|

市場調查報告書

商品編碼

1444128

壓鑄:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029)Die Casting - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

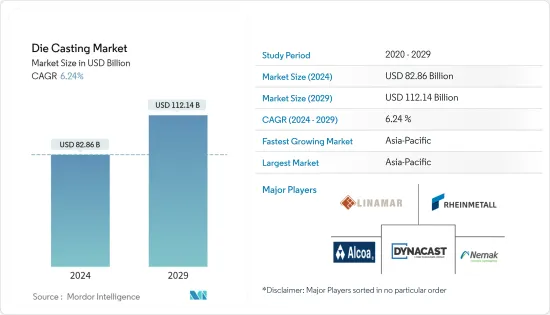

壓鑄市場規模預計到2024年為828.6億美元,預計到2029年將達到1121.4億美元,在預測期內(2024-2029年)年複合成長率為6.24%。

COVID-19的傳播對製造業產生了負面影響。全球多個主要經濟體陷入封鎖,供應鏈中斷。在此期間,所有製造單位和OEM工廠被迫暫停生產和運作。隨著經濟復甦,需求回歸市場,消費者偏好轉向輕型車,汽車產業對壓鑄件的需求龐大。預計這一趨勢將持續下去並推動市場成長。

從中期來看,所研究的市場主要由壓鑄行業供應鏈的複雜性、汽車市場的擴張、壓鑄件在工業機械中的普及不斷提高、建築行業的成長以及電氣和電子設備中鋁鑄件的成長,受到採用的推動。 CAFE 標準和 EPA 減少車輛排放氣體和提高燃油效率的政策正在推動汽車製造商透過採用非鐵金屬來減輕車輛重量。此後,採用壓鑄件作為減重策略,對汽車領域的前市場起到了重要的推動作用。

由於高導熱性,電氣和電子行業對鋁壓鑄部件的需求不斷成長,預計將在預測期內推動成長。此後,採用壓鑄件作為減重策略,對汽車領域的前市場起到了重要的推動作用。然而,原料供應緊張、原料價格波動以及冶金行業排放氣體的環境法規對市場成長構成了主要障礙。

由於中國和印度等國家對汽車的需求不斷成長,以及鋁壓鑄件在各種應用中的使用不斷增加,預計亞太地區將在壓鑄市場中佔據最大佔有率。在北美,由於建築和汽車行業產量的增加,鋁壓鑄市場也預計將大幅成長。

壓鑄市場趨勢

鋁有望在壓鑄製程中發揮重要作用

多年來,許多工業應用對鋁製高壓壓鑄零件的需求不斷增加,因為該工藝可生產輕質零件並為複雜形狀提供高度彈性。

近年來,汽車零件由於新技術的演進而不斷進步和創新。尤其是輕量材料在汽車零件製造中的應用正在引起全國的關注。

這種流行的一個重要原因是,由於採用製造關鍵零件的輕量汽車材料,汽車的燃油效率提高了。

此外,必須在不犧牲安全性、品質或性能的情況下實現車輛減重。鋁壓鑄件耐用且可無限回收,由於鋁具有多種優點,因此成為製造商的首選。為進一步加強市場開拓,龍頭企業的收購、聯盟數量也不斷增加。 2022年8月,文謙集團宣布將在安徽省六安經濟技術開發區興建新能源汽車鋁壓鑄件生產基地。

2021年10月,Sandhar Engineering Private Limited成立,作為完全子公司,開展製造和組裝各種鎖定裝置、電氣、電子、機械、汽車和工業零件的業務。 2021 年 4 月,Jaya Hind Industries 將與 KS Huayu Alutech GmbH (KSATAG) 的汽車缸體和缸頭生產技術合作夥伴關係延長至 2027 年。合約範圍也擴大到包括 Sunrise Industries 的新零件。電動車、底盤結構件等。2021年3月,Sandhar Technologies與Unicast Autotech簽署非約束性合作備忘錄,收購鋁壓鑄業務。

在預測期內,鋁壓鑄市場的成長可能會繼續擴大,以滿足汽車和非汽車產業對輕質和高導電性金屬零件不斷成長的需求。

亞太地區可能會經歷顯著成長

預計在預測期內,亞太地區將在壓鑄市場中佔據最大的市場佔有率。由於汽車行業的成長、工業部門的需求以及風力渦輪機和電訊應用範圍的擴大,預計亞太地區壓鑄市場將以更快的速度成長。

印度和中國的廉價勞動力和低製造成本預計將進一步加速亞太地區的市場成長。此外,對電動和混合汽車的需求不斷成長,導致汽車製造商在所有類型的車輛中專注於使用鋁等輕質材料,而不是較重的鋼鐵。

此外,製造電動車的公司也積極採購這些壓力壓鑄機並採用該技術,以滿足不斷成長的消費者需求。

一些公司已經採取了成長策略,例如擴大製造能力,以保持在該市場的競爭力。

壓鑄業概況

壓鑄市場由 Neamk、Alcoa Corporation、Linamar Corporation 和 Dynacast 等幾家主要企業主導。市場上的這些主要企業致力於透過各種合併、聯盟、合資和收購來擴大其全球影響力。例如,

- 2022年3月,利納馬公司收購了GF Casting Solutions (GF) 50%的股權。透過此次收購,利納馬公司增強了產品系列。

- 2022 年 1 月,Gibbs Die Casting 的子公司 Koch Enterprises, Inc. 收購了 Amprod Holdings, LLC。透過此次收購,該公司將產品系列擴展到美國。

- 2022 年 1 月,Sandhar Auto Electric Solutions Private Limited 成立,作為完全子公司,旨在推動電動車業務並提供先進的技術解決方案。 Sandhar Auto Electric Solutions Private Limited 主要從事電池電動汽車、氫燃料電池汽車、生質燃料技術車輛、全地形車輛 (ATV) 和其他先進汽車技術車輛的零件製造業務。涉及。

- 2021 年 8 月,利納馬公司宣布與荷蘭的 Innovative Mechatronic Systems BV (IMSystems) 建立合作夥伴關係。此次合作的重點是將阿基米德驅動傳動系統推向市場。

- 2021 年 4 月,Aludyne 宣布收購 Shiloh Industries 的 CastLight 部門。該部門生產鋁壓鑄件。

- Endurance Technologies 於 2021 年 2 月宣布,位於印度泰米爾納德邦 Kancheepuram 的新工廠已開始商業生產。該工廠將生產兩輪車和四輪車的整合式鋁壓鑄件和碟式煞車組件。

- 2020 年 4 月,Endurance Technologies 收購了位於義大利特倫蒂諾的 Adler SpA 99% 的控股權。此次收購預計將透過與義大利和德國 10 家製造工廠的合作,加強該公司在泛歐洲的足跡。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章 簡介

- 調查先決條件

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 市場促進因素

- 市場限制因素

- 產業吸引力-波特五力分析

- 新進入者的威脅

- 買方議價能力

- 供應商的議價能力

- 替代產品的威脅

- 競爭公司之間的敵意強度

第5章市場區隔

- 按用途

- 車

- 電氣和電子

- 工業的

- 其他用途

- 按流程

- 壓力鑄造

- 真空壓鑄

- 擠壓鑄造

- 其他工藝

- 按原料分

- 鋁

- 鎂

- 鋅

- 地區

- 北美洲

- 美國

- 加拿大

- 北美其他地區

- 歐洲

- 英國

- 法國

- 德國

- 義大利

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 泰國

- 馬來西亞

- 印尼

- 韓國

- 其他亞太地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 南非

- 土耳其

- 其他中東和非洲

- 北美洲

第6章 競爭形勢

- 供應商市場佔有率

- 公司簡介

- Form Technologies Inc.(Dynacast)

- Nemak

- Endurance Technologies Limited

- Sundaram Clayton Ltd

- Shiloh Industries

- Georg Fischer Limited

- Koch Enterprises(Gibbs Die Casting Group)

- Bocar Group

- Engtek Group

- Rheinmetall AG(Rheinmetall Automotive, formerly KSPG AG)

- Rockman Industries

- Ryobi Die Casting Ltd

- Linamar Corporation

- Meridian Lightweight Technologies UK Ltd

- Sandhar Group

- Alcoa Corporation

第7章市場機會與未來趨勢

The Die Casting Market size is estimated at USD 82.86 billion in 2024, and is expected to reach USD 112.14 billion by 2029, growing at a CAGR of 6.24% during the forecast period (2024-2029).

The COVID-19 outbreak hit the manufacturing industry adversely. The disruptions were caused in the supply chain as several major economies of the world were in lockdown. All the manufacturing units and OEM plants were forced to halt production and operations during this period. With the recovery of economies, the demand returned to the market witnessing huge demand for die-cast parts in the automotive industry as the consumer preference changed to lightweight vehicles. The trend is expected to continue and drive market growth.

Over the medium term, the market studied is largely driven by supply chain complexities in the die-casting industry, expanding automotive market, increasing penetration of die-casting parts in industrial machinery, growing constructional sector, and employing aluminum casts in electrical and electronics. CAFE standards and EPA policies to cut down automobile emissions and increase fuel efficiency are driving the automakers to reduce the weight of the automobile by employing lightweight non-ferrous metals. Subsequently, employing die-cast parts as a weight reduction strategy is acting as a major driver for the former market in the automotive segment.

Rising demand for aluminum die-casting parts in the electrical and electronics industry owing to its high thermal conductivity is likely to drive growth during the forecast period. Subsequently, employing die-cast parts as a weight reduction strategy is acting as a major driver for the former market in the automotive segment. However, a crunch in raw material supply, volatility in raw material prices, and environmental regulations on emissions for the metallurgy industries are acting as major barriers to market growth.

The Asia-Pacific region is anticipated to hold the largest market share in the die-casting market due to the rise in demand for automobiles in countries such as China and India and the rise in the use of aluminum die-casting for various applications. North America is also expected to witness significant growth in the aluminum die-casting market due to growing output from the construction and automotive sectors.

Die Casting Market Trends

Aluminum Anticipated to Play Key Role in Die Casting Process

The demand for aluminum high-pressure die-casting parts has been increasing across numerous industrial applications over the years, as the process manufactures lightweight parts and provides high flexibility for complex shapes.

In recent years, automotive parts have witnessed advancements and innovations with the evolution of new technologies. Among them, the use of lightweight materials for the manufacturing of auto components has been gaining attention across the country.

One of the important reasons for this popularity is the enhanced fuel economy of automobiles with the adoption of lightweight automotive materials manufacturing crucial parts.

Additionally, the lightweight of vehicles must be done without compromising on safety, quality, and performance. Aluminum die-cast parts are durable and can be endlessly recycled therefore, aluminum is most preferred by manufacturers due to its varied advantages.

Moreover, there is a rising number of acquisitions and partnerships by the major players to further enhance development in the market. For instance,

- In August 2022, Wencan Group Co., Ltd. announced that it intends to build a production base of aluminum die-cast parts for New Energy Vehicles (NEVs) in Lu'an Economic and Technological Development Zone, Anhui Province.

- In October 2021, Sandhar Engineering Private Limited was incorporated as a wholly owned Subsidiary Company for carrying out the business of manufacturers, and assembling various Locking Devices, Electrical, Electronics, Mechanical, Automobile, and Industrial parts.

- In April 2021, Jaya Hind Industries extended its technical partnership with KS Huayu AlutechGmbH (KSATAG) for the manufacturing of automotive cylinder blocks and cylinder heads till 2027. The scope of the agreement has also been expanded to cover new parts from Sunrise Industries, such as Electric Vehicles, Structural parts for Chassis, etc.

- In March 2021, Sandhar Technologies entered a non-binding Memorandum of Understanding with Unicast Autotech to acquire its aluminum die-casting business

The growth of the aluminum die-casting market is likely to continue to increase during the forecast period to meet the increasing demand for lightweight components and high-conductivity metal parts from the automotive and non-automotive sectors.

Asia-Pacific Region Likely to Witness Significant Growth

The Asia-Pacific region is anticipated to hold the largest market share in the die-casting market during the forecast period. The growing automobile industry, demand from the industrial sector, and increased scope of application in windmills and telecommunications are expected to drive the die-casting market at a faster pace in the Asia-Pacific region.

Cheaper labor and low manufacturing costs in India and China are expected to further accelerate the market growth in the Asia-Pacific region. In addition, increased demand for electric and hybrid vehicles has turned automakers' focus to using lightweight materials like aluminum as a substitute for heavier steel and iron in all types of vehicles. For instance,

- In May 2022, Tamil Nadu Small Industries Development Corporation invested an amount of INR 5.8 Crore to establish a common facility center for aluminum high-pressure die casting.

The growing expansion of automotive manufacturing industries across the country is likely to increase the demand for lightweight materials for automotive applications. For instance,

- In February 2021, MG Motors announced that INR 1,500 crore may be invested in the expansion and localization of its business to increase its production capacity at the Halol plant in Gujarat.

- The government of India has proposed the use of aluminum per vehicle in India from 29 Kg to 160 Kg for the electric vehicle during the forecast period.

In addition, the companies manufacturing electric vehicles are also actively procuring these pressure diecasting machines and are adopting this technology to make themselves ready for growing consumer demand.

Several players adopt growth strategies, such as manufacturing capacity expansion, to stay competitive in this market. For instance,

- In July 2021, YIZUMI established the Die Casting Technical Service Center (TSC) in the United States and India that offers integrated solutions for die casting cells, dies, die casting process, and product debugging.

- In February 2021, Endurance Technologies commenced commercial production at its new plant in Vallam, Vadagal, Kancheepuram, Tamil Nadu. The plant manufactures aluminum die-castings and carries out the integration of disc brake components with control brake modulators for supplying machined aluminum castings to Hyundai, Kia, and Royal Enfield.

Die Casting Industry Overview

The Die Casting market is dominated by several key players such as Neamk, Alcoa Corporation, Linamar Corporation, Dynacast, and many others. These key players in the market are focusing on expanding their presence globally through various mergers, partnerships, joint ventures, and acquisitions. For instance,

- In March 2022, Linamar Corporation acquired a 50% interest in GF Casting Solutions (GF). Through this acquisition, Linamar Corporation enhanced its product portfolio in automotive applications.

- In January 2022, Koch Enterprises, Inc., a subsidiary of Gibbs Die Casting acquired Amprod Holdings, LLC. Through this acquisition, the company expanded its product portfolio across the United States.

- In January 2022, Sandhar Auto Electric Solutions Private Limited was incorporated as a wholly owned Subsidiary Company to undertake e-mobility business and to provide Advanced Technology Solutions. Sandhar Auto Electric Solutions Private Limited is primarily involved in the business of manufacturing parts/components for Battery Electric Vehicles, Hydrogen Fuel Cell Vehicles, Biofuel based technology Vehicle, All Terrain Vehicles (ATVs), and any other Advanced Automotive Technology Vehicles.

- In August 2021, Linamar Corporation announced the partnership with Netherlands-based Innovative Mechatronic Systems B.V. (IMSystems). The partnership focuses on bringing the Archimedes Drive transmission system to market.

- In April 2021, Aludyne announced that it had acquired Shiloh Industries CastLight division. This division manufactures aluminum die-casting parts.

- In February 2021, Endurance Technologies announced that it had started commercial production at the new plant in Kancheepuram, Tamil Nadu, India. The plant will manufacture aluminum die-castings and integration of disc brake components for two and four-wheelers.

- In April 2020, Endurance Technologies acquired a controlling equity stake of 99% in Adler SpA, based out of Trentino, Italy. The acquisition is expected to improve the company's reach across Europe, with the aid of ten manufacturing plants combined in Italy and Germany.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.2 Market Restraints

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD Billion)

- 5.1 By Application

- 5.1.1 Automotive

- 5.1.2 Electrical and Electronics

- 5.1.3 Industrial

- 5.1.4 Other Applications

- 5.2 By Process

- 5.2.1 Pressure Die Casting

- 5.2.2 Vacuum Die Casting

- 5.2.3 Squeeze Die Casting

- 5.2.4 Other Processes

- 5.3 By Raw Material

- 5.3.1 Aluminum

- 5.3.2 Maginesium

- 5.3.3 Zinc

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 France

- 5.4.2.3 Germany

- 5.4.2.4 Italy

- 5.4.2.5 Russia

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 Australia

- 5.4.3.5 Thailand

- 5.4.3.6 Malaysia

- 5.4.3.7 Indonesia

- 5.4.3.8 South Korea

- 5.4.3.9 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 South Africa

- 5.4.5.2 Turkey

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles*

- 6.2.1 Form Technologies Inc. (Dynacast)

- 6.2.2 Nemak

- 6.2.3 Endurance Technologies Limited

- 6.2.4 Sundaram Clayton Ltd

- 6.2.5 Shiloh Industries

- 6.2.6 Georg Fischer Limited

- 6.2.7 Koch Enterprises (Gibbs Die Casting Group)

- 6.2.8 Bocar Group

- 6.2.9 Engtek Group

- 6.2.10 Rheinmetall AG (Rheinmetall Automotive, formerly KSPG AG)

- 6.2.11 Rockman Industries

- 6.2.12 Ryobi Die Casting Ltd

- 6.2.13 Linamar Corporation

- 6.2.14 Meridian Lightweight Technologies UK Ltd

- 6.2.15 Sandhar Group

- 6.2.16 Alcoa Corporation

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

壓鑄市場 - 全球產業規模、佔有率、趨勢、機會和預測,按工藝、原料、應用、地區和競爭細分,2019-2029F

壓鑄市場 - 全球產業規模、佔有率、趨勢、機會和預測,按工藝、原料、應用、地區和競爭細分,2019-2029F 工業鑄造市場:按工藝、材料和應用分類 - 2025-2030 年全球預測

工業鑄造市場:按工藝、材料和應用分類 - 2025-2030 年全球預測 到 2030 年金屬鋰電池外殼市場預測:按電池類型、材料、製造流程、應用和地區進行的全球分析

到 2030 年金屬鋰電池外殼市場預測:按電池類型、材料、製造流程、應用和地區進行的全球分析 金屬鋰電池外殼市場,規模,佔有率,趨勢,產業分析報告:各類型,各用途,各地區 - 市場預測 2025年~2034年

金屬鋰電池外殼市場,規模,佔有率,趨勢,產業分析報告:各類型,各用途,各地區 - 市場預測 2025年~2034年 壓鑄和鍛造市場:按類型、材料和最終用戶分類 - 全球預測 2025-2030

壓鑄和鍛造市場:按類型、材料和最終用戶分類 - 全球預測 2025-2030 壓鑄市場:按類型、材料和最終用戶分類 - 2025-2030 年全球預測

壓鑄市場:按類型、材料和最終用戶分類 - 2025-2030 年全球預測 壓鑄機械市場:按機器類型、原料和行業分類 - 2025-2030 年全球預測

壓鑄機械市場:按機器類型、原料和行業分類 - 2025-2030 年全球預測 鋁零件重力壓鑄市場:按組件、模具類型、最終用戶分類 - 全球預測 2025-2030 年

鋁零件重力壓鑄市場:按組件、模具類型、最終用戶分類 - 全球預測 2025-2030 年 金屬鋰電池外殼市場規模、佔有率、趨勢分析報告:按類型、按應用、按地區、細分市場預測,2025-2030 年

金屬鋰電池外殼市場規模、佔有率、趨勢分析報告:按類型、按應用、按地區、細分市場預測,2025-2030 年 高壓壓鑄設備市場規模、佔有率和趨勢分析報告:按機器類型、按應用、按類別、按產能、按地區和細分市場預測,2024-2030年

高壓壓鑄設備市場規模、佔有率和趨勢分析報告:按機器類型、按應用、按類別、按產能、按地區和細分市場預測,2024-2030年