|

市場調查報告書

商品編碼

1519906

聚氨酯(PU)塗料的全球市場:市場佔有率分析、產業趨勢/統計、成長預測(2024-2029)Polyurethane (PU) Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

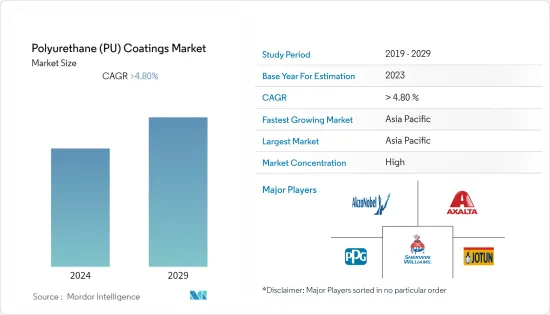

預計2024年全球聚氨酯塗料市場規模將達211.5億美元,2029年將達268.8億美元,2024年至2029年複合年成長率超過4%。

2020 年市場受到 COVID-19 的負面影響。大流行的情況已使世界上多個國家處於封鎖狀態。結果,所有製造和建設活動都停止了,對聚氨酯塗料的需求產生了負面影響。不過,情況有所好轉,聚氨酯塗料市場的成長已經恢復。

主要亮點

- 建築業正在推動市場成長,因為聚氨酯塗料被用作外牆塗料、內牆塗料、地板材料、屋頂和隔熱材料。此外,木材和金屬等輕質建築材料的日益普及也推動了聚氨酯塗料市場的發展。

- 用於生產 PU 塗料的原料(例如異氰酸酯和多元醇)的價格波動較大,波動較大。這會影響 PU 塗料製造商的盈利。

- 此外,PU塗層也用於塗覆植入、導管等醫療設備。它也用於提高醫療設備的生物相容性。

- 亞太地區佔據聚氨酯塗料消費量的主要佔有率。預計該地區將在預測期內實現最快的成長。

聚氨酯塗料市場發展趨勢

汽車產業主導市場

- 汽車工業是全球聚氨酯塗料最大的消費領域。汽車漆中使用的底漆大多採用陰極電塗裝工藝,近90%為陰極電塗裝漆。聚氨酯電泳漆在這個過程中發揮了極好的作用。

- PU漆用於OEM和重塗。環氧聚醯胺聚氨酯和丙烯酸聚氨酯塗料是該產業通常優選的塗料。

- 過去十年,汽車產業經歷了一段充滿希望的成長時期,但近年來這種勢頭有所放緩。

- 全球許多地區的新車銷售和生產都受到影響,包括歐洲、亞太地區和美國。在大多數國家,先前一直在成長的汽車生產受到了影響。然而,隨著全球情勢的改善,全球生產正在復甦。

- OICA資料顯示,2021年全球汽車銷量較2020年成長約5%。 2022年銷量為81,628,533輛,2021年為82,755,197輛,較2021年僅下降1.3%。

- 根據OICA預測,2022年全球汽車產量為8,501萬輛,與前一年同期比較成長6%,達8,014萬輛。

- 所有上述因素預計都會影響聚氨酯塗料在汽車應用中的使用。

中國在亞太市場佔主導地位

- 中國是PU材料的最大市場。這強大的消費群使其在全球PU塗料市場佔有重要地位。

- 根據中國工業協會(CAAM)2002年的報告,儘管中國乘用車銷量因COVID-19大流行而下降,但市場乘用車總銷量已恢復。 2022年銷量將超過2,350萬台,為過去四年來的最高數字。 PU 塗料有潛力推動 PU 塗料市場,因為它們用於保護汽車免受腐蝕和其他損壞。它也用於改善汽車的外觀。

- 根據中國國家統計局預測,2022年,中國建築業產值將超過31兆元(4.6兆美元),與前一年同期比較成長6%,產值達29.31兆元人民幣(4.36兆美元)。億美元)。與 10 年前相比,它也增加了近 100%,對 PU 塗料市場和建築行業保護建築物免受自然災害影響的技術趨勢產生了積極影響。它也用於提高建築物的能源效率。

- 近年來,隨著環保要求和意識的增強,我國水性PU塗料產業發展迅速,其成長速度遠超過整個PU材料產業。

- 據歐洲塗料公司稱,2023 年 10 月,研究人員展示了用於木器塗料應用的香草醛基紫外線固化聚氨酯分散體的合成。

- 中國的科思創最近在上海建成了聚氨酯分銷設施,以滿足亞太地區不斷成長的需求。

- 嚴格的環保監督為國內水性PU塗料的發展開闢了新的空間。

- 由於上述因素,預計在預測期內該地區對聚氨酯塗料的需求將會增加。

聚氨酯塗料產業概況

聚氨酯塗料市場具有綜合性。主要企業(排名不分先後)包括 Akzo Nobel NV、Jotun、Axalta Coating Systems、PPG Industries Inc. 和 The Sherwin-Williams Company。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 調查先決條件

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 促進因素

- 建築業的需求不斷增加

- 汽車產業需求增加

- 交通運輸業需求增加

- 抑制因素

- 原物料價格不穩定

- 其他限制因素

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章市場區隔(市場規模:金額)

- 科技

- 粉末

- 溶劑型

- 水系統

- 輻射固化

- 最終用戶產業

- 車

- 運輸

- 建築學

- 電力/電子

- 木材/家具

- 其他最終用戶產業

- 地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 義大利

- 法國

- 歐洲其他地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東/非洲

- 沙烏地阿拉伯

- 南非

- 其他中東/非洲

- 亞太地區

第6章 競爭狀況

- 併購、合資、聯盟、協議

- 市場佔有率(%)/排名分析

- 主要企業策略

- 公司簡介

- Akzo Nobel NV

- Asian Paints

- Axalta Coating Systems

- BASF SE

- IVM Chemicals SRL

- Jotun

- Polycoat Products

- PPG Industries Inc.

- RPM International Inc.

- The Sherwin-Williams Company

第7章 市場機會及未來趨勢

- PU塗料在航太和醫療產業的新應用

- 奈米技術與 PU 塗料融合的發展

The Polyurethane Coatings Market size is estimated at USD 21.15 billion in 2024, and is expected to reach USD 26.88 billion by 2029, growing at a CAGR of greater than 4% during the forecast period (2024-2029).

The market was negatively impacted due to COVID-19 in 2020. Owing to the pandemic scenario, several countries around the world went into lockdown. It halted all manufacturing and construction activities, thus creating a negative impact on the demand for polyurethane coatings. However, the condition recovered, thereby restoring the growth of the polyurethane coatings market.

Key Highlights

- The construction industry is driving the market's growth as PU coatings are used as exterior coatings, interior coatings, flooring, roofing, and insulation. Moreover, the increasing popularity of lightweight construction materials such as wood and metal is also driving the PU coatings market.

- The prices of raw materials used in the production of PU coatings, such as isocyanates and polyols, are volatile and can fluctuate significantly. It can impact the profitability of PU coatings manufacturers.

- In addition, PU coatings are being used to coat medical devices, such as implants and catheters. They are also being used to make medical devices more biocompatible.

- Asia-Pacific holds the major share in the consumption of polyurethane coatings. The region is also expected to witness the fastest growth during the forecast period.

Polyurethane Coatings Market Trends

Automotive Industry to Dominate the Market

- The automotive industry is the largest consumer of polyurethane coatings across the world. The majority of the primers used in automotive coatings utilize a cathodic electric deposit process, which constitutes almost 90% cathode electrophoretic paint. Polyurethane electrophoretic paint plays an excellent role in the process.

- PU coatings are used for both OEM and refinish applications. Epoxy polyamide polyurethane and acrylic polyurethane coats are the commonly preferred coatings in the industry.

- Despite an encouraging term of growth in the automotive sector during the past decade, the momentum slowed down in recent years.

- The sales and production of new vehicles were affected in various parts of the world, including Europe, Asia-Pacific, and the United States. It affected the previously growing automotive production in most nations. However, with the improving global scenario, production is recovering around the globe.

- According to the OICA data, global automotive sales increased by around 5% in 2021 compared to 2020. In 2022, there was only a 1.3% decline when compared to 2021, with sales of 8,16,28,533 and 8,27,55,197 in 2022 and 2021, respectively.

- As per OICA, the global production of automotive accounted for 85.01 million units in 2022, which is an increase of 6% compared to the previous year by 80.14 million units.

- All the factors above are expected to affect the usage of polyurethane coatings in automotive applications.

China to Dominate the Market in the Asia-Pacific Region

- China is the largest market for PU materials. This strong consumer base enables it to take a key position in the global PU coatings market.

- According to the China Association of Automobile Manufacturers (CAAM) 2002 report, despite the recent decline in passenger car sales in China during the COVID-19 pandemic, total passenger car sales in the market bounced back. In 2022, the sales exceeded 23.5 million units, making it the highest figure in the past four years. It includes the potential to drive the PU coating market as it is used to protect cars from corrosion and other damage. They are also being used to improve the appearance of cars.

- In 2022, as per the National Bureau of Statistics of China, the construction industry in China generated an output of over CNY 31 trillion (USD 4.6 trillion) with an increase of 6% from the previous year, accounting for CNY 29.31 trillion (USD 4.36 trillion). It also represented an increase of almost 100 % from a decade ago, with a positive impact on the PU coating market and the growing technological trends in the construction industry to protect buildings from the elements. They are also being used to improve the energy efficiency of buildings.

- Moreover, in recent years, due to the improvement of environmental protection requirements and awareness, China's water-borne PU coatings industry developed rapidly, with the growth rate far exceeding the overall PU materials industry.

- In October 2023, according to European Coatings, researchers demonstrated the synthesis of vanillin-based UV-curable polyurethane dispersions for wood coating applications.

- Covestro in China recently completed a polyurethane dispersion facility in Shanghai to meet rising demand in the Asia Pacific region.

- Strict environmental supervision opened up a new development space for water-borne PU coatings in the country.

- All the factors above, in turn, are projected to increase the demand for polyurethane coatings in the region during the forecast period.

Polyurethane Coatings Industry Overview

The polyurethane coatings market is consolidated in nature. The major players (not in any particular order) include Akzo Nobel NV, Jotun, Axalta Coating Systems, PPG Industries Inc., and The Sherwin-Williams Company, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Demand from the Construction Industry

- 4.1.2 Increase in Demand from the Automotive Industry

- 4.1.3 Growing Demand from the Transportation Industry

- 4.2 Restraints

- 4.2.1 Volatile Raw Material Prices

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Technology

- 5.1.1 Powder

- 5.1.2 Solvent-borne

- 5.1.3 Water-borne

- 5.1.4 Radiation Cured

- 5.2 End-user Industry

- 5.2.1 Automotive

- 5.2.2 Transportation

- 5.2.3 Construction

- 5.2.4 Electrical and Electronics

- 5.2.5 Wood and Furniture

- 5.2.6 Others End-user Industries (Aerospace, Industrial, and Textile)

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share(%)**/ Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Akzo Nobel NV

- 6.4.2 Asian Paints

- 6.4.3 Axalta Coating Systems

- 6.4.4 BASF SE

- 6.4.5 IVM Chemicals SRL

- 6.4.6 Jotun

- 6.4.7 Polycoat Products

- 6.4.8 PPG Industries Inc.

- 6.4.9 RPM International Inc.

- 6.4.10 The Sherwin-Williams Company

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 New applications for PU coatings in Aerospace and Medical Industries

- 7.2 Development in Integration of Nanotechnology and PU coatings

2026年全球軟觸感聚氨酯塗料市場報告

2026年全球軟觸感聚氨酯塗料市場報告 聚氨酯塗料市場規模、佔有率、成長及全球產業分析:依類型、應用和地區劃分的洞察與預測(2024-2032 年)

聚氨酯塗料市場規模、佔有率、成長及全球產業分析:依類型、應用和地區劃分的洞察與預測(2024-2032 年) 軟觸感聚氨酯塗料市場-全球產業規模、佔有率、趨勢、機會和預測,按產品類型、基材類型、最終用途、地區和競爭格局分類,2020-2030年預測

軟觸感聚氨酯塗料市場-全球產業規模、佔有率、趨勢、機會和預測,按產品類型、基材類型、最終用途、地區和競爭格局分類,2020-2030年預測 亞太地區的聚氨酯塗料市場(2025年)

亞太地區的聚氨酯塗料市場(2025年) 聚氨酯(PU)塗料市場需求、地區、應用分析及2034年預測報告EMEA的聚氨酯被覆劑市場:2025年聚氨酯塗料市場-全球產業規模、佔有率、趨勢、機會及預測(按基材、最終用戶、地區和競爭細分,2020-2030 年)

聚氨酯(PU)塗料市場需求、地區、應用分析及2034年預測報告EMEA的聚氨酯被覆劑市場:2025年聚氨酯塗料市場-全球產業規模、佔有率、趨勢、機會及預測(按基材、最終用戶、地區和競爭細分,2020-2030 年) 聚氨酯塗料市場規模、佔有率、趨勢分析報告(按技術、最終用途、地區、細分市場預測,2025-2030 年)

聚氨酯塗料市場規模、佔有率、趨勢分析報告(按技術、最終用途、地區、細分市場預測,2025-2030 年) 美洲聚氨酯塗料市場:2024年亞太地區聚氨酯塗料市場:2024年

美洲聚氨酯塗料市場:2024年亞太地區聚氨酯塗料市場:2024年