|

市場調查報告書

商品編碼

1519947

液體屋頂塗料:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029)Liquid Roofing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

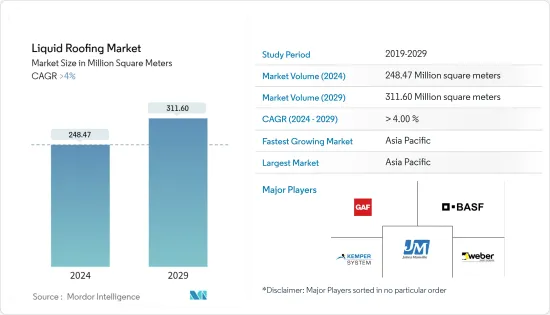

液體屋頂塗料市場規模預計在2024年達到2.4847億平方米,2029年達到3.116億平方米,在預測期(2024-2029年)複合年成長率將超過4%。

COVID-19的第一個影響是2020年液體屋頂市場需求疲軟。不過,2021年和2022年市場出現復甦跡象,長期前景看好。

消費者對延長使用壽命、降低溫度和易於維護等優點的認知不斷提高,正在推動液體屋頂市場的住宅需求。

然而,原料成本的波動可能會在不久的將來阻礙液體屋頂市場的成長。

由於全球減少碳排放的需求日益成長,未來五年可能會為液體屋頂市場提供者機。

由於中國、印度等國家液體屋頂消費量的增加,亞太地區主導了液體屋頂市場。

液體屋頂市場趨勢

住宅產業主導市場

- 由於建築業液體屋頂的大量消耗,住宅領域佔據了市場主導地位。

- 液體屋頂具有更長的使用壽命、更低的維護成本以及透過降低生命週期成本來增加價值等優點。消費者對液體屋頂的認知和接受程度的提高預計將推動市場成長。

- 矽膠塗料用於結構和建築物的屋頂,因為它們比其他液體薄膜具有優勢,例如耐候性、防紫外線、耐揮發性有機化合物和耐用性,這使得它們對建築商來說價格昂貴。替代屋頂更換項目。

- 舊建築的維修和重建預計將增加建設產業的投資,並有助於未來幾年市場需求的增加。

- 中國、印度和韓國等亞太國家的建築和裝修活動成長強勁,預計該地區在預測期內對液體屋頂市場的需求將增加。

- 主要經濟體向都市區快速遷移、政府在房地產市場上住宅建設支出增加以及豪華住宅需求上升等因素預計將有利於建設產業的成長。

- 2022年,中國建築業產值達到高峰約31.2兆元。

- 在北美,美國在建設產業中佔有很大佔有率。在美國以外,加拿大和墨西哥是建築業投資的主要貢獻者。

- 2022年美國住宅年金額為9,080億美元,比2021年的8,030億美元成長13%。

- 在加拿大,各種政府計劃,如經濟適用房舉措(AHI)、加拿大新建築計劃 (NBCP) 和加拿大製造,將大力支持該行業的擴張。 2022年8月,加拿大政府宣布將在三項關鍵舉措上投資超過20億美元。這三項舉措將總合支持全國約 17,000 套家庭住宅的開發,其中包括數千套經濟適用住宅。

- 根據美國建築師協會 (AIA) 共識建築預測,預計 2022 年建築物建築支出將成長 9%,2023 年將再成長 6%。這前景比我們 2022 年初的預測稍微樂觀一點。這主要是由於製造業的強勁成長和零售業的強勁成長。

- 由於歐盟復甦基金的新投資,歐洲建築業在 2022 年成長了 2.5%。儘管大多數歐盟建設公司面臨價格壓力,但景氣預計將在 2022 年初恢復並達到 COVID-19 之前的水平。此外,隨著 COVID-19 危機的緩解以及建築商越來越不願意投資新建築或維修現有房產,非住宅建築預計將加快步伐並支持整體建築市場的成長。

亞太地區主導市場

- 根據牛津經濟研究院預測,2020 年至 2030 年全球建設產業預計將成長 4.5 兆美元(42%)。此外,2020年至2030年,中國、印度、美國和印尼預計將佔全球建築成長的58.3%。

- 住宅和商業建築領域的擴張等因素預計將推動該地區的市場成長。

- 液體屋頂系統非常耐用,維護成本低,證明比其他防水系統更耐用,使用壽命更長。

- 越來越多的促進基礎設施發展的政府計劃,如越南的社會經濟發展計劃、印尼的國家中期發展計劃和菲律賓的發展計劃,預計將成為市場開拓的驅動力。

- 對節能結構的需求不斷成長,人們對液體屋頂成本效益的認知不斷提高,以及全球建設活動的活性化,可能會在預測期內進一步加速液體屋頂市場的發展。

- 2022 年第四季度,印度建築業估值超過 3 兆印度盧比。與 2020 年相比,這一數字顯著增加,2020 年金額因 COVID-19 大流行而減少。當時,該國的建設業和製造業是受災最嚴重的產業之一。然而,該行業似乎已迅速復甦,並再次恢復到危機前的水平。

- 中國的建設產業是世界上最大的建築業之一,近幾十年來經歷了顯著的成長。中國正在經歷快速的都市化和工業化,住宅、商業和基礎設施建設等建設活動不斷增加。然而,最近的事態發展表明,建設產業不斷受到房地產開發人員去槓桿化努力的壓力,推動更永續的建築實踐。

- 截至2022年5月,中國已開發實施基礎建設計劃價值超過2,500萬美元,總規模超過5兆美元。美國和印度緊隨其後,價值約 2 兆美元的基礎設施計劃上榜。另一方面,印度的大型基礎設施計劃數量最多。

- 因此,預計此類市場趨勢將在預測期內推動該地區液體屋頂市場的需求。

液體屋頂產業概述

液體屋頂市場部分分散。主要參與者(排名不分先後)包括 Kemper System Ltd、Johns Manville(波克夏海瑟威)、GAF、Saint-Gobain Weber 和BASF SE。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第1章 簡介

- 調查先決條件

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 促進因素

- 不斷成長的住宅市場

- 消費者對液體屋頂塗料的認知不斷增強

- 其他司機

- 抑制因素

- COVID-19 疫情造成的不利情況

- 其他阻礙因素

- 價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 買方議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章市場區隔:市場規模(基於數量)

- 種類

- 聚氨酯漆

- 丙烯酸塗料

- 瀝青塗層

- 矽膠漆

- 環氧塗層

- 其他類型(改質矽烷聚合物、三元乙丙橡膠、合成橡膠體膜、水泥膜、環氧塗料)

- 目的

- 圓頂屋頂

- 斜屋頂

- 屋頂平台

- 最終用戶產業

- 住宅

- 商業的

- 工業/設施

- 基礎設施

- 地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 馬來西亞

- 泰國

- 印尼

- 越南

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 北歐的

- 土耳其

- 俄羅斯

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 哥倫比亞

- 南美洲其他地區

- 中東/非洲

- 沙烏地阿拉伯

- 南非

- 奈及利亞

- 卡達

- 埃及

- 阿拉伯聯合大公國

- 其他中東和非洲

- 亞太地區

第6章 競爭狀況

- 併購、合資、聯盟、協議

- 市場佔有率(%)/排名分析

- 主要企業策略

- 公司簡介

- Akzo Nobel NV

- Alumasc Building Products

- BASF SE

- BMI UK & Ireland

- GAF

- GreenShield

- Johns Manville(A Berkshire Hathaway Company)

- Kemper System Ltd

- Laydex

- Liquid Roofing Systems LTD

- Saint-Gobain Weber

- SIG Design and Technology(Part of SIG PLC)

- Sika AG

- Langley

第7章 市場機會及未來趨勢

- 減少碳足跡的需求日益成長

- 其他機會

The Liquid Roofing Market size is estimated at 248.47 Million square meters in 2024, and is expected to reach 311.60 Million square meters by 2029, growing at a CAGR of greater than 4% during the forecast period (2024-2029).

The initial impact of COVID-19 was a demand slump in the liquid roofing market in 2020. However, the market showed signs of recovery in 2021 and 2022, and the long-term outlook appears positive.

Increasing consumer awareness of benefits such as lifespan extension, temperature reduction, and ease of maintenance is driving the residential demand for the liquid roofing market.

However, the volatility in the cost of the raw material may hinder the growth of the liquid roofing market in the near future.

The growing need to reduce carbon footprints across the globe is likely to provide opportunities for the liquid roofing market over the next five years.

The Asia-Pacific region dominates the liquid roofing market, owing to the increasing consumption of liquid roofing from countries like China, India, etc.

Liquid Roofing Market Trends

Residential Segment to Dominate the Market

- The residential sector stands to be the dominating segment owing to the large-scale consumption of liquid roofing in the construction industry.

- Beneficial attributes like long-term roofs, lower maintenance costs, and more value as life cycle costs decrease with liquid roofing. Increasing awareness and acceptability among consumers regarding liquid roofing is expected to drive market growth.

- Among types, the silicone coating is utilized in structures and building roofs due to its advantages over other fluid membranes, such as weathering resistance, UV protection, volatile organic compound tolerance, and durability, and provides construction owners with an alternative to an expensive re-roofing project.

- Refurbishing and renovation of old buildings have increased investments in the building and construction industry and are anticipated to contribute to a rise in market demand in the upcoming years.

- Asia-Pacific countries like China, India, and South Korea have been registering strong growth in construction and remodeling activities, and the requirement for a liquid roofing market is projected to increase in this region in the forecast period.

- Factors such as rapid urban migration in major economies, increased government spending in the real estate market for residential construction, and the growing demand for high-class residential homes are likely to benefit the growth of the construction industry.

- In 2022, the construction output value in China achieved its peak at around CNY 31.2 trillion.

- In North America, the United States has a major share in the construction industry. Besides the United States, Canada and Mexico contribute significantly to the construction sector investments.

- The annual value of residential construction in the United States was valued at USD 908 billion in 2022, an increase of 13% compared to USD 803 billion in 2021.

- In Canada, various government projects, including the Affordable Housing Initiative (AHI), New Building Canada Plan (NBCP), and Made in Canada, are set to hugely support the sector's expansion. In August 2022, the Canadian government announced a significant investment of more than USD 2 billion to fund three important initiatives that will collectively help to develop approximately 17,000 houses for families across the nation, including thousands of affordable housing units.

- In 2022, according to the American Institute of Architects (AIA) Consensus Construction Forecast, construction spending on buildings grew by an estimated 9% in 2022, and it is anticipated to grow by an additional 6% in 2023. This outlook is slightly more optimistic than forecasted at the beginning of 2022. This was largely due to strong growth in the manufacturing sector and growing strength in retail facilities.

- Europe's construction sector grew by 2.5% in 2022, owing to new investments from the European Union Recovery Fund. Business confidence picked up in early 2022 and is expected to reach pre-COVID-19 levels despite price pressures at most EU construction firms. Moreover, as the COVID-19 crisis abates and builders become less reluctant to invest in new corporate buildings and renovate existing properties, non-residential construction is expected to pick up the pace, thus supporting overall growth in the construction market.

Asia-Pacific Region to Dominate the Market

- According to Oxford Economics, the global construction industry is expected to grow by USD 4.5 trillion, or 42%, between 2020 and 2030. Additionally, China, India, the United States, and Indonesia are expected to account for 58.3% of global growth in construction between 2020 and 2030.

- Factors such as expansion in the residential and commercial construction sector will drive the market growth in the region.

- Liquid roofing systems are highly tenable, lower maintenance costs, are proven to be more durable than other waterproofing systems, are long-lasting, and aid in the prevention of uneven spots, bumps, any overlaps over the roof surface, etc.

- Rising government plans for advancing infrastructures, such as Vietnam's Socio-Economic Development Plan, Indonesia's National Medium-Term Development Plan, Philippine Development Plan, and other country's plans are expected to drive market growth.

- Emerging demand for energy-efficient structures, expanding awareness about the cost-effectiveness of liquid roofing, and increasing construction activities worldwide will further accelerate the liquid roofing market in the forecast period.

- India's construction industry was valued at over three trillion Indian rupees in the fourth quarter of 2022. This was a significant increase compared to 2020 when the value shrank due to the COVID-19 pandemic. The country's construction and manufacturing industries were among the worst hit at the time. However, the industry seemed to recover quickly and returned to pre-crisis level again.

- China's construction industry, one of the world's largest, has experienced significant growth in recent decades. China is undergoing rapid urbanization and industrialization, increasing construction activities such as residential, commercial, and infrastructure construction. In recent years, however, the construction industry has been under constant pressure from property developers' deleveraging measures, leading to more sustainable construction practices.

- In China, the infrastructure projects in development or execution of over USD 25 million as of May 2022 were worth over USD 5 trillion. The United States and India were the following countries on the list, with around USD 2 trillion worth of infrastructure projects. In contrast, the country with the highest number of big infrastructure projects was India.

- Hence, all such market trends are expected to drive the demand for liquid roofing market in the region during the forecast period.

Liquid Roofing Industry Overview

The Liquid Roofing Market is partially fragmented in nature. The major players (not in any particular order) include Kemper System Ltd, Johns Manville (Berkshire Hathaway Company), GAF, Saint-Gobain Weber, and BASF SE.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Residential Segment

- 4.1.2 Increasing Consumer Awareness for Liquid Roofing

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Unfavorable Conditions Arising Due to COVID-19 Outbreak

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Type

- 5.1.1 Polyurethane Coatings

- 5.1.2 Acrylic Coatings

- 5.1.3 Bituminous Coatings

- 5.1.4 Silicone Coatings

- 5.1.5 Epoxy Coatings

- 5.1.6 Other Types (Modified Silane Polymers, EPDM Rubbers, Elastomeric Membranes, Cementitious Membranes, and Epoxy Coatings)

- 5.2 Application

- 5.2.1 Domed Roofs

- 5.2.2 Pitched Roof

- 5.2.3 Flat Roofed

- 5.3 End-user Industry

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.3.3 Industrial/Institutional

- 5.3.4 Infrastructure

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Malaysia

- 5.4.1.6 Thailand

- 5.4.1.7 Indonesia

- 5.4.1.8 Vietnam

- 5.4.1.9 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 NORDIC

- 5.4.3.7 Turkey

- 5.4.3.8 Russia

- 5.4.3.9 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Nigeria

- 5.4.5.4 Qatar

- 5.4.5.5 Egypt

- 5.4.5.6 UAE

- 5.4.5.7 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)/Ranking Analysis**

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Akzo Nobel NV

- 6.4.2 Alumasc Building Products

- 6.4.3 BASF SE

- 6.4.4 BMI UK & Ireland

- 6.4.5 GAF

- 6.4.6 GreenShield

- 6.4.7 Johns Manville (A Berkshire Hathaway Company)

- 6.4.8 Kemper System Ltd

- 6.4.9 Laydex

- 6.4.10 Liquid Roofing Systems LTD

- 6.4.11 Saint-Gobain Weber

- 6.4.12 SIG Design and Technology (Part of SIG PLC)

- 6.4.13 Sika AG

- 6.4.14 Langley

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing Need to Reduce Carbon Footprints

- 7.2 Other Opportunities