|

市場調查報告書

商品編碼

1519900

苯乙烯嵌段共聚物(SBC)的全球市場:市場佔有率分析、產業趨勢/統計、成長預測(2024-2029)Styrenic Block Copolymers (SBCs) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

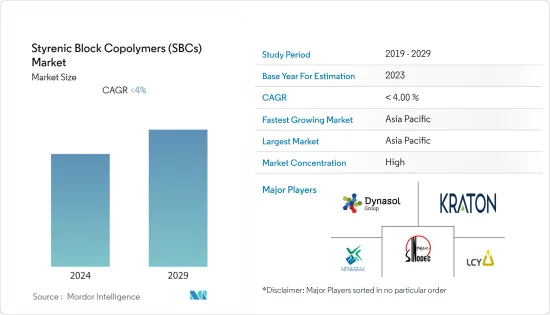

就產量而言,全球苯乙烯嵌段共聚物(SBC)市場規模到2024年將達到289萬噸,2024-2029年預測期間複合年成長率為3.92%,2029年將達到362萬噸。增加到1000萬噸。

COVID-19大流行阻礙了苯乙烯嵌段共聚物市場。考慮到這種情況,在封鎖期間,建築建設活動暫時停止,以遏制病毒的傳播。根據歐盟統計局的數據,歐盟 19 個國家的建設業下降了 28.4%,歐盟 27 個國家的建築業下降了 24%,聚丁二烯(SBS) 的需求下降。然而,由於瀝青改性(鋪路和屋頂)和製鞋產業的需求增加,放鬆管制後市場出現顯著成長。

短期內,瀝青改性應用的增加和製鞋行業採用的增加預計將刺激市場需求。

然而,對無瀝青道路和屋頂建設的日益關注預計將抑制市場成長。

黏劑的成長機會可能會在未來幾年創造市場機會。

亞太地區在市場上佔據主導地位,預計在預測期內仍將保持最高的複合年成長率。

苯乙烯嵌段共聚物(SBC)的市場趨勢

瀝青改性領域佔據市場主導地位

- 瀝青是道路、機場跑道、滑行道、自行車道等的重要建築材料。

- 黏合劑改質劑(SBC) 等改質劑可提高瀝青路面的抗熱裂、車轍和剝落等路面破壞能力,從而提高瀝青路面的性能並延長其使用壽命。

- 近年來,瀝青用改性瀝青的需求量不斷增加。這項需求與正在進行的道路建設活動直接相關。道路和人行道每天都承受重載,因此承受著持續的壓力。它們需要維護並且需要不時進行維修。此外,道路的建設和維護方式對車輛在其上滾動和爬行所消耗的能量有重大影響。

- 世界各國政府花錢修復和拓寬已開發國家現有的道路,並在開發中國家中國家建造全新的道路。

- 例如,2022年9月,歐盟委員會將透過歐洲互聯互通基金(CEF)投資50億歐元用於基礎建設計劃,包括道路和人行道,主要針對跨歐洲運輸網路(TEN-T網路)和多式聯運運輸(52.9 億美元)。

- 此外,美國瀝青路面市場的 65% 是公共資助的高速公路計劃,住宅和住宅建築佔剩餘的 35%。各級政府(聯邦/州/地方)每年在高速公路、道路和橋樑上的資本支出約為 800 億美元,其中約一半來自聯邦政府。

- 此外,聯邦公路管理局 (FHWA) 並未追蹤大量使用 SBC 的 189 萬英里當地道路的路面類型。

- 印度品牌資產基金會(IBEF)的報告顯示,印度高速公路建設將從2022年的10,457公里增加到2023年的10,993公里。

- 所有這些因素預計將增加對瀝青改性的需求,從而增加預測期內苯乙烯嵌段共聚物的成長。

亞太地區主導市場

- 亞太地區是全球苯乙烯嵌段共聚物市場最大的區域市場。該地區苯乙烯嵌段共聚物的主要消費國家包括中國、印度和日本。

- 最近在中國主要城市爆發新冠肺炎 (COVID-19) 疫情後,中國正在加強投資和高速公路建設力度,努力穩定經濟。根據國家統計局數據,2023年1月至8月中國資本投資達28.59兆元人民幣(約3.91兆美元),較2022年同期成長6.8%。

- 國家發展和改革委員會、運輸部在聯合記者會上宣布,到2035年,將建成功能齊全、高效安全的高速公路網。此外,中國計劃在2035年建成46.1萬公里的高速公路網,並於2050年將其擴展為世界上最好的高速公路網之一。

- 中國是最大的鞋類製造商、消費國和供應商。根據《世界鞋業年鑑2023》顯示,2022年,中國生產鞋類約130.47億雙,消費量39.3億雙,佔全球鞋類消費量的17.9%。同年,印度出口鞋類約93.08億雙,約佔全球鞋類出口額的61.3%。

- 印度道路運輸和公路部長表示,印度的建築業目前位居世界第三,未來五年可能成為世界第一。據國家投資促進和便利化局稱,到2025年印度建築業預計將達到1.4兆美元,以支撐苯乙烯嵌段共聚物的需求。

- 根據印度包裝工業協會(PIAI)的數據,印度包裝產業在經濟中排名第五。該協會預測,到2025年,包裝產業的產值將達到2,048.1億美元。這種情況可能會在預測期內提振受調查市場的需求。

- 日本的包裝產業,包括食品和藥品包裝,預計在未來幾年將成長。在目前的市場情況下,日本是世界上人均包裝材料消費量最高的國家。在亞洲,日本的包裝食品消費佔有率則位居第二,僅次於中國。對於食品和飲料包裝專業人士來說,這是一個巨大的商機。

- 根據日本包裝研究所 (JPI) 的數據,2022 年日本包裝產業的總出貨收益將約為6.58 兆日圓(約500 億美元),而前一年約為6.17 兆日圓(約合500 億美元)。根據Statista預測,食品飲料產業預計2024年將達到6,271萬美元,2027年將達到8,053萬美元。食品和飲料行業的這些趨勢預計將在未來幾年增加所調查市場對包裝和聚合物改性應用的需求。

- 由於上述因素,亞太苯乙烯嵌段共聚物市場預計在預測期內將顯著成長。

苯乙烯嵌段共聚物(SBC)產業概況

苯乙烯嵌段共聚物 (SBC) 市場因其性質而得到部分整合。該市場的主要企業包括中國石化集團公司(SINOPEC)、李長榮集團、台橡公司、戴納索集團和科騰公司。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 調查先決條件

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 促進因素

- 增加瀝青改性的使用

- 鞋業就業增加

- 抑制因素

- 越來越關注道路和屋頂的無瀝青施工

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 買方議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

- 價格概覽(2019-2029)

第5章市場區隔(市場規模:基於數量)

- 類型

- 聚丁二烯(SBS)

- 苯乙烯-異戊二烯-苯乙烯 (SIS)

- 氫化SBC (匯豐銀行)

- 目的

- 瀝青改性(鋪路/屋頂)

- 鞋類

- 聚合物改性

- 黏劑/密封劑

- 其他用途

- 地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 馬來西亞

- 泰國

- 印尼

- 越南

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 義大利

- 法國

- 俄羅斯

- 西班牙

- 土耳其

- 北歐國家

- 歐洲其他地區

- 南美洲

- 巴西

- 阿根廷

- 哥倫比亞

- 南美洲其他地區

- 中東/非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 卡達

- 埃及

- 奈及利亞

- 南非

- 亞太地區

第6章 競爭狀況

- 併購、合資、聯盟和協議

- 市場排名分析

- 主要企業策略

- 公司簡介

- Avient Corporation

- China Petrochemical Corporation(Sinopec)

- Grupo Dynasol

- INEOS

- Kraton Corporation

- Kuraray Co. Ltd

- LCY Group

- LG Chem

- TSRC

- Versalis SPA

- Zeon Corporation

第7章 市場機會及未來趨勢

- 黏劑的成長機會

The Styrenic Block Copolymers Market size in terms of production volume is expected to grow from 2.89 Million tonnes in 2024 to 3.62 Million tonnes by 2029, at a CAGR of 3.92% during the forecast period (2024-2029).

The COVID-19 pandemic hampered the styrenic block copolymers market. Considering this scenario, building and construction activities were stopped temporarily during the lockdown to curb the spread of the virus. According to Eurostat, the construction industry declined by 28.4% in the EU-19 countries and by 24% in the European Union (EU-27) countries, thereby witnessing a reduction in demand for styrene-butadiene-styrene (SBS). However, the market registered a significant growth rate after the restrictions were lifted due to the increasing demand from asphalt modification (paving and roofing) and footwear industries.

Over the short term, increasing applications in bitumen modification and the rising adoption in the footwear industry are expected to stimulate market demand.

However, the growing focus on asphalt-free construction of roads and roofing is expected to restrain market growth.

Growth opportunities in hot-melt adhesives are likely to create market opportunities in the coming years.

Asia-Pacific is expected to dominate the market and is likely to witness the highest CAGR during the forecast period.

Styrenic Block Copolymers (SBCs) Market Trends

The Asphalt Modification Segment to Dominate the Market

- Asphalt is an important construction material for roads, airport runways, taxiways, bicycle paths, etc.

- Modifiers, such as binder modifiers (SBCs), improve the performance of asphalt pavements by increasing their resistance to pavement distresses, such as thermal cracking, rutting, stripping, etc., thereby prolonging their service life.

- In recent years, the demand for modified bitumen used in asphalt has been witnessing steady growth. This demand directly correlates with ongoing road construction activities. Roadways and walkways are under continuous stress as they are subjected to heavy loads daily. They require maintenance and are subject to repair from time to time. Moreover, how roads are built and maintained significantly impacts the energy that is burned by the vehicles that roll or crawl on the surface.

- Governments worldwide are spending money to restore or expand existing roadways in the developed world and construct entirely new ones in the developing world.

- For instance, in September 2022, the European Commission released EUR 5 billion (USD 5.29 billion) through the Connecting Europe Facility (CEF) in infrastructure projects, which will include roadways and walkways, targeting mainly the trans-European transport network (TEN-T network) and multimodal transport.

- Moreover, 65% of the asphalt pavement market in the United States can be accounted for publicly funded highway projects, with residential and non-residential construction making up the remaining 35%. Capital spending on highways, roads, and bridges by all levels of government (federal/state/local) is around USD 80 billion annually, about half of which comes from federal funding.

- Furthermore, the Federal Highway Administration (FHWA) does not track pavement type for 1.89 million miles of local roads where the use of SBC is significant.

- As per the report of the Indian Brand Equity Foundation (IBEF), highway construction in India increased from 10,457 km in 2022 to 10,993 km in 2023.

- All such factors are likely to increase the demand for asphalt modification, which will, in turn, increase the growth of styrenic block copolymers during the forecast period.

Asia-Pacific to Dominate the Market

- Asia-Pacific represents the largest regional market for styrenic block copolymers market globally. The major countries responsible for the consumption of styrenic block copolymers in the region include China, India, and Japan.

- China is stepping up investment and highway construction as it scrambles to stabilize its economy following the recent outbreak of COVID-19 in major Chinese cities. According to the National Bureau of Statistics, China's capital investment reached CNY 28.59 trillion (~USD 3.91 trillion) in the first eight months of 2023, up by 6.8% compared to the same period in 2022.

- The National Development and Reform Commission (NDRC) and the Ministry of Transport announced in a joint news briefing that they would build a highway network that is fully functional, efficient, and safe by 2035. Moreover, China plans to build a 461,000 km highway network by 2035 and expand it into a world-class network by 2050.

- China is the largest manufacturer, consumer, and supplier of footwear. According to the World Footwear Yearbook 2023, in 2022, the country produced about 13,047 million pairs of footwear, while consumption was about 3,930 million, representing 17.9% of the total global footwear consumption. In the same year, the country exported about 9,308 million pairs of footwear, representing about 61.3% of the global exports of footwear.

- The construction sector in India, which is currently the third largest in the world, has the capability to become the largest in the world in the next 5 years, as per the Union Minister for Road Transport & Highways. According to the National Investment Promotion and Facilitation Agency, the construction Industry in India is expected to reach USD 1.4 trillion by 2025, thus supporting the demand for styrenic block copolymers from the industry.

- According to the Packaging Industry Association of India (PIAI), the country's packaging sector is the fifth largest sector in its economy. The association has predicted that the packaging sector will reach USD 204.81 billion by 2025. This scenario may boost the demand for the market studied during the forecast period.

- The Japanese packaging industry, including food and pharmaceutical packaging, is expected to grow in the coming years. In the present market scenario, Japan has the world's highest per capita consumption of packaging materials. In Asia, Japan holds the second-highest packaged food consumption share, next to China. This is a good business opportunity for food and beverage packaging professionals.

- As per the Japan Packaging Institute (JPI), the total shipment value of the Japanese packaging industry was around JPY 6.58 trillion (~USD 0.05 trillion) in 2022 compared to around JPY 6.17 trillion (~USD 0.05 trillion) in the previous year. The food and beverage industry is expected to reach USD 62.71 million in 2024 and is projected to reach USD 80.53 million by 2027, as per Statista forecast. Such trends in the food and beverage industry are expected to boost the demand for packaging, uplifting the polymer modification application of the market studied in the coming years.

- Owing to the factors mentioned above, the market for styrenic block copolymers in Asia-Pacific is projected to grow significantly during the forecast period.

Styrenic Block Copolymers (SBCs) Industry Overview

The styrenic block copolymers (SBCs) market is partially consolidated in nature. Some of the major players in the market include China Petrochemical Corporation (SINOPEC), LCY Group, TSRC Corporation, Dynasol Group, and Kraton Corporation (not in any particular order).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Application in Bitumen Modification

- 4.1.2 Rising Adoption in the Footwear Industry

- 4.2 Restraints

- 4.2.1 Growing Focus on Asphalt-free Construction of Roads and Roofing

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

- 4.5 Price Overview (2019-2029)

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Type

- 5.1.1 Styrene-Butadiene-Styrene (SBS)

- 5.1.2 Styrene-Isoprene-Styrene (SIS)

- 5.1.3 Hydrogenated SBC (HSBC)

- 5.2 Application

- 5.2.1 Asphalt Modification (Paving and Roofing)

- 5.2.2 Footwear

- 5.2.3 Polymer Modification

- 5.2.4 Adhesives and Sealants

- 5.2.5 Other Applications

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Malaysia

- 5.3.1.6 Thailand

- 5.3.1.7 Indonesia

- 5.3.1.8 Vietnam

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Russia

- 5.3.3.6 Spain

- 5.3.3.7 Turkey

- 5.3.3.8 Nordic Countries

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 Qatar

- 5.3.5.4 Egypt

- 5.3.5.5 Nigeria

- 5.3.5.6 South Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Avient Corporation

- 6.4.2 China Petrochemical Corporation (Sinopec)

- 6.4.3 Grupo Dynasol

- 6.4.4 INEOS

- 6.4.5 Kraton Corporation

- 6.4.6 Kuraray Co. Ltd

- 6.4.7 LCY Group

- 6.4.8 LG Chem

- 6.4.9 TSRC

- 6.4.10 Versalis SPA

- 6.4.11 Zeon Corporation

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growth Opportunities in Hot-melt Adhesives

醫用苯乙烯嵌段共聚物市場(依產品、應用、國家及地區)-2025 年至 2032 年全球產業分析、市場規模、市場佔有率及預測

醫用苯乙烯嵌段共聚物市場(依產品、應用、國家及地區)-2025 年至 2032 年全球產業分析、市場規模、市場佔有率及預測 苯乙烯嵌段共聚物市場按產品類型、形式、加工技術、應用、分銷管道和最終用途分類 - 2025 年至 2030 年全球預測SBC 及其衍生物市場按產品類型(苯乙烯-異戊二烯-苯乙烯、苯乙烯-丁二烯-苯乙烯、苯乙烯-乙烯-丁二烯-苯乙烯、SEPS 和其他 H-SBC)、應用和地區分類,2025 年至 2033 年

苯乙烯嵌段共聚物市場按產品類型、形式、加工技術、應用、分銷管道和最終用途分類 - 2025 年至 2030 年全球預測SBC 及其衍生物市場按產品類型(苯乙烯-異戊二烯-苯乙烯、苯乙烯-丁二烯-苯乙烯、苯乙烯-乙烯-丁二烯-苯乙烯、SEPS 和其他 H-SBC)、應用和地區分類,2025 年至 2033 年 2025 年全球醫用苯乙烯嵌段共聚物市場報告

2025 年全球醫用苯乙烯嵌段共聚物市場報告 苯乙烯嵌段共聚物(SBC)市場(全球)(2018-2034)

苯乙烯嵌段共聚物(SBC)市場(全球)(2018-2034) 醫用苯乙烯嵌段共聚物市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測

醫用苯乙烯嵌段共聚物市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測 2024 年至 2031 年苯乙烯嵌段共聚物市場(按類型、應用、最終用戶和地區)2024-2032 年按類型(苯乙烯-丁二烯-苯乙烯、苯乙烯-異戊二烯-苯乙烯、氫化 SBC 等)、應用和地區分類的苯乙烯嵌段共聚物市場報告全球醫用苯乙烯嵌段共聚物市場研究報告 - 2024 年至 2032 年產業分析、規模、佔有率、成長、趨勢與預測苯乙烯嵌段共聚物市場、佔有率、規模、趨勢、行業分析報告:依產品、依應用、依最終用戶、依地區、依細分市場、預測,2024-2032年

2024 年至 2031 年苯乙烯嵌段共聚物市場(按類型、應用、最終用戶和地區)2024-2032 年按類型(苯乙烯-丁二烯-苯乙烯、苯乙烯-異戊二烯-苯乙烯、氫化 SBC 等)、應用和地區分類的苯乙烯嵌段共聚物市場報告全球醫用苯乙烯嵌段共聚物市場研究報告 - 2024 年至 2032 年產業分析、規模、佔有率、成長、趨勢與預測苯乙烯嵌段共聚物市場、佔有率、規模、趨勢、行業分析報告:依產品、依應用、依最終用戶、依地區、依細分市場、預測,2024-2032年