|

市場調查報告書

商品編碼

1519948

Chrome:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029)Chromium - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

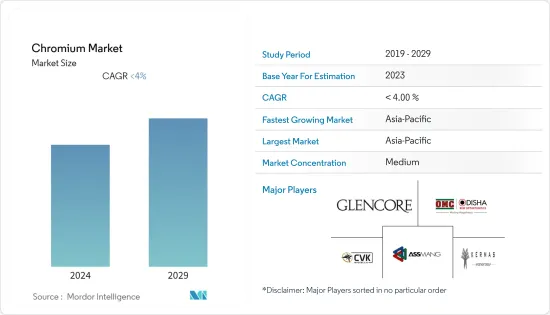

鉻市場規模預計到2024年將達到43.19千噸,到2029年將達到52.33千噸,在預測期內(2024-2029年)複合年成長率為3.91%。

由於全球對汽車、建築和施工行業的限制,COVID-19 大流行對鉻市場產生了重大影響。然而,從 2021 年開始,該行業正在成長,預計市場在預測期內將以相同的速度成長。

主要亮點

- 從中期來看,冶金應用需求的增加和工業中耐火材料使用的增加預計將推動市場成長。

- 然而,接觸鉻會導致健康和環境影響,預計這將阻礙市場成長。

- 未來幾年,三價鉻硬鉻電鍍製程的市場開拓預計將帶動市場成長。

- 亞太地區在過去幾年中一直引領市場,預計在預測期內仍將保持最高的複合年成長率。

鉻合金市場趨勢

冶金應用預計未來將成長

- 鉻在冶金過程中用於提高淬透性、衝擊強度、耐腐蝕性、對其他金屬的抗氧化性和許多其他性能,並用於重型機械、建築領域和其他應用。

- 根據美國地質調查局的數據,2023 年全球礦場生產了約 4,100 萬噸鉻。南非佔大部分佔有率(1,800萬噸),約佔總產量的45%。

- 鉻在不銹鋼的生產中發揮重要作用,因為即使加熱到非常高的溫度,它也不會硬化並保持耐腐蝕性。同樣,鉻用於提高鋁的強度和耐用性,幫助其即使在高溫下也能保持其形狀。

- 根據世界鋼鐵協會統計,2023年全球粗鋼產量達18.497億噸,較2022年的18.315億噸成長約1%。預計在預測期內將進一步增加。

- 從全球來看,亞太地區的鋼鐵產量最多,特別是中國、日本和印度。此外,預計中國仍將是最大的鋼鐵消費國。由於消費復甦,預計該國粗鋼產量在預測期內將增加。

- 2023年北美地區粗鋼產量為1.096億噸,較2022年增加5.3%。 2022年美國產量為8,070萬噸,較2022年成長7.6%。

- 冶金過程涉及將鉻與民用和軍用飛機引擎中的其他金屬混合,例如用於運輸酸、肥料和其他吸水材料的不銹鋼罐車和散裝料斗拖車,可以製造重要零件。

- 在汽車工業中,鉻主要用於汽車零件外部和內部的電鍍和化學處理。根據國際汽車工業協會(OICA)的數據,2022年全球汽車產量約8,501萬輛,較2021年的8,020萬輛成長5.99%。

- 在北美,根據OICA的數據,2022年汽車產量為14,798,146輛,比2021年的13,467,065輛成長9.88%。此外,在北美,2022 年電動車銷量為 1,108,000 輛,而 2021 年為 748,000 輛。

- 因此,汽車產量的增加和鋼鐵製造業的需求預計將推動鉻市場的需求。

亞太地區主導市場

- 亞太地區有可能成為全球最大的市場。這是因為中國、印度等地區製造業高度發達,冶金業需求不斷增加。

- 亞太地區在不銹鋼生產中使用的鉻比其他地區都多。這是由於不銹鋼在全球所有製造業中的重要性日益增加。

- 根據世界鋼鐵協會統計,2023年亞洲粗鋼產量為13.672億噸,較2022年成長0.7%。

- 2023年中國粗鋼產量達10.191億噸,較2022年成長約0.6%。 2023年印度粗鋼產量達1.402億噸,較2022年增加11.8%。

- 鉻在汽車工業中也很重要。由於中國是汽車產量最多的國家,因此該國的鉻市場預計將以非常快的速度成長。

- 亞太地區的生產和銷售主要由中國、印度和日本等國家主導,這些國家擁有大型汽車製造商和大量生產基地。

- 根據中國工業協會預測,2022年汽車產量將達到2,700萬輛,使中國成為全球最重要的汽車生產基地,較2021年成長3.4%。

- 在中國,重點是擴大電動車的生產和銷售。為此,該公司設定了2025年每年生產700萬輛電動車的目標。目標是到2025年中國新車產量的20%是電動車。

- 印度已成為該地區第二大汽車製造商。根據印度汽車工業協會(SIAM)統計,2022-2023年印度生產的汽車數量較2021-2022年增加約12.55%,達到2,593,187,867輛。

- 根據日本工業協會(JAMA)統計,2023會計年度日本國內汽車產量成長14.84%,達8,998,538輛。

- 化學工業在亞太地區正在迅速擴張。鉻在氧化過程、乙烯聚合以及聚乙烯和1-Hexene工業中使用的寡聚物催化劑中用作催化劑,這些品質預計將在未來幾年推動鉻市場的發展。

- 因此,預計上述因素將在未來幾年對市場產生重大影響。

鉻產業概覽

鉻市場本質上是部分整合的,少數大公司控制很大一部分市場。一些主要公司包括(排名不分先後)Kermas Investment Group、Assmang Proprietary Limited、CVK Madencilik、Odisha Mining Corporation Ltd 和 Glencore。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第1章 簡介

- 調查先決條件

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 促進因素

- 冶金應用需求不斷成長

- 工業中耐火材料的使用不斷增加

- 其他司機

- 抑制因素

- 健康影響

- 其他阻礙因素

- 產業價值鏈分析

- 波特五力分析

- 買方議價能力

- 供應商的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章市場區隔(市場規模:基於數量)

- 按用途

- 化學

- 冶金

- 耐火材料

- 其他用途(玻璃拋光、工業催化劑、顏料)

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 馬來西亞

- 泰國

- 印尼

- 越南

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 義大利

- 法國

- 西班牙

- 北歐的

- 土耳其

- 俄羅斯

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 哥倫比亞

- 南美洲其他地區

- 中東/非洲

- 沙烏地阿拉伯

- 南非

- 奈及利亞

- 卡達

- 埃及

- 阿拉伯聯合大公國

- 其他中東和非洲

- 亞太地區

第6章 競爭狀況

- 併購、合資、聯盟、協議

- 市場佔有率(%)**/市場排名分析

- 主要企業策略

- 公司簡介

- Al Tamman Indsil FerroChrome LLC

- Assmang Proprietary Limited

- CVK Madencilik

- Glencore

- Hernic Ferrochrome(Pty)Ltd(Hernic)

- International Ferro Metals(IFM)

- Kermas Investment Group

- MVC Holdings LLC

- Odisha Mining Corporation Ltd

- Tenaris

- YILDIRIM Group of Companies

第7章 市場機會及未來趨勢

- 三價鉻硬鉻鍍層的研發

- 其他機會

The Chromium Market size is estimated at 43.19 kilotons in 2024, and is expected to reach 52.33 kilotons by 2029, growing at a CAGR of 3.91% during the forecast period (2024-2029).

The COVID-19 pandemic had a big effect on the chromium market because of the global restrictions on the auto, building, and construction industries. However, since 2021, industries have grown, and the market is expected to do the same during the forecast period.

Key Highlights

- Over the medium term, the growing demand for metallurgical uses and increasing refractory applications in industries are expected to drive market growth.

- However, exposure to chromium can cause health and environmental effects, which are expected to hinder market growth.

- In the coming years, the development of the trivalent chromium hard chrome plating process is likely to lead to market growth.

- Asia-Pacific has led the market for the past few years, and it is also expected to register the highest CAGR during the forecast period.

Chromium Market Trends

Metallurgical Applications to Witness Growth in Future

- Chromium is being utilized in metallurgical processes to improve its hardenability, impact strengths, resistance to corrosion, oxidation to other metals, and many other properties for use in heavy machinery, the construction sector, and other applications.

- According to the US Geological Survey, roughly 41 million metric tons of chromium were produced globally from mines in 2023. With around 45% of the total production, South Africa accounted for the majority share (18 million metric tons).

- It is an important part of making stainless steel because, even when heated to very high temperatures, it keeps its hardening and corrosion-resistant properties. In the same way, chromium is used to make aluminum stronger and more durable and to keep its shape when heated at high temperatures.

- According to the World Steel Association, global crude steel production in 2023 reached 1,849.7 million tons, registering a growth of about 1% compared to 1,831.5 million tons in 2022. It is further expected to increase during the forecast period.

- The most significant quantity of steel globally is produced in Asia-Pacific, particularly in countries like China, Japan, and India. China is also projected to remain the largest consumer of iron and steel. The country's production of crude steel is likely to increase during the forecast period, owing to the recovery in consumption.

- Crude steel production in North America was 109.6 million tons in 2023, increasing by 5.3% compared to 2022. The United States produced 80.7 million tons in 2022, increasing by 7.6% from 2022.

- In metallurgical processes, mixing chromium with other metals can help make important parts for commercial and military aircraft engines, such as stainless steel tankers, acids, and bulk hopper trailers used to move fertilizers and other materials that absorb water.

- In the auto industry, chromium is mostly used for electroplating and conversion coatings on the outside and inside of car parts. According to the International Organization of Motor Vehicle Manufacturers (OICA), in 2022, around 85.01 million vehicles were produced across the globe, witnessing a growth rate of 5.99% compared to 80.20 million vehicles in 2021.

- In North America, according to the OICA, automotive production in 2022 accounted for 14,798,146 units, an increase of 9.88% compared to that in 2021, which was reportedly 13,467,065 units. Additionally, in North America, the sales of electric vehicles in 2022 accounted for 1,108 thousand units, compared to 748 thousand unit sales in 2021.

- Therefore, a rise in the number of vehicles manufactured, along with demand in the steel manufacturing industry, is expected to fuel the market demand for chromium.

Asia-Pacific Region to Dominate the Market

- Asia-Pacific is likely to be the biggest market in the world. This is because China, India, and other parts of the region have very well-developed manufacturing sectors, and the metallurgical industry is increasing its demand.

- Asia-Pacific uses more chromium to make stainless steel than any other region. This is because stainless steel is becoming more important in every manufacturing sector around the world.

- According to the World Steel Association, Asia produced 1,367.2 million tons of crude steel in 2023, an increase of 0.7% compared to 2022.

- China's crude steel production in 2023 reached 1,019.1 million tons, an increase of about 0.6% compared to 2022. India's crude steel production in 2023 reached 140.2 million tons, which increased by 11.8% compared to 2022.

- Chromium is also important in the auto industry. Since China makes the most cars, the market for chromium in that country is expected to grow at a very fast rate.

- The production and sales in Asia-Pacific are primarily dominated by countries like China, India, and Japan, which consist of large automotive manufacturers and a vast number of production bases within the countries.

- According to the China Association of Automobile Manufacturers (CAAM), with a total vehicle production of 27 million units in 2022, China has the most significant automotive production base in the world, registering an increase of 3.4 % compared to 2021.

- In China, the main focus is to increase production and sales of electric vehicles. To this end, the country has set a target to produce 7 million electric vehicles per year by 2025. By 2025, the goal is to bring electric vehicles into 20 % of total new vehicle production in China.

- India has become the second-largest automotive vehicle manufacturer in the region. According to the Society of Indian Automobile Manufacturers (SIAM), during FY 2022-2023, the total number of automobiles manufactured in the country grew by about 12.55% compared to FY 2021-2022 and reached 2,59,31,867 units.

- According to the Japan Automobile Manufacturers Association (JAMA), motor vehicle production in the country in 2023 grew by 14.84% and was valued at 8,998,538 units.

- In Asia-Pacific, the chemical industry is rapidly expanding. Chromium is employed as a catalyst in oxidation processes, ethylene polymerization, and oligomerization catalysts used in the industrial manufacture of polyethylene and 1-hexene, and these qualities are projected to boost the chromium market in the coming years.

- Therefore, the aforementioned factors are expected to significantly impact the market in the coming years.

Chromium Industry Overview

The chromium market is partially consolidated in nature, with a few major players dominating a significant portion of the market. Some of the major companies are (not in any particular order) Kermas Investment Group, Assmang Proprietary Limited, CVK Madencilik, Odisha Mining Corporation Ltd, and Glencore.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Demand for Metallurgical Uses

- 4.1.2 Increasing Refractory Applications in Industries

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Associated Health Effects

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Buyers

- 4.4.2 Bargaining Power of Suppliers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 By Application

- 5.1.1 Chemical

- 5.1.2 Metallurgical

- 5.1.3 Refractory

- 5.1.4 Other Applications (Glass Polishing, Industrial Catalysts, and Pigments )

- 5.2 By Geography

- 5.2.1 Asia-Pacific

- 5.2.1.1 China

- 5.2.1.2 India

- 5.2.1.3 Japan

- 5.2.1.4 South Korea

- 5.2.1.5 Malaysia

- 5.2.1.6 Thailand

- 5.2.1.7 Indonesia

- 5.2.1.8 Vietnam

- 5.2.1.9 Rest of Asia-Pacific

- 5.2.2 North America

- 5.2.2.1 United States

- 5.2.2.2 Canada

- 5.2.2.3 Mexico

- 5.2.3 Europe

- 5.2.3.1 Germany

- 5.2.3.2 United Kingdom

- 5.2.3.3 Italy

- 5.2.3.4 France

- 5.2.3.5 Spain

- 5.2.3.6 NORDIC

- 5.2.3.7 Turkey

- 5.2.3.8 Russia

- 5.2.3.9 Rest of Europe

- 5.2.4 South America

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 Colombia

- 5.2.4.4 Rest of South America

- 5.2.5 Middle East and Africa

- 5.2.5.1 Saudi Arabia

- 5.2.5.2 South Africa

- 5.2.5.3 Nigeria

- 5.2.5.4 Qatar

- 5.2.5.5 Egypt

- 5.2.5.6 United Arab Emirates

- 5.2.5.7 Rest of Middle East and Africa

- 5.2.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Al Tamman Indsil FerroChrome L.L.C

- 6.4.2 Assmang Proprietary Limited

- 6.4.3 CVK Madencilik

- 6.4.4 Glencore

- 6.4.5 Hernic Ferrochrome (Pty) Ltd (Hernic)

- 6.4.6 International Ferro Metals (IFM)

- 6.4.7 Kermas Investment Group

- 6.4.8 MVC Holdings LLC

- 6.4.9 Odisha Mining Corporation Ltd

- 6.4.10 Tenaris

- 6.4.11 YILDIRIM Group of Companies

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Development of Trivalent Chromium Hard Chrome Plating

- 7.2 Other Opportunities

磷酸鐵市場分析及預測(至2035年):類型、產品、應用、技術、終端用戶、成分、形態

磷酸鐵市場分析及預測(至2035年):類型、產品、應用、技術、終端用戶、成分、形態 鋼板用硬質合金鑽頭市場按塗層類型、柄型、刃數、工具機類型、直徑範圍、終端用戶產業、應用和銷售管道分類 - 全球預測(2026-2032 年)

鋼板用硬質合金鑽頭市場按塗層類型、柄型、刃數、工具機類型、直徑範圍、終端用戶產業、應用和銷售管道分類 - 全球預測(2026-2032 年) 全球銦礦開採市場:市場規模、佔有率、趨勢分析(按應用和地區分類)、細分市場預測(2025-2033 年)

全球銦礦開採市場:市場規模、佔有率、趨勢分析(按應用和地區分類)、細分市場預測(2025-2033 年) 全球鉻市場-2025年至2030年預測

全球鉻市場-2025年至2030年預測 鍍鉻棒材:全球市場佔有率及排名、總收入及需求預測(2025-2031 年)碳化鉻鋼板:全球市佔率及排名、總銷售量及需求預測(2025-2031年)按產品形態、通路、最終用戶和應用分類的吡啶甲吡啶市場-2025-2032年全球預測磷酸鉻市場按應用、等級、產品形態、終端用戶產業和分銷管道分類-2025-2032年全球預測鉻化學品市場按產品類型、應用、最終用途產業、形態、等級和分銷管道分類-2025-2032年全球預測鉻市場依產品類型、供應來源、最終用途產業、純度等級及通路分類-2025年至2032年全球預測

鍍鉻棒材:全球市場佔有率及排名、總收入及需求預測(2025-2031 年)碳化鉻鋼板:全球市佔率及排名、總銷售量及需求預測(2025-2031年)按產品形態、通路、最終用戶和應用分類的吡啶甲吡啶市場-2025-2032年全球預測磷酸鉻市場按應用、等級、產品形態、終端用戶產業和分銷管道分類-2025-2032年全球預測鉻化學品市場按產品類型、應用、最終用途產業、形態、等級和分銷管道分類-2025-2032年全球預測鉻市場依產品類型、供應來源、最終用途產業、純度等級及通路分類-2025年至2032年全球預測