|

市場調查報告書

商品編碼

1686175

變頻驅動器:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)Variable Frequency Drives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

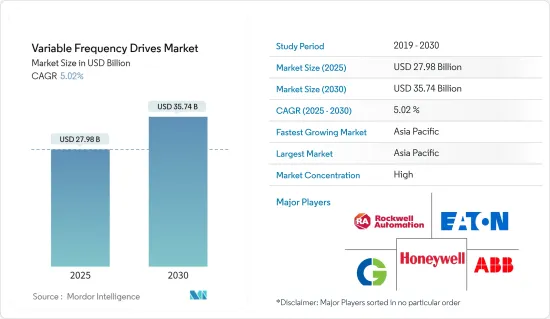

變頻驅動器市場規模預計在 2025 年為 279.8 億美元,預計到 2030 年將達到 357.4 億美元,預測期內(2025-2030 年)的複合年成長率為 5.02%。

主要亮點

- 快速工業化推動 VFD 跨產業滲透:由於快速工業化,尤其是在新興國家,變頻驅動器 (VFD) 市場正在以更快的速度成長。例如,中國預計2021年工業產值將成長9.6%,到2025年中國的目標是生產3,500萬輛汽車。這一擴張為VFD在各個領域的部署創造了巨大的機會。國際機器人聯合會預測,2024年全球工業機器人安裝量將成長到51.8萬台。

- 自動化推動成長:印度的 SAMARTH Udyog Bharat 4.0 等智慧製造舉措正在提高人們對工業 4.0 的認知,從而促進自動化的採用。

- 新興產業:VFD 擴大用於碳捕獲和氫氣生成等新應用,其應用範圍正在擴大。

- 政府支持:VFD 製造商和政府機構之間的合作正在加速市場擴張,例如與加爾各答和清奈地鐵計劃的夥伴關係。

- 能源效率:VFD 市場成長的關鍵驅動力:越來越關注能源效率也是 VFD 市場成長的關鍵驅動力。根據國際能源總署統計,馬達消耗了電力產業所用能源的近40%。 VFD 可提高能源效率,尤其是與泵浦和風扇等變扭矩負載應用中的馬達結合使用時。透過調節馬達速度,VFD 可以顯著降低能耗。

- 節能潛力 根據 ABB 白皮書,節能馬達和變頻器可以將全球電力消耗減少 10%。

- 監管支持:歐盟(EU)能源效率指令的目標是到 2030 年將能源效率提高 30%,高於 2020 年的 20%。

- 減少碳排放:歐盟委員會的「Fit for 55」舉措正在推動減少二氧化碳排放,從而鼓勵在注重節能的地區採用變頻器。

- 技術進步正在提高 VFD 的能力:技術進步正在加速各行各業對 VFD 的應用。現代驅動器配備了先進的網路和診斷功能,以提高生產力並降低營運成本。例如,將馬達驅動系統與 VFD 整合可以將商業建築每平方英尺的消費量降低高達 40%。

- 產品創新羅克韋爾自動化將於 2022 年升級其 PowerFlex 6000T VFD,以增強高速馬達應用的性能。

- 新品:艾默生 Copeland VFD 系列 (2021) 和 ABB 的緊湊型 ACS1000i (2022) 分別為工業冷凍和空間受限的環境而設計。

- 產業特定應用這些進步使得 VFD 在水和電力管理等領域更加可靠。

- 市場細分與區域洞察:VFD 市場根據電壓類型、最終用戶產業和地區進行細分。低電壓變頻器在 2021 年佔據 61.02% 的市場佔有率,預計到 2027 年將成長到 185.2 億美元,複合年成長率為 5.1%。能源和電力產業仍將是最大的終端用戶,2021 年約佔市場的 29%,預計到 2027 年將成長到 86.8 億美元。

- 亞太地區處於領先地位:該地區將在 2021 年佔據 42.18% 的佔有率,預計到 2027 年將成長至 136.7 億美元,複合年成長率為 6.2%。

- 產業優勢低壓變頻器在食品和飲料、石油和天然氣以及採礦等行業占主導地位。

- 暖通空調中的能源效率:暖通空調產業擴大採用變頻器,這可以將泵浦應用中的能耗降低 25%,伯明翰競技場劇院等計劃證明了這一點。

- VFD 市場的投資和創新:市場領導正在積極投資研發、生產能力和分銷網路,以擴大市場佔有率。技術創新專注於開發節能、經濟的變頻器,使其更易於在所有行業中使用。

- 新產品 Bison Gear & Engineering Corp. 將於 2022 年推出一款針對工業和戶外應用的新型多功能 VFD。

- 市場擴展:WEG 於 2022 年推出了 CFW900 VFD,將更高的功率密度與簡單的設計相結合。

- 擴大產品組合:丹佛斯傳動於 2021 年透過 VACON 1000 變頻器擴展了其中壓產品陣容。

變頻驅動市場趨勢

低壓部分佔據市場主導地位

低壓部分是 VFD 市場中最大的部分,佔 2021 年總市場佔有率的 61.02%。該部分預計將從 2022 年的 144.5 億美元成長到 2029 年的 200.4 億美元,複合年成長率為 5.1%。

- 能源效率備受關注低壓變頻器有助於最佳化各行各業的能源使用,其中包括商業建築,而商業建築占美國能源消耗的 40%。

- 監管推動:歐盟的 Tier-2 生態設計指令 (2021) 和歐洲綠色交易等政府政策正在推動能源密集型產業採用 VFD。

- 技術創新:先進的 VFD 現在包括煞車策略、加速期間的功率提升和減速期間的高級控制等功能。

- 工業應用:Invertek 的 Optidrive E3 安裝在吉隆坡的朝聖者集合點終點站,用於氣流管理。

亞太地區是成長最快的區域

亞太地區是 VFD 應用成長最快的地區,預計將從 2022 年的 101 億美元成長到 2029 年的 153.9 億美元,複合年成長率為 6.2%。

- 工業發展:中國快速的自動化和工業成長是該地區對 VFD 需求的主要驅動力。

- 能源法規:政府嚴格的能源效率政策為中國和印度等國家創造了成長機會。

- 戰略夥伴關係:羅克韋爾自動化將於 2021 年與新加坡 CAD-IT 合作,為東南亞提供智慧製造解決方案。

- 暖通空調領域的擴張:都市化地區暖通空調系統市場的不斷擴大正在推動對變頻器的需求,正如格蘭富與 BBP 合作在 2021 年實現東南亞永續製冷一樣。

變頻驅動器產業概況

變頻驅動器市場競爭格局分析

全球企業主導綜合市場

VFD 市場由全球企業集團主導,其中少數大型公司佔據相當大的佔有率。預計 2021 年市場規模為 218.2 億美元,到 2027 年將達到 301.7 億美元,複合年成長率為 5.0%。主要成長動力包括工業化和變頻器在 HVAC 等能源密集型領域的廣泛應用,這可以減少商業建築 30-40% 的能源使用。

市場領導者ABB、西門子、施耐德電機、丹佛斯和羅克韋爾自動化等公司引領 VFD 市場。

產品重點:這些公司正在大力投資研發節能解決方案,例如 ABB 的 ACS1000i 和西門子的再生能源驅動器。

技術創新:西門子和Schneider Electric專注於具有增強通訊功能的變頻器,用於遠端監控和診斷。

VFD 市場未來成功的策略:

技術創新、擴大應用和能源效率將繼續成為 VFD 市場成功的關鍵策略。人工智慧和機器學習的整合簡化了 VFD試運行並最佳化了效能。

新興機會:變頻器在交通運輸、氫氣生產和碳捕獲領域的應用不斷擴大,為其提供了新的成長途徑。

分散化趨勢:公司正在開發直接整合到馬達中的分散式變頻器,以降低安裝成本和複雜性。

IIoT 整合:在採用工業物聯網 (IIoT) 的行業中,聯網的 VFD 變得至關重要,以提供即時資料分析並提高營運效率。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概況

- 產業價值鏈分析

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

- 技術簡介

- 按類型

- 交流變頻器

- 直流驅動

- 按類型

- 評估宏觀經濟趨勢對市場的影響

第5章 市場動態

- 市場促進因素

- 工業化進程加快,變頻器在重點產業的應用日益廣泛

- 自動化推動成長

- 技術進步提高了 VFD 能力

- 市場限制

- 對設備的技術擔憂

- 設備高成本

- 網路安全問題

第6章 市場細分

- 按電壓類型

- 低電壓

- 中高壓

- 按最終用戶產業

- 基礎設施

- 食品加工

- 能源和電力

- 礦業與金屬

- 紙漿和造紙

- 其他最終用戶產業

- 按地區

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 其他亞太地區

- 拉丁美洲

- 中東和非洲

- 北美洲

第7章 競爭格局

- 公司簡介

- Eaton Corporation

- ABB Ltd

- Crompton Greaves Ltd

- Honeywell International Inc.

- Rockwell Automations Inc.

- Hitachi Group

- Siemens AG

- Mitsubishi Corporation

- Toshiba Corporation

- Schneider Electric SE

- Johnson Controls Inc.

- Nidec Corporation

- Danfoss AS

第8章投資分析

第9章:市場的未來

The Variable Frequency Drives Market size is estimated at USD 27.98 billion in 2025, and is expected to reach USD 35.74 billion by 2030, at a CAGR of 5.02% during the forecast period (2025-2030).

Key Highlights

- Rapid Industrialization Driving VFD Adoption Across Industries:The Variable Frequency Drives (VFD) market is witnessing accelerated growth due to rapid industrialization, especially in emerging economies. For example, China's industrial production surged by 9.6% in 2021, and the country aims to produce 35 million automotive units by 2025. This expansion is creating significant opportunities for VFD deployment across various sectors. The rise of automation in manufacturing is further boosting the market, with the International Federation of Robotics predicting that global industrial robot installations will increase to 518,000 units by 2024.

- Automation driving growth: Smart manufacturing initiatives such as India's SAMARTH Udyog Bharat 4.0 are raising awareness of Industry 4.0, which in turn is increasing automation adoption.

- Emerging industries: VFDs are increasingly being used in new applications, such as carbon capture and hydrogen generation, broadening their reach.

- Government support: Collaborations between VFD manufacturers and government agencies are accelerating market expansion, as seen in Danfoss' partnership with Kolkata and Chennai Metro Rail projects.

- Energy Efficiency: A Key Driver for VFD Market Growth:The growing emphasis on energy efficiency is another critical driver of VFD market growth. According to the International Energy Agency, electric motors consume nearly 40% of the energy used in power industries. VFDs enhance energy efficiency, particularly when paired with motors in variable torque load applications like pumps and fans. By adjusting motor speed, VFDs can significantly reduce energy consumption.

- Energy-saving potential: ABB's whitepaper suggests that energy-efficient motors and VFDs could cut global electricity consumption by 10%.

- Regulatory support: The European Union's updated Energy Efficiency Directive targets a 30% improvement in energy efficiency by 2030, up from 20% in 2020.

- Carbon reduction: The European Commission's 'Fit for 55' initiative is pushing for lower carbon emissions, which is driving VFD deployment in energy-conscious sectors.

- Technological Advancements Enhancing VFD Capabilities: Technological progress is accelerating the adoption of VFDs across industries. Modern drives come equipped with advanced networking and diagnostic capabilities, which enhance productivity and reduce operational costs. For instance, integrating motor-driven systems with VFDs can cut per-square-foot energy consumption by up to 40% in commercial buildings.

- Product innovation: Rockwell Automation introduced upgraded PowerFlex 6000T VFDs in 2022, enhancing performance for high-speed motor applications.

- New releases: Emerson's 2021 Copeland VFD line and ABB's compact ACS1000i (2022) are designed for industrial refrigeration and space-constrained environments, respectively.

- Industry-specific applications: These advancements are increasing the reliability of VFDs in sectors like water and power management.

- Market Segmentation and Regional Insights: The VFD market is divided by voltage type, end-user industry, and geography. Low voltage VFDs held a 61.02% market share in 2021 and are expected to grow to USD 18.52 billion by 2027 at a CAGR of 5.1%. The energy and power sector remains the largest end-user, accounting for nearly 29% of the market in 2021, with projected growth to USD 8.68 billion by 2027.

- Asia-Pacific leads the way: The region held a 42.18% share in 2021 and is expected to grow to USD 13.67 billion by 2027, at a 6.2% CAGR.

- Sector dominance: Low-voltage VFDs dominate sectors such as food and beverage, oil and gas, and mining.

- Energy efficiency in HVAC: The HVAC industry is a notable adopter, where VFDs are capable of cutting energy use by 25% in pump applications, demonstrated in projects like the Birmingham Hippodrome theater.

- Investment and Innovation in the VFD Market: Market leaders are actively investing in R&D, production capabilities, and distribution networks to increase market share. Innovation is focused on developing energy-efficient, cost-effective VFDs to enhance their usability across industries.

- New products: Bison Gear & Engineering Corp. released a versatile new VFD in 2022, targeting industrial and outdoor applications.

- Market expansion: WEG introduced the CFW900 VFD in 2022, combining increased power density with simplified design.

- Portfolio expansion: Danfoss Drives expanded its medium-voltage offerings with the VACON 1000 drive in 2021.

Variable Frequency Drives Market Trends

Low Voltage Segment to Dominate the Market

The low-voltage segment is the largest in the VFD market, accounting for 61.02% of the total market share in 2021. This segment is forecasted to grow from USD 14.45 billion in 2022 to USD 20.04 billion by 2029, with a CAGR of 5.1%.

- Energy efficiency in focus: Low-voltage VFDs help optimize energy use across multiple industries, including commercial buildings, which account for 40% of U.S. energy consumption.

- Regulatory push: Government policies like the EU's Tier-2 Ecodesign Directive (2021) and the European Green Deal are driving adoption of VFDs in energy-intensive industries.

- Technological innovations: Advanced VFDs now come with features like braking methods, power boost during ramp-up, and advanced controls during ramp-down.

- Industry application: The food processing industry is a major adopter, with Invertek's Optidrive E3 being installed for airflow management at Kuala Lumpur's Pilgrim Assembly Point Terminal.

Asia Pacific The Fastest-Growing Regional Segment

Asia-Pacific is the fastest-growing region for VFD adoption, with projected growth from USD 10.10 billion in 2022 to USD 15.39 billion by 2029 at a CAGR of 6.2%.

- Industrial development: Rapid automation and industrial growth in China are driving significant VFD demand in the region.

- Energy regulations: Strict government policies around energy efficiency are creating growth opportunities in countries like China and India.

- Strategic partnerships: Companies are expanding in the region, with Rockwell Automation partnering with Singapore-based CAD-IT in 2021 to provide smart manufacturing solutions in Southeast Asia.

- HVAC sector expansion: The growing market for HVAC systems in urbanizing regions is driving VFD demand, as seen in Grundfos' 2021 partnership with BBP for sustainable cooling in Southeast Asia.

Variable Frequency Drives Industry Overview

Variable Frequency Drives Market: Competitive Landscape Analysis

Global players dominate a consolidated market:

The VFD market is dominated by global conglomerates, with a few major players controlling a significant share. Valued at USD 21.82 billion in 2021, the market is expected to reach USD 30.17 billion by 2027, growing at a CAGR of 5.0%. The primary growth drivers include industrialization and increased VFD adoption in energy-intensive sectors such as HVAC, which can reduce energy usage by 30-40% in commercial buildings.

Market leaders: Companies like ABB, Siemens, Schneider Electric, Danfoss, and Rockwell Automation lead the VFD market.

Product focus: These firms invest heavily in R&D to develop energy-efficient solutions, such as ABB's ACS1000i and Siemens' regenerative energy drives.

Technological innovation: Siemens and Schneider Electric focus on VFDs with enhanced communication capabilities for remote monitoring and diagnostics.

Strategies for future success in the VFD market:

Technological innovation, expanding applications, and energy efficiency remain key strategies for success in the VFD market. The integration of AI and machine learning is simplifying VFD commissioning and optimizing performance.

Emerging opportunities: VFD applications in transportation, hydrogen production, and carbon capture are expanding, offering new avenues for growth.

Decentralization trend: Companies are developing decentralized VFDs built directly into motors, reducing installation costs and complexity.

IIoT integration: Connected VFDs are becoming essential, providing real-time data analytics and enhancing operational efficiency in industries adopting the Industrial Internet of Things (IIoT).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitutes

- 4.3.5 Degree of Competition

- 4.4 Technology Snapshot

- 4.4.1 By Type

- 4.4.1.1 AC Drives

- 4.4.1.2 DC Drives

- 4.4.1 By Type

- 4.5 Assessment of the Impact of Macroeconomic Trends on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rapid Industrialization and Increased Use of VFDs across Major Vertical Industries

- 5.1.2 Automation driving growth

- 5.1.3 Technological Advancements Enhancing VFD Capabilities

- 5.2 Market Restraints

- 5.2.1 Technical Concerns of the Equipment

- 5.2.2 High Cost of the Equipment

- 5.2.3 Cybersecurity Apprehensions

6 MARKET SEGMENTATION

- 6.1 By Voltage Type

- 6.1.1 Low Voltage

- 6.1.2 Medium and High Voltage

- 6.2 By End-user Industry

- 6.2.1 Infrastructure

- 6.2.2 Food Processing

- 6.2.3 Energy and Power

- 6.2.4 Mining and Metals

- 6.2.5 Pulp and Paper

- 6.2.6 Other End-user Industries

- 6.3 By Geography

- 6.3.1 North America

- 6.3.1.1 United States

- 6.3.1.2 Canada

- 6.3.2 Europe

- 6.3.2.1 United Kingdom

- 6.3.2.2 Germany

- 6.3.2.3 France

- 6.3.2.4 Rest of Europe

- 6.3.3 Asia Pacific

- 6.3.3.1 China

- 6.3.3.2 India

- 6.3.3.3 Japan

- 6.3.3.4 Rest of the Asia Pacific

- 6.3.4 Latin America

- 6.3.5 Middle East and Africa

- 6.3.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Eaton Corporation

- 7.1.2 ABB Ltd

- 7.1.3 Crompton Greaves Ltd

- 7.1.4 Honeywell International Inc.

- 7.1.5 Rockwell Automations Inc.

- 7.1.6 Hitachi Group

- 7.1.7 Siemens AG

- 7.1.8 Mitsubishi Corporation

- 7.1.9 Toshiba Corporation

- 7.1.10 Schneider Electric SE

- 7.1.11 Johnson Controls Inc.

- 7.1.12 Nidec Corporation

- 7.1.13 Danfoss AS

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

變頻驅動器市場(按產品類型、電壓、額定功率、應用和最終用戶)—2025-2032 年全球預測

變頻驅動器市場(按產品類型、電壓、額定功率、應用和最終用戶)—2025-2032 年全球預測 2025年變頻驅動器全球市場報告

2025年變頻驅動器全球市場報告 全球暖通空調變頻驅動器市場全球大型變頻驅動器市場

全球暖通空調變頻驅動器市場全球大型變頻驅動器市場 2032 年變頻驅動器 (VFD) 市場預測:按類型、電壓類型、額定功率、應用、最終用戶和地區進行的全球分析

2032 年變頻驅動器 (VFD) 市場預測:按類型、電壓類型、額定功率、應用、最終用戶和地區進行的全球分析 日本變頻驅動器市場報告(按產品類型、功率範圍(微、低、中、高)、應用、最終用途和地區)2025 年至 2033 年

日本變頻驅動器市場報告(按產品類型、功率範圍(微、低、中、高)、應用、最終用途和地區)2025 年至 2033 年 變頻驅動器(VFD)市場 2025-2029

變頻驅動器(VFD)市場 2025-2029 中東和非洲變頻驅動器市場(按類型、電壓、額定功率、應用、最終用戶和地區分類)- 趨勢和預測(至 2030 年)

中東和非洲變頻驅動器市場(按類型、電壓、額定功率、應用、最終用戶和地區分類)- 趨勢和預測(至 2030 年) 2026 年至 2032 年變頻驅動器市場規模(按產業、應用、額定功率和地區分類)2025 年至 2033 年變頻驅動器市場規模、佔有率、趨勢及預測(依產品類型、功率範圍、應用、最終用途及地區)

2026 年至 2032 年變頻驅動器市場規模(按產業、應用、額定功率和地區分類)2025 年至 2033 年變頻驅動器市場規模、佔有率、趨勢及預測(依產品類型、功率範圍、應用、最終用途及地區)