|

市場調查報告書

商品編碼

1521404

自修復塗料:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029)Self-Healing Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

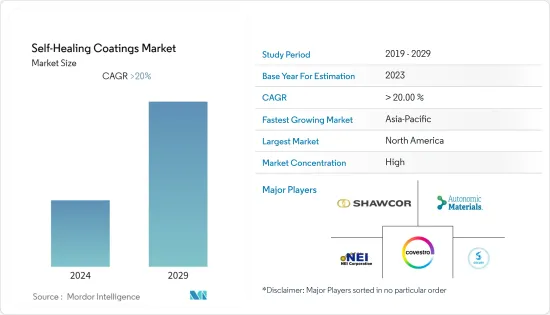

自修復塗料市場規模預計到 2024 年為 27.1 億美元,預計到 2029 年將達到 72.4 億美元,在預測期內(2024-2029 年)複合年成長率將超過 21%。

COVID-19 大流行對自修復塗料市場產生了負面影響。疫情對物流業和製造業產生了重大影響,阻礙了市場拓展。不過,該產業在2021年開始復甦。此後,隨著汽車、建築和電子行業的持續成長,該行業繼續保持強勁成長。

主要亮點

- 中期推動市場的主要因素是新興國家建築和基礎設施行業市場開拓的進展以及汽車和航太行業的日益普及。

- 另一方面,與傳統材料相比,自修復材料的高成本阻礙了所研究市場的成長。

- 電子產業擴大採用自癒塗層可能是市場的一個機會。

- 歐洲在市場上佔據主導地位,對幾家主要企業和行業進行了大量投資。然而,預計亞太地區在預測期內將實現最高成長。

自修復塗料市場趨勢

建築和建設產業主導市場。

- 自修復塗料在建設產業中發揮重要作用。這些塗層具有快速修復裂縫的潛力,因為自癒過程可以實現快速加工。將其用於混凝土中,可以增加建築物、橋樑等的強度並延長其使用壽命。

- 英國土木工程師學會估計,到2025年,排名前三的國家——中國、印度和美國——將佔全球建設產業成長的近60%。

- 據Industry Sources稱,2022年全球建築市場規模預計為9.7兆美元,以中國、美國和印度為主導,預計2037年將達到13.9兆美元。

- 美國在北美建設產業中佔有很大佔有率。

- 根據美國人口普查局統計,2023年美國年度建築業價值為19,787億美元,較2022年成長約7.03%。

- 由於中國和印度的住宅建築市場不斷擴大,亞太地區的住宅預計將錄得最高漲幅。到2030年,這兩個國家的中產階級預計將佔全球中階的43.3%以上。

- 全球範圍內的此類建築建設活動預計將增加該行業對自修復塗料的需求並推動市場成長。

亞太地區成長最快

- 由於建築、電氣和電子以及運輸等行業的需求,預計亞太地區在預測期內將實現最高成長。

- 在整個全部區域,主要國家的人口成長和快速都市化正在推動住宅建設的需求。

- 根據Global Construction Perspectives和牛津經濟研究院的聯合研究,印度未來14年將需要每天建造31,000套住宅才能滿足不斷成長的住宅需求,到2030年終,每天將需要建造170,000套住宅。 。

- 根據美國國際貿易管理局的數據,中國是世界上最大的建築市場,預計到2030年將以年均8.6%的速度成長。據國家發展和改革委員會稱,2025年中國重大建設計劃投資將達1.43兆美元。

- 根據中國國家統計局數據顯示,2023年中國建築業總產值成長1.99%,達到712847.2億元人民幣(約108,677.8億美元)。

- 根據住宅及城鄉建設部預測,2025年中國建築業預計將維持GDP的6%。鑑於這些預測,2022年1月,中國政府宣布了五年計劃,透過品質和主導發展來提高建設產業的永續性。

- 印度的住宅產業也在成長,政府的支持和措施進一步刺激了需求。在2022-2023年預算中,住房與城市發展部(MoHUA)已撥款約98.5億美元,為住宅建設和完成停滯計劃創造資金。

- 自修復塗層在汽車和電子等其他最終用戶行業中也發揮多種作用。在汽車行業,自修復塗料用於汽車重塗塗料,並配製成OEM透明塗層和塑膠透明塗層。目前,這款智慧型手機的背面採用了自修復聚合物塗層。

- 該地區對電子產品的需求主要來自中國、印度和日本。此外,低廉的人事費用和靈活的政策使中國成為電子製造商強勁且利潤豐厚的市場。

- 日本電子情報技術產業協會(JEITA)公佈的資料顯示,2022年日本電子產業總產值約為111,243億日圓(約845.9億美元),比上年成長近8% 。

- 從年銷量和產量來看,中國是全球最大的汽車市場。根據OICA預測,2022年中國汽車產量將達2,702萬輛,較2021年成長3%。

- 因此,建築建設活動的活性化、電子產業的成長以及其他產業的需求正在推動自修復塗料和其他應用的成長,預計將在預測期內推動市場成長。

自修復塗料產業概況

自修復塗料市場因其性質而得到鞏固。該市場的主要企業包括(排名不分先後)NEI Corporation、Solvay、Autonomic Materials, Inc.、Covestro AG 和 Akzo Nobel NV。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章 簡介

- 調查先決條件

- 調查範圍

第2章調查方法

第3章執行概述

第4章市場動態

- 促進因素

- 建築及基礎建設產業發展

- 汽車和航太產業的採用率增加

- 其他阻礙因素

- 抑制因素

- 自修復塗料成本高

- 其他阻礙因素

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 買方議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章 市場區隔(以金額為準的市場規模)

- 按形式

- 外在

- 基本的

- 按最終用戶產業

- 建築/施工

- 車

- 航太

- 電力/電子

- 其他最終用戶產業(船舶、醫療設備等)

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 馬來西亞

- 泰國

- 印尼

- 越南

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 義大利

- 法國

- 西班牙

- 北歐國家

- 土耳其

- 俄羅斯

- 歐洲其他地區

- 南美洲

- 巴西

- 阿根廷

- 哥倫比亞

- 南美洲其他地區

- 中東/非洲

- 沙烏地阿拉伯

- 南非

- 奈及利亞

- 卡達

- 埃及

- 阿拉伯聯合大公國

- 其他中東/非洲

- 亞太地區

第6章 競爭狀況

- 併購、合資、聯盟、協議

- 市場佔有率(%)**/市場排名分析

- 主要企業策略

- 公司簡介

- 3M

- Akzo Nobel NV

- Autonomic Materials Inc.

- BASF SE

- Covestro AG

- FEYNLAB INC

- GVD Corporation

- NEI Corporation

- Solvay

- spotLESS Materials Inc.

- Winn & Coales(Denso)Ltd

- Revivify Coatings America

第7章 市場機會及未來趨勢

- 自修復塗料在電子產業的廣泛採用

- 其他機會

The Self-Healing Coatings Market size is estimated at USD 2.71 billion in 2024, and is expected to reach USD 7.24 billion by 2029, growing at a CAGR of greater than 21% during the forecast period (2024-2029).

The COVID-19 pandemic had a negative impact on the self-healing coatings market. The pandemic significantly influenced the logistics and manufacturing industries, stifling market expansion. The industry, however, rebounded in 2021. Since then, it has been growing at a good rate, as the automotive, construction, and electronic industries have all experienced continuous growth.

Key Highlights

- Over the medium term, the key factors driving the market are the growing development of the construction and infrastructure industries in emerging countries and increasing adoption in the automotive and aerospace industries.

- On the flip side, the high cost of self-healing materials over conventional materials is hindering the growth of the studied market.

- The increasing adoption of self-healing coatings in the electronics industry is likely to act as an opportunity for the market.

- Europe has been dominating the market due to several key players and major investments in the industries. However, Asia-Pacific is expected to register the highest growth during the forecast period.

Self-Healing Coatings Market Trends

Building and Construction Industry to Dominate the Market

- Self-healing coatings play an important role in the construction industry. These coatings have the potential to fix the cracks rapidly, as the self-healing process allows for speedy treatment. It is used in concrete to provide strength and extend the life of buildings, bridges, and other structures.

- As per the estimates of the Institution of Civil Engineers, the top three countries, i.e., China, India, and the United States, will account for almost 60% of all growth in the global construction industry by 2025.

- According to Industrial Sources, global construction was valued at USD 9.7 trillion in 2022, and it is forecasted to reach USD 13.9 trillion by 2037, driven by superpower construction markets China, the United States, and India.

- The United States includes a significant share of the construction industry in North America.

- According to the US Census Bureau, the annual value for construction in the United States accounted for USD 1,978.7 billion in 2023, which was an increase of about 7.03% compared to that of 2022.

- Due to the increasing housing construction markets in China and India, Asia-Pacific is expected to record the highest growth in house prices. By 2030, these two countries are expected to represent more than 43.3% of the world's middle class.

- All these building and construction activities in various locations throughout the world are expected to increase the demand for self-healing coatings in the industry, propelling the market's growth.

Asia-Pacific to Register Highest Growth

- Asia-Pacific is expected to register the highest growth during the forecast period due to demand from industries such as building and construction, electrical and electronics, and transportation.

- Across the region, due to the growing population and rapid urbanization in major countries, the demand for residential construction has been rising.

- According to a joint study conducted by Global Construction Perspectives and Oxford Economics, India will need to build 31,000 homes every day for the next 14 years to meet its growing housing demand, adding up to 170 million properties by the end of 2030.

- As per the US International Trade Administration, China is the largest global construction market and is expected to grow at an average annual rate of 8.6% by 2030. According to the National Development and Reform Commission (NDRC), China will invest USD 1.43 trillion in significant construction projects till 2025.

- According to the National Bureau of Statistics of China, the gross output value of the construction industry in China in 2023 increased by 1.99% and was valued at CNY 71,284.72 billion (~USD 10,086.78 billion).

- According to the Ministry of Housing and Urban Rural Development's forecast, China's construction sector is projected to remain at 6 % of its GDP in 2025. In view of these forecasts, in January 2022, the Chinese government announced a five-year plan to improve sustainability in the construction industry through quality and driven development.

- In addition, the residential sector in India is growing, and government support and initiatives are further boosting demand. In the 2022-2023 budget, the Ministry of Housing and Urban Development (MoHUA) allocated about USD 9.85 billion to construct houses and create funds to complete the halted projects.

- Self-healing coatings also serve a variety of other purposes in other end-user industries, such as automotive, electronics, and many more. In the automotive industry, self-healing coatings are used in automotive refinish coatings, with OEM clear-coat and plastic clear-coat formulations. Smartphones now use a self-healing polymer coating on the back.

- The demand for electronics products in the region mainly comes from China, India, and Japan. Furthermore, China is a robust and favorable market for electronics producers, owing to the country's low labor cost and flexible policies.

- According to the data released by the Japanese Electronics and Information Technology Industries Association (JEITA), in 2022, the total production value of the electronics industry in Japan accounted for around JPY 11,124.3 billion (~USD 84.59 billion), showcasing a rise of nearly 8% from the previous year.

- China is the world's largest automotive market in terms of annual sales and manufacturing output. According to OICA, vehicle production in China reached a total of 27.02 million units in 2022, an increase of 3% over 2021.

- Thus, the growing building and construction activities, the rising electronics sector, and the demand from other industries are instrumental in the growth of self-healing coatings and other applications, which, in turn, is expected to boost the market's growth during the forecast period.

Self-Healing Coatings Industry Overview

The self-healing coatings market is consolidated in nature. Some of the key players in the market include (not in any particular order) NEI Corporation, Solvay, Autonomic Materials, Inc., Covestro AG, and Akzo Nobel NV.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Development of Construction and Infrastructure Industry

- 4.1.2 Increasing Adoption in Automotive and Aerospace Industries

- 4.1.3 Other Restraints

- 4.2 Restraints

- 4.2.1 High Cost of Self-healing Coatings

- 4.2.2 Other Restraints

- 4.3 Industry Value-chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 By Form

- 5.1.1 Extrinsic

- 5.1.2 Intrinsic

- 5.2 By End-user Industry

- 5.2.1 Building and Construction

- 5.2.2 Automotive

- 5.2.3 Aerospace

- 5.2.4 Electrical and Electronics

- 5.2.5 Other End-user Industries (Marine, Medical Devices, etc.)

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Malaysia

- 5.3.1.6 Thailand

- 5.3.1.7 Indonesia

- 5.3.1.8 Vietnam

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Spain

- 5.3.3.6 NORDIC Countries

- 5.3.3.7 Turkey

- 5.3.3.8 Russia

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Nigeria

- 5.3.5.4 Qatar

- 5.3.5.5 Egypt

- 5.3.5.6 United Arab Emirates

- 5.3.5.7 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/ Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 3M

- 6.4.2 Akzo Nobel NV

- 6.4.3 Autonomic Materials Inc.

- 6.4.4 BASF SE

- 6.4.5 Covestro AG

- 6.4.6 FEYNLAB INC

- 6.4.7 GVD Corporation

- 6.4.8 NEI Corporation

- 6.4.9 Solvay

- 6.4.10 spotLESS Materials Inc.

- 6.4.11 Winn & Coales (Denso) Ltd

- 6.4.12 Revivify Coatings America

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Adoption of Self-healing Coatings in Electronics Industry

- 7.2 Other Opportunities

全球自修復塗層市場自修復塗料市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測

全球自修復塗層市場自修復塗料市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測 自修復塗料市場:按形式、最終用戶分類 - 2025-2030 年全球預測

自修復塗料市場:按形式、最終用戶分類 - 2025-2030 年全球預測 自我修復塗料市場,規模,佔有率,趨勢,產業分析報告:不同形態,各最終用途,各地區 - 市場預測 2025~2034年

自我修復塗料市場,規模,佔有率,趨勢,產業分析報告:不同形態,各最終用途,各地區 - 市場預測 2025~2034年 2030 年自修復塗料市場預測:按塗料類型、形式、最終用戶和地區進行的全球分析

2030 年自修復塗料市場預測:按塗料類型、形式、最終用戶和地區進行的全球分析 自我修復型智慧塗料的全球市場

自我修復型智慧塗料的全球市場 全球自我修復塗料市場研究報告 - 2023 年至 2030 年的行業分析、規模、佔有率、成長、趨勢和預測

全球自我修復塗料市場研究報告 - 2023 年至 2030 年的行業分析、規模、佔有率、成長、趨勢和預測 全球自修復塗料市場:按幾何形狀(內在、外在)、最終用途行業(汽車、建築和施工、航空航天、海洋)、地區(亞太、歐洲、北美、南美、中東和非洲) ) 預測(到 2028 年)

全球自修復塗料市場:按幾何形狀(內在、外在)、最終用途行業(汽車、建築和施工、航空航天、海洋)、地區(亞太、歐洲、北美、南美、中東和非洲) ) 預測(到 2028 年)