|

市場調查報告書

商品編碼

1523335

校車:市場佔有率分析、產業趨勢、成長預測(2024-2029)School Bus - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

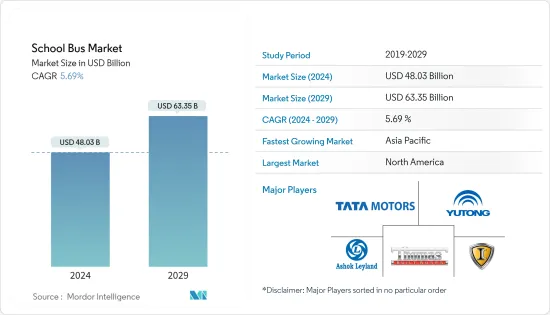

校車市場規模預計到 2024 年為 480.3 億美元,預計到 2029 年將達到 633.5 億美元,在預測期內(2024-2029 年)複合年成長率為 5.69%。

多種因素正在重塑學生交通,校車市場正在改變。對學生安全的日益關注推動了對技術先進公車的需求。此外,世界各國政府支持教育基礎設施的努力正在支持經濟成長。 2023年,按地區分類,北美將佔據壓倒性的市場佔有率,其次是歐洲、亞太地區、拉丁美洲和中東/非洲。

此外,快速的都市化和人口成長是需要創新解決方案來最佳化路線和緩解擁塞的關鍵因素。在世界向永續性轉變的推動下,對電動校車的需求不斷成長,正在為市場創造成長機會。人們對零排放電動公車的興趣也激增。用於路線最佳化的人工智慧和支援物聯網的維護監控等先進技術的整合為市場參與者提供了實現產品差異化的巨大機會。

此外,採用包括即時追蹤、維護計劃和資料分析在內的車隊管理解決方案已成為關鍵趨勢。這使得教育機構能夠最佳化業務、提高安全性並降低整體成本。然而,教育機構,特別是新興國家的教育機構,面臨預算限制,使得市場擴張成為一個問題。

校車製造商、技術提供者和教育機構之間的合作促進創新。這種合作夥伴關係對於滿足市場的多樣化需求並提供全面、整合的解決方案至關重要。

儘管仍存在許多挑戰,但校車市場預計將繼續其成長軌跡。

校車市場趨勢

由於電動校車銷量增加,預計未來幾年將出現成長

到 2035 年,政府對採用電動車和銷售電動車的獎勵、油價上漲、污染水平上升、環保意識增強、營業成本低於 ICE 出行以及歐洲、中國和印度等各個主要市場都將增加。到2020 年將禁止新銷售內燃機汽車,該技術在全球迅速流行。

全球超過 95% 的校車使用石化燃料,尤其是柴油。大量研究表明,吸入柴油引擎廢氣會導致呼吸道疾病,這種疾病在作為主要通勤者的兒童中普遍存在。如果我們用電動公車替換美國所有校車,我們每年將平均避免 530 萬噸溫室氣體排放。

電動公車零排放氣體,每年營運成本幾乎是柴油公車的一半。在中國深圳,電動公車的獎勵將擴大到包括校車,電動公車的使用量預計將增加。電動公車正在美國加州、紐約州、加拿大魁北克省進行測試和引進,預計將成為市場成長的驅動力。美國加州處於採用電動校車的最前線。例如,2022年11月,美國加州宣布將追加投資18億美元用於校車電氣化。該州已斥資 12 億美元對其校車車隊進行電氣化改造。

此外,隨著歐盟委員會宣布從2035年起歐洲將禁止銷售內燃機車輛,歐洲校車電動化也正在取得進展。

此外,校車市場的領導企業也積極響應這項需求,透過研究、併購、策略聯盟等方式,在電動客車領域取得競爭優勢。例如

2022年10月,比亞迪與洛斯奧利沃斯小學區簽署協議,使其成為美國第一個安裝100%零排放公車的學區。

2022年5月,總部位於加拿大不列顛哥倫比亞省溫哥華的Greenpower Motor宣布將在美國市場推出名為Nano BEAST(電池電動車學校運輸)的新型A型電池電動校車。

因此,校車電動化預計將推動校車市場的成長。

北美在校車市場開拓中發揮重要作用

北美擁有完善且廣泛的學校交通系統,許多學校和教育機構都嚴重依賴校車來運送學生。此外,該地區的人口密度和地理位置也大大增加了對校車的需求,特別是在步行到達學校不方便的郊區和農村地區。

北美的經濟繁榮也發揮著至關重要的作用,促進了對教育和相關基礎設施的大量投資,包括不斷更新和擴大我們的校車車隊。美國和加拿大對校車實施嚴格的安全法規,為具有先進安全功能的車輛創造了不斷成長的市場。例如

在美國,拜登政府推出了清潔校車(CSB)計劃,作為兩黨基礎設施法案的一部分。該舉措旨在用低排放或零排放氣體的新車型取代目前使用石化燃料的校車。重點是推廣環保且有助於學童健康的公車。

此外,美國環保署 (EPA) 也透過實施溫室氣體 (GHG) 第三階段計畫發揮了重要作用,該計畫實施了更嚴格的排放標準。此外,在北美,丙烷(也稱為液化天然氣 (LNG))也獎勵,並作為低排放氣體選項納入 CSB 計劃。

此外,政府資金和補貼進一步刺激市場,並為教育機構投資現代高效公車提供財政支持。此外,北美是技術進步的早期採用者,例如整合先進的安全功能和探索替代燃料,增加了整個校車市場的成長潛力。例如

2022年10月,戴姆勒卡車北美子公司ThomasBuiltBuses宣布交付美國印第安納州門羅縣公立學校第200輛Proterra動力Saf-T-LinerC2Jouley電池電動式校車。

亞太和歐洲校車市場的推動因素還包括兒童上下學安全交通途徑的需求不斷成長,以及中國和印度等市場家長為孩子提供校車服務的能力不斷增強。 、兒童入學率的增加以及主要客車製造商在這些市場的存在,預計將出現成長。

校車行業概況

校車市場適度整合。該市場的特點是擁有來自世界各地的主要校車製造商以及也向其他國家供貨的當地校車製造商。來自美國、中國和印度的製造商主要主導市場。這些參與者也參與合資、併購、新產品發布和產品開拓,以擴大其品牌組合併鞏固其市場地位。

主導全球市場的一些主要企業包括 ThomasBuilt Buses、宇通客車有限公司、塔塔汽車有限公司、Ashok Leyland Ltd 和 IC Bus。主要企業正在爭取大訂單並推出新產品,以確保其市場地位並保持市場領先地位。例如,2022年4月,領先的全電動式中型和重型卡車製造商Lion Electric公司宣佈為魁北克省訂單50輛全電動式LIONC級校車。 2022 年 9 月,倫敦德懷特學校與全球智慧公車運輸公司 Zeelo 合作推出電動公車服務。這項措施預計將使倫敦德懷特學校的碳排放每年減少 33%。

此外,2022 年 5 月,First Student 將從 Lion Electric 採購的電動巴士引入其網路。 First Student 的目標是最終在其網路上擁有 250 輛電動公車。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第1章簡介

- 調查先決條件

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 市場促進因素

- 全球政府支持教育基礎設施的努力推動成長

- 市場限制因素

- 有關排放氣體和安全的嚴格監管合規標準構成障礙

- 產業吸引力-波特五力分析

- 新進入者的威脅

- 買家/消費者的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭公司之間敵對關係的強度

第5章 市場區隔(金額單位)

- 依推進類型

- 內燃機(ICE)

- 壓縮天然氣(CNG)/液化天然氣(LNG)

- 電動和混合

- 按容量設計類型

- A型

- B型

- C型

- D型

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 北美其他地區

- 歐洲

- 德國

- 英國

- 法國

- 俄羅斯

- 西班牙

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太地區

- 世界其他地區

- 南美洲

- 中東/非洲

- 北美洲

第6章 競爭狀況

- 供應商市場佔有率

- 公司簡介

- Thomas Built Buses Inc.

- Collins Bus Corporation

- IC Bus(Navistar International Corporation)

- Blue Bird Corporation

- Lion Electric Company

- Yutong Buses Co. Ltd

- Anhui Ankai Automobile

- JCBL Limited

- Tata Motors

第7章 市場機會及未來趨勢

- 公車中人工智慧和物聯網技術的整合提供了未來的成長機會

第8章市場規模與單位銷售預測

第9章 各地方政府校車安全監理標準

The School Bus Market size is estimated at USD 48.03 billion in 2024, and is expected to reach USD 63.35 billion by 2029, growing at a CAGR of 5.69% during the forecast period (2024-2029).

The school bus market is transforming, driven by multiple factors reshaping student transportation. Growing concerns for student safety are fuelling the demand for technologically advanced buses. Additionally, government initiatives worldwide supporting education infrastructure are propelling growth. In 2023, the regional market share was dominated by North America, followed by Europe, Asia-Pacific, Latin America, and the Middle-East and Africa.

Furthermore, rapid urbanization and population growth are key drivers necessitating innovative solutions for route optimization and congestion reduction. The growing demand for electric school buses, driven by a global shift toward sustainability, presents growth opportunities for the market. There has also been a surge in interest in zero-emission, electric-powered buses. Integrating advanced technologies, including artificial intelligence for route optimization and IoT-enabled maintenance monitoring, presents a significant opportunity for market players to differentiate their offerings.

Moreover, the adoption of fleet management solutions, encompassing real-time tracking, maintenance scheduling, and data analytics, is emerging as a key trend. This allows educational institutions to optimize operations, enhance safety, and reduce overall costs. However, budget constraints in educational institutions, especially in developing regions, pose challenges for market expansion.

Collaboration between school bus manufacturers, technology providers, and educational institutions fosters innovation. These partnerships are essential in addressing the market's diverse needs and providing comprehensive, integrated solutions.

Despite all the challenges, the school bus market is expected to continue its growth trajectory in the coming years.

School Bus Market Trends

Growing Sales of Electric School Buses to Witness Growth in Coming Years

Electromobility is gaining pace across the world due to the government incentives provided to the adoption of electromobility and sales of electric vehicles, rising oil prices, increasing pollution levels, growing environmental consciousness, lower operating costs than ICE mobility, and announcements by various major markets like Europe, China, and India to ban new sales of IC engine vehicles by 2035.

More than 95% of school buses worldwide run on fossil fuels, especially diesel. Numerous studies show that inhaling diesel exhaust causes respiratory diseases, seen widely in children, who are the main commuters. Replacing all the school buses only in the United States with electric buses would avoid an average of 5.3 million tons of greenhouse gas emissions yearly.

Electric buses emit zero emissions, and their annual operating cost is almost half that of diesel buses. In Shenzhen, China, it is expected that the incentives for electric transit buses will also be extended to school buses, thus increasing their adoption. A few states in the United States, such as California and New York, and Quebec in Canada, are also testing and adopting electric buses, which is expected to drive the growth of the market. The state of California in the United States is at the forefront of adopting electric school buses. For instance, in November 2022, the state of California in the United States announced the investment of another USD 1.8 billion in the electrification of school buses. The state has spent USD 1.2 billion on the electrification of school buses so far.

Furthermore, the electrification of school buses in Europe is also rising due to the announcement of the European Commission to ban the sales of IC engine vehicles in Europe from 2035.

In addition, leading players in the school bus market are actively catering to this demand through research, mergers and acquisitions, strategic collaborations, etc, to gain a competitive edge in the electric bus segment. For instance,

In October 2022, BYD signed a deal with Los Olivos Elementary School District to create the first US school district with a 100% zero-emissions bus fleet.

In May 2022, Greenpower Motor Co., based in Vancouver, British Columbia, Canada, unveiled a new Type A battery electric school bus named Nano BEAST (Battery Electric Automotive School Transportation) for the US market.

Thus electric segment of school buses is anticipated to drive the growth of the school bus market.

North America to Play a Key Role in the Development of the School Bus Market

With a well-established and extensive school transportation system, North America boasts many schools and educational institutions that heavily rely on school buses for student transportation. Additionally, the region's population density and geographic factors contribute significantly to the demand for school buses, especially in suburban and rural areas where schools are not easily accessible by foot.

The economic prosperity of North America also plays a pivotal role, allowing substantial investments in education and related infrastructure, including the consistent update and expansion of school bus fleets. The United States and Canada enforce stringent safety regulations for school buses, fostering a market for vehicles with advanced safety features. For instance,

In the United States, the Biden administration has rolled out the 'Clean School Bus' (CSB) program as part of the Bipartisan Infrastructure Law. This initiative aims to replace current school buses running on fossil fuels with newer low- or zero-emission models. The key focus is on promoting buses that are environmentally friendly and contribute to the health of school children.

Furthermore, the Environmental Protection Agency (EPA) also plays a crucial role by implementing the Green House Gases (GHG) phase 3 program, which enforces stricter emission standards. Additionally, North America also provides incentives for propane, also known as liquefied natural gas (LNG), and it is included in the CSB program as a low-emission option.

Moreover, government funding and subsidies further fuel the market, providing financial support for educational institutions to invest in modern and efficient buses. Additionally, North America's early adoption of technological advancements, such as integrating advanced safety features and exploring alternative fuels, increases the overall growth potential of the school bus market. For instance,

In October 2022, Thomas Built Buses, a subsidiary of Daimler Truck North America, announced the delivery of the 200th Proterra Powered Saf -T-Liner C2 Jouley battery-electric school bus to Monroe County Public Schools in Indiana, United States.

The market for school buses in Asia-Pacific and Europe is also expected to grow rapidly due to the growing demand for safe and secure transportation for school-going children, rising disposable incomes of parents in markets like China and India who now can afford school bus services for their children, rising sales of electric school buses in Europe, increasing enrolment of children in schools, and the presence of large bus manufacturers in these markets.

School Bus Industry Overview

The school bus market is moderately consolidated. The market is characterized by the presence of major global and local school bus manufacturers who also cater to other countries. The United States, China, and India players mainly dominate the market. These players also engage in joint ventures, mergers and acquisitions, new product launches, and product development to expand their brand portfolios and cement their market positions.

Some of the major players dominating the global market are Thomas Built Buses, Yutong Bus Co., Tata Motors Ltd, Ashok Leyland Ltd, and IC Bus. Key players are securing large orders and launching new products to secure their market position and stay ahead of the market curve. For instance, in April 2022, Lion Electric Company, a leading all-electric medium and heavy truck manufacturer, announced that it had received an order for 50 all-electric school buses of the LIONC segment for the province of Quebec. In September 2022, Dwight School London introduced electric bus services in partnership with the global smart bus transport company Zeelo. The initiative is expected to reduce the carbon emissions of Dwight School London by as high as 33% annually.

Additionally, in May 2022, First Student introduced electric school buses in its network with the buses procured from Lion Electric Company. First Student aims to eventually induct 250 electric school buses into its network.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Government Initiatives Worldwide Supporting Education Infrastructure are Propelling Growth

- 4.2 Market Restraints

- 4.2.1 Stringent Regulatory Compliance Standards Related to Emissions and Safety Present Hurdles

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (VALUE IN USD BILLION)

- 5.1 By Propulsion Type

- 5.1.1 Internal Combustion Engine (ICE)

- 5.1.2 Compressed Natural Gas (CNG)/ Liquified Natural Gas (LNG)

- 5.1.3 Electric and Hybrid

- 5.2 By Capacity Design Type

- 5.2.1 Type A

- 5.2.2 Type B

- 5.2.3 Type C

- 5.2.4 Type D

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.1.4 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Russia

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 Rest of the World

- 5.3.4.1 South America

- 5.3.4.2 Middle-East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles*

- 6.2.1 Thomas Built Buses Inc.

- 6.2.2 Collins Bus Corporation

- 6.2.3 IC Bus (Navistar International Corporation)

- 6.2.4 Blue Bird Corporation

- 6.2.5 Lion Electric Company

- 6.2.6 Yutong Buses Co. Ltd

- 6.2.7 Anhui Ankai Automobile

- 6.2.8 JCBL Limited

- 6.2.9 Tata Motors

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Integration of AI and IoT enabled Technologies in Buses Presents Growth Opportunities for Future

8 MARKET SIZE AND FORECAST IN VOLUME

9 REGULATORY STANDARDS FOR SAFETY OF SCHOOL BUSES BY GOVERNMENTS IN DIFFERENT REGIONS

2024 年校車世界市場報告

2024 年校車世界市場報告 2024-2028年全球校車市場

2024-2028年全球校車市場 小型校車市場 - 按動力(柴油、混合動力、電動)、類別(A1 型、A2 型)、最終用途(學區、私人承包商、包機服務)和預測,2024 年 - 2032 年

小型校車市場 - 按動力(柴油、混合動力、電動)、類別(A1 型、A2 型)、最終用途(學區、私人承包商、包機服務)和預測,2024 年 - 2032 年 校車市場 - 按動力(柴油、混合動力、電動)、類別(A 型、B 型、C 型、D 型)、最終用途(學區、私人承包商、包機服務)和預測,2024 年 - 2032 年

校車市場 - 按動力(柴油、混合動力、電動)、類別(A 型、B 型、C 型、D 型)、最終用途(學區、私人承包商、包機服務)和預測,2024 年 - 2032 年 中型校車市場規模 - 按燃料(柴油、電動、混合動力)、按類別(A 型、B 型)、最終用戶(學區、私人承包商、包機服務)和預測,2024 年 - 2032 年

中型校車市場規模 - 按燃料(柴油、電動、混合動力)、按類別(A 型、B 型)、最終用戶(學區、私人承包商、包機服務)和預測,2024 年 - 2032 年 全球校車市場戰略機遇

全球校車市場戰略機遇