|

市場調查報告書

商品編碼

1521312

3D列印粉末:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029)3D Printing Powder - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

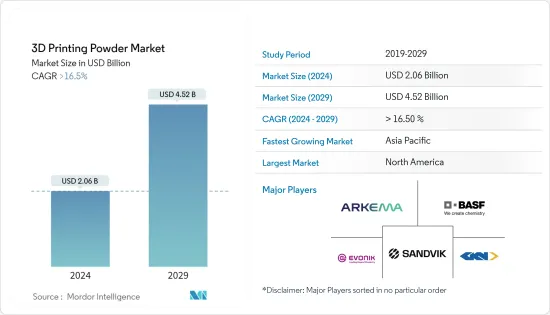

3D列印粉末市場規模預計到2024年為20.6億美元,預計到2029年將達到45.2億美元,在預測期內(2024-2029年)複合年成長率超過16.5%。

COVID-19 大流行對 3D 列印粉末市場產生了各種影響,帶來了挑戰,但也創造了創新和成長的機會。此次疫情加速了3D列印在包括醫療保健在內的各行業的接受度,預計其長期影響將是正面的。因為公司正在投資 3D 列印技術和材料,以加強業務和彈性。

主要亮點

- 疫情加速了對醫療應用中使用的 3D 列印粉末的需求。醫療設備原型設計和個人防護設備(PPE)製造是該市場的主要驅動力。

- 儘管 3D 列印具有變革潛力,但該技術的廣泛採用受到 3D 列印粉末高昂的材料和後處理成本的阻礙。

- 在一個過程中使用多種材料進行列印的能力使得製造具有更複雜結構和功能的產品成為可能,並且越來越受歡迎。支援多材料列印製程的 3D 列印粉末可能會帶來機會。

- 亞太地區主導3D列印粉末市場,其中中國、印度和日本對市場需求貢獻顯著。

3D列印粉末市場趨勢

汽車產業的需求不斷增加

- 汽車產業是利用該技術的主要產業,在最終用戶產業中佔據很大佔有率。多年來,汽車行業廣泛採用該技術來快速製造原型設備和小型自訂產品。它的廣泛應用在汽車和目的地設備製造商 (OEM) 的輕量化零件生產中尤為明顯。

- 3D 列印粉末用於積層製造的各種製程。主要用於汽車、航太和國防產品。 3D 列印硬體透過選擇性沉積連續的優質粉末層來建構物件。

- 3D列印中通常使用不同的材料和不同形式的粉末沉積。其中包括尼龍、生質塑膠、陶瓷、蠟、青銅、不鏽鋼、鈷鉻合金和鈦。

- 3D列印粉末在汽車領域有應用,如殼體、支架、渦輪增壓器、輪胎模具、傳動板、控制閥和幫浦。還包括冷卻通風口、車身面板、儀表板、座椅框架和原型製作、保險桿和其他引擎部件的應用。

- 3D 列印粉末還有助於車輛減重過程,有助於提高車輛性能和效率。

- 根據OICA稱,與2021年相比,2022年全球汽車產業目前將出現6%的顯著成長。 2022年,全球各個已開發國家和開發中國家的汽車產量均增加,包括中國、德國、韓國、英國和義大利。 2022年,汽車產量超過8502萬輛。

- 中國的汽車製造業是全世界最大的。 2021年產銷量小幅成長,2022年成長3%。根據中國工業協會統計,2022年乘用車產量較2021年成長11.2%。

- 快速原型製作市場的開拓、航太領域需求的增加以及發展中地區汽車技術的進步將推動未來幾年對3D列印粉末市場的需求。

亞太地區主導市場

- 由於中國、韓國、日本和印度汽車產業高度發達,亞太地區預計將主導全球市場。再加上該地區多年來為推進醫療和航太技術而持續進行的投資。

- 根據印度汽車工業協會統計,印度汽車工業總合生產汽車2593萬輛。 2022年4月至2023年3月期間包括乘用車、商用車、三輪車、二輪車、四輪車,2021年4月至2022年3月產量為2,304萬輛。

- 3D列印粉末可用於製造航太領域的各種零件。包括過渡導管、引擎零件、飛機起落架旋翼葉輪、噴桿、機架支架、襯套、承載環、耐腐蝕零件等。

- 近年來,亞太地區航太零件生產和組裝基地數量不斷增加,預計在不久的將來打開3D列印零件和粉末的消費前景。

- 根據通用航空工業協會公告,2022年活塞飛機交付數量將較2021年增加8.2%,總合達1,524架。渦輪螺旋槳飛機數量增加10.4%,達到582架,噴射機數量略有增加,從710架增加到712架。 2022 年飛機總交付為 229 億美元。這與前一年同期比較成長了約5.8%。

- 在亞太地區,開發中國家的醫療技術成長巨大。對牙冠、助聽器和整形外科替換部件等客製化植入的需求正在推動醫療產業的擴張。

- 中國、日本、韓國和印度航太和國防領域的發展帶動了新興國家建築業的發展。醫療產業的巨大成長預計將在未來幾年推動 3D 列印粉末市場。

3D列印粉末產業概況

3D列印粉末市場因其性質而部分整合。主要企業(排名不分先後)包括 Sandvik AB、Arkema、 BASF SE、GKN Powder Metallurgy 和 Evonik Industries AG。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第1章簡介

- 研究成果

- 研究場所

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 促進因素

- 航太和汽車產業的應用不斷增加

- 醫療領域需求不斷擴大

- 其他司機

- 抑制因素

- 材料成本和後處理成本高

- 危險的本質

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 買方議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章 市場區隔(以金額為準的市場規模)

- 粉末型

- 塑膠粉末

- 金屬粉末

- 陶瓷粉

- 玻璃粉

- 其他類型(如複合粉末)

- 最終用戶產業

- 車

- 航太/國防

- 醫療保健

- 建築學

- 其他最終用戶產業(消費品、工業等)

- 地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東/非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲

- 亞太地區

第6章 競爭狀況

- 併購、合資、聯盟、協議

- 市場佔有率(%)**/排名分析

- 主要企業策略

- 公司簡介

- Arkema

- BASF SE

- ERASTEEL

- Evonik Industries AG

- ExOne

- GENERAL ELECTRIC

- GKN Powder Metallurgy

- Hoganas AB

- Metalysis

- Sandvik AB

第7章 市場機會及未來趨勢

- 建築創新

- 多材料列印的需求不斷成長

The 3D Printing Powder Market size is estimated at USD 2.06 billion in 2024, and is expected to reach USD 4.52 billion by 2029, growing at a CAGR of greater than 16.5% during the forecast period (2024-2029).

The COVID-19 pandemic had a mixed impact on the 3D printing powder market, presenting challenges but also creating opportunities for innovation and growth. The pandemic accelerated the acceptance of 3D printing in various industries, such as healthcare, and the long-term impact is expected to be positive. It is because companies invest in 3D printing technologies and materials to enhance their operations and resilience.

Key Highlights

- The pandemic spurred demand for 3D printing powders used in medical applications. It is a major driving factor for this market, such as creating prototypes of medical devices and manufacturing personal protective equipment (PPE).

- Despite the transformative potential of 3D printing, the widespread adoption of this technology is hindered by the high material and post-processing cost of 3D printing powder.

- The ability to print with multiple materials in a single process is gaining traction, allowing the creation of products with more complex structures and functionalities. It will provide an opportunity for 3D printing powders that are compatible with multi-material printing processes.

- The Asia-Pacific region dominated the market for 3D printing powder, with China, India, and Japan being the major contributors to the market demand.

3D Printing Powders Market Trends

Growing Demand from Automobile Sector

- The automotive industry is a primary industry that utilizes this technology, holding a significant share in the end-user industries segment. Over the years, the automotive sector extensively employed this technology for the rapid production of prototype equipment and small custom products. Its widespread use is particularly notable in the manufacturing of lightweight components for both automobiles and Original Equipment Manufacturers (OEMs).

- 3D printing powder is used in different processes in additive manufacturing. It is being majorly used in automobile, aerospace, and defense products. 3D printing hardware builds an object by selectively sticking together successive layers of excellent powder.

- Various forms of powder adhesion are commonly used to 3D print, using a wide range of materials. These include nylon, bio-plastics, ceramics, wax, bronze, stainless steel, cobalt chrome, and titanium.

- 3D printing powder finds applications in the automobile sector in the form of housing and brackets, turbochargers, tire molds, transmission plates, and control valves and pumps. It also includes applications in cooling vents, body panels, dashboards, seat frames and prototyping, bumpers, and other engine components.

- Also, 3D printing powder helps in vehicle weight reduction processes that support increasing the performance and efficiency of the vehicles.

- As per OICA, the Global Automotive Industry is currently growing at a substantial rate of 6% in 2022 over 2021. In 2022, various developed and developing countries across the world, including China, Germany, South Korea, Canada, the United Kingdom, and Italy, experienced an increase in automotive production. In 2022, over 85.02 million units of Motor vehicles were manufactured.

- The Chinese automotive manufacturing industry is the largest in the world. The industry witnessed a slight increase in 2021, with a 3% increase in 2022, wherein production and sales inclined. According to the China Association of Automobile Manufacturers (CAAM), the production of passenger cars increased by 11.2% in 2022 over 2021.

- Increasing applications for rapid prototyping, growing demand for the aerospace sector, and technological advancements in automobiles in developing regions are driving the demand for the 3D printing powder market through the years to come.

Asia-Pacific Region to Dominate the Market

- Asia-Pacific is expected to dominate the global market owing to the highly developed automobile sector in China, Korea, Japan, and India. It is coupled with the continuous investments done in the region to advance medical and aerospace technologies through the years.

- As per the Society of Indian Automobile Manufacturers, the Automotive Industry in India manufactured a combined total of 25.93 million vehicles. The vehicles include passenger vehicles, commercial vehicles, three-wheelers, two-wheelers, and quadricycles during the period from April 2022 to March 2023, in comparison to 23.04 million units produced from April 2021 to March 2022.

- 3D printing powder can be used for manufacturing various components in the aerospace sector. It includes transition ducts, engine components, aircraft landing gear rotor blades, spray bars, flame holders, liners, carrier rings, and corrosion-resistant components.

- The growing production and assembly bases for aerospace components in the Asia-Pacific regions in recent years are expected to provide scope for the consumption of 3D-printed components and powders in the near future.

- As per the General Aviation Manufacturers Association, there was an 8.2% rise in piston airplane deliveries in 2022 compared to 2021, totaling 1,524 units. Turboprop airplane deliveries increased by 10.4%, reaching 582 units, while business jet deliveries experienced a marginal increase from 710 to 712 units. The total value of airplane deliveries in 2022 amounted to approximately USD 22.9 billion. It reflected a growth of around 5.8% over the previous year.

- In Asia-Pacific, the growth in medical technology in developing countries is immense. The need for customized implants like tooth crowns, hearing aids, and orthopedic replacement parts is supporting the expansion of the medical industry.

- The growth in aerospace and defense sectors in China, Japan, Korea, and India increased the architectural and construction industries in developing countries. The tremendous growth in the medical sector is expected to drive the market for 3D printing powder through the years to come.

3D Printing Powders Industry Overview

The 3D printing powder market is partially consolidated in nature. The major players (not in any particular order) include Sandvik AB, Arkema, BASF SE, GKN Powder Metallurgy, and Evonik Industries AG, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Applications in Aerospace and Automobile Industries

- 4.1.2 Growing Demand from Medical Sector

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 HIgh Material and Post Processing Cost

- 4.2.2 Hazardous in Nature

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Powder Type

- 5.1.1 Plastic Powder

- 5.1.2 Metal Powder

- 5.1.3 Ceramic Powder

- 5.1.4 Glass Powder

- 5.1.5 Other Types (Composite Powder, etc.)

- 5.2 End-user Industry

- 5.2.1 Automotive

- 5.2.2 Aerospace and Defense

- 5.2.3 Medical

- 5.2.4 Architecture

- 5.2.5 Other End-user Industries (Consumer Goods, Industrial, etc.)

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Arkema

- 6.4.2 BASF SE

- 6.4.3 ERASTEEL

- 6.4.4 Evonik Industries AG

- 6.4.5 ExOne

- 6.4.6 GENERAL ELECTRIC

- 6.4.7 GKN Powder Metallurgy

- 6.4.8 Hoganas AB

- 6.4.9 Metalysis

- 6.4.10 Sandvik AB

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Innovations in Architectural Sector

- 7.2 Increasing Demand for Multi-Material Printing

用於 3D 列印的 PLA 市場:依應用領域(消費品、汽車零件、工業應用、醫療、航空航天與國防、其他)和地區劃分 - 全球預測至 2036 年

用於 3D 列印的 PLA 市場:依應用領域(消費品、汽車零件、工業應用、醫療、航空航天與國防、其他)和地區劃分 - 全球預測至 2036 年 全球3D列印材料市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球3D列印材料市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 2026年全球3D列印材料市場報告

2026年全球3D列印材料市場報告 3D列印材料市場規模、佔有率和趨勢分析報告:按產品、應用、地區和細分市場預測(2026-2033年)

3D列印材料市場規模、佔有率和趨勢分析報告:按產品、應用、地區和細分市場預測(2026-2033年) 噴射清洗細分市場 - 全球產業規模、佔有率、趨勢、機會、預測:按清洗類型、操作方式、產品類型、地區和競爭格局分類,2021-2031年

噴射清洗細分市場 - 全球產業規模、佔有率、趨勢、機會、預測:按清洗類型、操作方式、產品類型、地區和競爭格局分類,2021-2031年 按材料成分、粒徑分佈、粉末分級、應用技術和最終用途產業分類的氣霧化金屬粉末市場-2026-2032年全球預測生質塑膠3D列印市場:按材料類型、列印技術和應用分類,全球預測(2026-2032年)鎳合金粉末市場(按粉末類型、粒度範圍、製造流程、形狀和應用分類)-全球預測(2026-2032年)

按材料成分、粒徑分佈、粉末分級、應用技術和最終用途產業分類的氣霧化金屬粉末市場-2026-2032年全球預測生質塑膠3D列印市場:按材料類型、列印技術和應用分類,全球預測(2026-2032年)鎳合金粉末市場(按粉末類型、粒度範圍、製造流程、形狀和應用分類)-全球預測(2026-2032年) 日本3D列印材料市場報告(按類型、形式、最終用戶和地區分類,2026-2034年)3D列印粉末市場規模、佔有率和趨勢分析報告:按材料類型、應用、地區和細分市場預測(2025-2033年)

日本3D列印材料市場報告(按類型、形式、最終用戶和地區分類,2026-2034年)3D列印粉末市場規模、佔有率和趨勢分析報告:按材料類型、應用、地區和細分市場預測(2025-2033年)