|

市場調查報告書

商品編碼

1519937

環戊烷:市場佔有率分析、產業趨勢/統計、成長預測(2024-2029)Cyclopentane - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

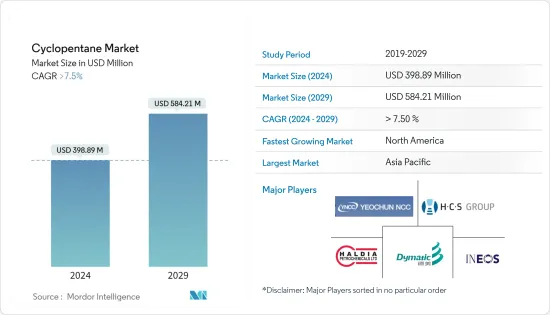

環戊烷市場規模預計將從2024年的3.9889億美元增至2029年的5.8421億美元,在預測期內(2024-2029年)複合年成長率超過7.5%。

COVID-19 大流行阻礙了環戊烷市場。由於多個國家的國家封鎖、嚴格的社交距離措施以及全球供應鏈網路的中斷,冷媒產業受到大多數生產工廠和產業關閉的嚴重影響。然而,限制解除後,市場卻出現了顯著的成長。由於環戊烷在冷凍、絕緣和化學溶劑等各種應用中的使用量不斷增加,市場出現了成長。

主要亮點

- 聚氨酯製造中發泡應用對環戊烷的需求不斷增加,以及冷凍應用中環戊烷的使用量不斷增加,預計將推動環戊烷市場的發展。

- 另一方面,更好的替代品的可用性和與環戊烷相關的健康相關問題預計將阻礙市場成長。

- 發泡在建築和汽車應用中的使用增加預計將在預測期內為市場創造機會。

- 由於冷凍、絕緣和化學溶劑應用對環戊烷的需求不斷增加,亞太地區預計將主導市場。

環戊烷市場趨勢

冷凍應用領域佔據市場主導地位

- 環戊烷是由環己烷在氧化鋁存在下在高溫高壓下分解而製得。環戊烷主要用作聚氨酯生產中的發泡,也用於冰箱、冷凍庫等的生產。

- 食品和飲料行業對冰箱的需求正在增加。在穩定溫度下保存食品的需求不斷成長,推動了食品和飲料行業對冰箱和冷凍庫的需求。

- 此外,在製藥業,醫院、藥房、診所和診斷中心對安全儲存血液、血液衍生材料和溫度敏感藥物的需求不斷成長,推動了醫療保健和製藥行業對冷凍的需求。

- 在歐洲地區,冰箱製造商使用環戊烷作為聚氨酯泡棉隔熱材料的發泡,而不是CFC(氟氯化碳)和HCFC(氟烴塑膠)。由於對 HCFC 化合物使用的嚴格規定,環戊烷在冷凍應用中的使用正在增加。

- 同樣,亞太地區、中東和非洲以及拉丁美洲地區的政府也推出了各種政策,逐步淘汰冷凍應用中 HCFC(氟烴塑膠)的使用。這些地區的人口成長以及住宅冷凍和建築應用需求的增加推動了對環戊烷的需求。

- 2022年,LG電子冰箱產量達到約977萬台。 LG 電子冰箱在韓國、印度、墨西哥和中國製造。 LG電子冰箱產量較去年同期下降15.19%。然而,預計冰箱產量在預測期內將進一步增加,從而推動環戊烷市場。

- 因此,冷凍應用領域將在預測期內主導市場。

亞太地區主導市場

- 預計亞太地區將在預測期內主導環戊烷市場。在中國和印度等國家,由於環戊烷在家用和商用冰箱中的使用量不斷增加,其需求量也不斷增加。

- 中國是氟烴塑膠(HFCs)最大的生產國和消費國。由於與 HCFC 相關的環境問題,預計將逐步淘汰 HCFC。這似乎為包括環戊烷在內的非氟氯烴發泡提供了充足的機會。

- 根據中國國家統計局統計,中國家用冰箱產量為8,664萬台。這與上年度8992萬台的產量相比略有下降。然而,隨著中國都市化的快速發展,產量預計將會增加,從而推動當前的研究市場。

- 同樣,在日本,家用冰箱產量正從上年度的126萬台增加到2022年的128萬台,成長率為1.59%。因此,冰箱產量的增加將帶動國內環戊烷市場。

- 此外,隨著化學市場的擴大,對環戊烷作為化學溶劑的需求也不斷增加。例如,印度化工產業多年來投資穩健,2000 年 4 月至 2022 年 12 月期間外國直接投資流入量達 209.6 億美元。此外,政府在2023-24年聯邦預算中向化學和石化部撥款2,093萬美元,以促進國內化學品製造。

- 總體而言,冰箱和化學工業對環戊烷的需求不斷增加可能會在預測期內推動該地區的市場。

環戊烷產業概況

環戊烷市場得到鞏固。市場主要企業(排名不分先後)包括 Dymatic Chemicals, Inc、Haldia Petrochemicals Limited、HCS Group GmbH、INEOS 和 YEOCHUN NCC。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章 簡介

- 調查先決條件

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 促進因素

- 作為生產聚氨酯發泡的需求不斷增加

- 冷凍應用需求增加

- 其他司機

- 抑制因素

- 更好的替代方案的可用性

- 與環戊烷相關的健康問題

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 買方議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章市場區隔:市場規模(以金額為準)

- 功能

- 發泡/冷媒

- 溶劑/試劑

- 其他特性(橡膠黏劑、樹脂等)

- 目的

- 冷凍的

- 隔熱材料

- 化學溶劑

- 其他用途(個人護理、燃料添加劑等)

- 地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 義大利

- 法國

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東/非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲

- 亞太地區

第6章 競爭狀況

- 併購、合資、聯盟、協議

- 市場佔有率(%)**/排名分析

- 主要企業策略

- 公司簡介

- Dymatic Chemicals, Inc

- Haldia Petrochemicals Limited

- HCS Group GmbH

- INEOS

- Liaoning Yufeng Chemical Co., Ltd.

- Meilong Cyclopentane Chemical Co.,Ltd.

- Merck KGaA

- PURECHEM.CO.KR

- SINTECO SRL

- TRECORA RESOURCES

- YEOCHUN NCC CO., LTD

第7章 市場機會及未來趨勢

- 發泡在建築和汽車應用的使用增加

- 其他機會

The Cyclopentane Market size is estimated at USD 398.89 million in 2024, and is expected to reach USD 584.21 million by 2029, growing at a CAGR of greater than 7.5% during the forecast period (2024-2029).

The COVID-19 pandemic hampered the cyclopentane market. Due to nationwide lockdowns in several countries, strict social distancing measures, and disruption in global supply chain networks, the refrigerant industry was severely hit as most of the production plants and industries were shut down. However, the market registered a significant growth rate well after the restrictions were lifted. The market registered a growth rate due to the rising usage of cyclopentane in various applications, such as refrigeration, insulation, and chemical solvents.

Key Highlights

- The growing demand for cyclopentane in blowing agent applications to manufacturing polyurethane and the increasing usage in refrigeration applications are expected to drive the market for cyclopentane.

- On the flip side, the availability of better substitute products and health-related issues associated with cyclopentane is expected to hinder the growth of the market.

- The increasing use of blowing agents in construction and automotive applications is expected to create opportunities for the market during the forecast period.

- The Asia-Pacific region is expected to dominate the market owing to the rising demand for cyclopentane from refrigeration, insulation, and chemical solvent applications.

Cyclopentane Market Trends

Refrigeration Application Segment to Dominate the Market

- The cyclopentane is formed by cracking cyclohexane in the presence of alumina at high pressure and temperature. Cyclopentane is majorly used as a foam-blowing agent in the production of polyurethane, which is further used in the manufacture of refrigerators, freezers, etc.

- The demand for refrigerators is increasing in the food and beverage sectors. The rising demand for storing food products at stable temperatures is fueling the demand for refrigerators and freezers in the food and beverage sector.

- Furthermore, in the pharmaceutical sector, the increase in the demand for safe storage of blood and blood derivatives and temperature-sensitive medicines from hospitals, pharmacies, clinics, and diagnostic centers is also propelling the demand for refrigeration in the healthcare and pharmaceutical industry.

- In the European region, refrigerator manufacturers are using cyclopentane as a blowing agent in polyurethane foam insulation in place of CFC (Chlorofluorocarbon) and HCFC (hydrochlorofluorocarbon). Due to the stringent regulations on the usage of HCFC compounds, the usage of cyclopentane is increasing in refrigeration applications.

- Similarly, in Asia Pacific, Middle-East and Africa, and Latin America regions, the governments introduced various policies to phase out the usage of HCFC (hydrochlorofluorocarbon) in refrigerator applications. The demand for cyclopentane is being driven by a growth in population and an increase in demand for residential refrigerators and building applications in these regions.

- In 2022, the production volume of refrigerators by LG Electronics amounted to around 9.77 million. LG Electronics' refrigerators were manufactured in South Korea, India, Mexico and China. The production volume of refrigerators by LG Electronics decreased by 15.19% as compared to the previous year. However, the production volume of refrigerators is further expected to increase over the forecast period, thereby driving the market for cyclopentane.

- Thus, the refrigeration application segment will dominate the market during the forecast period.

Asia-Pacific Region to Dominate the Market

- Asia-Pacific region is expected to dominate the market for cyclopentane during the forecast period. In countries like China and India, owing to increasing use in residential and commercial refrigerators, the demand for cyclopentane is increasing in the region.

- China is the largest producer & consumer of hydrochlorofluorocarbons (HFCs). It is expected to phase out HCFCs due to the environmental concerns associated with them. It will create ample opportunities for the non-HCFC foaming agents, including cyclopentane.

- According to the National Bureau of Statistics of China, the production volume of household refrigerators in China is registered at 86.64 million units. It is slightly declined as compared to 89.92 million units manufactured in the previous year. However, the production volume is expected to increase with the rapid urbanization across China, thereby driving the current studied market.

- Similarly, in Japan, the production volume of residential refrigerators increased at a growth rate of 1.59% to 1.28 million units in 2022, as compared to 1.26 million units manufactured in the previous year. Thus, the increasing production volume of refrigerators will drive the market for cyclopentane in the country.

- Furthermore, the demand for cyclopentane as a chemical solvent is increasing in the region, with an increasing chemical market. For instance, the Indian chemical sector witnessed healthy investments over the years, as evidenced by the FDI inflows that reached USD 20.96 billion between April 2000 and December 2022. Further, the government allocated USD 20.93 million to the Department of Chemicals and Petrochemicals under the Union Budget 2023-24, thereby boosting chemical manufacturing in the country.

- Overall, the increasing demand for cyclopentane from refrigerators and chemical industries is likely to drive the market in the region during the forecast period.

Cyclopentane Industry Overview

The Cyclopentane market is consolidated. Some of the major players (not in any particular order) in the market include Dymatic Chemicals, Inc., Haldia Petrochemicals Limited, HCS Group GmbH, INEOS, and YEOCHUN NCC CO., LTD, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Demand in Blowing Agent Application to Manufacture Polyurethane

- 4.1.2 Increasing Demand in Refrigeration Application

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Availability of Better Substitute Products

- 4.2.2 Health Related Issues Associated with Cyclopentane

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Function

- 5.1.1 Blowing Agent & Refrigerant

- 5.1.2 Solvent & Reagent

- 5.1.3 Other Functions (Rubber Adhesives, Resins, etc.)

- 5.2 Application

- 5.2.1 Refrigeration

- 5.2.2 Insulation

- 5.2.3 Chemical Solvent

- 5.2.4 Other Applications (Personal Care, Fuel Additives, etc.)

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Dymatic Chemicals, Inc

- 6.4.2 Haldia Petrochemicals Limited

- 6.4.3 HCS Group GmbH

- 6.4.4 INEOS

- 6.4.5 Liaoning Yufeng Chemical Co., Ltd.

- 6.4.6 Meilong Cyclopentane Chemical Co.,Ltd.

- 6.4.7 Merck KGaA

- 6.4.8 PURECHEM.CO.KR

- 6.4.9 SINTECO S.R.L

- 6.4.10 TRECORA RESOURCES

- 6.4.11 YEOCHUN NCC CO., LTD

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Use of Blowing Agents in Construction and Automotive Applications

- 7.2 Other Opportunities

環戊烷市場規模、佔有率和成長分析(按功能、應用和地區)- 產業預測 2025-2032

環戊烷市場規模、佔有率和成長分析(按功能、應用和地區)- 產業預測 2025-2032 環戊烷的全球市場(2018年~2034年)

環戊烷的全球市場(2018年~2034年) 環戊烷市場:按功能和應用分類 - 2025-2030 年全球預測

環戊烷市場:按功能和應用分類 - 2025-2030 年全球預測 環戊烷市場:現況分析與預測(2024-2032)

環戊烷市場:現況分析與預測(2024-2032) 全球環戊烷市場:按功能、應用、地區分類 - 2028 年預測

全球環戊烷市場:按功能、應用、地區分類 - 2028 年預測 環戊烷市場 - 按類型(溶劑和試劑、泡沫發泡劑)、按等級、按應用(商用冰箱、家用冰箱、保溫容器、電氣和電子產品、燃料添加劑)和預測,2024 年 - 2032 年

環戊烷市場 - 按類型(溶劑和試劑、泡沫發泡劑)、按等級、按應用(商用冰箱、家用冰箱、保溫容器、電氣和電子產品、燃料添加劑)和預測,2024 年 - 2032 年 環戊烷(CAS 287-92-3的)全球市場:實際成果與預測(2018年~2029年)世界環戊烷市場

環戊烷(CAS 287-92-3的)全球市場:實際成果與預測(2018年~2029年)世界環戊烷市場