|

市場調查報告書

商品編碼

1642044

商業生產力軟體:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Business Productivity Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

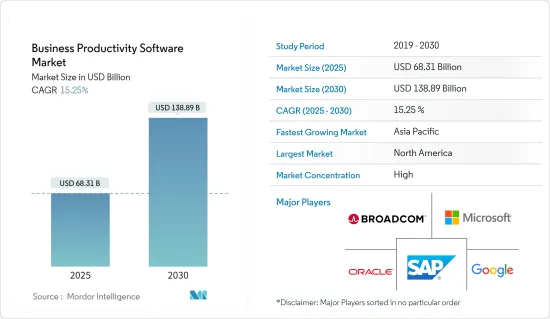

預計 2025 年商業生產力軟體市場規模為 683.1 億美元,到 2030 年將達到 1,388.9 億美元,預測期內(2025-2030 年)的複合年成長率為 15.25%。

可以在世界任何地方即時開展業務。協作工具具有經濟和環境效益,包括降低差旅成本和提高生產力。

主要亮點

- 雖然人工智慧和物聯網正在推動技術進步浪潮,但商業生產力是目前正在興起的商業領域之一。業務生產力可以追溯到組織成功執行其整體策略的能力。此外,企業的生產力與員工的生產力成正比。企業正在廣泛採用各種工具來幫助員工提高工作效率。

- 由於智慧型手機和自帶設備(BYOD)的廣泛使用,行動工作人員的擴大是市場發展的強大推動力。

- 雲端運算和人工智慧引入業務流程將刺激市場。此外,企業產生的資料推動著採用更好的資料管理技術的需求,從而推動市場成長。

- 商業生產力軟體支援並整合您業務各個方面的資料和流程。它還最佳化了雲端處理,幫助您更好地與客戶、供應商、供應商、員工和客戶合作。

- 在疫情期間,各組織都採取了在家工作政策來保障員工的安全。這導致對商業生產力軟體的需求增加,包括調度軟體、協作工具和其他解決方案。

商業生產力軟體市場趨勢

內容管理和協作的採用率最高

- 傳統上,企業內容管理 (ECM) 仍然局限於後勤部門且是非結構化的。然而,近年來,ECM 已轉向在業務中扮演更具互動性的角色。機器學習、雲端技術和行動功能為企業開闢了新的機會。視訊、音訊和社交等新類型的內容正在模糊傳統 ECM 的界限。

- Microsoft SharePoint 提供了許多工具來建立具有強大文件管理和其他 SharePoint 功能的 ECMS。客戶正在尋求與系統和文件管理的強大的內部整合,各種參與者都表示 SharePoint 提供了用於自訂 ECMS 的強大套件。

- 雲端基礎的服務已顯示出透過網路提供經濟高效、靈活、易於管理且權威的資源設施的潛力。雲端基礎的ECM 服務透過最佳共用利用來提高硬體資源的能力。這些特點正在鼓勵組織和個人用戶將其服務和應用程式遷移到雲端。

- 雲端對於文件協作工具至關重要,Office 365 等工具提供雲端協作等功能。現代職場的員工不再只滿足於優厚的薪資和社會福利。他們希望擁有職場。根據銀行控股公司 Capital One 的調查,超過四分之三的員工表示,他們在協作的職場環境中表現較好。隨著自動化趨勢的發展,它的普及度也日益提高,對於尋求解決方案來提供服務的企業來說,它變得更加重要。

- 此外,合規辦公室是針對公共和私人組織提供的易於使用且合規的服務,在提供高安全標準的同時也提供數位創新的機會。在整個歐盟,政界人士、公共部門和行業協會都直言不諱地表示需要雲端服務。關於使用雲端服務的合法性已經有很多討論和爭論。一些公共當局已經進行了風險評估,並主動決定不遵守現行立法。

預計北美將佔據大部分市場佔有率

- 預計北美將主導商業生產力軟體市場。技術進步的快速採用是該市場成長的主要動力。北美是採用雲端運算服務以及採用人工智慧和物聯網方面最成熟的市場,這歸功於多種因素,包括存在許多擁有先進IT基礎設施和技術專長的公司。

- 競爭非常激烈,主要生產力軟體供應商如亞馬遜網路服務公司(美國)、微軟(Office 365)和Google都位於該地區。此外,北美的財政實力使其能夠大量投資先進的解決方案和技術。這些優勢使該地區的組織在市場上具有競爭優勢。

- 由於雲端基礎技術的使用日益增多,生產力管理軟體的市場發展預計將加速。透過連接的設備,雲端基礎的技術可以存取儲存的文件。透過減少員工停工時間並提高生產力,雲端基礎的技術有助於生產力管理。

- 例如,根據美國生產力管理軟體公司Flexera的預測,到2021年,94%的公司將使用雲端基礎的技術進行生產力管理。因此,生產力管理軟體市場將受到雲端基礎的技術日益廣泛的使用的推動。

業務生產力軟體產業概況

商業生產力軟體市場競爭激烈,由幾家大公司組成。目前,只有少數主要參與者佔據市場佔有率。憑藉著壓倒性的市場佔有率,這些大公司正致力於擴大海外基本客群。這些公司正在利用策略合作措施來增加市場佔有率和盈利。

2022年2月,美國軟體新興企業Pendo宣布了其生產力管理計畫Pendo Adopt。該計劃將幫助組織提高員工績效並提高生產力。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場動態

- 市場概況

- 市場促進因素

- 智慧型手機普及率和 BYOD 採用率不斷提高

- 對雲端運算、商業智慧和人工智慧的需求不斷成長

- 資料管理需求日益增加

- 市場限制

- 實施和培訓成本高

- 產業吸引力-波特五力模型

- 供應商的議價能力

- 購買者/消費者的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭強度

- COVID-19 市場影響評估

第5章 市場區隔

- 按部署

- 本地

- 在雲端

- 按組織規模

- 中小企業

- 大型企業

- 按最終用戶產業

- BFSI

- 通訊業

- 製造業

- 媒體與娛樂

- 運輸

- 零售

- 其他最終用戶產業

- 按解決方案

- 內容管理與協作

- 資產管理

- 人工智慧和預測分析

- 工作管理結構

- 其他解決方案

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 世界其他地區

第6章 競爭格局

- 公司簡介

- Microsoft Corporation

- Google LLC

- Oracle Corporation

- Broadcom Inc.(Symantec Corporation)

- SAP SE

- Salesforce.com Inc.

- VMware Inc.

- IBM Corporation

- Amazon.com Inc.

- AppScale Systems Inc.

第7章投資分析

第8章 市場機會與未來趨勢

The Business Productivity Software Market size is estimated at USD 68.31 billion in 2025, and is expected to reach USD 138.89 billion by 2030, at a CAGR of 15.25% during the forecast period (2025-2030).

Business can be conducted from anywhere, across the world, in real-time. Collaboration tools are economically and environmentally helpful, as their benefits include reduced travel costs and increased productivity.

Key Highlights

- While AI and IoT propagate the wave of incoming technology advances, business productivity is one area of business that is currently emerging. Business productivity can be traced to an organization's ability to execute an overall strategy successfully. Moreover, business productivity is directly proportional to employee productivity. Businesses are widely adopting various tools to aid employees in enhancing their productivity.

- The increased adoption of smartphones and bring-your-own devices (BYOD), which have expanded the mobile workforce, are strong drivers in the market.

- Implementing cloud computing or AI in business processes stimulates the market. Moreover, vast data being generated across businesses propels the need for adopting better data management techniques, driving the market's growth.

- Business Productivity Software supports and integrates data and processes in every aspect of the business. It also aids in optimizing cloud computing and helps in better collaboration with clients, vendors, suppliers, employees, and customers.

- Organizations adopted the work-from-home policy during the pandemic to ensure their employees' safety. Thus, the demand for business productivity software, such as scheduling software, collaboration tools, and other solutions, increased.

Business Productivity Software Market Trends

Content Management and Collaboration to have the Highest Adoption Rate

- Traditionally, enterprise content management (ECM) was confined to the back office and remained unstructured. However, over the past few years, ECM shifted toward a more interactive role in businesses. Machine learning, cloud technology, and mobile capability presented new opportunities for businesses. New types of content, including video, audio, and social, blur the lines of a traditional ECM.

- Microsoft SharePoint offers many tools to build an ECMS with solid document management and other SharePoint facilities. Customers look for strong internal integration with systems and document management, and as per various players, SharePoint offers a strong toolkit for customizing an ECMS.

- The cloud-based services exhibit the potential to provide cost-effective, flexible, easy-to-manage, and authoritative resource facilities over the internet. Cloud-based ECM services upsurge the capabilities of hardware resources through optimal and shared utilization. These features encourage organizations and individual users to shift their services and applications to the cloud.

- Cloud is essential for document collaboration tools, and tools like Office 365 provide features such as cloud collaboration. Employees in the modern workplace no longer accept adequate pay and perks as sufficient. They seek out working places where they may advance their careers and learn. Over 3/4 of workers, according to a study by Capital One, a bank holding company, perform better in collaborative work environments. The penetration rate is also increasing with automation trends, which has become increasingly important for enterprises looking for solutions offering services.

- Further, Compliant Office is an easy-to-use and regulatory-compliant service for both public and private sector organizations, which features high-security standards while still providing opportunities for digital innovation. Across the EU, politicians, the public sector, and industry organizations have been very vocal about their need for cloud services. There has been much debate and discussion about the legality of their usage. Some public organizations even conducted their risk assessments and actively decided not to comply with current legislation.

North America is Expected to Hold a Majority Share

- North America is expected to dominate the business productivity software market. The early adoption of technological advancements has majorly driven the growth in this market. North America is the most mature market in terms of cloud computing services adoption or AI and IoT adoption due to several factors, such as the presence of many enterprises with advanced IT infrastructure and the availability of technical expertise.

- The major productivity software vendors, like Amazon Web Services Inc. (US), Microsoft (Office 365), Google, etc., are based in this region, so there is strong competition. Also, North America's strong financial position enables it to invest heavily in advanced solutions and technologies. These advantages have provided regional organizations with a competitive edge in the market.

- The market for productivity management software is anticipated to develop due to the rise in cloud-based technology use. Through connected devices, cloud-based technology offers access to stored files. By decreasing employee downtime and increasing productivity, cloud-based technology aids in the management of productivity.

- For instance, 94% of businesses will use cloud-based technology for productivity management in 2021, according to Flexera, a US-based company that makes productivity management software. As a result, the market for productivity management software is driven by the growth in the usage of cloud-based technologies.

Business Productivity Software Industry Overview

The business productivity software market is highly competitive and consists of several major players. Few of the major players currently dominate the market share. These major players with a prominent market share focus on expanding their customer base across foreign countries. These companies leverage strategic collaborative initiatives to increase their market share and profitability.

In February 2022, a US-based software startup called Pendo introduced Pendo Adopt, a productivity management program. This program aids an organization's staff to improve their performance, which raises productivity.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increase in Smartphone Penetration and Increased Adoption of BYOD

- 4.2.2 Growing Demand for Cloud Computing, Business Intelligence, and AI

- 4.2.3 Growing Need for Data Management

- 4.3 Market Restraints

- 4.3.1 High Installation and Training Costs

- 4.4 Industry Attractiveness - Porter Five Forces

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

- 4.5 Assessment of the Impact of COVID-19 on the Market

5 MARKET SEGMENTATION

- 5.1 Deployment

- 5.1.1 On-premise

- 5.1.2 On-cloud

- 5.2 Organization Size

- 5.2.1 Small and Medium Enterprises

- 5.2.2 Large Enterprises

- 5.3 End User Industry

- 5.3.1 BFSI

- 5.3.2 Telecommunication

- 5.3.3 Manufacturing

- 5.3.4 Media and Entertainment

- 5.3.5 Transportation

- 5.3.6 Retail

- 5.3.7 Other End User Industries

- 5.4 Solutions

- 5.4.1 Content Management and Collaboration

- 5.4.2 Asset Creation

- 5.4.3 AI and Predictive Analytics

- 5.4.4 Structured Work Management

- 5.4.5 Other Solutions

- 5.5 Geography

- 5.5.1 North America

- 5.5.2 Europe

- 5.5.3 Asia Pacific

- 5.5.4 Rest of the World

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Microsoft Corporation

- 6.1.2 Google LLC

- 6.1.3 Oracle Corporation

- 6.1.4 Broadcom Inc. (Symantec Corporation)

- 6.1.5 SAP SE

- 6.1.6 Salesforce.com Inc.

- 6.1.7 VMware Inc.

- 6.1.8 IBM Corporation

- 6.1.9 Amazon.com Inc.

- 6.1.10 AppScale Systems Inc.