|

市場調查報告書

商品編碼

1444711

熱噴塗 - 市場佔有率分析、產業趨勢與統計、成長預測(2024 - 2029)Thermal Spray - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

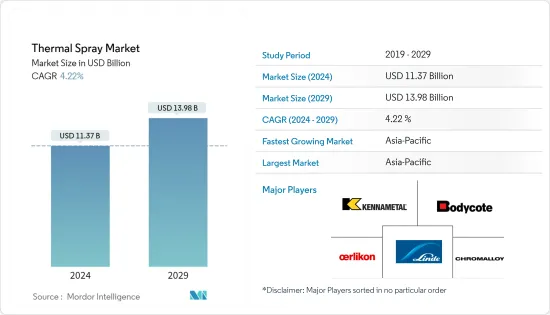

2024年熱噴塗市場規模估計為113.7億美元,預計到2029年將達到139.8億美元,在預測期內(2024-2029年)CAGR為4.22%。

2020 年,市場受到 COVID-19 大流行的負面影響。封鎖擾亂了製造活動和供應鏈,許多預定項目被更改或推遲。然而,自從限制解除以來,由於航空航太、渦輪機、汽車、電子、石油和天然氣、醫療設備等各種最終用途行業的需求不斷成長,該行業一直在復甦。

主要亮點

- 短期內,熱噴塗塗層在醫療器材中的使用不斷增加、熱噴塗陶瓷塗層的日益普及、硬鉻塗層的替代以及熱噴塗塗層在航空航太工業中的使用不斷增加是推動市場的一些因素要求。

- 然而,有關製程可靠性和一致性的問題以及近年來硬質三價鉻塗層的出現可能會阻礙市場的成長。

- 噴塗技術(冷噴塗製程)的進步、熱噴塗加工材料的回收以及石油和天然氣行業不斷成長的需求可能會在未來幾年為市場創造利潤豐厚的成長機會。

- 亞太地區預計將主導市場,並且在預測期內也可能出現最高的CAGR。

熱噴塗市場趨勢

增加在航太工業的使用

- 航空航太工業是熱噴塗材料市場最大的最終用戶。熱噴塗塗層用於航空航太工業,以保護零件在飛行過程中免受極端溫度和壓力的影響。

- 除了提供高耐熱性和長壽命外,它們還旨在保護引擎渦輪葉片和驅動系統。熱噴塗主要用於噴射引擎部件,如曲軸、活塞環、氣缸、閥門等。此外,它們還用於塗層起落架(起落架內的軸承和軸),以承受著陸和起飛時的力。

- 除了延長使用壽命外,熱噴塗塗層還可以提高飛機和旋翼飛機引擎及相關零件的燃油效率、降低維護成本並提高速度。

- 根據日本飛機開發公司的資料,2021 年全球機隊新增波音飛機數量為 340 架,而 2020 年為 157 架。

- 在亞太地區(不含中國),根據波音《2021-2040年商業展望》,到2040年可能將新增交付飛機約8,945架,市場服務價值達19,450億美元。此外,到2040年,光是中國就可能新增交付約8,700架,市場服務價值達1.8兆美元。

- 此外,韓國是美國航空航太業最大的市場之一。韓國政府計劃在 2025 年之前為 KF-X 項目投資 170 億美元。2018 年 11 月,國內航空公司濟州航空訂購了 40 架 737 MAX 8 飛機,價值 44 億美元。這些訂單預計將於 2022 年至 2026 年期間完成。

- 根據美國聯邦航空管理局 (FAA) 的數據,由於航空貨運的成長,預計 2037 年美國商用飛機機隊總數將達到 8,270 架。此外,由於現有機隊老化,美國幹線航空母艦機隊預計將以每年 54 架飛機的速度成長。

- 德國航空航太業包括全國 2,300 多家公司,其中德國北部的公司最集中。該國擁有許多飛機內飾部件和材料生產基地,主要集中在巴伐利亞州、不來梅州、巴登-符騰堡州和梅克倫堡-前波莫瑞州。

- 上述因素預計將在預測期內支持航空航太工業熱噴塗的消費。

亞太地區將主導市場

- 在亞太地區,中國是GDP最大的經濟體。中國和印度是世界上成長最快的經濟體之一。

- 據中國民用航空局(CAAC)稱,中國是最大的飛機製造商和國內航空旅客市場之一。此外,飛機零件及總裝製造業發展迅速,小型飛機零件生產企業超過200家。此外,中國航空公司計劃在未來20年內採購約7,690架新飛機,價值約1.2兆美元,預計將進一步提高熱噴塗市場的市場需求。

- 中國是全球最大的電子產品生產基地。中國積極從事電子產品的製造,例如智慧型手機、電視、電線、電纜、攜帶式計算設備、遊戲系統和其他個人電子設備。 2021年,中國電子產品出口額較上年增加近11.4%。由於國際市場需求持續穩定,主要廠商營收年增16.2%。

- 中國是全球最大的粗鋼生產國。根據世界鋼鐵協會統計,2021年,中國產量佔全球產量的50%以上。 2021年,受政策變動影響,全國粗鋼年產能為10.328億噸,較2020年的10.647億噸下降3%。該國仍然是全球最大的鋼鐵生產國。

- 印度的汽車產業是印度經濟表現的重要指標,因為該產業在技術進步和宏觀經濟擴張中發揮著至關重要的作用。根據 IBEF(印度品牌資產)的數據,2021 年印度乘用車市值為 327 億美元,到 2027 年可能達到 548.4 億美元,2022-2027 年CAGR將超過 9%基礎)。

- 日本的電氣和電子工業是世界領先的工業之一。該國在電腦、遊戲機、手機和各種其他關鍵電腦零件的生產方面處於世界領先地位。消費性電子產品佔日本經濟產出的三分之一。日本電子資訊科技產業協會(JEITA)公佈的資料顯示,2021年,日本電子產業總產值約109,543.46億日元,較上年成長近10%。

- 由於美國和加拿大這些終端用戶產業的崛起,預計北美將在預測期內主導市場。

熱噴塗產業概況

全球熱噴塗市場本質上是分散的。市場上一些主要的參與者包括 OC Oerlikon Management AG、Linde plc、Chromalloy Gas Turbine LLC、Bodycote 和 Kennametal Inc. 等(排名不分先後)。

額外的好處:

- Excel 格式的市場估算 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章:簡介

- 研究假設

- 研究範圍

第 2 章:研究方法

第 3 章:執行摘要

第 4 章:市場動態

- 促進要素

- 熱噴塗塗層在醫療器材中的使用不斷增加

- 熱噴塗陶瓷塗層越來越受歡迎

- 替代硬鉻塗層

- 航太工業中熱噴塗塗層的使用不斷增加

- 限制

- 三價硬鉻塗層的出現

- 有關過程可靠性和一致性的問題

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 替代產品的威脅

- 競爭程度

第 5 章:市場區隔(市場價值規模)

- 產品類別

- 塗料

- 材料

- 塗層材料

- 粉末

- 陶瓷

- 金屬

- 聚合物和其他粉末

- 線材/棒材

- 其他塗料(液體)

- 補充資料(輔助資料)

- 熱噴塗設備

- 熱噴塗系統

- 除塵設備

- 噴槍和噴嘴

- 供料設備

- 備用零件

- 降噪外殼

- 其他熱噴塗設備

- 熱噴塗塗層和飾面

- 燃燒

- 電能

- 最終用戶產業

- 航太

- 工業用燃氣渦輪機

- 汽車

- 電子產品

- 油和氣

- 醫療設備

- 能源與電力

- 煉鋼

- 紡織品

- 印刷和造紙

- 地理

- 亞太

- 中國

- 印度

- 日本

- 韓國

- 東協國家

- 亞太其他地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 歐洲其他地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 中東和非洲其他地區

- 亞太

第 6 章:競爭格局

- 併購、合資、合作與協議

- 市佔率(%)分析

- 領先企業採取的策略

- 公司簡介

- Thermal Spray Material Companies

- Aisher APM LLC

- AMETEK Inc.

- Aimtek Inc.

- C&M Technologies GmbH

- Castolin Eutectic GmbH

- CENTERLINE (WINDSOR) LIMITED (Supersonic Spray Technologies)

- CRS Holdings LLC

- Global Tungsten & Powders Corp.

- HC Starck Inc.

- HAI Inc.

- Hoganas AB

- Hunter Chemical LLC

- Kennametal Inc.

- LSN Diffusion Limited

- Linde PLC

- Metallisation Limited

- Metallizing Equipment Co. Pvt. Ltd

- OC Oerlikon Management AG

- Polymet

- Powder Alloy Corporation

- Saint-Gobain

- Sandvik AB

- Fisher Barton

- Thermion

- Thermal Spray Coatings Companies

- APS Materials Inc.

- ASB Industries Inc.

- Bodycote

- Chromalloy Gas Turbine LLC

- FM Industries Inc.

- FW Gartner Thermal Spraying (Curtis-Wright)

- Fisher Barton (Thermal Spray Technologies)

- Thermion

- TOCALO Co. Ltd

- Lincotek Trento SpA

- Linde PLC (Praxair ST Technologies Inc.)

- OC Oerlikon Management AG

- Thermal Spray Equipment Companies

- Air Products and Chemicals Inc.

- Arzell Inc.

- ASB Industries Inc.

- Bay State Surface Technologies Inc. (Aimtek Inc.)

- Camfil Air Pollution Control (APC)

- Castolin Eutectic

- Centerline (Windsor) Ltd (SUPERSONIC SPRAY TECHNOLOGIES)

- Donaldson Company Inc.

- Flame Spray Technologies BV

- GTV Verschleibschutz GmbH

- HAI Inc.

- Imperial Systems Inc.

- Kennametal Inc.

- Lincotek Equipment SpA

- Linde PLC

- Metallisation Limited

- Metallizing Equipment Co. Pvt. Ltd

- OC Oerlikon Management AG

- Plasma Powders

- Powder Feed Dynamics Inc.

- Progressive Surface

- Saint-Gobain

- Thermion

- Thermal Spray Material Companies

第 7 章:市場機會與未來趨勢

- 噴塗技術的進步(冷噴塗製程)

- 熱噴塗加工材料的回收利用

- 石油和天然氣產業的需求不斷增加

The Thermal Spray Market size is estimated at USD 11.37 billion in 2024, and is expected to reach USD 13.98 billion by 2029, growing at a CAGR of 4.22% during the forecast period (2024-2029).

The market was negatively affected by the COVID-19 pandemic in 2020. The lockdown disrupted manufacturing activities and supply chains, and many scheduled projects were changed or postponed. However, the sector has been recovering since restrictions were lifted owing to the rising demand from various end-use industries, such as aerospace, turbines, automotive, electronics, oil and gas, medical devices, etc.

Key Highlights

- Over the short term, the increasing usage of thermal spray coatings in medical devices, the rising popularity of thermal spray ceramic coatings, the replacement of hard chrome coatings, and the rising use of thermal spray coatings in the aerospace industry are some factors driving the market demand.

- However, issues regarding process reliability and consistency and the emergence of hard trivalent chrome coatings in recent years may hinder the market's growth.

- Advancements in spraying technology (cold spray process), recycling of thermal spray processing materials, and increasing demand from the oil and gas industry will likely create lucrative growth opportunities for the market in the coming years.

- The Asia-Pacific region is expected to dominate the market and is also likely to witness the highest CAGR during the forecast period.

Thermal Spray Market Trends

Increasing Usage in the Aerospace Industry

- The aerospace industry is the largest end-user of the thermal spray material market. Thermal spray coatings are used in the aerospace industry to protect components from extreme temperatures and pressures during flight.

- In addition to providing high thermal resistance and longevity, they are designed to protect engine turbine blades and actuation systems. Thermal sprays are primarily employed in jet engine components, such as crankshafts, piston rings, cylinders, valves, etc. Additionally, they are used in coating landing gear (bearings and axles inside landing gear) to withstand forces during landing and takeoff.

- Apart from enhanced service life, thermal spray coatings offer improved fuel efficiency, reduced maintenance cost, and higher speed in aircraft and rotorcraft engines and related components.

- As per the Japan Aircraft Development Corporation data, the number of Boeing aircraft added to the global aircraft fleet was 340 units in 2021, compared to 157 units in 2020.

- In the Asian-Pacific region (excluding China), according to the Boeing Commercial Outlook 2021-2040, around 8,945 new deliveries may be made by 2040, with a market service value of USD 1,945 billion. Moreover, around 8,700 new deliveries may be made in China alone by 2040, with a market service value of USD 1,800 billion.

- Additionally, South Korea is one of the largest markets for the US aerospace industry. The Korean government plans to invest USD 17 billion in the KF-X program until 2025. In November 2018, the domestic airline, Jeju Air, ordered forty 737 MAX 8 airplanes worth USD 4.4 billion. The orders are projected to be completed between 2022 and 2026.

- According to the Federal Aviation Administration (FAA), the United States' total commercial aircraft fleet is expected to reach 8,270 in 2037 due to air cargo growth. Also, the United States mainliner carrier fleet is expected to grow at a rate of 54 aircraft per year due to the age of the existing fleet.

- The German aerospace industry includes more than 2,300 firms across the country, with northern Germany recording the highest concentration of firms. The country hosts many aircraft interior components and materials production bases, mainly in Bavaria, Bremen, Baden-Wurttemberg, and Mecklenburg-Vorpommern.

- The above factors are expected to support the consumption of thermal spray in the aerospace industry during the forecast period.

Asia-Pacific Region to Dominate the Market

- In the Asia-Pacific region, China is the largest economy in terms of GDP. China and India are among the fastest-growing economies in the world.

- According to the Civil Aviation Administration of China (CAAC), China is one of the largest aircraft manufacturers and markets for domestic air passengers. Moreover, the aircraft parts and assembly manufacturing sector has been growing rapidly, with over 200 small aircraft parts manufacturers. Moreover, Chinese airline companies are planning to purchase about 7,690 new aircraft in the next 20 years, valued at approximately USD 1.2 trillion, which is further expected to raise the market demand for the thermal spray market.

- China is the largest base for electronics production in the world. China is actively engaged in the manufacturing of electronic products, such as smartphones, TVs, wires, cables, portable computing devices, gaming systems, and other personal electronic devices. In 2021, an increment of nearly 11.4% was witnessed in the export value of Chinese electronics products with respect to the previous year. The revenues of major manufacturers expanded by 16.2% on a year-on-year basis due to the consistent demand from the international market.

- China is the largest producer of crude steel globally. According to the World Steel Association, in 2021, China accounted for more than 50% of global production. In 2021, the country's annual production capacity of crude steel stood at 1,032.8 million tons, declining by 3% compared to 1064.7 million tons produced in 2020 due to some policy changes. the country still reminas the largest steel producer globally.

- The automotive industry in India is an important indicator of how well the Indian economy is performing, as this sector plays a vital role in both technological advancements and macroeconomic expansion. In 2021, the Indian passenger car market was valued at USD 32.70 billion, and it is likely to reach a value of USD 54.84 billion by 2027, registering a CAGR of more than 9% between 2022-2027, according to IBEF (Indian Brand Equity Foundation).

- The electrical and electronics industry in Japan is one of the world's leading industries. The country is a world leader in terms of the production of computers, gaming stations, cell phones, and various other key computer components. Consumer electronics account for one-third of the Japanese economic output. According to the data released by the Japan Electronics and Information Technology Industries Association (JEITA), in 2021, the total production value of the electronics industry in Japan amounted to around JPY 10,954,346 million showcasing a rise of nearly 10% from the previous year.

- Owing to the rise of these end-user industries in the United States and Canada, North America is projected to dominate the market during the forecast period.

Thermal Spray Industry Overview

The global thermal spray market is fragmented in nature. Some of the major players in the market include OC Oerlikon Management AG, Linde plc, Chromalloy Gas Turbine LLC, Bodycote, and Kennametal Inc., among others (not in any particular order).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Usage of Thermal Spray Coatings in Medical Devices

- 4.1.2 Rising Popularity of Thermal Spray Ceramic Coatings

- 4.1.3 Replacement of Hard Chrome Coating

- 4.1.4 Rising Use of Thermal Spray Coatings in the Aerospace Industry

- 4.2 Restraints

- 4.2.1 Emergence of Hard Trivalent Chrome Coatings

- 4.2.2 Issues Regarding Process Reliability and Consistency

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Product Type

- 5.1.1 Coatings

- 5.1.2 Materials

- 5.1.2.1 Coating Material

- 5.1.2.1.1 Powders

- 5.1.2.1.1.1 Ceramics

- 5.1.2.1.1.2 Metal

- 5.1.2.1.1.3 Polymers and Other Powders

- 5.1.2.1.2 Wires/Rods

- 5.1.2.1.3 Other Coating Materials (Liquids)

- 5.1.2.2 Supplementary Materials (Auxiliary Material)

- 5.1.3 Thermal Spray Equipment

- 5.1.3.1 Thermal Spray Coating System

- 5.1.3.2 Dust Collection Equipment

- 5.1.3.3 Spray Gun and Nozzle

- 5.1.3.4 Feeder Equipment

- 5.1.3.5 Spare Parts

- 5.1.3.6 Noise-reducing Enclosures

- 5.1.3.7 Other Thermal Spray Equipment

- 5.2 Thermal Spray Coatings and Finishes

- 5.2.1 Combustion

- 5.2.2 Electric Energy

- 5.3 End-user Industry

- 5.3.1 Aerospace

- 5.3.2 Industrial Gas Turbines

- 5.3.3 Automotive

- 5.3.4 Electronics

- 5.3.5 Oil and Gas

- 5.3.6 Medical Devices

- 5.3.7 Energy and Power

- 5.3.8 Steel Making

- 5.3.9 Textile

- 5.3.10 Printing and Paper

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Rest of the Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 South Africa

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%) Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Thermal Spray Material Companies

- 6.4.1.1 Aisher APM LLC

- 6.4.1.2 AMETEK Inc.

- 6.4.1.3 Aimtek Inc.

- 6.4.1.4 C&M Technologies GmbH

- 6.4.1.5 Castolin Eutectic GmbH

- 6.4.1.6 CENTERLINE (WINDSOR) LIMITED (Supersonic Spray Technologies)

- 6.4.1.7 CRS Holdings LLC

- 6.4.1.8 Global Tungsten & Powders Corp.

- 6.4.1.9 H.C. Starck Inc.

- 6.4.1.10 HAI Inc.

- 6.4.1.11 Hoganas AB

- 6.4.1.12 Hunter Chemical LLC

- 6.4.1.13 Kennametal Inc.

- 6.4.1.14 LSN Diffusion Limited

- 6.4.1.15 Linde PLC

- 6.4.1.16 Metallisation Limited

- 6.4.1.17 Metallizing Equipment Co. Pvt. Ltd

- 6.4.1.18 OC Oerlikon Management AG

- 6.4.1.19 Polymet

- 6.4.1.20 Powder Alloy Corporation

- 6.4.1.21 Saint-Gobain

- 6.4.1.22 Sandvik AB

- 6.4.1.23 Fisher Barton

- 6.4.1.24 Thermion

- 6.4.2 Thermal Spray Coatings Companies

- 6.4.2.1 APS Materials Inc.

- 6.4.2.2 ASB Industries Inc.

- 6.4.2.3 Bodycote

- 6.4.2.4 Chromalloy Gas Turbine LLC

- 6.4.2.5 FM Industries Inc.

- 6.4.2.6 FW Gartner Thermal Spraying (Curtis-Wright)

- 6.4.2.7 Fisher Barton (Thermal Spray Technologies)

- 6.4.2.8 Thermion

- 6.4.2.9 TOCALO Co. Ltd

- 6.4.2.10 Lincotek Trento SpA

- 6.4.2.11 Linde PLC (Praxair ST Technologies Inc.)

- 6.4.2.12 OC Oerlikon Management AG

- 6.4.3 Thermal Spray Equipment Companies

- 6.4.3.1 Air Products and Chemicals Inc.

- 6.4.3.2 Arzell Inc.

- 6.4.3.3 ASB Industries Inc.

- 6.4.3.4 Bay State Surface Technologies Inc. (Aimtek Inc.)

- 6.4.3.5 Camfil Air Pollution Control (APC)

- 6.4.3.6 Castolin Eutectic

- 6.4.3.7 Centerline (Windsor) Ltd (SUPERSONIC SPRAY TECHNOLOGIES)

- 6.4.3.8 Donaldson Company Inc.

- 6.4.3.9 Flame Spray Technologies BV

- 6.4.3.10 GTV Verschleibschutz GmbH

- 6.4.3.11 HAI Inc.

- 6.4.3.12 Imperial Systems Inc.

- 6.4.3.13 Kennametal Inc.

- 6.4.3.14 Lincotek Equipment SpA

- 6.4.3.15 Linde PLC

- 6.4.3.16 Metallisation Limited

- 6.4.3.17 Metallizing Equipment Co. Pvt. Ltd

- 6.4.3.18 OC Oerlikon Management AG

- 6.4.3.19 Plasma Powders

- 6.4.3.20 Powder Feed Dynamics Inc.

- 6.4.3.21 Progressive Surface

- 6.4.3.22 Saint-Gobain

- 6.4.3.23 Thermion

- 6.4.1 Thermal Spray Material Companies

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Advancements in Spraying Technology (Cold Spray Process)

- 7.2 Recycling of Thermal Spray Processing Materials

- 7.3 Increasing Demand Frome The Oil and Gas Industry