|

市場調查報告書

商品編碼

1519842

汽車機器人市場佔有率分析、產業趨勢與統計、成長預測(2024-2029)Automotive Robotics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

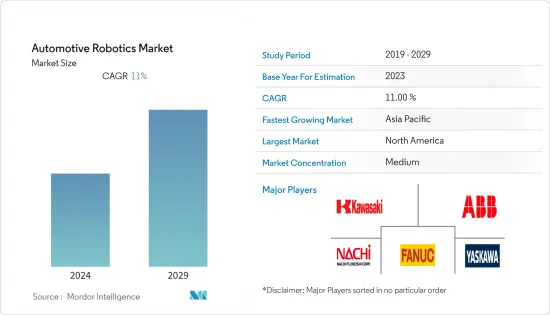

2024年汽車機器人市場規模為108億美元,預計2029年將達到184億美元,在預測期間(2024-2029年)複合年成長率為11%。

汽車機器人旨在支持汽車行業的車輛生產。電動車的驚人成長正在積極引導機器人的使用,以滿足市場不斷成長的消費者需求。汽車產業多年來一直在生產中使用工業機器人。

關節式機器人構成了汽車機器人的大部分,其中焊接是汽車行業最常用的功能。汽車產業的機器人系統具有成本效益、高效且安全。

自動化產業的發展重點是降低成本、節省時間、生產高品質的產品以及以最小的錯誤率提高生產力。在生產工廠中,汽車機器人被部署來實現內部流程自動化並與工人建立合作,從而減少他們的工作量並提高效率。福特汽車和寶馬等公司正在努力將該技術引入其生產工廠。

例如,2023 年 11 月,Realtime Robotics 宣布推出新的最佳化即服務解決方案。該解決方案將專有的最佳化軟體與經驗豐富的機器人技術相結合,並應用工程見解來提高製造商的生產力。它最近被德國漢諾威的大眾商用車公司用於電動車製造的概念驗證計劃。

隨著汽車技術的進步和電動車需求的增加,汽車機器人預計將在汽車行業中強勁成長,汽車生產過程中涉及各種機器人任務。考慮到市場潛力,機器人製造商正在努力推出各種新型號,以滿足汽車產業對機器人的高需求。

例如,2023年6月,ABB宣布推出四款全新大型機器人型號和22個變體,以IRB 6710、IRB 6720、IRB 6730和IRB 6740等下一代型號為汽車行業客戶提供支援。

預計北美在預測期內成長最快,其次是歐洲和亞太地區。主要企業之間的策略聯盟、新興國家可支配收入增加導致的汽車產量增加以及引入節能汽車機器人的研發活動投資增加等因素為市場帶來了積極的前景。

汽車機器人市場趨勢

焊接機器人佔有率第一

汽車產業已廣泛採用汽車機器人,其中焊接是最突出的應用之一。製造環境中常用的焊接機器人有兩種。它們是半自動焊接機器人系統和自動焊接機器人系統,用於汽車製造中的大多數焊接任務,提供精度、效率和速度。

這些機器人有可能透過提高工廠安全性和降低人事費用將生產時間延長一倍甚至三倍,從而幫助節省數百萬美元。

考慮到產業的減重需求,機器人焊接機在先進一流車輛的生產中發揮重要作用。由於嚴格的行業標準,機器人不斷證明其能力。

隨著技術的進步,越來越多的公司依賴機器人焊接系統來實現需要更精確組裝的高科技應用,例如電動車和自動駕駛汽車。

例如,2023年7月,Ficep UK宣布推出新的自動化和機器人加工解決方案,以回應市場對高品質焊接系統的需求,以解決技術純熟勞工短缺問題並提高生產力。在與 AGT Robotics 的新合作中,Ficep 開發了 Sabre 焊接機器人,以無縫解決當今鋼結構製造市場中製造商面臨的最困難和集中工藝。

機器人技術在許多行業的製造中發揮著重要作用,其中汽車佔據了壓倒性的市場佔有率。許多公司希望科技能夠根據他們的需求而發展。

例如,2023年1月,自動化生產解決方案軟體供應商Oqton與彈性電弧焊接機器人製造商Valk Welding宣佈建立新的合作關係。兩家公司共同開發的新技術和工藝旨在加強自動化機器人焊接在專業或小批量生產中的使用。

汽車產業正在將重點轉向新技術趨勢,例如更小的機器人和控制器、更快的通訊速度、更低的飛濺和更快的焊接。因此,焊接領域預計佔有率最高。

亞太地區可望引領汽車機器人市場

由於對流程自動化、效率和生產力提高以及人為錯誤減少的需求不斷成長,亞太地區擴大採用機器人技術。機器人技術正在應用於汽車、醫療保健、國防和航太等多個領域,以實現流程自動化和高效管理資源。工業機器人主要應用在亞太地區,因為它們在汽車產業中佔據主導地位,且製造設備成本較低。由於亞太地區中小型工業的快速擴張,汽車機器人市場預計在預測期內將顯著成長。

亞太地區是全球成長最快的地區,印度、中國、台灣和韓國等國家正成為該地區的領導者。 ABB 和 KUKA 等主要供應商在該地區設有業務。政府法規和資金正在授權計劃改善基礎設施。這些方面有利於該地區成為汽車製造中心,並正在推動汽車機器人市場的發展。

中國和印度是亞太地區的主要發展中國家,汽車、電子、航空等眾多產業都在這些國家開設工廠,增加了汽車機器人的需求,使亞太地區成為新興地區已經成為一個地區了。

該地區的主要企業正在大力投資即將推出的車輛,同時採用機器人技術和其他先進製造技術。例如,2023年11月,RSP將進入印度價值130億美元的機器人自動化市場,並於2024年推出製造部門。斯堪的納維亞機器人系統印度私人有限公司已在清奈註冊。我們為印度客戶提供汽車、電子等各領域的工業機器人配件。

2023年8月,中國汽車製造商吉利控股集團推出高階智慧科技品牌“吉悅”,並推出首款高科技車型。極悅01是與百度公司在「汽車機器人」領域合作的成果,將由吉利汽車生產。

因此,由於亞太地區的這一發展,亞太地區所佔的佔有率是最高的。

汽車機器人產業概況

汽車機器人市場由全球和地區的老牌企業進行整合和主導。公司採用新產品發布、聯盟和合併等策略來維持其市場地位。

- 2023年8月,消費汽車ADAS(高階駕駛輔助系統)節能運算解決方案領先供應商地平線機器人公司與Aptiv PLC及其中國子公司Wind River建立了策略合作夥伴關係。此次合作標誌著安波福與中國國內汽車級運算解決方案供應商在 ADAS 和自動駕駛領域的首次合作。

該市場的主要企業包括Nachi-Fujikoshi Corp、ABB Ltd、FANUC Corporation、Kawasaki Robotics和Yaskawa Electric Corporation。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 調查先決條件

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 市場促進因素

- 汽車工業快速成長

- 市場限制因素

- 引進工業機器人成本高

- 產業吸引力-波特五力分析

- 新進入者的威脅

- 買家/消費者的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭公司之間敵對關係的強度

第5章市場區隔:市場規模(單位:十億美元)

- 按最終用戶類型

- 汽車製造商

- 汽車零件製造商

- 依零件類型

- 控制器

- 機械臂

- 末端執行器

- 驅動器與感測器

- 依產品類型

- 笛卡兒機器人

- SCARA機器人

- 關節式機器人

- 其他產品類型

- 依功能類型

- 焊接機器人

- 噴漆機器人

- 組裝機器人

- 切割/切割機器人

- 按地區

- 北美洲

- 美國

- 加拿大

- 北美其他地區

- 歐洲

- 德國

- 英國

- 法國

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太地區

- 世界其他地區

- 南美洲

- 中東/非洲

- 北美洲

第6章 競爭狀況

- 供應商市場佔有率

- 公司簡介

- ABB Ltd

- Omron Adept Robotics

- FANUC Corp.

- Honda Motor Co. Ltd

- Kawasaki Robotics

- KUKA Robotics

- Yaskawa Electric Corporation

- Harmonic Drive System

- RobCo SWAT Ltd

- Nachi-Fujikoshi Corp.

第7章 市場機會及未來趨勢

The Automotive Robotics Market size is estimated at USD 10.80 billion in 2024, and is expected to reach USD 18.40 billion by 2029, growing at a CAGR of 11% during the forecast period (2024-2029).

Automotive robots are designed to support the production of automobiles in the automotive industry. This extraordinary growth of electric vehicles is positively inducing the use of robots to meet the market's growing consumer requirements. The automotive industry has been using industrial robotics in production for many years.

Articulated robots hold a large part of automotive robots; by function, welding makes the largest use of robots in the automotive industry. Robotic systems in the automotive industry are cost-effective, efficient, and safe, as they can do their job quicker than their human counterparts.

Several companies majorly focus on reducing costs, saving time, producing high-quality products, and increasing productivity with a minimum error rate in the automation industry, thus driving the market. In the production plant, automotive robots are deployed to automate internal processes to reduce the workload of employees by creating a work collaboration with the workers to improve efficiency. Companies such as Ford Motors Co. and BMW are working on introducing technology in their production plants.

For instance, in November 2023, Realtime Robotics announced the launch of its new Optimization-as-a-Service solution. The solution uses a combination of proprietary optimization software and experienced robotics and applies engineering insights to improve a manufacturer's overall productivity. It has recently been used by Volkswagen Commercial Vehicles in Hanover, Germany, in a proof-of-concept project for EV manufacturing.

With the rising advancements in vehicle technologies and growing demand for electric vehicles, automotive robotics is expected to witness strong growth in the automotive industry for various robotic operations involved in the automobile production process. Considering the market potential, robotic manufacturers are working on launching various new models to cater to the high demand for robotics in the automotive industry.

For example, in June 2023, ABB announced the launch of four new large robot models and 22 variants to support automotive customers with next-generation models, including the IRB 6710, IRB 6720, IRB 6730, and IRB 6740.

North America is expected to grow significantly during the forecast period, followed by Europe and Asia-Pacific. Factors such as strategic collaborations among key players, growing vehicle production due to inflating disposable incomes in emerging economies, and rising investments in R&D activities for introducing energy-efficient automotive robots are creating a positive outlook for the market.

Automotive Robotics Market Trends

Welding Robots Hold the Highest Share

The automotive industry has adopted automotive robotics widely, with welding being one of the most prominent applications. Within the manufacturing environment, two types of welding robots are generally used, i.e., semiautomatic and automatic welding robot systems, for most welding operations in automotive manufacturing, which offer precision, efficiency, and speed.

These robots have increased factory safety and have helped save millions of dollars as they have the potential to double, or even triple, production time by cutting labor costs.

Considering the industry demands for lighter vehicles, robotic welders play an important role in producing advanced, top-tier vehicles. With strict industry standards, robots consistently prove their ability.

More companies are relying on robotic welding systems with technological advances for high-tech applications such as EV vehicles and self-driving cars, which require even more precise assembly.

For instance, in July 2023, Ficep UK launched a new automatic and robotic processing solution in response to market demand for a quality welding system to help address skilled labor shortages and increase productivity. In a new partnership with AGT Robotics, Ficep developed the Sabre welding robot to seamlessly tackle the most challenging and labor-intensive processes fabricators face in today's structural steel fabrication market.

Robotics play an important part in manufacturing in many industries, with automotive being the dominating segment. Many companies expect technology to evolve with their needs.

For example, in January 2023, Oqton, a software provider of automation production solutions, and Valk Welding, a manufacturer of flexible arc welding robots, announced a new partnership. The new techniques and processes jointly developed by the companies are intended to enhance the utilization of automated robotic welding for unique or small-batch production.

The automotive industry is shifting its focus toward new technology trends, like compact robots and controllers, higher communication speed, low spatter, and high-speed welding. Thus, the welding segment is expected to hold the highest share.

Asia-Pacific is Expected to Lead the Automotive Robotics Market

Robotics technology is increasingly being adopted in Asia-Pacific due to rising demand for the automation of processes, improved efficiency and productivity, and reduced human errors. Various sectors, including automotive, healthcare, defense, and aerospace, have adopted robotics technology for process automation and efficient resource management. Industrial robots are used mainly in Asia-Pacific due to their dominance in the automotive industry and low cost of manufacturing units. The automotive robotics market is expected to witness major growth during the forecast period due to the rapid expansion of small and medium-scale industries across Asia-Pacific.

Asia-Pacific is the fastest developing region globally, with countries like India, China, Taiwan, and South Korea evolving as the leaders in this region. Leading vendors, such as ABB and KUKA, are instituting the region as their operational bases. Government regulations and funds have empowered projects to improve the infrastructure. These aspects have made the region the favored automotive manufacturing hub, thus driving the automotive robotics market.

China and India are the principal countries in Asia-Pacific in terms of development, and many industries, such as automotive, electronics, and aviation, are opening their factories in these countries, thus generating the demand for automotive robotics and making Asia-Pacific an emerging region.

Major players in the region are adopting robotics and other advanced manufacturing technologies while also making huge investments in their upcoming vehicles. For instance, in November 2023, RSP tapped into India's USD 13 billion robotics and automation market to start a manufacturing unit in 2024. The Indian entity Scandinavian Robot Systems India Private Limited has been registered in Chennai. It will supply a range of industrial robot accessories to Indian customers of various sectors, such as automotive and electronics.

In August 2023, Chinese automaker Geely Holding Group launched a premium intelligent technology brand, JI YUE, and unveiled its first high-tech model. The JI YUE 01, the results of a tie-up with Baidu Inc. on "automotive robotics," will be produced by Geely.

Thus, owing to such developments in the region, Asia-Pacific holds the highest share.

Automotive Robotics Industry Overview

The automotive robotics market is consolidated and led by globally and regionally established players. The companies adopt strategies such as new product launches, collaborations, and mergers to sustain their market positions.

- In August 2023, Horizon Robotics, a leading provider of energy-efficient computing solutions for advanced driver assistance systems (ADAS) in consumer vehicles, formed a strategic partnership with Aptiv PLC and its subsidiary Wind River in China. The collaboration marks Aptiv's first partnership with a Chinese domestic auto-grade computing solutions supplier for ADAS and automated driving.

Some of the major players in the market include Nachi-Fujikoshi Corp., ABB Ltd, FANUC Corporation, Kawasaki Robotics, and Yaskawa Electric Corporation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Exponential Increase in Automotive Sector

- 4.2 Market Restraints

- 4.2.1 High Cost of Installation Related to Industrial Robots

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size in Value USD billion)

- 5.1 By End-user Type

- 5.1.1 Vehicle Manufacturers

- 5.1.2 Automotive Component Manufacturers

- 5.2 By Component Type

- 5.2.1 Controllers

- 5.2.2 Robotic Arms

- 5.2.3 End Effectors

- 5.2.4 Drive and Sensors

- 5.3 By Product Type

- 5.3.1 Cartesian Robots

- 5.3.2 SCARA Robots

- 5.3.3 Articulated Robots

- 5.3.4 Other Product Types

- 5.4 By Function Type

- 5.4.1 Welding Robots

- 5.4.2 Painting Robots

- 5.4.3 Assembling and Disassembling Robots

- 5.4.4 Cutting and Milling Robots

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 Rest of the World

- 5.5.4.1 South America

- 5.5.4.2 Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles*

- 6.2.1 ABB Ltd

- 6.2.2 Omron Adept Robotics

- 6.2.3 FANUC Corp.

- 6.2.4 Honda Motor Co. Ltd

- 6.2.5 Kawasaki Robotics

- 6.2.6 KUKA Robotics

- 6.2.7 Yaskawa Electric Corporation

- 6.2.8 Harmonic Drive System

- 6.2.9 RobCo S.W.A.T Ltd

- 6.2.10 Nachi-Fujikoshi Corp.