|

市場調查報告書

商品編碼

1849958

Glyphosate:市場佔有率分析、行業趨勢、統計數據、成長預測(2025-2030 年)Glyphosate - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

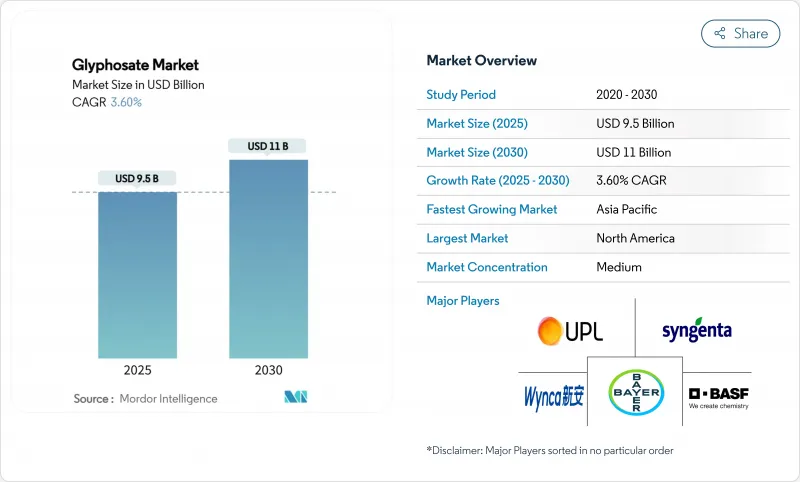

全球Glyphosate市場預計到 2025 年將達到 95 億美元,到 2030 年將達到 110 億美元,複合年成長率為 3.6%。

Glyphosate的穩定需求反映了其在保護性耕作、大規模連作系統以及與碳權相關的犁地項目中的既有地位。北美地區早期推廣耐除草劑作物支撐了草甘膦的穩定使用,而亞太地區機械化和生物技術種植面積的快速成長則推動了草甘膦用量的成長。由於供應全球80%以上出口量的中國工廠為滿足環保法規而減產,以及拜耳公司警告可能因訴訟成本而退出生產,Glyphosate基本面仍面臨挑戰。隨著產能整合降低價格的極端波動,價格前景正在改善,為生產商提供了更清晰的成本預測,儘管面臨監管方面的阻力,草甘膦的使用量仍在穩步成長。動態基本面影響市場:中國原藥生產商控制全球80%以上的出口量,而拜耳仍是最主要的品牌製劑生產商。

全球Glyphosate市場趨勢與洞察

基因改造耐除草劑作物的商業化

中國核准2024年起推廣耐Glyphosate種子性狀,這意味著超過100萬英畝的土地可以種植美國和巴西早已廣泛應用的生物品種。諸如耐五種除草劑(包括Glyphosate)的Bykonic大豆等新型複合技術,可望帶來更廣泛的雜草控制潛力。持續的性狀升級將維持除草劑防治方案的有效性,從而滿足大面積作物對Glyphosate的長期需求。

高效除草方案的需求日益成長

全球農民面臨530種已知的抗除草劑雜草,因此對可靠的頻譜除草劑的需求日益成長。Glyphosate的作用機制、施用靈活性以及與精準施藥平台的兼容性對於雜草綜合治理至關重要。在許多非洲市場,非專利製劑的價格越來越親民,也更容易取得,這促使以前依賴人工除草的小農戶開始更多地使用嘉磷塞。

監管限制

歐盟於2023年將Glyphosate的使用許可延長了10年,但允許成員國自行製定更嚴格的限制措施。德國於2024年從全面禁用轉為限制使用,但法律挑戰仍在繼續。紐西蘭也出現了類似的不確定性,該國針對提案收到了3,100份公眾意見。基準值,並可能導致需求轉向那些擁有更清晰授權框架的國家。

細分市場分析

到2024年,穀類將佔Glyphosate市場佔有率的43.5%,這反映出草甘膦在全球玉米和小麥保護性耕作系統中的大量使用。巴西持續的雙季種植和中國高粱種植面積的擴大支撐了市場需求。豆類和油籽市場預計到2030年將以5.6%的複合年成長率成長,主要受南美洲大豆種植面積和印度芥菜種植面積增加的推動。

變數噴霧器等技術進步最佳化了施藥量,但總施藥面積保持穩定。棉花和甘蔗在人工除草成本高的熱帶地區仍然十分重要。園藝種植者正在採用更嚴格的施藥系統,但滴灌噴霧器和篩網噴霧器仍然是果園和葡萄園的基本施藥方式。

區域分析

預計到2024年,北美將佔據Glyphosate市場34%的佔有率,這主要得益於大規模犁地大豆和玉米種植系統,其中超過80%的種植戶依賴根除式和作物內除草劑。在加拿大,草原地區的小麥和油菜種植也採用了類似的耕作方式;而在墨西哥,玉米種植機械化的不斷提高正穩步推高草甘膦的需求。訴訟仍然是一個主要的不穩定因素,如果拜耳公司退出市場,未決訴訟將威脅到國內供應。喬治亞和其他一些地區頒布的州級責任豁免條款旨在保護草甘膦的持續生產。

預計亞太地區將實現最快成長,到2030年複合年成長率將達到5.86%。中國農藥產量穩定在24萬至25萬噸左右,Glyphosate仍名列非專利活性成分之列。印度農藥價值鏈正在擴展,隨著農民採用低成本除草方法,通用Glyphosate的使用量不斷增加。印尼、越南和泰國正在增加播前除草劑的使用,以支持雙季種植。澳洲的大面積穀物農場儘管已步入成熟期,但需求仍保持穩定,這得益於精準的噴灑系統,該系統能夠更好地控制噴灑作業。

南美洲是全球消費量,這主要得益於巴西2025年預計3.223億噸的糧食產量,從而推動了除草劑使用強度的增加。犁地種植面積超過3500萬公頃,因此Glyphosate對於播種前雜草的控制至關重要。阿根廷的貨幣困境加劇了價格敏感性,但對種植面積的依賴並未降低。像先正達在保利尼亞投資6,500萬美元的新型區域技術中心,專注於研發在熱帶氣候下仍能維持藥效的配方,這些都為長期成長提供了支持。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 基因改造耐除草劑作物的商業化

- 高效除草方案的需求日益成長

- 擴大耕地面積及農業集約化

- 將Glyphosate耐受性狀整合到基因編輯作物中

- 再生犁地信用計畫推動了碳權額度的採用

- 整合的生產能力有助於穩定長期價格。

- 市場限制

- 監管限制

- 向有機和生物除草劑的轉變

- 品牌供應商提起訴訟可能導致撤回訂單的風險

- 在主要作物區推廣雜草抗性

- 監管環境

- 技術展望

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 按作物類型

- 糧食

- 豆類和油籽

- 水果和蔬菜

- 經濟作物

- 其他作物

- 透過採用基因改造生物

- 基因改造作物

- 非基因改造

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 北美其他地區

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 歐洲

- 德國

- 法國

- 義大利

- 西班牙

- 英國

- 俄羅斯

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 亞太其他地區

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東地區

- 非洲

- 南非

- 其他非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Bayer AG

- Zhejiang Xinan(Wynca)

- Syngenta AG

- BASF SE

- UPL Ltd

- Corteva, Inc.

- FMC Corporation

- Nufarm Ltd

- Zhejiang Jiangshan Agrochemical(Jiangshan Chemical Co.)

- Jiangsu Yangnong Chemical(Sinochem Holdings)

- Albaugh LLC(Albaugh Group)

- Bharat Rasayan

- Jiangsu Good-Harvest(Good Harvest Weien Co.)

- King Quenson Industry(King Quenson Group)

第7章 市場機會與未來展望

The global glyphosate market stands at USD 9.5 billion in 2025 and is forecast to reach USD 11 billion by 2030, advancing at a 3.6% CAGR.

Stable demand reflects glyphosate's entrenched role in conservation tillage, large-scale row-crop systems, and carbon-credit-linked no-till programs. North America's early adoption of herbicide-tolerant crops underpins consistent usage, while Asia-Pacific's rapid mechanization and rise in biotech acreage accelerate volume growth. Supply fundamentals remain tight because Chinese plants that supply more than 80% of global exports are curbing output to meet environmental rules, and Bayer has warned of a possible production exit amid litigation costs. Price visibility has improved as capacity consolidation limits extreme volatility, giving growers clearer cost forecasts and supporting steady adoption despite regulatory headwinds. Competitive dynamics also shape the glyphosate market: Chinese technical-grade producers control more than 80% of global export volume, while Bayer remains the most visible branded formulator.

Global Glyphosate Market Trends and Insights

Commercialization of GM Herbicide-Tolerant Crops

China's 2024 approval of glyphosate-tolerant seed traits opened more than 1 million mu to biotech varieties, echoing long-running adoption in the United States and Brazil. New stacked technologies, such as Bayer's Vyconic soybeans, tolerant to five herbicides, including glyphosate, promise broader weed-control windows. Continuous trait upgrades ensure herbicide programs remain effective, anchoring long-term glyphosate demand across large acreage crops.

Rising Demand for Effective Weed Control Solutions

Farmers face 530 confirmed herbicide-resistant weed biotypes worldwide, increasing the urgency for reliable broad-spectrum options. Glyphosate's mode of action, application flexibility, and compatibility with precision spraying platforms make it integral to integrated weed management. In many African markets, generic formulations have improved affordability, driving uptake among smallholders who previously relied on manual weeding.

Regulatory Restrictions

The European Union renewed glyphosate for 10 years in 2023 but gave member states leeway to impose stricter limits. Germany moved from an outright ban to restricted use in 2024, and legal challenges continue. Similar uncertainties have surfaced in New Zealand, where proposals to raise residue limits prompted 3,100 public submissions. Fragmented rules complicate stewardship, raise compliance costs, and may shift demand toward countries with clearer approval frameworks.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Agricultural Land and Intensified Farming

- Integration of Glyphosate-Tolerant Traits in Gene-Edited Crops

- Shift Toward Organic and Bio-Herbicides

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Grains and cereals generated 43.5% of the glyphosate market in 2024, reflecting heavy use in corn and wheat conservation systems worldwide. Continued double-cropping in Brazil and expanded sorghum acreage in China anchor demand. The pulses and oilseeds segment is forecast to post a 5.6% CAGR through 2030 as South American soybean hectares and Indian mustard cultivation rise.

Technology advances such as variable-rate sprayers optimize doses, yet total treated hectares keep volumes steady. Cotton and sugarcane remain important in tropical zones where manual weeding costs are high. Although horticultural producers apply more restrictive regimes, dripline injection, and shielded sprayers maintain a baseline of usage in orchards and vineyards.

The Glyphosate Market is Segmented by Crop Type (Grains and Cereals, Commercial Crops, and More), by GMO Adoption (GM Crops and Non-GM Crops), and by Geography (Asia-Pacific, North America, South America, Europe, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America's 34% share of the glyphosate market in 2024 stems from extensive no-till soy and corn systems, where over 80% of growers depend on herbicides for burndown and in-crop applications. Canada mirrors these practices across prairie wheat and canola, while Mexico's transition to mechanized maize farming introduces steady incremental demand. Litigation remains the main destabilizer, with pending cases threatening domestic supply if Bayer exits. State-level liability shields enacted in Georgia and other jurisdictions aim to safeguard continued manufacture.

Asia-Pacific is projected to deliver the fastest regional growth at a 5.86% CAGR by 2030. China's pesticide volumes have stabilized at around 240,000-250,000 tons, yet glyphosate remains a top-10 active ingredient. India's agrochemical value chain is scaling, and generic glyphosate volumes rise as farmers adopt low-cost weed control. Indonesia, Vietnam, and Thailand show growing adoption of pre-plant burndown to support double-cropping. Australia's broadacre cereal farms maintain mature but steady demand, reinforced by precision guidance systems that fine-tune application.

South America ranks second in overall consumption, anchored by Brazil's 322.3 million-ton grain harvest in 2025, which drives high herbicide intensity. No-till covers more than 35 million hectares, making glyphosate indispensable for grass weed control before planting. Argentina's currency challenges add price sensitivity but do not diminish acreage reliance. New regional tech hubs, such as Syngenta's USD 65 million facility in Paulinia, focus on tropical-climate formulations that preserve efficacy under high humidity, supporting long-term growth.

- Bayer AG

- Zhejiang Xinan (Wynca)

- Syngenta AG

- BASF SE

- UPL Ltd

- Corteva, Inc.

- FMC Corporation

- Nufarm Ltd

- Zhejiang Jiangshan Agrochemical (Jiangshan Chemical Co.)

- Jiangsu Yangnong Chemical (Sinochem Holdings)

- Albaugh LLC (Albaugh Group)

- Bharat Rasayan

- Jiangsu Good-Harvest (Good Harvest Weien Co.)

- King Quenson Industry (King Quenson Group)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Commercialization of GM herbicide-tolerant crops

- 4.2.2 Rising demand for effective weed control solutions

- 4.2.3 Expansion of agricultural land and intensified farming

- 4.2.4 Integration of glyphosate-tolerant traits in gene-edited crops

- 4.2.5 Regenerative no-till carbon-credit programmes boost usage

- 4.2.6 Capacity consolidation stabilises long-term prices

- 4.3 Market Restraints

- 4.3.1 Regulatory restrictions

- 4.3.2 Shift toward organic and bio-herbicides

- 4.3.3 Litigation-driven exit risk of branded suppliers

- 4.3.4 Accelerating weed resistance in major crop belts

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 By Crop Type

- 5.1.1 Grains and Cereals

- 5.1.2 Pulses and Oilseeds

- 5.1.3 Fruits and Vegetables

- 5.1.4 Commercial Crops

- 5.1.5 Other Crops

- 5.2 By GMO Adoption

- 5.2.1 GM Crops

- 5.2.2 Non-GM Crops

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.1.4 Rest of North America

- 5.3.2 South America

- 5.3.2.1 Brazil

- 5.3.2.2 Argentina

- 5.3.2.3 Rest of South America

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 France

- 5.3.3.3 Italy

- 5.3.3.4 Spain

- 5.3.3.5 United Kingdom

- 5.3.3.6 Russia

- 5.3.3.7 Rest of Europe

- 5.3.4 Asia-Pacific

- 5.3.4.1 China

- 5.3.4.2 India

- 5.3.4.3 Japan

- 5.3.4.4 Australia

- 5.3.4.5 Rest of Asia-Pacific

- 5.3.5 Middle East

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 UAE

- 5.3.5.3 Turkey

- 5.3.5.4 Rest of Middle East

- 5.3.6 Africa

- 5.3.6.1 South Africa

- 5.3.6.2 Rest of Africa

- 5.3.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Bayer AG

- 6.4.2 Zhejiang Xinan (Wynca)

- 6.4.3 Syngenta AG

- 6.4.4 BASF SE

- 6.4.5 UPL Ltd

- 6.4.6 Corteva, Inc.

- 6.4.7 FMC Corporation

- 6.4.8 Nufarm Ltd

- 6.4.9 Zhejiang Jiangshan Agrochemical (Jiangshan Chemical Co.)

- 6.4.10 Jiangsu Yangnong Chemical (Sinochem Holdings)

- 6.4.11 Albaugh LLC (Albaugh Group)

- 6.4.12 Bharat Rasayan

- 6.4.13 Jiangsu Good-Harvest (Good Harvest Weien Co.)

- 6.4.14 King Quenson Industry (King Quenson Group)

7 Market Opportunities and Future Outlook

Glyphosate市場預測至2034年:按作物、製劑形式、分銷管道、應用和區域分類的全球分析

Glyphosate市場預測至2034年:按作物、製劑形式、分銷管道、應用和區域分類的全球分析 Glyphosate市場:按應用、作物、劑型和地區分類

Glyphosate市場:按應用、作物、劑型和地區分類 Glyphosate市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、應用、地區和競爭格局分類,2021-2031年

Glyphosate市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、應用、地區和競爭格局分類,2021-2031年 Glyphosate市場:按劑型、作物、分銷管道、最終用戶和應用分類的全球市場預測,2026-2032年

Glyphosate市場:按劑型、作物、分銷管道、最終用戶和應用分類的全球市場預測,2026-2032年 日本Glyphosate市場規模、佔有率、趨勢和預測:按作物類型、基因改造生物 (GMO) 狀態和地區分類,2026-2034 年

日本Glyphosate市場規模、佔有率、趨勢和預測:按作物類型、基因改造生物 (GMO) 狀態和地區分類,2026-2034 年 2026年全球Glyphosate市場報告

2026年全球Glyphosate市場報告 Glyphosate市場規模、佔有率和成長分析(按最終用戶、應用、劑型、通路、作物類型和地區分類)—2026-2033年產業預測

Glyphosate市場規模、佔有率和成長分析(按最終用戶、應用、劑型、通路、作物類型和地區分類)—2026-2033年產業預測 草甘膦市場機會、成長促進因素、產業趨勢分析及預測(2026-2035年)

草甘膦市場機會、成長促進因素、產業趨勢分析及預測(2026-2035年) 全球Glyphosate市場

全球Glyphosate市場 全球Glyphosate市場評估:依作物類型、形式、應用、地區、機會和預測(2018-2032年)

全球Glyphosate市場評估:依作物類型、形式、應用、地區、機會和預測(2018-2032年)