|

市場調查報告書

商品編碼

1429491

環氧塗料:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029)Epoxy Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

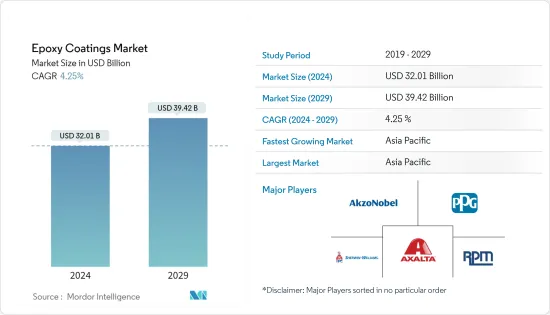

環氧塗料市場規模預計到2024年為320.1億美元,預計到2029年將達到394.2億美元,在預測期內(2024-2029年)複合年成長率為4.25%。

環氧塗料市場受到 COVID-19 大流行的負面影響。汽車和運輸業的低迷、因疫情封鎖而暫時停止的建設活動對相變材料市場的需求產生了負面影響。然而,市場現已達到疫情前的水平,預計在預測期內將穩定成長。

主要亮點

- 推動市場的主要因素是水性環氧塗料的需求不斷增加,而建設產業的成長預計也將增加環氧塗料的市場需求。

- 然而,有關揮發性有機化合物(VOC)排放的嚴格法規預計將阻礙市場成長。

- 引入揮發性有機化合物排放極低或無揮發性有機化合物的環氧樹脂可能是未來的一個機會。

- 環氧塗料消費量最高的亞太地區預計將在預測期內主導全球市場。

環氧塗料市場發展趨勢

建設產業的需求不斷成長

- 環氧塗料主要用於地板、金屬等材料的快乾、防護塗層等。環氧塗料可用作工業和商業地板材料等應用中的環氧地板漆。

- 根據美國人口普查局的數據,2023 年 4 月的建築支出經季節已調整的後的年成長率估計為 19,084 億美元,比 3 月修正後的數字 18,850 億美元高出 1.2%。 4 月的數字比 2022 年 4 月預測的 17,809 億美元高出 7.2%。

- 此外,2023年1月至4月期間的建築支出達到5,667億美元,比2022年同期的5,339億美元成長約6%。

- 德國擁有歐洲大陸最大的建築存量,是歐洲最大的建築市場。德國政府為該國設定的主要目標之一是經濟適用住宅。政府計劃每年建造40萬套住宅,其中10萬套將提供公共補貼。

- 德國也已批准在 2022 年 10 月建造 25,399 套住宅。根據聯邦統計局(Destatis)的數據,與 2021 年 10 月相比,建築許可證數量減少了 4,198 個(14.2%)。此外,2022 年 1 月至 10 月期間總合發放了 297,453 張住宅建築許可證。

- 建築業的擴張和普及預計將成為環氧塗料市場的主要驅動力並推動市場向前發展。

亞太地區主導市場

- 由於建築、汽車、運輸和工業等最終用戶行業的需求不斷成長,預計亞太地區在預測期內將出現最高成長。

- 根據中國國家統計局數據,2022年第四季中國建築業產值預計達到2,760億元人民幣(約400億美元),較上一季(276億美元)成長約50%。隨著國家強調節能結構,相變材料也廣泛應用於建築領域。

- 由於在日本舉辦的活動,預計日本的建築業也會蓬勃發展。例如,2025年將在大阪舉辦世博會。大多數建築的靈感來自於自然災害的復原和重建。東京車站計劃建造兩棟高層建築:一棟37層、高230m的辦公大樓計劃於2021年開業,一棟61層、高390m的辦公大樓計劃於2027年開業。

- 此外,根據印度工商聯合會(FICCI)的數據,到2022年,印度都市區根據PMAY計劃開發和批准的住宅數量預計將分別達到約550萬套和1140萬套。馬蘇。

- 此外,中國還是各類汽車產銷售量最大、最具主導地位的國家。中國工業協會公佈,2022年汽車產量將達2,702萬輛,比2021年的2,608萬輛成長約3.4%。

- 此外,隨著日本汽車產業的擴張,許多汽車製造商增加了在日本的產能。根據日本汽車經銷商協會(JADA)的數據,Toyota2022年在國內銷售了約125萬輛汽車,成為日本最大的汽車製造商。

- 綜上所述,亞太地區環氧塗料市場預計在研究期間將顯著成長。

環氧塗料產業概況

環氧塗料市場得到部分整合。主要企業包括(排名不分先後)PPG Industries, Inc.、AkzoNobel NV、Axalta Coating Systems, LLC、The Sherwin-Williams Company 和 RPM International Inc.。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 調查先決條件

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 促進因素

- 對水性環氧塗料的需求不斷增加

- 建築和建設產業的成長

- 其他司機

- 抑制因素

- 關於VOC排放的嚴格規定

- 其他阻礙因素

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章市場區隔(以金額為準的市場規模)

- 科技

- 水基的

- 溶劑型

- 粉底

- 最終用戶產業

- 建築/施工

- 車

- 運輸

- 工業

- 其他最終用戶產業

- 地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 義大利

- 法國

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東/非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲

- 亞太地區

第6章 競爭形勢

- 併購、合資、聯盟、協議

- 市場佔有率(%)**/排名分析

- 主要企業策略

- 公司簡介

- AkzoNobel NV

- Asian Paints

- Axalta Coating Systems, LLC

- BASF SE

- Berger Paints India Limited

- Dur-A-Flex, Inc.

- The Euclid Chemical Company

- Kansai Paint Co. Ltd

- Koster Bauchemie AG

- Nippon Paint Holdings Co., Ltd.

- Pidilite Industries Limited

- PPG Industries, Inc.

- RPM International Inc.

- The Sherwin-Williams Company

- Tikkurila

- Wanhua

- West Pacific Coatings

第7章 市場機會及未來趨勢

- 介紹具有最小或無 VOC排放的環氧樹脂

- 其他機會

The Epoxy Coatings Market size is estimated at USD 32.01 billion in 2024, and is expected to reach USD 39.42 billion by 2029, growing at a CAGR of 4.25% during the forecast period (2024-2029).

The epoxy coatings market was affected negatively due to the COVID-19 pandemic. The weakening automotive and transportation industry, as well as a brief halt in construction activity owing to the pandemic lockdown, had a detrimental impact on the phase change materials market demand. However, the market has now reached pre-pandemic levels and is expected to grow at a steady pace during the forecast period.

Key Highlights

- The major factors driving the market studied are increasing demand for water-borne epoxy coatings, and growth in the building and construction industry is also expected to increase the market demand for epoxy coatings.

- However, stringent regulations on volatile organic compounds (VOC) emissions are expected to hinder the market's growth.

- The introduction of epoxies with minimal or no VOC emissions is likely to act as an opportunity in the future.

- Asia-Pacific is expected to dominate the global market, with the largest consumption of epoxy coatings during the forecast period.

Epoxy Coatings Market Trends

Increasing Demand from the Building and Construction Industry

- Epoxy coatings are majorly used for quick-drying, protective coating, etc., for floors, metal, and other materials. Epoxy coatings can be used as epoxy floor paints in applications such as industrial or commercial flooring applications.

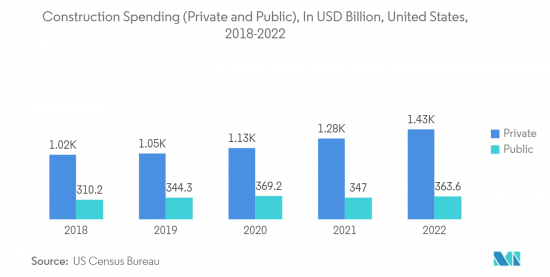

- According to the United States Census Bureau, the construction spending during April 2023 was estimated at a seasonally adjusted annual rate of USD 1,908.4 billion, 1.2 percent above the revised March estimate of USD 1,885.0 billion. The April figure is 7.2 percent above the April 2022 estimate of USD 1,780.9 billion.

- Moreover, during the first four months of 2023, the construction spending amounted to USD 566.7 billion, approximately 6 percent above the USD 533.9 billion spending for the same period in 2022.

- With the largest building stock on the continent, Germany is Europe's largest construction market. One of the main goals the German government established for the nation was affordable housing. The government plans to build 400,000 new housing units every year, 100,000 of which would be publicly subsidized.

- Germany had also given the go-ahead for the construction of 25,399 dwellings for October 2022. In comparison to October 2021, this implies a decrease in building permits of 4,198, or 14.2%, according to the Federal Statistics Office (Destatis). Moreover, a total of 297,453 residential building licenses were issued between January and October 2022.

- The expansion and proliferation of the building and construction sector is anticipated to be the main driver of the market for epoxy coating and thus drive the market forward.

Asia-Pacific Region to Dominate the Market

- Asia-Pacific region is expected to have the highest growth during the forecast period, owing to the increase in demand from the end-user industries, including building and construction, automotive, transportation, industrial, and other industries.

- The fourth quarter of 2022 saw an increase in China's construction output of around 50% over the previous quarter (USD 27.6 billion), reaching an estimated CNY 276 billion (about USD 40 billion), according to the National Bureau of Statistics of China. Due to the nation's emphasis on energy-efficient structures, phase change materials are also widely used in the construction sector.

- The Japanese construction sector is also predicted to boom because of the events that will be held in the nation. For example, in 2025, Osaka will host the World Expo. Most of the building is motivated by rehabilitation and recovery after natural catastrophes. Two high-rise structures for Tokyo Stations, a 37-story, 230m tall office tower scheduled to open in 2021 and a 61-story, 390m tall office tower scheduled to open in 2027.

- Furthermore, the number of residences developed and sanctioned under the PMAY plan in India's urban regions in 2022 was probably around 5.5 million and 11.4 million, respectively, according to the Federation of Indian Chambers of Commerce and Industry (FICCI).

- Furthermore, China has been the largest and most dominant nation in terms of vehicle production and sales of all types. In 2022, automotive production in the country reached 27.02 million units, which increased by approximately 3.4%, compared to 26.08 million vehicles produced in 2021, as stated by the China Association of Automobile Manufacturers.

- Additionally, as Japan's automotive sector is expanding, many automobile manufacturers increased their manufacturing capacity in the nation. According to the Japan Automobile Dealers Association (JADA), Toyota was the largest automobile manufacturer in Japan in 2022, selling around 1.25 million vehicles domestically, followed by Suzuki, which sold slightly more than 600,000 vehicles domestically in the same year.

- Hence, the market for epoxy coatings in the Asia-Pacific region is projected to grow significantly during the study period.

Epoxy Coatings Industry Overview

The epoxy coatings market is partially consolidated in nature. The major companies include (not in any particular order) PPG Industries, Inc., AkzoNobel NV, Axalta Coating Systems, LLC, The Sherwin-Williams Company, RPM International Inc, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand for Water-borne Epoxy Coatings

- 4.1.2 Growing Building and Construction Industry

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Stringent Regulation on VOC Emissions

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Technology

- 5.1.1 Water-based

- 5.1.2 Solvent-based

- 5.1.3 Powder-based

- 5.2 End-user Industry

- 5.2.1 Building and Construction

- 5.2.2 Automotive

- 5.2.3 Transportation

- 5.2.4 Industrial

- 5.2.5 Other End-user Industries

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 AkzoNobel NV

- 6.4.2 Asian Paints

- 6.4.3 Axalta Coating Systems, LLC

- 6.4.4 BASF SE

- 6.4.5 Berger Paints India Limited

- 6.4.6 Dur-A-Flex, Inc.

- 6.4.7 The Euclid Chemical Company

- 6.4.8 Kansai Paint Co. Ltd

- 6.4.9 Koster Bauchemie AG

- 6.4.10 Nippon Paint Holdings Co., Ltd.

- 6.4.11 Pidilite Industries Limited

- 6.4.12 PPG Industries, Inc.

- 6.4.13 RPM International Inc.

- 6.4.14 The Sherwin-Williams Company

- 6.4.15 Tikkurila

- 6.4.16 Wanhua

- 6.4.17 West Pacific Coatings

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Introduction of Epoxies with Minimal or No VOC Emissions

- 7.2 Other Opportunities

2024 年環氧塗料全球市場報告

2024 年環氧塗料全球市場報告 2024 年環氧粉末塗料全球市場報告

2024 年環氧粉末塗料全球市場報告 全球環氧塗料市場:按類型、基材、表面處理、最終用戶 - 預測 2025-2030

全球環氧塗料市場:按類型、基材、表面處理、最終用戶 - 預測 2025-2030 環氧粉末塗料市場:依方法和應用分類-2025-2030年全球預測

環氧粉末塗料市場:依方法和應用分類-2025-2030年全球預測 環氧塗層鋼筋市場:按等級、環氧類型、銷售管道、最終用戶 - 2025-2030 年全球預測

環氧塗層鋼筋市場:按等級、環氧類型、銷售管道、最終用戶 - 2025-2030 年全球預測 全球環氧塗料市場規模、佔有率及趨勢分析報告,依技術(溶劑型、水性和粉末型)、應用(建築、交通、工業等)、區域展望和預測,2024 - 2031

全球環氧塗料市場規模、佔有率及趨勢分析報告,依技術(溶劑型、水性和粉末型)、應用(建築、交通、工業等)、區域展望和預測,2024 - 2031 2023-2030年全球固體環氧塗料市場

2023-2030年全球固體環氧塗料市場 環氧粉末塗料市場規模和份額分析-增長趨勢和預測(2023-2028)

環氧粉末塗料市場規模和份額分析-增長趨勢和預測(2023-2028) 環氧樹脂塗料的全球市場

環氧樹脂塗料的全球市場