|

市場調查報告書

商品編碼

1429213

渦輪膨脹機:市場佔有率分析、產業趨勢、成長預測(2024-2029)Turbo Expander - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

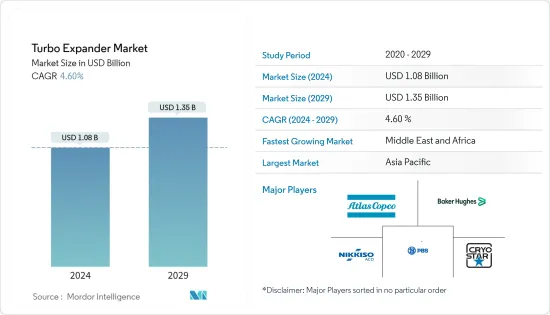

渦輪膨脹機市場規模預計到 2024 年為 10.8 億美元,預計到 2029 年將達到 13.5 億美元,在預測期內(2024-2029 年)複合年成長率為 4.60%。

主要亮點

- 從中期來看,增加對天然氣作為發電和各行業燃料的投資預計將增加對渦輪膨脹機市場的需求。

- 另一方面,太陽能和風力發電等再生能源來源佔有率的增加預計將阻礙市場成長。

- 然而,增加技術投資以有效生產能源和減少二氧化碳排放預計將為渦輪膨脹機市場提供重大機會。

渦輪膨脹機市場趨勢

發電板塊佔有較大佔有率

- 渦輪膨脹機與蒸氣渦輪或燃氣渦輪機類似,是一種帶有膨脹渦輪的旋轉機器,可將氣體中包含的能量轉化為機械功。蒸氣渦輪或燃氣渦輪機的目的是透過驅動發電機或作為其他旋轉機械(例如壓縮機或高功率泵)的原動機,將機械功轉化為有用的電力。

- 2022年,天然氣將在發電中發揮主要作用,約佔發電總量的23%。這主要是由於美國和中國天然氣發電的強勁成長。未來二十年,全球燃氣發電廠裝置容量預計將增加,到 2040 年,電網新增容量預計將超過 1,500 吉瓦。

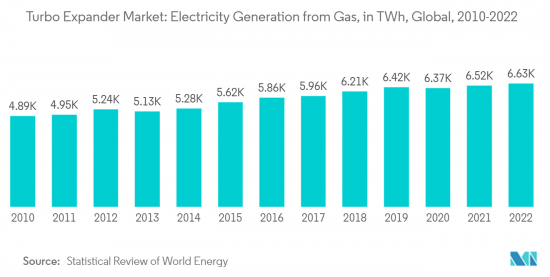

- 2022年天然氣發電量為6,631.4太瓦時,較2021年成長1%。由於轉向清潔能源來源的需求不斷增加以及全球燃煤電廠的提前關閉,預計在預測期內也會出現類似的趨勢。

- 此外,自 2011 年以來,日本已將核能發電能力大部分替換為液化天然氣 (LNG) 發電廠。

- 2022年12月,馬裡蘭州一家電力開發公司透露,計劃在西維吉尼亞建設的180萬千瓦天然氣聯合循環發電設施將採用碳捕獲技術。競爭對手 Power Ventures (CPV) 宣佈在西維吉尼亞州多德里奇縣開設新的 CPV Shea 能源中心。

- 因此,在預測期內,擴大轉向天然氣發電預計將推動發電行業渦輪膨脹機市場的發展。

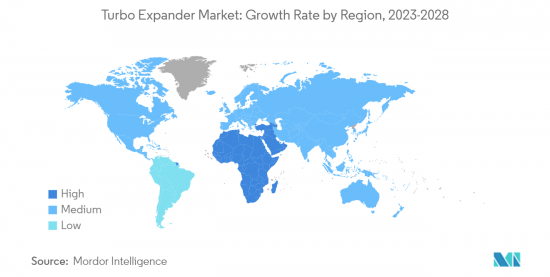

亞太地區主導市場

- 2022年,渦輪膨脹機市場主要由亞太地區主導,預計未來這種情況也將持續下去。渦輪膨脹機需求增加的主要原因之一是擴大使用天然氣發電。由於大多數國家旨在透過轉向天然氣等更清潔的替代燃料來減少碳排放,預計這種資源的消費量將會增加。因此,渦輪膨脹機的需求預計將快速成長。

- 中國制定了氣改電策略,到2030年將天然氣佔發電總量的比重從2021年的4.2%提高到15%。

- 此外,預計未來亞太地區將啟動許多煉油廠和液化天然氣計劃。由於渦輪膨脹機大量用於煉油廠的能源回收和液化天然氣工廠的液化天然氣膨脹,預計此類設備的需求將激增。

- 例如,2022年1月,馬來西亞國家石油公司和馬來西亞沙巴州宣布有意建立一個年處理量200萬噸(mmty)的液化天然氣(LNG)接收站。該設施將建在西皮丹石油和天然氣工業,是馬來西亞國家石油公司與沙巴州合作的一部分,旨在擴大對該州工業和商業實體的清潔能源供應。

- 此外,印度等許多新興經濟體正在經歷快速的經濟成長,並有潛力變得更加工業化。因此,渦輪膨脹機的市場預計將因其在冷凍和能源提取等各種工業應用中的使用而得到推動。

- 因此,鑑於上述幾點,亞太地區預計將在預測期內主導渦輪膨脹機市場。

渦輪膨脹機產業概況

渦輪膨脹機市場正在變得半固體。市場上的主要企業(排名不分先後)包括阿特拉斯·科普柯 AB、貝克休斯公司、Cryostar SAS、Nikkiso ADC 和 PBS Group。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第1章簡介

- 調查範圍

- 市場定義

- 研究場所

第2章調查方法

第3章執行摘要

第4章市場概況

- 介紹

- 2028年之前的市場規模與需求預測(單位:美元)

- 最新趨勢和發展

- 政府法規政策

- 市場動態

- 促進因素

- 增加對發電用天然氣和各種工業燃料的投資

- 抑制因素

- 擴大再生能源來源的佔有率

- 促進因素

- 供應鏈分析

- 波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間敵對關係的強度

第5章市場區隔

- 裝載裝置

- 壓縮機

- 發電機

- 液壓煞車

- 最終用戶產業

- 油和氣

- 發電

- 能源回收

- 其他最終用戶產業

- 地區

- 北美洲

- 美國

- 加拿大

- 北美其他地區

- 歐洲

- 德國

- 法國

- 英國

- 義大利

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 其他亞太地區

- 南美洲

- 巴西

- 阿根廷

- 智利

- 南美洲其他地區

- 中東/非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

- 卡達

- 其他中東和非洲

- 北美洲

第6章 競爭形勢

- 併購、合資、聯盟、協議

- 主要企業策略

- 公司簡介

- Atlas Copco AB

- Baker Hughes Company

- Cryostar SAS

- Nikkiso ACD

- PBS Group

- LA Turbine

- Elliott Group

- Blair Engineering

- Air Products and Chemicals Inc.

第7章 市場機會及未來趨勢

- 增加高效率能源生產和減少碳排放的技術投資

簡介目錄

Product Code: 48372

The Turbo Expander Market size is estimated at USD 1.08 billion in 2024, and is expected to reach USD 1.35 billion by 2029, growing at a CAGR of 4.60% during the forecast period (2024-2029).

Key Highlights

- Over the medium term, the increasing investment in the adaption of natural gas for power generation and fuel for various industries is expected to increase the demand for a turbo expander market.

- On the other hand, an increasing share of renewable energy sources such as solar and wind energy is expected to hinder the market growth.

- Nevertheless, the increasing technological investments in the market to produce energy efficiently and control carbon emissions are expected to create huge opportunities for the turbo expanders market.

Turboexpander Market Trends

Power Generation Segment to Have a Significant Share

- A turboexpander is a rotating machine with an expansion turbine that converts the energy contained in a gas into mechanical work, much like a steam or gas turbine. A steam or gas turbine's goal is to convert the mechanical work into helpful power by either driving an electric generator or being the prime mover for another rotating machine, such as a compressor or a high-power pump.

- Natural gas played a significant role in electricity generation in 2022, accounting for almost 23% of the total. It was mainly due to robust growth in electricity generation from natural gas in the United States and China. The global installed capacity of gas-fired power plants is expected to increase over the next twenty years, with more than 1,500 GW of new capacity projected to be added to the power network by 2040.

- In 2022, electricity generation through natural gas was recorded at 6631.4 TWh, an increase of 1% compared to 2021. A similar trend is expected during the forecasted period due to the increasing demand for adapting cleaner energy sources and the early retirement of coal power plants worldwide.

- Additionally, since 2011, Japan largely replaced its nuclear power generation capacity with plants powered by liquefied natural gas (LNG).

- In December 2022, A power production development firm in Maryland revealed that a planned 1.8 GW combined-cycle natural gas-fired power facility in West Virginia would contain carbon capture technology. Competitive Power Ventures (CPV) announced the new CPV Shay Energy Center location in Doddridge County, West Virginia.

- Therefore, the increasing shift towards natural gas-based power generation is expected to drive the turbo expander market in the power generation sector during the forecast period.

Asia-Pacific to Dominate the Market

- In 2022, the turbo expander market was mainly dominated by Asia-Pacific, which is predicted to continue in the upcoming years. One of the major reasons for the rising demand for turbo expanders is the growing utilization of natural gas to generate power. With most nations aiming to reduce their carbon emissions by transitioning to cleaner fuel alternatives like natural gas, there is an anticipated increase in the consumption of this resource. It is expected to lead to a surge in demand for turbo expanders.

- China formulated a gas-to-power strategy to raise the percentage of natural gas in its overall power generation blend to 15% by 2030, up from 4.2% in 2021.

- In addition, numerous refineries and LNG projects are anticipated to emerge in the Asia-Pacific region in the projected timeframe. As a significant quantity of turbo expanders are utilized for recuperating energy in refineries and in the expansion of LNG within LNG plants, it is expected that there will be a surge in demand for such equipment.

- For instance, in January 2022, Petronas and the Malaysian State of Sabah disclosed their intentions to establish a liquefied natural gas (LNG) terminal with a capacity of two million metric tons/year (mmty). The upcoming facility in the Sipitang Oil and Gas Industrial Park is a component of Petronas' cooperation with the state in expanding Sabah's distribution of cleaner energy to industrial and commercial entities.

- Furthermore, many developing economies, such as India, are growing quickly, potentially leading to increased industrialization. As a result, the market for turbo expanders is expected to be stimulated due to their utilization in various industrial applications such as refrigeration and energy extraction.

- Therefore, due to the abovementioned points, the Asia-Pacific region is expected to dominate the turbo expander market during the forecasted period.

Turboexpander Industry Overview

The turbo expander market is semi-consolidated. Some of the major players in the market (in no particular order) include Atlas Copco AB, Baker Hughes Company, Cryostar SAS, Nikkiso ADC, and PBS Group., among others

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2028

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increasing Investment in the Adaption of Natural Gas for Power Generation and Fuel for Various Industries

- 4.5.2 Restraints

- 4.5.2.1 Increasing Share of Renewable Energy Sources

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Loading Devices

- 5.1.1 Compressor

- 5.1.2 Generator

- 5.1.3 Hydraulic Brake

- 5.2 End-user Industry

- 5.2.1 Oil and Gas

- 5.2.2 Power Generation

- 5.2.3 Energy Recovery

- 5.2.4 Other End-user Industries

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 France

- 5.3.2.3 United Kingdom

- 5.3.2.4 Italy

- 5.3.2.5 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 Australia

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Chile

- 5.3.4.4 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 South Africa

- 5.3.5.4 Qatar

- 5.3.5.5 Rest of Middle-East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Atlas Copco AB

- 6.3.2 Baker Hughes Company

- 6.3.3 Cryostar SAS

- 6.3.4 Nikkiso ACD

- 6.3.5 PBS Group

- 6.3.6 LA Turbine

- 6.3.7 Elliott Group

- 6.3.8 Blair Engineering

- 6.3.9 Air Products and Chemicals Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Technological Investments in the Market to Produce Energy Efficiently and Control Carbon Emissions