|

市場調查報告書

商品編碼

1439877

固化劑 - 市場佔有率分析、產業趨勢與統計、成長預測(2024 - 2029)Curing Agent - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

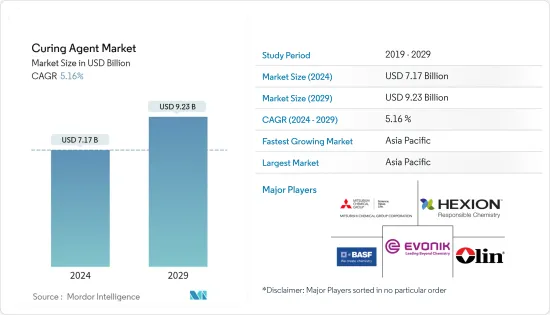

固化劑市場規模預計到2024年為71.7億美元,預計到2029年將達到92.3億美元,在預測期內(2024-2029年)CAGR為5.16%。

固化劑市場受到了 COVID-19 大流行的負面影響,因為生產和流動性放緩,其中油漆和塗料、建築等行業由於遏制措施和經濟狀況而被迫推遲生產。目前,市場已從疫情中恢復過來。市場於2022年達到疫情前水準,預計未來將穩定成長。

油漆和塗料以及建築行業不斷成長的需求預計將推動市場成長。

然而,與固化劑相關的嚴格環境法規(目的是減少揮發性有機化合物(VOC)排放)預計將阻礙市場擴張。

環保型低揮發性有機化合物或無揮發性有機化合物製劑的開發預計將為市場蓬勃發展提供機會。

亞太地區主導了全球市場,其中中國、印度和日本等國家是最大的消費國。

固化劑市場趨勢

建築業對環氧固化劑的需求不斷成長

- 在固化劑中,環氧固化劑用於多種應用,預計在預測期內將佔據最大的市場佔有率。

- 在建築業中,環氧固化劑用於生產具有耐環境性和卓越強度的熱固性黏合劑。

- 環氧固化劑用於開發用於建築的輕量複合材料,以提供建築基礎設施並克服施工挑戰。

- 環氧樹脂作為底漆、密封劑和防水劑廣泛用於保護混凝土免受潮濕。環氧樹脂用於固化混凝土,因為它們為混凝土提供了良好的附著力、快速乾燥和高機械強度。

- 根據牛津經濟研究院的資料,到2025年,全球建築業預計將達到 13.3 兆美元,從2020年起的五年增加產值 2.6 兆美元。

- 亞太地區的建築業是世界上最大的。由於中國和印度住房建設市場的不斷擴大,預計亞太地區的住房成長將達到最高。預計到2030年,這兩個地區將佔全球中產階級的 43.3%以上。

- 此外,根據中國國家統計局的資料,中國建築業產值在2022年達到峰值,約4.11兆美元。結果,這些因素往往會增加市場需求。

- 因此,由於上述因素,預計所研究的市場在預測期內將顯著成長。

亞太地區將主導市場

- 由於中國、印度、日本等主要國家的油漆塗料、黏合劑、建築等行業不斷擴大,預計亞太地區將在預測期內佔據最大的固化劑市場。

- 固化劑用於底漆、粉末塗料和面漆配方、輕量複合材料、砂漿、電氣鑄件等的生產。由於其水下固化,甚至適合海洋應用。

- 固化劑因其廣泛的性能而可用於多種應用,例如低溫或高溫固化、可變的適用期、更高的強度和優異的耐腐蝕性。

- 據中國塗料工業協會表示,亞太地區仍然是塗料行業的主要成長動力。中國擁有1000多家塗料企業,已成為該產業的主要參與者。

- 這種成長吸引了全球領先的塗料製造商的投資,如Nippon Paint、AkzoNobel、 Chugoku Marine Paints、PPG Industries、BASF和Axalta Coatings,這些製造商都在中國建立了製造基地。

- 2022年7月,BASF歐洲公司透過其子公司BASF塗料(廣東)(BCG)在華南廣東省江門市的塗料基地擴大了汽車修補漆的生產能力。透過本次擴建計畫,公司產能達年3萬噸。

- 此外,印度油漆和塗料行業在過去二十年也取得了顯著成長。該產業擁有 3,000 多家塗料製造商,全球主要企業均在該國開展業務。

- 2023年 1月,亞洲塗料批准投資200 億印度盧比(2.4053 億美元)在印度中央邦新建一座年產能 4 億公升的水性塗料製造廠。該工廠的生產預計將在三年內投入使用。

- 因此,上述因素顯示亞太市場建築業的成長對預測期內的研究市場產生了正面影響。

固化劑產業概況

固化劑市場本質上是部分分散的。研究市場的主要參與者(排名不分先後)包括BASF SE、Hexion、Olin Corporation、三菱化學公司和Evonik Industries AG等。

附加優惠:

- Excel 格式的市場估算(ME)表

- 3 個月的分析師支持

目錄

第1章 簡介

- 研究假設

- 研究範圍

第2章 研究方法

第3章 執行摘要

第4章 市場動態

- 促進要素

- 油漆和塗料行業的需求不斷成長

- 建築業對環氧固化劑的需求不斷成長

- 其他促進要素

- 限制

- 嚴格的環境法規

- 其他限制

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 替代產品和服務的威脅

- 競爭程度

第5章 市場區隔(市場價值規模)

- 類型

- 環氧樹脂

- 聚氨酯

- 橡皮

- 丙烯酸纖維

- 其他類型(矽膠等)

- 依應用

- 建築與施工

- 複合材料

- 油漆和塗料

- 黏合劑和密封劑

- 電氣和電子

- 其他應用(風能等)

- 地理

- 亞太

- 中國

- 印度

- 日本

- 韓國

- 亞太其他地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 義大利

- 法國

- 歐洲其他地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 中東和非洲其他地區

- 亞太

第6章 競爭格局

- 併購、合資、合作與協議

- 市佔率(%)**/排名分析

- 領先企業採取的策略

- 公司簡介

- Alfa Chemicals

- BASF SE

- Cardolite Corporation

- DIC Corporation

- Evonik Industries AG

- Hexion

- Huntsman International LLC

- Mitsubishi Chemical Corporation

- Olin Corporation

- Supreme Polytech Pvt. Ltd.

第7章 市場機會與未來趨勢

- 環保低VOC或無VOC固化劑的開發

- 其他機會

The Curing Agent Market size is estimated at USD 7.17 billion in 2024, and is expected to reach USD 9.23 billion by 2029, growing at a CAGR of 5.16% during the forecast period (2024-2029).

The curing agent market was negatively impacted by the COVID-19 pandemic as there was a slowdown in production and mobility wherein industries, such as paints and coatings, building and construction, etc., were forced to delay their production due to containment measures and economic disruptions. Currently, the market has recovered from the pandemic. The market reached pre-pandemic levels in 2022 and is expected to grow steadily in the future.

The increasing demand from the paints and coatings and building and construction industries is expected to fuel market growth.

However, stringent environmental regulations associated with curing agents to reduce volatile organic compounds (VOC) emissions are anticipated to hamper market expansion.

The development of environmentally friendly low or non-VOC agents is expected to provide opportunities for the market to flourish.

The Asia-Pacific region dominated the market around the world, with countries like China, India, and Japan being the biggest consumers.

Curing Agent Market Trends

Growing Demand for Epoxy Curing Agents In Building and Construction Industry

- Among curing agents, epoxy curing agents are used for a variety of applications and are expected to account for the largest share of the market during the forecast period.

- In the construction industry, epoxy curing agents are used to produce thermosetting adhesives that provide environmental resistance and superior strength.

- Epoxy curing agents are used to develop lightweight composites for building and construction to provide architectural infrastructure and overcome construction challenges.

- Epoxy resins as primers, sealers, and waterproofing agents are extensively used to protect concrete from moisture. Epoxy resins are used in curing concrete as they provide great adhesion, fast drying, and high mechanical strength to concrete.

- According to Oxford Economics, the global construction industry is expected to reach USD 13.3 trillion by 2025 - adding USD 2.6 trillion to output in five years from 2020.

- The construction sector in the Asia-Pacific region is the largest in the world. The highest growth for housing is expected to be registered in the Asia-Pacific region, owing to the expanding housing construction markets in China and India. These two regions are expected to represent over 43.3% of the global middle class by 2030.

- Also, according to the National Bureau of Statistics of China, China's construction output peaked in 2022 at about USD 4.11 trillion. As a result, these factors tend to increase the market demand.

- Therefore, owing to such factors mentioned above, the studied market is expected to grow significantly during the forecast period.

Asia-Pacific Region to Dominate the Market

- The Asia-Pacific region is expected to account for the largest market for curing agents during the forecast period owing to the expanding industries such as paints and coatings, adhesives, construction, etc., in major countries such as China, India, Japan, etc.

- Curing agents are used in primer, powder coating, and topcoat formulations, production of lightweight composites, mortars, electrical castings, and many more. They are even suitable for marine applications because of their underwater cure.

- Curing agents can be used for a variety of applications because of their wide range of properties, such as low or high-temperature cure, variable pot life, higher strength, and excellent corrosion resistance.

- According to the China Paint Industry Association, Asia-Pacific continues to be a major growth driver for the coatings industry. With more than 1000 coating companies in operation, China has become a major player in the industry.

- This growth has attracted investments from leading global coating manufacturers such as Nippon Paint, AkzoNobel, Chugoku Marine Paints, PPG Industries, BASF SE, and Axalta Coatings, which have established manufacturing bases in China.

- In July 2022, BASF SE, through its subsidiary BASF Coatings (Guangdong) Co., Ltd. (BCG), expanded its manufacturing capabilities for automotive refinish coatings at its coatings site in Jiangmen, Guangdong Province in South China. The company increased its production capacity to 30,000 tons annually through this expansion project.

- Further, the Indian paint and coatings industry also witnessed significant growth over the past two decades. The industry comprises more than 3,000 paint manufacturers, with the presence of major global players in the country.

- In January 2023, Asian Paints approved an investment of INR 20 billion (USD 240.53 million) for a new waterborne paint manufacturing plant with 400 million liters per annum capacity in Madhya Pradesh, India. The facility's manufacturing is expected to be commissioned in three years.

- Therefore, the factors mentioned above indicate a positive influence of the growing construction industry in the Asia-Pacific market on the studied market over the forecast period.

Curing Agent Industry Overview

The curing agent market is partially fragmented in nature. The major players in the studied market (not in any particular order) include BASF SE, Hexion, Olin Corporation, Mitsubishi Chemical Corporation, and Evonik Industries AG, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand from the Paints and Coatings Industry

- 4.1.2 Growing Demand for Epoxy Curing Agents in Building and Construction Industry

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Stringent Environmental Regulations

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Type

- 5.1.1 Epoxy

- 5.1.2 Polyurethane

- 5.1.3 Rubber

- 5.1.4 Acrylic

- 5.1.5 Other Types (Silicone, etc.)

- 5.2 By Application

- 5.2.1 Building and Construction

- 5.2.2 Composites

- 5.2.3 Paints and Coatings

- 5.2.4 Adhesives and Sealants

- 5.2.5 Electrical and Electronics

- 5.2.6 Other Applications (Wind Energy, etc.)

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Alfa Chemicals

- 6.4.2 BASF SE

- 6.4.3 Cardolite Corporation

- 6.4.4 DIC Corporation

- 6.4.5 Evonik Industries AG

- 6.4.6 Hexion

- 6.4.7 Huntsman International LLC

- 6.4.8 Mitsubishi Chemical Corporation

- 6.4.9 Olin Corporation

- 6.4.10 Supreme Polytech Pvt. Ltd.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Development of Environmental Friendly Low or Non-VOC Curing Agents

- 7.2 Other Opportunities

B-羥烷基醯胺的全球市場:實際成果與預測(2019年~2030年)

B-羥烷基醯胺的全球市場:實際成果與預測(2019年~2030年) B-羥基烷基醯胺市場報告:至2030年的趨勢、預測與競爭分析

B-羥基烷基醯胺市場報告:至2030年的趨勢、預測與競爭分析 固化劑市場:按類型、應用分類 - 2025-2030 年全球預測

固化劑市場:按類型、應用分類 - 2025-2030 年全球預測 全球固化劑市場(2024-2028)

全球固化劑市場(2024-2028) 固化劑市場,按類型、形式、應用、最終用戶、國家和地區 - 2024-2032 年行業分析、市場規模、市場佔有率和預測

固化劑市場,按類型、形式、應用、最終用戶、國家和地區 - 2024-2032 年行業分析、市場規模、市場佔有率和預測 固化劑市場規模、佔有率和趨勢分析報告:按類型、最終用途、地區、細分市場預測,2024-2030 年

固化劑市場規模、佔有率和趨勢分析報告:按類型、最終用途、地區、細分市場預測,2024-2030 年 固化劑市場- 按類型(環氧樹脂、聚氨酯、橡膠、丙烯酸)、按功能、按應用(油漆和塗料、電氣和電子、風能、建築和施工、複合材料、粘合劑和密封劑)和預測,2024 - 2032 年

固化劑市場- 按類型(環氧樹脂、聚氨酯、橡膠、丙烯酸)、按功能、按應用(油漆和塗料、電氣和電子、風能、建築和施工、複合材料、粘合劑和密封劑)和預測,2024 - 2032 年 全球固化劑市場

全球固化劑市場