|

市場調查報告書

商品編碼

1693647

商用車-市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Commercial Vehicles - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

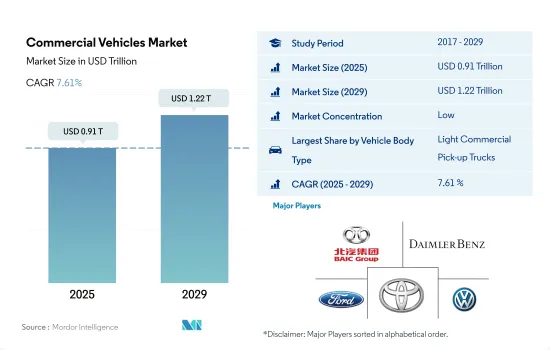

預計 2025 年商用車市場規模將達到 9,100 億美元,到 2029 年預計將達到 12,200 億美元,預測期內(2025-2029 年)的複合年成長率為 7.61%。

- 新興經濟體工業部門的成長和商業物流活動的活性化是商用車需求的主要驅動力。需求激增的主要驅動力是建築業和電子商務行業的擴張,這推動了對高效物料運輸的需求。商用車產量在2020年下降300萬輛之後將有所回升,2021年將達到約2,320萬輛,呈現穩定復甦的態勢。

- 由於新冠疫情導致大多數國際邊境關閉,商用車製造業在 2021 年面臨長期供應鏈中斷,阻礙了市場成長。疫情對交通運輸業的影響巨大,對貨運業和製造業保障貨物的暢通都造成了重大障礙。

- 由於對商用車的需求不斷增加,卡車製造商正在推出新的先進卡車以滿足日益成長的需求和排放法規。商用車租賃行業也因對業務效率的需求增加以及跨行業公司實現規模經濟而成長。近年來,電子商務已成為全球零售業不可或缺的一部分。 2020年,超過20億人在網路上購買商品和服務,當年全球電子商務銷售額超過4.2兆美元。預計未來幾年整個商用車市場將經歷顯著成長。

人們對運輸業二氧化碳排放的日益擔憂預計將在未來幾年推動電動商用車的普及。

- 2021年,全球商用車產量回升,繼2020年下降300萬輛之後,達到約2,320萬輛。輕型商用車通常被歸類為重量在3.5噸以下的車輛。廣義上,商用車是指任何用於運輸貨物或人員的機動車輛。北美將在產量方面處於領先地位,2021 年將生產 1,090 萬輛商用車。亞洲和大洋洲已成為重型卡車的最大生產地,預計 2021 年產量將達到 330 萬輛左右。汽車產業對清潔能源的需求不斷成長是這一領域的一個顯著成長要素。

- 全球商用車產量在 2019 年至 2020 年期間下降了 13% 之後,於 2021 年復甦。全球商用車市場在疫情期間面臨重大中斷,由於持續到 2020 年的國家封鎖,製造設施陷入停頓。雖然 2021 年需求和產量有所恢復,但由於全球晶片短缺導致產量削減,市場面臨挫折。

- 隨著人們對交通運輸業二氧化碳排放的擔憂日益加劇,商用車產業正在優先考慮替代燃料來源。世界各國政府正帶頭實施法規,鼓勵廣泛採用電動車。中國、印度、法國和英國已宣布計劃在 2040 年停止生產汽油和柴油汽車。預計這一轉變將在未來幾年推動電動商用車的普及。

全球商用車市場趨勢

全球需求成長和政府支持將推動電動車市場成長

- 電動車(EV)已成為汽車產業的重要組成部分,因為它具有提高能源效率、減少溫室氣體和污染排放的潛力。這種快速成長背後的主要因素是日益成長的環境問題和政府的支持政策。其中,電動車全球銷售呈現強勁成長勢頭,2022年較2021年成長10.82%。據預測,2025年底,電動乘用車年銷量將超過500萬輛,約佔汽車總銷量的15%。

- 領先的製造商和組織(例如倫敦警察廳和消防隊)正在積極推行電動車策略。例如,該公司設定了在 2025 年實現零排放汽車、在 2030 年實現 40% 貨車電氣化、到 2040 年實現全電動化的目標。預計全球也將出現類似的趨勢,2024 年至 2030 年間電動車的需求和銷售量將急劇成長。

- 在電池技術和汽車電氣化進步的推動下,亞太地區和歐洲有望主導電動車生產。 2020年5月,起亞汽車歐洲公司公佈“S計劃”,宣布轉向電動化策略。這項決定是在起亞電動車在歐洲創下銷售紀錄之際做出的。起亞有一個雄心勃勃的計劃,到 2025 年在全球推出 11 款電動車,涵蓋轎車、SUV 和 MPV 等各個領域。該公司的目標是到 2026 年實現全球電動車年銷量達到 50 萬輛。

商用車行業概況

商用車市場較為分散,前五大企業佔30%的市佔率。該市場的主要企業包括北京汽車股份有限公司、戴姆勒股份公司(梅賽德斯-奔馳股份公司)、福特汽車公司、豐田汽車公司、大眾汽車公司等。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章執行摘要和主要發現

第2章 報告要約

第3章 引言

- 研究假設和市場定義

- 研究範圍

- 調查方法

第4章 產業主要趨勢

- 人口

- 非洲

- 亞太地區

- 歐洲

- 中東

- 北美洲

- 南美洲

- 人均GDP

- 非洲

- 亞太地區

- 歐洲

- 中東

- 北美洲

- 南美洲

- 消費者汽車購買支出(cvp)

- 非洲

- 亞太地區

- 歐洲

- 中東

- 北美洲

- 南美洲

- 通貨膨脹率

- 非洲

- 亞太地區

- 歐洲

- 中東

- 北美洲

- 南美洲

- 汽車貸款利率

- 電氣化的影響

- 電動車充電站

- 電池組價格

- 非洲

- 亞太地區

- 歐洲

- 中東

- 北美洲

- 南美洲

- 新款 Xev 車型發布

- 物流績效指數

- 非洲

- 亞太地區

- 歐洲

- 中東

- 北美洲

- 南美洲

- 燃油價格

- 製造商生產統計

- 法律規範

- 價值鍊和通路分析

第5章市場區隔

- 汽車模型

- 商用車

- 大型商用卡車

- 輕型商用皮卡車

- 輕型商用廂型車

- 中型商用卡車

- 商用車

- 推進類型

- 混合動力和電動車

- 按燃料類別

- BEV

- FCEV

- HEV

- PHEV

- 內燃機

- 按燃料類別

- 天然氣

- 柴油引擎

- 汽油

- LPG

- 混合動力和電動車

- 按地區

- 非洲

- 亞太地區

- 澳洲

- 中國

- 印度

- 印尼

- 日本

- 馬來西亞

- 韓國

- 泰國

- 其他亞太地區

- 歐洲

- 捷克共和國

- 中東

- 北美洲

- 加拿大

- 南美洲

第6章競爭格局

- 關鍵策略趨勢

- 市場佔有率分析

- 商業狀況

- 公司簡介

- BAIC Motor Corporation Ltd.

- BYD Auto Co. Ltd.

- Daimler AG(Mercedes-Benz AG)

- Dongfeng Motor Corporation

- Ford Motor Company

- General Motors Company

- Groupe Renault

- Mahindra & Mahindra Limited

- Nissan Motor Co. Ltd.

- Rivian Automotive Inc.

- Saic General Motors Corporation Limited

- Scania AB

- Tata Motors Limited

- Toyota Motor Corporation

- Volkswagen AG

- Volvo Group

第7章:CEO面臨的關鍵策略問題

第 8 章 附錄

- 世界概況

- 概述

- 五力分析框架

- 全球價值鏈分析

- 市場動態(DRO)

- 資訊來源及延伸閱讀

- 圖片列表

- 關鍵見解

- 數據包

- 詞彙表

簡介目錄

Product Code: 93035

The Commercial Vehicles Market size is estimated at 0.91 trillion USD in 2025, and is expected to reach 1.22 trillion USD by 2029, growing at a CAGR of 7.61% during the forecast period (2025-2029).

- The industrial sector's growth in emerging economies and the rise in commercial logistics activities are key drivers of the demand for commercial vehicles. This demand surge is primarily fueled by the expanding construction and e-commerce industries, which are driving the need for efficient material transportation. Following a dip of three million units in 2020, the production of commercial vehicles rebounded, reaching approximately 23.2 million units in 2021, marking a steady recovery.

- With most international borders closed due to the COVID-19 pandemic, the commercial vehicle manufacturing industry faced prolonged disruptions in its supply chain in 2021, hampering market growth. The pandemic's impact on the transportation sector was profound, presenting significant hurdles for both the freight and manufacturing industries in ensuring smooth movement of goods.

- Due to increased demand for commercial vehicles, truck manufacturers have been introducing new advanced trucks to meet the rising demand and emission standards. Commercial vehicle leasing and the rental industry are also growing due to the increasing demand for operational efficiencies and the realization of economies of scale by businesses across multiple industries. E-commerce has become an essential component of the global retail framework in recent years. Over 2 billion people purchased goods or services online in 2020, and global e-commerce sales surpassed USD 4.2 trillion in the same year. The overall commercial vehicle market is expected to grow significantly in the future.

The rising concerns over carbon emissions from the transportation sector are expected to drive the penetration of electric commercial vehicles in the coming years

- In 2021, global commercial vehicle manufacturing rebounded, reaching approximately 23.2 million units, following a decline of 3 million units in 2020. Light commercial vehicles, typically weighing under 3.5 tons, are classified as such. Broadly, commercial vehicles refer to motor vehicles designed for transporting goods and people. North America took the lead in production, manufacturing 10.9 million commercial vehicles in 2021. Asia and Oceania emerged as the top producers of heavy trucks, with an estimated output of nearly 3.3 million units in 2021. A notable growth driver for this sector is the increasing demand for clean energy in the automotive industry.

- After a 13% dip from 2019 to 2020, global commercial vehicle output rebounded in 2021. The global commercial vehicles market faced significant disruptions during the pandemic, with manufacturing facilities shutting down due to national lockdowns that extended into 2020. Although the demand and output recovered in 2021, the market faced a setback due to a global chip shortage, leading to production cutbacks.

- Amid the rising concerns over carbon emissions from the transportation sector, the commercial fleet industry is prioritizing alternative fuel sources. Governments worldwide are taking the lead in implementing regulations to promote electric vehicle adoption. China, India, France, and the United Kingdom have announced plans to halt gasoline and diesel vehicle production by 2040. This shift is expected to drive the penetration of electric commercial vehicles in the coming years.

Global Commercial Vehicles Market Trends

The rising global demand and government support propel electric vehicle market growth

- Electric vehicles (EVs) have become indispensable in the automotive industry, driven by their potential to enhance energy efficiency and reduce greenhouse gas and pollution emissions. This surge is primarily attributed to growing environmental concerns and supportive government initiatives. Notably, global EV sales witnessed a robust 10.82% growth in 2022 compared to 2021. Projections indicate that annual sales of electric passenger cars will surpass 5 million by the end of 2025, accounting for approximately 15% of total vehicle sales.

- Leading manufacturers and organizations, like the London Metropolitan Police & Fire Service, have been actively pursuing their electric mobility strategies. For instance, they have set a target of a zero-emission fleet by 2025, with a goal of electrifying 40% of their vans by 2030 and achieving full electrification by 2040. Similar trends are expected globally, with the period from 2024 to 2030 witnessing a surge in demand and sales of electric vehicles.

- Asia-Pacific and Europe are poised to dominate electric vehicle production, driven by their advancements in battery technology and vehicle electrification. In May 2020, Kia Motors Europe unveiled its "Plan S," signaling a strategic shift toward electrification. This decision came on the heels of record-breaking sales of Kia's EVs in Europe. Kia has ambitious plans to introduce 11 EV models globally by 2025, spanning various segments like passenger vehicles, SUVs, and MPVs. The company aims to achieve annual global EV sales of 500,000 by 2026.

Commercial Vehicles Industry Overview

The Commercial Vehicles Market is fragmented, with the top five companies occupying 30%. The major players in this market are BAIC Motor Corporation Ltd., Daimler AG (Mercedes-Benz AG), Ford Motor Company, Toyota Motor Corporation and Volkswagen AG (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Population

- 4.1.1 Africa

- 4.1.2 Asia-Pacific

- 4.1.3 Europe

- 4.1.4 Middle East

- 4.1.5 North America

- 4.1.6 South America

- 4.2 GDP Per Capita

- 4.2.1 Africa

- 4.2.2 Asia-Pacific

- 4.2.3 Europe

- 4.2.4 Middle East

- 4.2.5 North America

- 4.2.6 South America

- 4.3 Consumer Spending For Vehicle Purchase (cvp)

- 4.3.1 Africa

- 4.3.2 Asia-Pacific

- 4.3.3 Europe

- 4.3.4 Middle East

- 4.3.5 North America

- 4.3.6 South America

- 4.4 Inflation

- 4.4.1 Africa

- 4.4.2 Asia-Pacific

- 4.4.3 Europe

- 4.4.4 Middle East

- 4.4.5 North America

- 4.4.6 South America

- 4.5 Interest Rate For Auto Loans

- 4.6 Impact Of Electrification

- 4.7 EV Charging Station

- 4.8 Battery Pack Price

- 4.8.1 Africa

- 4.8.2 Asia-Pacific

- 4.8.3 Europe

- 4.8.4 Middle East

- 4.8.5 North America

- 4.8.6 South America

- 4.9 New Xev Models Announced

- 4.10 Logistics Performance Index

- 4.10.1 Africa

- 4.10.2 Asia-Pacific

- 4.10.3 Europe

- 4.10.4 Middle East

- 4.10.5 North America

- 4.10.6 South America

- 4.11 Fuel Price

- 4.12 Oem-wise Production Statistics

- 4.13 Regulatory Framework

- 4.14 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

- 5.1 Vehicle Type

- 5.1.1 Commercial Vehicles

- 5.1.1.1 Heavy-duty Commercial Trucks

- 5.1.1.2 Light Commercial Pick-up Trucks

- 5.1.1.3 Light Commercial Vans

- 5.1.1.4 Medium-duty Commercial Trucks

- 5.1.1 Commercial Vehicles

- 5.2 Propulsion Type

- 5.2.1 Hybrid and Electric Vehicles

- 5.2.1.1 By Fuel Category

- 5.2.1.1.1 BEV

- 5.2.1.1.2 FCEV

- 5.2.1.1.3 HEV

- 5.2.1.1.4 PHEV

- 5.2.2 ICE

- 5.2.2.1 By Fuel Category

- 5.2.2.1.1 CNG

- 5.2.2.1.2 Diesel

- 5.2.2.1.3 Gasoline

- 5.2.2.1.4 LPG

- 5.2.1 Hybrid and Electric Vehicles

- 5.3 Region

- 5.3.1 Africa

- 5.3.2 Asia-Pacific

- 5.3.2.1 Australia

- 5.3.2.2 China

- 5.3.2.3 India

- 5.3.2.4 Indonesia

- 5.3.2.5 Japan

- 5.3.2.6 Malaysia

- 5.3.2.7 South Korea

- 5.3.2.8 Thailand

- 5.3.2.9 Rest-of-APAC

- 5.3.3 Europe

- 5.3.3.1 Czech Republic

- 5.3.4 Middle East

- 5.3.5 North America

- 5.3.5.1 Canada

- 5.3.6 South America

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 BAIC Motor Corporation Ltd.

- 6.4.2 BYD Auto Co. Ltd.

- 6.4.3 Daimler AG (Mercedes-Benz AG)

- 6.4.4 Dongfeng Motor Corporation

- 6.4.5 Ford Motor Company

- 6.4.6 General Motors Company

- 6.4.7 Groupe Renault

- 6.4.8 Mahindra & Mahindra Limited

- 6.4.9 Nissan Motor Co. Ltd.

- 6.4.10 Rivian Automotive Inc.

- 6.4.11 Saic General Motors Corporation Limited

- 6.4.12 Scania AB

- 6.4.13 Tata Motors Limited

- 6.4.14 Toyota Motor Corporation

- 6.4.15 Volkswagen AG

- 6.4.16 Volvo Group

7 KEY STRATEGIC QUESTIONS FOR VEHICLES CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

02-2729-4219

+886-2-2729-4219

東協商用車:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

東協商用車:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 商用車空氣懸吊系統市場(按車輛類型、零件類型、技術、應用和分銷管道分類)-2026-2032年全球預測

商用車空氣懸吊系統市場(按車輛類型、零件類型、技術、應用和分銷管道分類)-2026-2032年全球預測 商用車市場-全球產業規模、佔有率、趨勢、機會和預測,按車輛類型、應用類型、動力類型、地區和競爭格局分類,2021-2031年預測

商用車市場-全球產業規模、佔有率、趨勢、機會和預測,按車輛類型、應用類型、動力類型、地區和競爭格局分類,2021-2031年預測 日本商用車市場報告(按車輛類型(巴士、重型商用卡車、輕型商用皮卡、輕型商用廂型車、中型商用卡車)、引擎類型(混合動力和電動車、內燃機)和地區分類,2026-2034 年)

日本商用車市場報告(按車輛類型(巴士、重型商用卡車、輕型商用皮卡、輕型商用廂型車、中型商用卡車)、引擎類型(混合動力和電動車、內燃機)和地區分類,2026-2034 年) 人工智慧及其在商用車市場的應用,全球(2024-2029)

人工智慧及其在商用車市場的應用,全球(2024-2029) 2025年全球商用車市場報告

2025年全球商用車市場報告 2025-2029年全球商用車市場2025 年至 2033 年商用車市場規模、佔有率、趨勢及預測(按車型、推進類型、最終用途和地區分類)

2025-2029年全球商用車市場2025 年至 2033 年商用車市場規模、佔有率、趨勢及預測(按車型、推進類型、最終用途和地區分類) 商用車市場:依產品、最終用途及地區分類亞太商用車:市場佔有率分析、產業趨勢與成長預測(2025-2030 年)

商用車市場:依產品、最終用途及地區分類亞太商用車:市場佔有率分析、產業趨勢與成長預測(2025-2030 年)

▼