|

市場調查報告書

商品編碼

1640538

聚丙烯纖維:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Polypropylene Fibers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

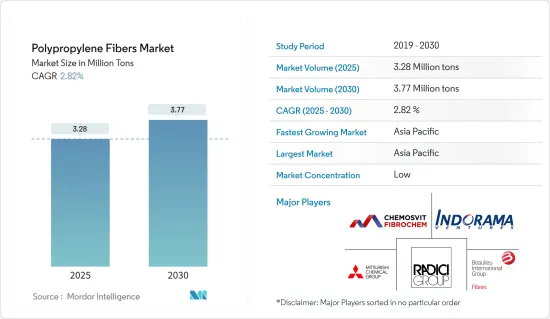

聚丙烯纖維市場規模估計預測2025年為328萬噸,預計2030年將達到377萬噸,預測期(2025-2030年)的複合年成長率為2.82%。

短期內,衛生和醫療領域對聚丙烯纖維的使用增加以及建築業的需求上升是推動市場發展的主要因素。

可用性、更便宜的替代品的可用性以及低熔點等因素可能會阻礙市場成長。

然而,再生聚丙烯纖維的前景很可能成為市場成長的機會。

亞太地區在全球聚丙烯纖維市場中佔據主導地位,並可能在預測期內呈現最高的成長率。

聚丙烯纖維市場趨勢

紡織業可望主導市場

- PPF 在紡織業的應用包括纖維、纖維材料和其他基於 PP 的紡織材料,並用於床罩、地毯、襯墊、地毯、膠帶、繩索、服飾(家居、運動、嬰兒等)防護衣)、技術紡織品和環保紡織品。 PP短纖維的主要分類有地毯型、羊毛型、棉型、超細纖維。

- 聚丙烯繩用於農業和農作物包裝,也可用於重型蔬果人工林,幫助水果蔬菜掛在莖枝上。

- 技術過濾器用於各種工業應用,包括濕式過濾和製藥。這些過濾器對油漆、被覆劑、石化產品等具有優異的耐化學性。

- 根據美國全國紡織組織理事會(NCTO)的資料,2023年美國紡織品和服裝出貨收益將達648億美元。此外,美國紡織業也向美國軍方供應8,000多種不同的紡織產品。

- 同樣,根據聯邦統計局(德國聯邦當局)的數據,紡織業收益預計將在 2022 年達到 129.7 億歐元(139.6 億美元),2023 年達到 123.8 億歐元(133.7 億美元)。

- 聚丙烯纖維因其耐用性、防污性和防潮性、成本效益以及保持鮮豔色彩的能力而常用於地毯。這使得它成為各種環境(包括高流量區域)的實用選擇。

- 根據英國國家統計局的數據,2022 年英國地毯和地墊製造收入達到 7.8 億英鎊(9.8134 億美元)。

- 同樣,根據巴西紡織服飾協會統計,巴西紡織服飾鏈出口額為11.4億美元,進口額為59億美元。

- 鑑於上述情況,紡織業預計將佔據市場主導地位。

亞太地區可望主導市場

- 亞太地區在全球聚丙烯纖維市場中佔據主導地位,預計在預測期內將出現最高成長率。中國憑藉其大規模的生產活動成為聚丙烯纖維的主要生產國。

- 中國是世界上最大的紡織品和服飾生產國和出口國。中國擁有龐大的生產能力,需要更多的紡織和服飾產品。根據國務院新聞辦公室預測,2023年我國重點紡織企業利潤總額年均成長7.2%。同時,2023年中國紡織品服飾出口額將達2,936億美元。

- 但人事費用上升和全球保護主義抬頭削弱了該國的競爭力。近年來,該國人事費用大幅上升,超過了許多亞洲其他國家。

- 此外,聚丙烯纖維具有無毒、低過敏性的特點,廣泛應用於醫療產業,如醫用服飾、一次性產品、創傷護理、醫療設備過濾器和手術網片等。

- 中國擁有僅次於美國的世界第二大醫療產業,醫療市場監管更嚴格。到2030年,中國預計將佔全球醫療保健產業收益的25%。

- 根據中國國家統計局的數據,2023年中國醫療保健費用將達到人民幣22,393億元(3,099.4億美元),與前一年的資料相比成長迅速。

- 印度醫療保健產業的發展主要受健康意識的增強、保險覆蓋率的擴大、收入的增加以及疾病的減少所驅動。印度的醫療保健產業受惠於每年1.6%的人口成長率。

- 印度醫院產業佔全球醫療保健市場的80%,正面臨來自國內外投資者的龐大投資需求,到2023年將達到1,320億美元。

- 聚丙烯纖維廣泛用於建築業,以增強混凝土,提高耐久性,減少開裂,並抵抗化學品和環境因素。

- 預計所有這些因素都將在預測期內推動亞太聚丙烯纖維市場的發展。

聚丙烯纖維產業概況

全球聚丙烯纖維市場細分化,參與企業眾多。然而,主要企業Indorama Ventures 佔有相當大的市場佔有率。主要參與企業(不分先後順序)包括 Beaulieu Fibers International (BFI)、Chemosvit Fibrochem SRO、Radici Partecipazioni SpA、Indorama Ventures 和三菱化學株式會社。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 調查前提條件

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場動態

- 驅動程式

- 擴大衛生和醫療領域的應用

- 建築業需求增加

- 其他

- 限制因素

- 有更便宜的替代品

- 熔點低,在某些應用中無法使用

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

- 原料分析

第5章 市場區隔(市場規模(數量))

- 類型

- 史泰博

- 線

- 最終用戶產業

- 纖維

- 建築學

- 醫療健康產業

- 其他

- 地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 東南亞國協

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 土耳其

- 歐洲其他地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭格局

- 併購、合資、合作與協議

- 市場排名分析

- 主要企業策略

- 公司簡介

- ABC Polymer Industries LLC

- Beaulieu Fibres International(BFI)

- Belgian Fibers

- Chemosvit Fibrochem SRO

- China National Petroleum Corporation

- DuPont

- Fiberpartner Aps

- Freudenberg Group

- Indorama Ventures

- International Fibres Group

- Radici Partecipazioni SpA

- Sika AG

- Mitsubishi Chemical Corporation

- Huimin Taili Chemical Fiber Products Co. Ltd

- Tri Ocean Textile Co. Ltd

- W. Barnet GmbH & Co. KG

- Zenith Fibres Ltd

- Kolon Fiber Inc.

第7章 市場機會與未來趨勢

- 回收聚丙烯纖維的未來用途

The Polypropylene Fibers Market size is estimated at 3.28 million tons in 2025, and is expected to reach 3.77 million tons by 2030, at a CAGR of 2.82% during the forecast period (2025-2030).

Over the short term, the significant factors driving the market are the rising usage of polypropylene fibers in hygiene and health care and the increasing demand for these fibers from the construction industry.

Factors such as availability, cheaper substitute availability, and lower melting points likely hinder the market's growth.

However, the prospects of recycled polypropylene fibers are likely to act as opportunities for market growth.

Asia-Pacific dominated the global polypropylene fibers market and is likely to witness the highest growth rate during the forecast period.

Polypropylene Fibers Market Trends

The Textile Industry is expected to Dominate the Market

- PPF applications in the textile industry include fibers, fibrous materials, and other PP-based textile materials, including bed covers, carpets, underlays, rugs, tapes, ropes, clothing (home, sport, children's protective), technical textiles, and environmentally-friendly textiles. The primary classification of PP staple fibers is carpet, woolen, cotton types, and microfibers.

- Polypropylene ropes are used for agriculture and crop packing and can also be used in heavy fruit and vegetable plantations to help the fruit/vegetable hold on to its stem or branch.

- Technical filters are used in various industrial applications, such as wet filtration and pharmaceuticals. These filters provide excellent chemical resistance to paints, coatings, petrochemicals, etc.

- According to National Council of Textile Organization (NCTO) data, US textile and apparel shipments totaled USD 64.8 billion in 2023. Moreover, the US textile industry supplies over 8,000 different textile products to the US military.

- Similarly, according to the Federal Statistical Office (a federal authority of Germany), the revenue of the textile industry reached EUR 12.97 billion (USD 13.96 billion) in 2022 and EUR 12.38 billion (USD 13.30 billion) in 2023.

- Polypropylene fiber is commonly used in carpets due to its durability, stain, moisture resistance, cost-effectiveness, and ability to retain vibrant colors. This makes it a practical choice for various settings, including high-traffic areas.

- According to the Office for National Statistics (United Kingdom), sales from the manufacture of carpets and rugs in the United Kingdom reached GBP 780 million (USD 981.34 million) in 2022.

- Similarly, as per the Brazilian Association of the Textile and Clothing Industry, Brazil's textile and apparel chain exports and imports are valued at USD 1.14 billion and USD 5.9 billion, respectively.

- Thus, based on the aspects above, the textile segment is expected to dominate the market.

Asia-Pacific to is expected Dominate the Market

- Asia-Pacific dominated the global polypropylene fibers market and will likely witness the highest growth rate during the forecast period. China is a leading producer of polypropylene fibers due to the high number of large-scale manufacturing activities.

- China is the world's largest producer and exporter of textiles and clothing. Due to its enormous production capacity, China needs more textiles and clothing products. According to the State Council Information Office of the People's Republic of China, the total profits of China's major textile enterprises increased by 7.2% annually in 2023. Meanwhile, the country's textile and garments exports hit USD 293.6 billion in 2023.

- However, the increasing labor costs and rising global protectionism weakened its competitiveness. The labor costs in the country increased significantly in recent years and surpassed that of many other countries in Asia.

- Also, polypropylene fiber, known for its non-toxic and hypoallergenic properties, is extensively used in the healthcare industry for applications such as medical clothing, disposable products, wound care, filters for medical devices, and surgical mesh.

- China has the second-largest healthcare industry in the world after the United States, and its healthcare market is more rigorous. By 2030, China will account for 25% of the global healthcare industry's revenue.

- According to the National Bureau of Statistics of China, health expenditures in China were valued at CNY 2,239.3 billion (USD 309.94 billion) in 2023 and have been rapidly growing compared to the previous year's data.

- The healthcare sector in India is mainly driven by increasing health awareness, access to insurance, rising income, and diseases. The medical industry in India is benefiting from the growing population at a rate of 1.6% per year.

- The hospital industry in India, which accounts for 80% of the global healthcare market, is witnessing colossal investor demand from international and domestic investors, reaching USD 132 billion by 2023.

- Polypropylene fiber is widely employed in the construction industry for applications such as reinforcing concrete, enhancing durability, reducing cracking, and resisting chemicals and environmental factors.

- All these factors are expected to boost the polypropylene fibers market in Asia-Pacific during the forecast period.

Polypropylene Fibers Industry Overview

The global polypropylene fibers market is partially fragmented, with many players. However, the leading company, Indorama Ventures, occupies a considerable market share. Some of the key players (not in any particular order) include Beaulieu Fibers International (BFI), Chemosvit Fibrochem SRO, Radici Partecipazioni SpA, Indorama Ventures, and Mitsubishi Chemical Corporation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Rising Usage in Hygiene and Healthcare

- 4.1.2 Rising Demand from the Construction Industry

- 4.1.3 Others

- 4.2 Restraints

- 4.2.1 Availability of Cheaper Substitutes

- 4.2.2 Low Melting Point Hinders Usage in Some Applications

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

- 4.5 Raw Material Analysis

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Type

- 5.1.1 Staple

- 5.1.2 Yarn

- 5.2 End-user Industry

- 5.2.1 Textile

- 5.2.2 Construction

- 5.2.3 Healthcare and Hygiene

- 5.2.4 Other End-user Industries

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Turkey

- 5.3.3.6 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East & Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East & Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 ABC Polymer Industries LLC

- 6.4.2 Beaulieu Fibres International (BFI)

- 6.4.3 Belgian Fibers

- 6.4.4 Chemosvit Fibrochem SRO

- 6.4.5 China National Petroleum Corporation

- 6.4.6 DuPont

- 6.4.7 Fiberpartner Aps

- 6.4.8 Freudenberg Group

- 6.4.9 Indorama Ventures

- 6.4.10 International Fibres Group

- 6.4.11 Radici Partecipazioni SpA

- 6.4.12 Sika AG

- 6.4.13 Mitsubishi Chemical Corporation

- 6.4.14 Huimin Taili Chemical Fiber Products Co. Ltd

- 6.4.15 Tri Ocean Textile Co. Ltd

- 6.4.16 W. Barnet GmbH & Co. KG

- 6.4.17 Zenith Fibres Ltd

- 6.4.18 Kolon Fiber Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Future Applications For Recycled Polypropylene Fibers