporation

- 6.4.6 HF Sinclair Corporation

- 6.4.7 LODHA Petro

- 6.4.8 ORGKHIM Biochemical Holding

- 6.4.9 Panama Petrochem Ltd

- 6.4.10 Repsol

- 6.4.11 Sterlite Lubricants

- 6.4.12 TotalEnergies

- 6.4.13 Witmans Industries Pvt. Ltd

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Demand of Bio Based Rubber Processing Oil

- 7.2 Other Opportunities

全球加工油市場按類型、應用、功能和地區分類-預測(至2030年)

全球加工油市場按類型、應用、功能和地區分類-預測(至2030年) 2026年全球加工油市場報告

2026年全球加工油市場報告 加工油市場規模、佔有率和成長分析(按類型、功能、生產技術、應用和地區分類)-2026-2033年產業預測

加工油市場規模、佔有率和成長分析(按類型、功能、生產技術、應用和地區分類)-2026-2033年產業預測 加工油的全球市場 (~2035年):油類型·生產技術·用途·終端用戶·流通管道·各地區

加工油的全球市場 (~2035年):油類型·生產技術·用途·終端用戶·流通管道·各地區 加工油市場按應用、產品類型、黏度等級和來源分類 - 全球預測 2025-2032

加工油市場按應用、產品類型、黏度等級和來源分類 - 全球預測 2025-2032 全球加工油市場,2024-2031年

全球加工油市場,2024-2031年 工藝油市場-全球產業規模、佔有率、趨勢、機會和預測,按類型、功能、應用、生產技術、地區和競爭細分,2020-2030 年

工藝油市場-全球產業規模、佔有率、趨勢、機會和預測,按類型、功能、應用、生產技術、地區和競爭細分,2020-2030 年 全球加工油市場:產業分析、規模、佔有率、成長、趨勢、預測(2024-2031)

全球加工油市場:產業分析、規模、佔有率、成長、趨勢、預測(2024-2031)