|

市場調查報告書

商品編碼

1523317

氨:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029)Ammonia - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

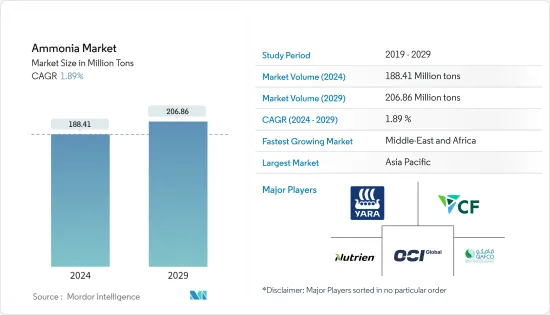

2024年氨市場規模預計為18,841萬噸,預計2029年將達到20686萬噸,在預測期內(2024-2029年)複合年成長率為1.89%。

COVID-19大流行期間,農業、紡織、採礦和其他最終用戶產業受到嚴重影響,對全球氨市場產生了負面影響。然而,行業內製藥業的成長正在改善,預計將有助於開拓市場。目前,合成氨市場已從疫情中恢復並呈現強勁成長。

主要亮點

- 短期內,化肥行業的大量使用以及火藥製造中氨的使用量增加預計將在預測期內推動市場成長。

- 然而,濃氨的有害影響可能會阻礙市場成長。

- 也就是說,使用氨作為冷媒以及擴大採用綠色氨可能會成為 2024 年至 2029 年的市場機會。

- 亞太地區佔據市場主導地位,預計 2024 年至 2029 年將維持最高複合年成長率。

氨市場趨勢

農業預計將主導市場

- 據世界經濟論壇稱,氨對於農業和全球食品供應鏈至關重要。氨也被認為是清潔氫的未來能源來源。

- 氨與大氣中的氮結合,利用吸收的氮產生關鍵的作物養分,然後用於生產氮肥。作為化學肥料生產的重要原料,氨可以改善作物健康,並長期維持和提高土壤肥力。

- 據聯合國稱,世界人口持續成長,預計2050年將達到90億。屆時,同樣土地面積的糧食生產需求預計將增加60%。實現糧食安全需要以負擔得起的價格獲得充足的營養食品。這可以透過最佳化肥料的使用來實現。

- 此外,美國是三大化肥原料的最大進口國之一。關鍵化肥原料的主要生產國包括中國、俄羅斯、加拿大和摩洛哥。 2023年3月,美國農業部(USDA)宣布前兩輪新津貼計劃,創新擴大47個州和兩個地區的國內化肥產能。美國農業部也宣布已收到來自350多家獨立公司的30億美元申請,突顯了國內化肥產業的強勁復甦。

- 此外,美國農業部也宣布提供 2,900 萬美元的初始津貼。這筆津貼將幫助獨立公司增加美國製造的化肥產量並促進良性競爭。

- 2023年3月,CBH集團宣布新的奎納納化肥工廠開業,這將為西澳糧農帶來顯著利益。該計劃標誌著CBH液體肥料業務的啟動,將增加其顆粒肥料產能15,000單位。新設施將擁有 32,000 噸尿素硝酸銨 (UAN) 儲存能力和 55,000 噸顆粒散裝肥料儲存能力。

- 因此,所有上述因素預計將增加2024-2029年農業產業對氨的需求。

亞太地區預計將主導市場

- 由於中國、印度和日本等國家的大量消費,亞太地區在氨市場佔據主導地位。

- 中國是世界上最大的氨生產國和消費國。根據美國地質調查局 (USGS) 的數據,該國 2023 年氨產量為 4,300 萬噸。由於化肥、紡織、製藥和採礦等農業產業擴大使用氨,該國對氨的需求不斷增加。

- 中國農業用地面積約佔全球整體面積的7%,養活了全球22%的人口。該國是各種作物的最大生產國,包括水稻、棉花和馬鈴薯。因此,大規模的農業活動增加了對用作肥料的氨的需求。

- 此外,印度是高度依賴農業的經濟體之一。超過55%的人口仍以農業為生。根據化肥部公告,2023會計年度尿素產量約2,800萬噸,而上年度為2,572萬噸。印度的尿素產量正在上升。

- 紡織業也受益於氨的能力。液態氨在鞣製過程中的使用非常廣泛,染料在紡織品染色中的使用也是如此。液氨在合成纖維的發展中扮演重要角色。氨溶液使織物染色幾乎可以達到任何顏色。

- 日本在紡織品生產方面擁有悠久的傳統,是最大的產業用紡織品製造商之一。為了在充滿中國和其他新興國家廉價紡織產品的全球市場中保持競爭力,日本紡織業正在轉型為專門生產科技和智慧紡織產品的產業。合成蜘蛛絲和穿戴式健康監測器等創新是日本紡織業差異化的努力之一。

- 另外,根據印度股權基金會的數據,2023年4月至2023年10月印度紡織品服裝出口(包括手工藝品)為211.5億美元。預計2025-26年將達1900億美元。

- 因此,所有上述因素都可能導致2024-2029年氨市場需求增加。

合成氨產業展望

氨市場高度分散。主要參與者(排名不分先後)包括 CF Industries Holdings Inc.、Yara、Nutrien Ltd.、OCI 和卡達化肥公司 (QAFCO)。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第1章簡介

- 調查先決條件

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 促進因素

- 在化肥產業的豐富應用

- 增加火藥生產中的使用

- 抑制因素

- 濃縮狀態有危險

- 價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 買方議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章市場區隔(市場規模)

- 類型

- 液體

- 氣體

- 最終用戶產業

- 農業

- 纖維

- 礦業

- 製藥

- 冷凍的

- 其他最終用戶產業(食品和飲料、橡膠、水處理、石油、紙漿和造紙業)

- 地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東/非洲

- 沙烏地阿拉伯

- 南非

- 其他中東/非洲

- 亞太地區

第6章 競爭狀況

- 併購、合資、聯盟、協議

- 市場佔有率(%)分析

- 主要企業策略

- 公司簡介

- BASF SE

- CF Industries Holdings Inc.

- Chambal Fertilisers and Chemicals Limited

- CSBP

- Eurochem Group

- Group DF(Ostchem)

- IFFCO

- Jsc Togliattiazot

- Koch Fertilizer LLC

- Nutrien Ltd

- OCI

- PT Pupuk Sriwidjaja Palembang(Pusri)

- Qatar Fertiliser Company(QAFCO)

- Rashtriya Chemicals And Fertilizers Limited

- SABIC

- Yara

第7章 市場機會及未來趨勢

- 使用氨作為冷媒

- 擴大綠色氨的採用

The Ammonia Market size is estimated at 188.41 Million tons in 2024, and is expected to reach 206.86 Million tons by 2029, growing at a CAGR of 1.89% during the forecast period (2024-2029).

During the COVID-19 pandemic, there was a negative impact on the ammonia market globally as agriculture, textile, mining, and other end-user industries were significantly affected. However, growth in the pharmaceutical segment is improving in the industry, and this is expected to assist in market development. Currently, the ammonia market has recovered from the pandemic and is growing significantly.

Key Highlights

- In the short term, abundant use in the fertilizer industry and ammonia's increasing usage for the production of explosives are projected to fuel the market's growth during the forecast period.

- However, the hazardous effects of ammonia in its concentrated form are likely to hinder the growth of the market.

- Nevertheless, the use of ammonia as a refrigerant and the growing adoption of green ammonia are likely to act as opportunities for the market between 2024 and 2029.

- Asia-Pacific is expected to dominate the market and is likely to witness the highest CAGR from 2024 to 2029.

Ammonia Market Trends

The Agriculture Industry is Expected to Dominate the Market

- According to the World Economic Forum, ammonia is vital in agriculture and the global food supply chain. Ammonia has also been recognized as a future energy source for clean hydrogen.

- Ammonia binds nitrogen from the atmosphere and produces the primary crop nutrients using the absorbed nitrogen, which is then used to produce nitrogen fertilizers. As an essential raw material for fertilizer production, ammonia improves crop health and, in the long run, maintains and even increases soil fertility.

- According to the United Nations, the world population continues to grow and will reach 9 billion by 2050. By then, on the same land area, the demand for food production is expected to increase by 60%. Achieving food security requires the availability of sufficient, nutritious food at affordable prices. This can be achieved through the use of optimized fertilizers.

- Additionally, the United States is among the top importers of the three major fertilizer ingredients. Major producers of the main fertilizer components include China, Russia, Canada, and Morocco. In March 2023, the US Department of Agriculture (USDA) announced the first two rounds of a new grant program to expand innovative production for domestic fertilizer production capacity in 47 states and two territories. The USDA further announced that it received USD 3 billion in applications from more than 350 independent companies, thus highlighting significant recovery in the country's fertilizer industry.

- Furthermore, the USDA also announced its first USD 29 million grant offering in the first round. The subsidy will help independent companies increase their production of American-made fertilizers and encourage healthy competition.

- In March 2023, CBH Group announced the opening of its new Kwinana Fertilizer Plant, which will benefit grain farmers in Western Australia significantly. The project marks the start of CBH's liquid fertilizer business, increasing its granular fertilizer production capacity by 15,000. The new facility has 32,000 tons of urea ammonium nitrate (UAN) storage capacity and 55,000 tons of granular bulk fertilizer.

- Therefore, all the aforementioned factors are expected to enhance the demand for ammonia from the agriculture industry between 2024 and 2029.

Asia-Pacific is Expected to Dominate the Market

- Asia-Pacific dominates the ammonia market owing to large consumption from countries such as China, India, and Japan.

- China is the largest producer and consumer of ammonia in the world. According to the US Geological Survey (USGS), the country produced 43 million metric tons of ammonia in 2023. The demand for ammonia in the country is rising due to increasing applications in the agriculture industry, such as fertilizers, textiles, pharmaceuticals, and mining.

- China accounts for approximately 7% of the overall agricultural acreage globally, thus feeding 22% of the world's population. The country is the largest producer of various crops, including rice, cotton, potatoes, and others. Hence, the demand for ammonia, which is used as a fertilizer, is rapidly increasing owing to the country's large-scale agricultural activities.

- Further, India is one of the economies that are largely dependent on agriculture. Agriculture is still the primary source of livelihood for more than 55% of the population. As per the Department of Fertilizers, in FY2023, about 28 million metric tons of urea were produced in India, which was 25.72 million metric tons in the previous year. Urea production in India presented an increasing trend.

- The textile industry also benefits from ammonia's capabilities. The use of liquid ammonia in tanning is widespread, as is the use of dyes in textile dyeing. Liquid ammonia plays an important role in the development of synthetic fabrics. The solution of ammonia enables fabric coloring to achieve almost any color.

- Japan has a long tradition in textile production and is one of the largest manufacturers of technical textiles. To remain competitive in the global market flooded with cheap textiles from China and other emerging countries, the Japanese textile industry is transforming into an industry that specializes in technological and smart textiles. Innovations such as synthetic spider silk and wearable health monitors are among the efforts to differentiate the Japanese textile industry.

- In addition, according to the Indian Brand Equity Foundation, India's textile and apparel exports (including handicrafts) from April 2023 to October 2023 stood at USD 21.15 billion. The industry is expected to reach USD 190 billion by 2025-26.

- Thus, all the above-mentioned factors are likely to provide the increasing demand for the ammonia market between 2024 and 2029.

Ammonia Industry Oveview

The ammonia market is highly fragmented in nature. The major players (not in any particular order) include CF Industries Holdings Inc., Yara, Nutrien Ltd, OCI, and Qatar Fertiliser Company (QAFCO).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Abundant Use in the Fertilizer Industry

- 4.1.2 Increasing Usage to Produce Explosives

- 4.2 Restraints

- 4.2.1 Hazardous Effects in its Concentrated Form

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Type

- 5.1.1 Liquid

- 5.1.2 Gas

- 5.2 End-user Industry

- 5.2.1 Agriculture

- 5.2.2 Textiles

- 5.2.3 Mining

- 5.2.4 Pharmaceutical

- 5.2.5 Refrigeration

- 5.2.6 Other End-user Industries (Food and Beverage, Rubber, Water Treatment, Petroleum, and Pulp and Paper Industries)

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%) Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 BASF SE

- 6.4.2 CF Industries Holdings Inc.

- 6.4.3 Chambal Fertilisers and Chemicals Limited

- 6.4.4 CSBP

- 6.4.5 Eurochem Group

- 6.4.6 Group DF (Ostchem)

- 6.4.7 IFFCO

- 6.4.8 Jsc Togliattiazot

- 6.4.9 Koch Fertilizer LLC

- 6.4.10 Nutrien Ltd

- 6.4.11 OCI

- 6.4.12 PT Pupuk Sriwidjaja Palembang (Pusri)

- 6.4.13 Qatar Fertiliser Company (QAFCO)

- 6.4.14 Rashtriya Chemicals And Fertilizers Limited

- 6.4.15 SABIC

- 6.4.16 Yara

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Use of Ammonia as a Refrigerant

- 7.2 Growing Adoption of Green Ammonia

氨市場:按產品類型、產量、純度、分銷管道、應用分類 - 2025-2030 年全球預測

氨市場:按產品類型、產量、純度、分銷管道、應用分類 - 2025-2030 年全球預測 藍氨市場 - 全球產業規模、佔有率、趨勢、機會和預測,按應用、技術、地區和競爭細分,2019-2029F

藍氨市場 - 全球產業規模、佔有率、趨勢、機會和預測,按應用、技術、地區和競爭細分,2019-2029F 氨市場規模、佔有率、趨勢分析報告:按產品、按應用、按地區、細分市場預測,2025-2030

氨市場規模、佔有率、趨勢分析報告:按產品、按應用、按地區、細分市場預測,2025-2030 全球氨市場:按類型(無水/水)、銷售管道(直接/間接)、最終用途行業(農業、紡織、冷凍、採礦、製藥)和地區 - 預測(截至 2029 年)

全球氨市場:按類型(無水/水)、銷售管道(直接/間接)、最終用途行業(農業、紡織、冷凍、採礦、製藥)和地區 - 預測(截至 2029 年) 氨市場:按類型、產品類型和最終用途分類:2024-2033 年全球機會分析和產業預測

氨市場:按類型、產品類型和最終用途分類:2024-2033 年全球機會分析和產業預測 全球氨市場研究報告 - 2024 年至 2032 年行業分析、規模、佔有率、成長、趨勢和預測

全球氨市場研究報告 - 2024 年至 2032 年行業分析、規模、佔有率、成長、趨勢和預測 藍氨市場 - 全球和區域分析:按應用、按產品、按地區 - 分析和預測(2024-2034)

藍氨市場 - 全球和區域分析:按應用、按產品、按地區 - 分析和預測(2024-2034) 2030 年藍氨市場預測:按製造流程、分銷管道、技術、應用、最終用戶和地區進行的全球分析

2030 年藍氨市場預測:按製造流程、分銷管道、技術、應用、最終用戶和地區進行的全球分析 氨市場:依產品類型、最終用戶、地區 - 全球產業分析、規模、佔有率、成長、趨勢、預測,2024-2032 年

氨市場:依產品類型、最終用戶、地區 - 全球產業分析、規模、佔有率、成長、趨勢、預測,2024-2032 年 2024 年藍氨世界市場報告

2024 年藍氨世界市場報告