|

市場調查報告書

商品編碼

1521411

手錶:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029)Atomic Clock - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

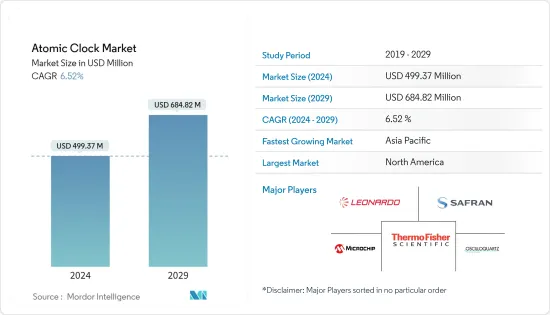

預計 2024 年手錶市場規模為 4.9937 億美元,2029 年將達到 6.8482 億美元,在預測期內(2024-2029 年)複合年成長率為 6.52%。

航太和軍事領域對高精度手錶的需求不斷成長,推動了手錶市場的成長。手錶可確保準確的單向距離測量,並確保保持傳輸的 GPS 訊號的相位精度。量子計算和量子通訊的開拓預計將為市場帶來更好的機會。

全球導航和定位系統的擴展、手錶在 GPS 和 GNSS 系統中應用的興起也推動了手錶市場的成長。然而,高昂的部署和維護成本可能會阻礙預測期內的市場成長。

手錶市場趨勢

預測期內國防占主導市場佔有率

隨著世界各國軍隊尋求透過整合新的精確定位導航系統來實現老化飛機的現代化,國防領域的最終用戶對手錶的需求量很大。大多數當前一代飛機都使用 GNSS (GPS) 和 TACAN 定位導航系統,預計在預測期內對新飛機的需求也將產生對手錶的平行需求。

在此背景下,2018年12月,美國宣布將在其機隊中整合下一代GPS接收器,以提高導航和定位的品質。美國生命週期管理中心已選擇羅克韋爾柯林斯為其 F-16 機隊提供最新一代數位 GPS 抗干擾接收器 (DIGAR)。預計各個軍隊的類似舉措將在預測期內推動該領域的成長。

包括美國、德國、印度、澳洲、阿拉伯聯合大公國和中國在內的許多國家正在投資對其現有軍用飛機機隊進行現代化改造,而不是購買全新的平台。例如,2018年12月,美國宣布其戰鬥機將配備下一代GPS接收器,以改善導航和定位測量。根據該舉措,美國生命週期管理中心選擇羅克韋爾柯林斯為其 F-16 機隊提供最新一代數位 GPS 抗干擾接收器(DIGAR)。預計各個軍隊的類似舉措將在預測期內推動該領域的成長。

飛機導航設備的進步預計將為公司創造新的市場機會。例如,諾斯羅普·格魯曼公司的ASAF(全源自適應融合)軟體允許在不使用全球定位系統(GPS)衛星訊號的情況下引導軍用飛機和機載武器系統。此類軟體與先進的感測器系統相結合,預計將提高航空平台的營運效率。

預計北美在預測期內將佔據最大的市場佔有率

根據斯德哥爾摩國際和平研究所(SIPRI)預測,2022年全球國防支出將超過2兆美元,美國等軍事強國2022年將大幅增加國防預算。 2021年至2022年美國國防支出增加710億美元,佔全球國防支出近40%。

美國繼續開發和採購下一代飛機,以滿足與俄羅斯和中國的大國衝突的需求。美國擁有 13,247 架飛機,包括作戰飛機、儲備飛機和退役飛機。由於與日本和台灣等國家的外交和軍事關係,日本被迫投入大量資金增加其機隊,以應對中國的挑釁性軍事行動。

此外,美國介入中東地區的軍事衝突對攻擊機和運輸機的採購也產生了重大影響。美國空軍提案2023會計年度預算要求為1,940億美元,比2022會計年度預算要求增加202億美元(11.7%)。該預算的大部分將用於採購新飛機以及新技術的研發,以支持國家的軍事行動。此外,太空領域支出的增加、商業和國防應用衛星發射的數量增加以及 NASA 和 SpaceX 擴大太空探勘活動是美國市場的重要助推器,並正在推動北美地區的手錶市場。

手錶產業概況

手錶市場是半固定的,全球只有少數參與企業在企業發展。主要參與企業包括 Thermo Fisher Scientific Inc.、Oscilloquartz (Adtran Networks SE)、Microchip Technology Inc.、Leonardo SpA 和 Safran。市場競爭非常激烈,各公司都在爭奪最大的市場佔有率。

每家公司都利用其內部製造能力、全球網路、產品陣容、研發投資和強大的基本客群來競爭。特定價格分佈內的技術力和產品特性也是重要的市場參數。對精確定位和導航功能不斷成長的需求正在推動市場參與企業擴大產品系列。新進入者的威脅是中等的,由於產品/服務的擴張和技術創新的不斷發展,預計市場的競爭格局將會加劇。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章 簡介

- 調查先決條件

- 調查範圍

第2章調查方法

第3章執行概述

第4章市場動態

- 市場概況

- 市場促進因素

- 市場限制因素

- 波特五力分析

- 買家/消費者的議價能力

- 供應商的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間敵對關係的強度

第5章市場區隔

- 類型

- 銣 (Rb)手錶

- 銫 (Cs)手錶

- 氫 (H) 脈澤手錶

- 最終用戶

- 防禦

- 戰鬥機和直升機

- 無人車

- 裝甲車

- 可攜式系統

- 船(驅逐艦、巡防艦等)

- 潛水艇

- 巡邏船

- 宇宙

- 防禦

- 目的

- 監視

- 導航

- 電子戰

- 遙測

- 通訊

- 按地區

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 俄羅斯

- 義大利

- 西班牙

- 波蘭

- 歐洲其他地區

- 亞太地區

- 中國

- 日本

- 印度

- 其他亞太地區

- 拉丁美洲

- 巴西

- 其他拉丁美洲

- 中東/非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

- 其他中東/非洲

- 北美洲

第6章 競爭狀況

- 供應商市場佔有率

- 公司簡介

- AccuBeat Ltd.

- Excelitas Technologies Corp.

- IQD Frequency Products Limited

- Leonardo SpA

- Microchip Technology Incorporated

- Oscilloquartz(Adtran Networks SE)

- Stanford Research Systems

- Tekron International Limited

- VREMYA-CH JSC

- Safran

- MacQsimal(CSEM)(accelopment Schweiz AG)

- Thermo Fisher Scientific Inc

第7章 市場機會及未來趨勢

The Atomic Clock Market size is estimated at USD 499.37 million in 2024, and is expected to reach USD 684.82 million by 2029, growing at a CAGR of 6.52% during the forecast period (2024-2029).

The atomic clock market's growth is attributed to the increasing need for high-precision atomic clocks in the aerospace and military sectors. Atomic clocks guarantee accurate one-way range measurements, ensuring the user maintains the transmitted GPS signal's phase precision. Developments in quantum computing and quantum communication are expected to create better opportunities for the market.

The expansion of global navigation and positioning systems and the rise of atomic clock applications in GPS and GNSS systems are also fueling the growth of the atomic clock market. However, the high cost of deployment and maintenance may hinder the market's growth during the forecast period.

Atomic Clock Market Trends

Defense to Dominate Market Share During the Forecast Period

The atomic clocks are in huge demand from defense end-users as the global armed forces look to modernize their aging fleet by integrating new and accurate position and navigation systems. Most current-generation aircraft utilize GNSS (GPS) and TACAN positioning and navigation systems, and the demand for new aircraft would also generate parallel demand for atomic clocks during the forecast period.

On this note, in December 2018, the US Air Force announced the fleet-wide integration of next-generation GPS receivers to enhance the quality of navigation and positioning measurements. The US Air Force Life Cycle Management Center selected Rockwell Collins to provide its latest-generation Digital GPS Anti-Jam Receiver (DIGAR) for its fleet of F-16 aircraft. Similar initiatives from various armed forces are anticipated to propel the segment's growth during the forecast period.

Many countries, such as the United States, Germany, India, Australia, the United Arab Emirates, and China, are investing in modernizing their existing fleet of military aircraft rather than acquiring entirely new platforms. For instance, in December 2018, the US Air Force announced that their fighter aircraft would be fitted with next-generation GPS receivers to enhance the quality of navigation and positioning measurements. Under this initiative, the US Air Force Life Cycle Management Center selected Rockwell Collins to provide its latest-generation Digital GPS Anti-Jam Receiver (DIGAR) for its fleet of F-16 aircraft. Similar initiatives from various armed forces are anticipated to propel the segment's growth during the forecast period.

The anticipated advancement of navigational aids for aircraft is expected to create new market opportunities for companies. For instance, Northrop Grumman Corporation's All Source Adaptive Fusion (ASAF) software allows military aircraft and airborne weapon systems to guide them without using Global Positioning System (GPS) satellite signals. Such software, when used with advanced sensor systems, is anticipated to improve the operational efficiencies of the air platforms.

North America is Expected to Have the Largest Market Share During the Forecast Period

The world defense expenditure crossed over USD 2 trillion in 2022, with significant military powers such as the US surging their defense budgets in 2022, according to the Stockholm International Peace Research Institute (SIPRI). US defense spending increased by USD 71 billion from 2021 to 2022, which comprised nearly 40% of global defense expenditures.

The US Air Force continues developing and procuring next-generation aircraft to meet the demands of great power conflicts with Russia and China. The US Air Force comprises 13,247 aircraft that are part of an operational, reserve, and out-of-service fleet. The country's diplomatic and military relations with nations such as Japan and Taiwan have compelled it to drive significant investments into increasing the fleet of aircraft to counter any provocative military action from China successfully.

Furthermore, the US involvement in the military conflict in the Middle Eastern region majorly drove its procurement of attack aircraft and transport aircraft. The Department of Air Force proposed a budget request of USD 194 billion for FY2023, a USD 20.2 billion or 11.7% increase from the FY2022 budget request. A major chunk of this budget will be channeled toward the procurement of new aircraft and research and development of new technologies that can aid the military actions undertaken by the country. Also, the rising expenditure on the space sector, increasing number of satellite launches for commercial and defense applications, and growing space exploration activities from NASA and SpaceX are significant boosters for the US market, which drives the atomic clock market in the North American region.

Atomic Clock Industry Overview

The atomic clock market is semi-consolidated, with a handful of players operating globally. Thermo Fisher Scientific Inc., Oscilloquartz (Adtran Networks SE), Microchip Technology Inc., Leonardo SpA, and Safran are some of the major market players. The market is highly competitive, with players competing to gain the largest market share.

Market players compete, leveraging their in-house manufacturing capabilities, global network footprint, product offerings, research and development investments, and robust client base. Technical capabilities and product features at definite price points are also key market parameters. The increasing demand for accurate positioning and navigation capabilities drives the market players to broaden their product portfolio. With a moderate threat of new entrants, the market's competitive landscape is projected to intensify due to heightened product/service extensions and technological innovations.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Buyers/Consumers

- 4.4.2 Bargaining Power of Suppliers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Rubidium (Rb) Atomic Clock

- 5.1.2 Cesium (Cs) Atomic Clock

- 5.1.3 Hydrogen (H) Maser Atomic Clock

- 5.2 End User

- 5.2.1 Defense

- 5.2.1.1 Combat Aircraft and Helicopters?

- 5.2.1.2 Unmanned Vehicles?

- 5.2.1.3 Armoured Vehicles

- 5.2.1.4 Portable Systems

- 5.2.1.5 Naval Ships (Destroyers, Frigates, etc)

- 5.2.1.6 Submarines?

- 5.2.1.7 Patrol Vessels?

- 5.2.2 Space

- 5.2.1 Defense

- 5.3 Application

- 5.3.1 Surveillance

- 5.3.2 Navigation

- 5.3.3 Electronic Warfare?

- 5.3.4 Telemetry

- 5.3.5 Communication

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 Germany

- 5.4.2.3 France

- 5.4.2.4 Russia

- 5.4.2.5 Italy

- 5.4.2.6 Spain

- 5.4.2.7 Poland

- 5.4.2.8 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Rest of Asia-Pacific

- 5.4.4 Latin America

- 5.4.4.1 Brazil

- 5.4.4.2 Rest of Latin America

- 5.4.5 Middle East and Africa

- 5.4.5.1 United Arab Emirates

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 South Africa

- 5.4.5.4 Rest of Middle East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 AccuBeat Ltd.

- 6.2.2 Excelitas Technologies Corp.

- 6.2.3 IQD Frequency Products Limited

- 6.2.4 Leonardo S.p.A.

- 6.2.5 Microchip Technology Incorporated

- 6.2.6 Oscilloquartz (Adtran Networks SE)

- 6.2.7 Stanford Research Systems

- 6.2.8 Tekron International Limited

- 6.2.9 VREMYA-CH JSC

- 6.2.10 Safran

- 6.2.11 MacQsimal (CSEM) (accelopment Schweiz AG)

- 6.2.12 Thermo Fisher Scientific Inc