|

市場調查報告書

商品編碼

1406249

白雲石:市場佔有率分析、產業趨勢與統計、2024年至2029年成長預測Dolomite - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

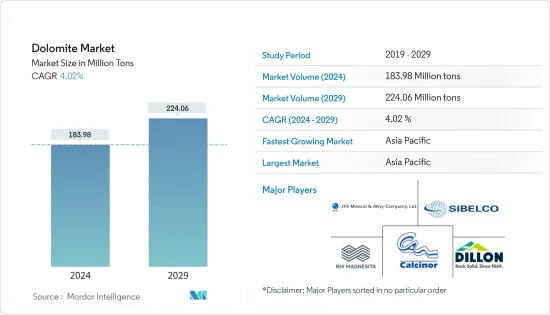

預計2024年白雲石市場規模為18398萬噸,預計2029年將達22406萬噸,在預測期內(2024-2029年)複合年成長率為4.02%。

2020年,市場受到COVID-19大流行的負面影響,導致生產和運輸放緩,水泥、陶瓷等行業因遏制措施和經濟中斷而被迫推遲生產。目前市場正從疫情中恢復。預計2022年市場將達到疫情前水準並持續穩定成長。

主要亮點

- 亞太地區建築業應用的擴大和鋼鐵產量的擴大正在推動市場成長。

- 然而,以含有橄欖石礦物的火成岩取代原料白雲石可能會阻礙探勘市場需求。

- 此外,預計使用白雲石作為鈣和鎂補充品將在製藥行業創造市場機會。

- 亞太地區主導了全球市場需求,其中中國、印度和日本等國家是最大的消費者。

白雲石市場趨勢

建設產業需求增加

- 白雲石用作波特蘭水泥混凝土的骨料,用於道路、建築物和其他結構。白雲石也與瀝青材料結合用於道路和類似建築。白雲石土由於其強度和在精製過程中的相容性而在鋼鐵工業中得到了廣泛的應用。

- 在水泥生產中,白雲石被煅燒並切割成特定尺寸的塊。建設產業是水泥最大的消費者之一。因為商業和工業建築在全球範圍內蓬勃發展。

- 美國人口普查局的數據顯示,2023年1月至9月建築支出年增約4.6%,達1.46兆美元。

- 亞太地區建築業是世界上最大的建築業,在中國和印度住宅建築市場擴張的推動下,預計將成長最快。

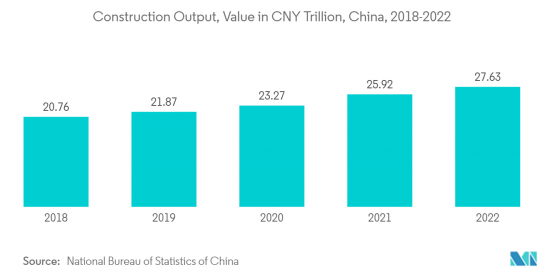

- 根據中國國家統計局數據,2022年國內建築業產值達到高峰約4.11兆美元。

- 此外,印度正在擴大其商業部門。該國正在進行多個計劃。例如,價值9億美元的CommerzIII商業辦公室綜合大樓於2022年第一季動工。本計劃位於孟買戈爾岡,興建一棟43層商業辦公大樓,占地面積2,60,128平方公尺。該計劃預計將於 2027 年第四季完成,同時將在預測期內使所研究的市場受益。

- 由於上述因素,建設產業的白雲石消費量預計在預測期內將以健康的速度成長。

亞太地區主導市場

- 由於中國、印度和日本等主要國家的建築和醫療保健等工業部門的擴張,預計亞太地區在預測期內將佔據全球白雲石市場的最大佔有率。

- 中國擁有龐大的建築業,近兩年基礎設施和住宅領域的發展支撐了建築業的整體成長,無論是數量或金額。

- 中國是世界上最大的水泥生產國,在快速成長的建設產業的支持下,對水泥的需求不斷增加。例如,根據中國國家統計局(NBS)的數據,2023年上半年水泥產量將從2022年同期的9.79億噸增加到9.8億噸,支撐市場成長。

- 此外,根據中國國家統計局的數據,2022年中國付加約8.3兆元(約1.23兆美元),與前一年同期比較成長3%以上。

- 此外,醫療保健行業的擴張預計將推動市場成長。根據 IBEF 的數據,印度的製藥業依數量排名世界第三,依金額排名第 14 位。印度製藥業佔國內生產總值(GDP)的近1.72%。

- 因此,由於上述趨勢,亞太地區預計將在預測期內主導白雲石市場。

白雲石產業概況

白雲石市場因其性質而部分分散。研究市場的主要企業包括(排名不分先後)Sibelco、Calcinor、RHI Magnesita、JFE Mineral & Alloy Company, Ltd、Dillon 等。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第1章簡介

- 調查先決條件

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 促進因素

- 擴大亞太地區的建設活動

- 擴大鋼鐵生產

- 其他司機

- 抑制因素

- 用火成岩取代原料白雲石

- 其他阻礙因素

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 買方議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章市場區隔(市場規模)

- 礦物類型

- 集聚

- 射擊

- 燒結

- 最終用戶產業

- 農業

- 陶瓷/玻璃

- 水泥

- 採礦/冶金

- 藥品

- 水處理

- 其他最終用戶產業(例如飼料)

- 地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 義大利

- 法國

- 歐洲其他地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東/非洲

- 沙烏地阿拉伯

- 南非

- 其他中東/非洲

- 亞太地區

第6章 競爭形勢

- 併購、合資、聯盟、協議

- 市場佔有率(%)**/排名分析

- 主要企業策略

- 公司簡介

- Calcinor

- Carmeuse

- Dillon

- Imerys

- JFE Mineral & Alloy Company,Ltd.

- Lhoist

- Omya AG

- Raw Edge Industrial Solutions Limited

- RHI Magnesita

- Sibelco

第7章 市場機會及未來趨勢

- 對鈣和鎂補充品的需求增加

- 其他機會

The Dolomite Market size is estimated at 183.98 Million tons in 2024, and is expected to reach 224.06 Million tons by 2029, growing at a CAGR of 4.02% during the forecast period (2024-2029).

The market was negatively impacted by the COVID-19 pandemic in 2020 as there was a slowdown in production and mobility, wherein industries such as cement, ceramics, etc., were forced to delay their production due to containment measures and economic disruptions. Currently, the market has recovered from the pandemic. The market reached pre-pandemic levels in 2022 and is expected to grow steadily in the future.

Key Highlights

- The increasing applications in construction industries and expanding steel production in the Asia-Pacific region have been driving the market growth.

- However, the substitution of raw dolomites with igneous rock containing olivine minerals may hamper the demand for the studied market.

- Furthermore, the use of dolomite as a calcium and magnesium supplement is predicted to generate a market opportunity in the pharmaceutical industry.

- Asia-Pacific region dominated the market demand around the world, with countries like China, India, and Japan, being the biggest consumers.

Dolomite Market Trends

Increasing Demand from Construction Industry

- Dolomite is used as aggregate in Portland cement concrete, which is used for roads, buildings, and other structures. Dolomite is also used in combination with bituminous materials for roads and similar construction. Dolomite ground finds a huge application in the iron and steel industry due to its strength and compatibility in the process of purifying iron and steel.

- In the production of cement, dolomite is calcined, and then it is cut into blocks of a specific size. The construction industry is one of the largest consumers of cement. The growing commercial and industrial construction activities are experiencing a boom globally.

- According to the U.S. Census Bureau, the construction spending over the first 9 months of 2023 increased by about 4.6% to USD 1.46 trillion, compared to the same period in 2022.

- The construction sector in the Asia-Pacific region is the largest in the world, and the highest growth for housing is expected to be registered in the Asia-Pacific region, owing to the expanding housing construction markets in China and India.

- According to the National Bureau of Statistics of China, the domestic construction output peaked in 2022 at a value of about USD 4.11 trillion.

- Furthermore, India is expanding its commercial sector. Several projects have been going on in the country. For instance, the CommerzIII Commercial Office Complex construction worth USD 900 million started in Q1 2022. The project involves the construction of a 43-story commercial office complex with a permissible floor area of 2,60,128 square meters in Goregaon, Mumbai. The project is expected to be completed in Q4 2027, thus benefitting the studied market simultaneously during the forecast period.

- Owing to the factors mentioned above, the consumption of dolomite is expected to rise at a healthy rate from the construction industry over the forecast period.

Asia-Pacific to Dominate the Market

- The Asia-Pacific region is expected to account for the largest share of the global dolomite market during the forecast period owing to expanding industrial sectors, such as construction and healthcare, in major countries such as China, India, Japan, etc.

- China hosts a vast construction sector, and the developments in the infrastructure and residential sectors in the past two years have supported the growth of the construction sector at large, both in terms of volume and value.

- China is the largest cement producer globally, and the demand for cement is constantly increasing, supported by the rapidly growing construction industry. For instance, according to the National Bureau of Statistics (NBS) of China, cement output in the first half of 2023 increased to 980 million metric tons from 979 million metric tons in the same period in 2022, thus supporting the growth of the market.

- Also, according to the National Bureau of Statistics of China, the construction industry in China generated an added value of approximately CNY 8.3 trillion (~ USD 1.23 trillion) in 2022, reflecting an increase of more than 3% compared to the previous year.

- Also, the expanding healthcare sector is expected to fuel the market's growth. For instance, India is a global pharmaceutical hub, according to IBEF, the Indian Pharmaceutical industry is the third largest in the world in terms of volume and 14th largest in terms of value. The Indian Pharma sector contributes to nearly 1.72% of the country's GDP.

- Therefore, owing to such trends mentioned above, the Asia-Pacific region is expected to dominate the dolomite market during the forecast period.

Dolomite Industry Overview

The dolomite market is partially fragmented in nature. The major players in the studied market (not in any particular order) include Sibelco, Calcinor, RHI Magnesita, JFE Mineral & Alloy Company, Ltd., and Dillon, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Construction Activities in Asia-Pacific

- 4.1.2 Expanding Steel Production

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Substitution of Raw Dolomite With Igneous Rock

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Mineral Type

- 5.1.1 Agglomerated

- 5.1.2 Calcined

- 5.1.3 Sintered

- 5.2 End-user Industry

- 5.2.1 Agricuture

- 5.2.2 Ceramics and Glass

- 5.2.3 Cement

- 5.2.4 Mining and Metellurgy

- 5.2.5 Pharmaceuticals

- 5.2.6 Water Treatment

- 5.2.7 Other End-user Industries (Animal Feed, etc.)

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers & Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share(%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Calcinor

- 6.4.2 Carmeuse

- 6.4.3 Dillon

- 6.4.4 Imerys

- 6.4.5 JFE Mineral & Alloy Company,Ltd.

- 6.4.6 Lhoist

- 6.4.7 Omya AG

- 6.4.8 Raw Edge Industrial Solutions Limited

- 6.4.9 RHI Magnesita

- 6.4.10 Sibelco

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increase in Demand for Calcium And Magnesium Supplements

- 7.2 Other Opportunities

白雲石礦業市場規模、佔有率及成長分析(按礦物類型、應用和地區)-2025-2032 年產業預測白雲石市場規模、佔有率和成長分析(按產品、最終用途和地區)- 產業預測 2025-2032

白雲石礦業市場規模、佔有率及成長分析(按礦物類型、應用和地區)-2025-2032 年產業預測白雲石市場規模、佔有率和成長分析(按產品、最終用途和地區)- 產業預測 2025-2032 白雲石全球市場規模、佔有率和趨勢分析報告:按產品、最終用途、地區和細分市場進行預測(2025-2030)

白雲石全球市場規模、佔有率和趨勢分析報告:按產品、最終用途、地區和細分市場進行預測(2025-2030) 白雲石市場:按產品、等級和最終用戶分類 - 全球預測 2025-2030白雲石採礦市場:按產品類型、應用、最終用戶產業、製造流程 - 全球預測 2025-2030

白雲石市場:按產品、等級和最終用戶分類 - 全球預測 2025-2030白雲石採礦市場:按產品類型、應用、最終用戶產業、製造流程 - 全球預測 2025-2030 2024 年白雲石世界市場報告

2024 年白雲石世界市場報告 白雲石全球市場2024-2028

白雲石全球市場2024-2028 全球白雲石粉市場研究報告 - 2024 年至 2032 年產業分析、規模、佔有率、成長、趨勢與預測

全球白雲石粉市場研究報告 - 2024 年至 2032 年產業分析、規模、佔有率、成長、趨勢與預測 全球白雲石採礦市場規模研究與預測,按應用(建築材料、農業、動物飼料、陶瓷和玻璃、鋼鐵、塑膠、油漆和塗料、紙張、其他)以及區域分析,2023-2030

全球白雲石採礦市場規模研究與預測,按應用(建築材料、農業、動物飼料、陶瓷和玻璃、鋼鐵、塑膠、油漆和塗料、紙張、其他)以及區域分析,2023-2030 白雲石採礦市場報告:2030 年趨勢、預測與競爭分析

白雲石採礦市場報告:2030 年趨勢、預測與競爭分析