|

市場調查報告書

商品編碼

2066757

軟性中型散貨箱(FIBC):市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)Flexible Intermediate Bulk Container (FIBC) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

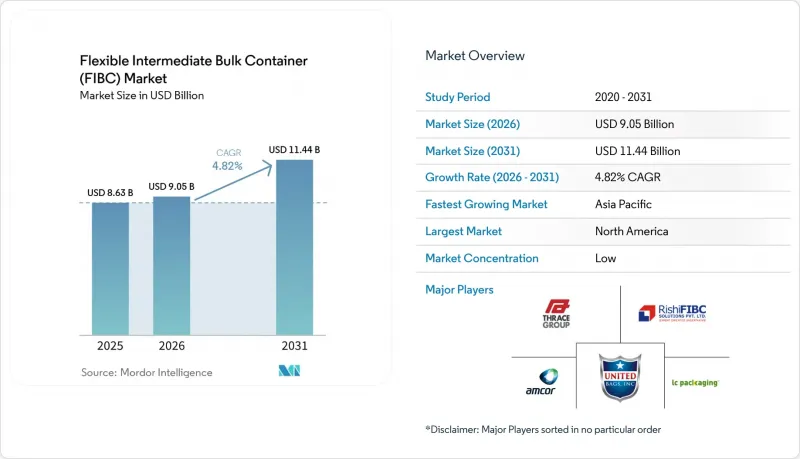

根據 Mordor Intelligence 預測,軟性中型散貨箱(FIBC) 市場規模預計將在 2025 年達到 86.3 億美元,2026 年達到 90.5 億美元,到 2031 年達到 114.4 億美元,2026 年至 2031 年的複合成長率為 4.82%。

本報告按類型(A、B、C、D)、設計(U型、擋板式、圓形、四面板式及其他)、最終用戶(食品、化學、製藥、建築、採礦及其他)、容量(500公斤以下、500-1000公斤、1000-1500公斤、1500公斤以下、500-1000公斤、1000-1500公斤、1500公斤以下、500-1000公斤、1000-1500材質、PP市場預測以美元計價。

全球軟性中型散貨箱(FIBC)市場趨勢與洞察

食品和農產品大宗出口繁榮

全球糧食和特種作物供應鏈回流趨勢推動了對食品級軟性貨櫃的需求,這種集裝袋能夠降低單位運輸成本並防止交叉污染。將於2024年生效的美國農業用水法規修正案將加強農產品可追溯性,迫使出口商採用可與數位化記錄系統無縫整合的條碼軟性貨櫃。巴西和印度等正在擴大港口基礎設施的國家正在投資建造散裝物料處理筒倉,以容納軟性集裝袋的排放設施,從而促進中期成長。大宗商品價格的波動進一步促使生產商選擇能夠降低包裝成本並維持利潤率的軟性中型散貨箱市場解決方案。因此,食品安全法規與成本管理之間的協同作用支撐著該領域的韌性。

危險化學品處理法規的推出將刺激需求。

美國職業安全與健康管理局 (OSHA) 於 2024 年修訂了聯合國全球化學品統一分類和標籤制度 (GHS) 第 7 版,提高了運輸易燃粉末和溶劑容器的技術要求。採用導電紗線和 CROHMIQ 織物的 C 型和 D 型包裝袋現已成為化工廠、製藥混合廠和鋰礦加工廠的標準配置。儘管成本差異高達 20-30%,採購負責人仍在從通用包裝袋轉向認證產品,因為這些產品被視為降低風險、減少運作和保險風險的資產。短短 18 個月的合規期加速了訂單成長,北美和歐洲特種產品線的運轉率仍然很高。因此,靜電防護軟性中型散貨箱的市場需求預計將持續成長。

PP樹脂價格波動

受原油價格波動和煉油廠停產的影響,聚丙烯原物料價格波動佔包裝袋生產成本的60%至70%,對缺乏避險手段的中小型加工商帶來壓力。儘管2024年6月樹脂價格下跌帶來了暫時的緩解,但長期的不確定性迫使買家推遲大宗訂單或按季度重新談判。大型製造商正透過後向整合樹脂混煉業務和加速採用再生聚丙烯來抵消風險,但中型企業的利潤率正面臨壓力。隨著期貨合約的增加和再生材料使用量的擴大,軟性中型散貨箱市場短期內的負面影響正在逐步緩解。

細分市場分析

到2025年,A型容器的需求量將佔總需求量的65.74%,凸顯了其在糧食、水泥和非易燃化學品運輸領域的重要地位。同時,D型靜電防護袋的需求量正以7.53%的複合年成長率成長,因為鋰礦精煉廠和製藥乾燥機製造商指定使用非接地解決方案以避免點火風險。

由於法律規範加大且無需外部接地線,D型貨櫃成為最佳選擇,降低了偏遠礦場和海上鑽井設施的合規複雜性。高抗張強度CROHMIQ織物擁有超過4000萬次安全運輸的記錄,證明了其在惡劣環境下的可靠性,並推動了軟性中型散貨箱市場的未來成長。

預計到2025年,帶有內部隔板以防止鼓脹並提高裝載密度的擋板式和Q型袋將佔據34.12%的市場佔有率。這對於船舶貨艙和都市區物流中心而言具有決定性優勢。 U型袋尺寸精度高,可與機器人填充框架無縫配合,預計到2031年將以8.28%的複合年成長率成長。

圓形和四面體設計的容器在需要最大容量和精確排放的應用中仍然佔據一席之地,但由於精益倉儲的持續推進,帶擋板的設計正變得越來越受歡迎。在採用托盤掃描的自動化設施中,統一尺寸的面積備受青睞,這推動了異形軟性中型散貨箱市場的發展。

區域分析

預計到2025年,北美將佔全球銷售額的38.25%,這得益於成熟的化學品供應鏈、龐大的農產品出口量以及嚴格的OSHA合規要求,這些因素共同推動了高利潤認證包裝袋的銷售。隨著資產所有者對智慧包裝維修進行再投資,以及國內頁岩化學品產量保持強勁,該地區正處於穩步成長的軌道上。

亞太地區正以7.78%的複合年成長率(CAGR)保持最快增速,這主要得益於對電池金屬提煉的大量投資以及眾多製造業領域的擴張。中國包頭稀土元素中心、印度與生產連結獎勵計畫以及東南亞農產品出口的成長,都促進了該地區對導電和高密度設計產品的訂單增加。像Bulkcorp International這樣的本土製造商正在擴大產能並簽訂出口契約,展現了其強大的競爭力,從而推動了軟性中型散貨箱(FIBC)市場的發展。

歐洲憑藉在「綠色新政」下率先採用再生材料規範並部署逆向物流以完善多程運輸模式,保持顯著的市場佔有率。南美洲受益於大豆、玉米和鋰鹵水的出口,這些產品需要食品級或重型包裝袋;而中東和非洲則受益於石化行業的擴張和大型企劃。因此,區域多角化正在為整個軟性中型散貨箱(FIBC)市場創造機會。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 食品和農產品大宗出口繁榮

- 危險化學品處理法規正在推動需求成長。

- 電子商務履約中批量二次包裝的過渡

- 智慧軟性貨櫃袋(物聯網/RFID)的即時追溯實施

- 引進符合循環經濟要求的紙本和再生聚丙烯貨櫃袋

- 鋰和稀土元素供應鏈中礦用噸袋的標準化

- 市場限制因素

- PP樹脂價格波動

- 與嚴格的靜電消除認證相關的成本

- 海運貨櫃短缺正在擾亂軟性貨櫃的供應。

- 剛性 IBC 租賃池的擴張正在蠶食對一次性 FIBC 的需求。

- 供應鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按類型

- A型

- B型

- C型

- D型

- 有意為之

- U型面板

- 擋板/Q袋

- 圓

- 4塊面板

- 其他設計

- 按最終用戶行業分類

- 食品和農業

- 化工/石油化工

- 製藥

- 建築/施工

- 採礦和礦產

- 其他

- 按產能

- 500公斤或以下

- 500~1,000 kg

- 1,000~1,500 kg

- 1500公斤或以上

- 材質

- 維珍PP

- 含再生材料的PP

- 紫外線穩定聚丙烯

- 紙基複合材料

- 生物基聚合物混合物

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲和紐西蘭

- 其他亞太國家

- 中東和非洲

- 中東

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 埃及

- 其他非洲國家

- 中東

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Greif Inc.

- Amcor Plc

- LC Packaging International BV

- Thrace Group

- Rishi FIBC Solutions Pvt Ltd

- United Bags Inc.

- Bag Corp

- Bulk Lift International LLC

- Conitex Sonoco

- Intertape Polymer Group

- Emmbi Industries Ltd

- Schoeller Allibert Group BV

- BAG Supplies Canada Ltd

- Southern Packaging LP

- Plastipak Group

- FlexiTuff International Ltd

- Bulk Pack Exports Ltd

- J&HM Dickson Ltd

- Houston Bulk Bag Co.

- Jumbo Bag Corporation

- Mule Bag Co.

第7章 市場機會與未來展望

According to Mordor Intelligence, the flexible intermediate bulk container market size is projected to be USD 8.63 billion in 2025, USD 9.05 billion in 2026, and reach USD 11.44 billion by 2031, growing at a CAGR of 4.82% from 2026 to 2031.

This report is Segmented by Type (A, B, C, D), Design (U-Panel, Baffle, Circular, 4-Panel, Others), End-User (Food, Chemicals, Pharma, Construction, Mining, Others), Capacity (Up To 500kg, 500-1000kg, 1000-1500kg, Above 1500kg), Material (Virgin PP, Recycled PP, UV PP, Paper, Bio-Based), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Flexible Intermediate Bulk Container (FIBC) Market Trends and Insights

Food and Agro Commodities Bulk-Export Boom

Global reshoring of grain and specialty-crop supply chains is boosting demand for food-grade flexible bulk bags that lower per-unit freight cost and prevent cross-contamination. Updated U.S. agricultural-water rules effective 2024 require tighter produce traceability, pushing exporters toward barcode-ready FIBCs that integrate seamlessly with digital record systems. Countries expanding port infrastructure, such as Brazil and India, are investing in bulk-handling silos designed around FIBC discharge equipment, reinforcing mid-term growth. Commodity-price swings further encourage growers to choose flexible intermediate bulk container market solutions that cut packaging spend while protecting margins. The confluence of food-safety regulation and cost discipline therefore underpins the segment's resilience.

Hazardous-Chemical Handling Rules Boosting Demand

OSHA's 2024 alignment with UN GHS revision 7 raises the technical bar for containers that carry flammable powders and solvents. Type C and Type D bags with conductive yarns and CROHMIQ fabrics are now standard at chemical plants, pharmaceutical mixers and lithium-ore processors. Procurement managers are switching from commodity sacks to certified units despite premiums of 20-30%, viewing them as risk-mitigation assets that reduce downtime and insurance exposure. Short 18-month compliance windows have pulled forward orders, keeping utilization high for specialty lines in North America and Europe. The result is a durable uplift in the flexible intermediate bulk container market for electrostatic-safe variants.

PP Resin Price Volatility

Polypropylene feedstock swings, driven by crude-oil moves and refinery outages, make up 60-70% of bag production cost, undermining smaller converters that lack hedging tools. June 2024 resin drops offered brief relief, yet chronic uncertainty compels buyers to delay blanket orders or renegotiate quarterly. Larger manufacturers offset exposure by backward integrating into resin compounding and accelerating adoption of recycled PP, but mid-tier players face margin squeeze. The short-term drag on the flexible intermediate bulk container market gradually eases as futures-based contracts and recycled feedstocks gain traction.

Other drivers and restraints analyzed in the detailed report include:

- E-Commerce Fulfilment Shift to Bulk Secondary Packaging

- Smart-FIBC Rollout for Real-Time Traceability

- Growth of Rigid-IBC Rental Pools

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Type A containers supplied 65.74% of 2025 demand, underscoring their value positioning across grain, cement and non-flammable chemical flows. Electrostatic-safe Type D bags, however, expand at 7.53% CAGR as lithium-ore refiners and pharmaceutical dryers specify non-grounded solutions to avert ignition risks.

Intensifying regulatory oversight and the absence of external grounding wires position Type D as the premium choice, enabling remote mines and offshore rigs to cut compliance complexity. High-tensile CROHMIQ fabrics have clocked more than 40 million safe trips, validating reliability in harsh environments and reinforcing future gains for the flexible intermediate bulk container market.

Baffle or Q-Bag variants held 34.12% share in 2025 owing to internal panels that stop bulging and unlock higher stack density, a decisive benefit for ship holds and urban DCs. U-Panel sacks track at 8.28% CAGR through 2031, supported by tight dimensional tolerances that mate smoothly with robotized filling frames.

Circular and 4-Panel designs maintain presence where maximum volume or precise discharge is required, yet continual lean-warehouse initiatives favor baffles. Automated facilities scanning pallets welcome the uniform footprint, sustaining the flexible intermediate bulk container market momentum for engineered geometries.

Geography Analysis

North America generated 38.25% of global revenue in 2025, underpinned by a mature chemical supply chain, high agricultural export volumes, and strict OSHA compliance that favors higher-margin certified bags. The region keeps a stable growth path as asset owners reinvest in smart-packaging retrofits and domestic shale-chemicals output holds firm.

Asia-Pacific records the most rapid 7.78% CAGR due to heavy investment in battery metal refining and broad-based manufacturing expansion. China's Baotou rare-earth hub, India's production-linked incentives and Southeast Asia's agribusiness exports converge to lift regional orders for conductive and high-stack designs. Local producers such as Bulkcorp International scale capacity and secure export contracts, testifying to competitive depth that fuels the flexible intermediate bulk container (FIBC) market.

Europe retains a significant share by pioneering recycled-material specifications under the Green Deal and by deploying reverse logistics that complement multi-trip models. South America benefits from soy, corn and lithium-brine exports that require food-grade or heavy-duty sacks, while the Middle East and Africa gain from petrochemical expansions and infrastructure megaprojects. Regional diversification therefore spreads opportunity across the flexible intermediate bulk container (FIBC) market landscape.

- Greif Inc.

- Amcor Plc

- LC Packaging International BV

- Thrace Group

- Rishi FIBC Solutions Pvt Ltd

- United Bags Inc.

- Bag Corp

- Bulk Lift International LLC

- Conitex Sonoco

- Intertape Polymer Group

- Emmbi Industries Ltd

- Schoeller Allibert Group BV

- BAG Supplies Canada Ltd

- Southern Packaging LP

- Plastipak Group

- FlexiTuff International Ltd

- Bulk Pack Exports Ltd

- J&HM Dickson Ltd

- Houston Bulk Bag Co.

- Jumbo Bag Corporation

- Mule Bag Co.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Food and agro commodities bulk export boom

- 4.2.2 Hazardous-chemical handling regulations boosting demand

- 4.2.3 E-commerce fulfilment shift to bulk secondary packaging

- 4.2.4 Smart-FIBC (IoT/RFID) rollout for real-time traceability

- 4.2.5 Paper and recycled-PP FIBC adoption under circular-economy mandates

- 4.2.6 Mining super-sack standardisation in lithium and rare-earth supply chains

- 4.3 Market Restraints

- 4.3.1 PP resin price volatility

- 4.3.2 Stringent static-dissipation certification costs

- 4.3.3 Ocean-freight container shortages disrupting FIBC supply

- 4.3.4 Growth of rigid-IBC rental pools cannibalising one-way FIBC demand

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Type

- 5.1.1 Type A

- 5.1.2 Type B

- 5.1.3 Type C

- 5.1.4 Type D

- 5.2 By Design Type

- 5.2.1 U-Panel

- 5.2.2 Baffle / Q-Bag

- 5.2.3 Circular

- 5.2.4 4-Panel

- 5.2.5 Other Designs

- 5.3 By End-user Industry

- 5.3.1 Food and Agriculture

- 5.3.2 Chemicals and Petrochemicals

- 5.3.3 Pharmaceuticals

- 5.3.4 Building and Construction

- 5.3.5 Mining and Minerals

- 5.3.6 Others

- 5.4 By Capacity

- 5.4.1 Up to 500 kg

- 5.4.2 500 - 1,000 kg

- 5.4.3 1,000 - 1,500 kg

- 5.4.4 Above 1,500 kg

- 5.5 By Material / Polymer Type

- 5.5.1 Virgin PP

- 5.5.2 Recycled-content PP

- 5.5.3 UV-stabilized PP

- 5.5.4 Paper-based Composite

- 5.5.5 Bio-based Polymer Blends

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Russia

- 5.6.2.7 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 Australia and New Zealand

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 Middle East

- 5.6.4.1.1 United Arab Emirates

- 5.6.4.1.2 Saudi Arabia

- 5.6.4.1.3 Turkey

- 5.6.4.1.4 Rest of Middle East

- 5.6.4.2 Africa

- 5.6.4.2.1 South Africa

- 5.6.4.2.2 Nigeria

- 5.6.4.2.3 Egypt

- 5.6.4.2.4 Rest of Africa

- 5.6.4.1 Middle East

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Greif Inc.

- 6.4.2 Amcor Plc

- 6.4.3 LC Packaging International BV

- 6.4.4 Thrace Group

- 6.4.5 Rishi FIBC Solutions Pvt Ltd

- 6.4.6 United Bags Inc.

- 6.4.7 Bag Corp

- 6.4.8 Bulk Lift International LLC

- 6.4.9 Conitex Sonoco

- 6.4.10 Intertape Polymer Group

- 6.4.11 Emmbi Industries Ltd

- 6.4.12 Schoeller Allibert Group BV

- 6.4.13 BAG Supplies Canada Ltd

- 6.4.14 Southern Packaging LP

- 6.4.15 Plastipak Group

- 6.4.16 FlexiTuff International Ltd

- 6.4.17 Bulk Pack Exports Ltd

- 6.4.18 J&HM Dickson Ltd

- 6.4.19 Houston Bulk Bag Co.

- 6.4.20 Jumbo Bag Corporation

- 6.4.21 Mule Bag Co.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

金屬中型散貨箱市場:按容器類型、容量、產品類型、最終用途產業和分銷管道分類-2026-2032年全球市場預測

金屬中型散貨箱市場:按容器類型、容量、產品類型、最終用途產業和分銷管道分類-2026-2032年全球市場預測 軟性中型散貨箱市場規模、佔有率、趨勢和預測:按產品、應用和地區分類,2026-2034年

軟性中型散貨箱市場規模、佔有率、趨勢和預測:按產品、應用和地區分類,2026-2034年 2026年全球乾散貨市場報告散裝卸料機市場:依產品類型、材料類型、運作模式及最終用戶產業分類-2026-2032年全球市場預測軟性中型散貨箱市場:依設計類型、材質、最終用途產業和分銷管道分類-2026-2032年全球市場預測

2026年全球乾散貨市場報告散裝卸料機市場:依產品類型、材料類型、運作模式及最終用戶產業分類-2026-2032年全球市場預測軟性中型散貨箱市場:依設計類型、材質、最終用途產業和分銷管道分類-2026-2032年全球市場預測 軟性中型集裝袋市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類,並提供2026-2034年的洞察和預測鈣塑膠週轉箱市場:按產品類型、材料、終端用戶產業和分銷管道分類 - 全球預測(2026-2032年)

軟性中型集裝袋市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類,並提供2026-2034年的洞察和預測鈣塑膠週轉箱市場:按產品類型、材料、終端用戶產業和分銷管道分類 - 全球預測(2026-2032年) 軟性中型散貨箱市場規模、佔有率和趨勢分析報告:按產品類型、最終用途、地區和細分市場預測,2025 年至 2033 年

軟性中型散貨箱市場規模、佔有率和趨勢分析報告:按產品類型、最終用途、地區和細分市場預測,2025 年至 2033 年 折疊式貨櫃屋市場:按材質、按應用、按尺寸、按設計/配置、按最終用戶、按價格分佈、按地區

折疊式貨櫃屋市場:按材質、按應用、按尺寸、按設計/配置、按最終用戶、按價格分佈、按地區 軟性中型散貨貨櫃 (FIBC) 市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測

軟性中型散貨貨櫃 (FIBC) 市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測