|

市場調查報告書

商品編碼

1523348

夾層玻璃:市場佔有率分析、產業趨勢/統計、成長預測(2024-2029)Laminated Glass - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

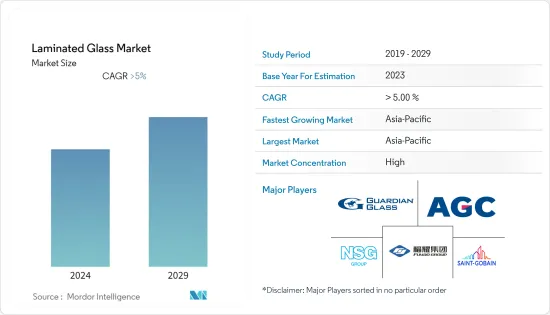

預計2024年夾層玻璃市場規模為206.2億美元,2029年將達268.3億美元,預測期間(2024-2029年)複合年成長率將超過5%。

COVID-19 對夾層玻璃市場產生了負面影響。與許多行業一樣,夾層玻璃市場在疫情初期也經歷了放緩。這是由於供應鏈中斷、勞動力短缺和建設活動減少所造成的。隨著封鎖措施的放鬆和建設活動的恢復,夾層玻璃的需求有所回升。因疫情而推遲或暫停的建設計劃已恢復,對玻璃產品的需求增加,包括用於住宅、商業和基礎設施計劃的夾層玻璃。

主要亮點

- 在建築領域擴大應用夾層玻璃以結構玻璃代替磚,以及技術進步是推動夾層玻璃市場的主要因素。

- 由於其多個製造步驟,夾層玻璃比其他普通窗玻璃更昂貴,這可能會阻礙市場成長。

- 此外,發展中國家的快速都市化以及汽車行業對夾層玻璃的需求不斷成長預計將為市場相關人員提供各種機會。

- 亞太地區呈現高成長率,中國、印度和日本等國家是夾層玻璃的重要消費者。

夾層玻璃市場趨勢

主導市場的汽車細分市場

- 夾層玻璃可減少進入機艙的噪音並提高乘客的舒適度。隨著消費者越來越重視舒適性和安靜的駕駛體驗,汽車製造商開始轉向夾層玻璃來提高隔音效果。

- 夾層玻璃可以加入具有紫外線防護功能的中間膜,可防止內部裝潢建材褪色並保護乘客免受有害紫外線的傷害。此功能在陽光強烈的區域至關重要。

- 電動車 (EV) 的日益普及為夾層玻璃製造商提供了機會。電動車製造商通常會優先考慮先進的功能和技術,使其產品脫穎而出,例如使用夾層玻璃來提高安全性、舒適性和能源效率。

- 根據國際能源總署(IEA)發布的預測,純電動車銷量將從 2021 年的約 460 萬輛增加到 2022 年的 730 萬輛。消費者對永續交通的興趣增加以及旨在減少直接空氣污染的政府立法等因素導致純電動車銷量增加。

- 此外,根據IEA公佈的預計,2022年,全球電動車銷量將達到約84.76%,進而帶動國內電動車產量的增加。這相當於約 900 萬台的銷售量,而同年透過國際貿易銷售的數量為 160 萬台。

- 根據經濟分析局(BEA)發布的最新預測,2023年美國乘用車年銷量將為312萬輛,高於2022年的286萬輛。

- 因此,由於上述因素,預計市場將在預測期內出現成長。

亞太地區主導市場

- 亞太地區正在經歷快速的人口成長和都市化,推動了建築和基礎設施發展的需求。夾層玻璃廣泛應用於亞太地區商業、住宅、機構建築的建築幕牆、門窗、天窗等。

- 該地區是世界上成長最快的經濟體之一,建設計劃投資巨大。夾層玻璃因其安全性和美觀性而受到建築師和建築商的青睞。上海、北京、新加坡和孟買等城市的高層建築、購物中心、飯店和多用戶住宅的建設正在推動夾層玻璃的需求。

- 此外,根據國家統計局最新發布的計算,2022年中國建築業產值將超過31兆元。

- 亞太地區是全球最大的汽車市場,在汽車生產和銷售方面處於領先地位。夾層玻璃主要用於汽車擋風玻璃,用於安全和降噪。該地區汽車工業的成長進一步推動了夾層玻璃的需求。

- 根據中國工業協會最新測算,截至2022年4月,中國商用車產量約21萬輛,乘用車產量約99.6萬輛。本月該產業總合生產了 120 萬台。

- 根據日本經濟產業省(METI)發布的估計,2022年日本汽車工業的汽車產值將約為19.29兆日圓(1,300億美元),而前一年約為17.65兆日圓。億美元)。

- 所有這些預計都將對該地區未來幾年的市場成長產生重大影響。

夾層玻璃產業概況

夾層玻璃市場部分整合。市場的主要企業包括(排名不分先後)聖戈班、AGC Glass Europe、Guardian Industries Holdings、日本板硝子和福耀玻璃工業集團。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 調查先決條件

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 促進因素

- 用結構玻璃代替磚的應用越來越多

- 技術進步

- 抑制因素

- 製造成本高

- 其他阻礙因素

- 價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 買方議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章 市場區隔(以金額為準的市場規模)

- 按類型

- 聚乙烯丁醛(PVB)

- Sentry Glass Plus (新加坡)

- 乙烯醋酸乙烯(EVA)

- 其他(離子塑膠、防火夾層玻璃)

- 按最終用戶產業

- 車

- 建築/施工

- 電子產品

- 其他(安全/國防)

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 泰國

- 馬來西亞

- 印尼

- 越南

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 土耳其

- 俄羅斯

- 北歐國家

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 哥倫比亞

- 南美洲其他地區

- 中東/非洲

- 沙烏地阿拉伯

- 南非

- 奈及利亞

- 埃及

- 卡達

- 阿拉伯聯合大公國

- 其他中東/非洲

- 亞太地區

第6章 競爭狀況

- 併購、合資、聯盟、協議

- 市場佔有率(%)/排名分析

- 主要企業策略

- 公司簡介

- AGC Inc.

- Asahi India Glass Limited

- CARDINAL GLASS INDUSTRIES INC.

- Central Glass Co. Ltd

- Fuyao Group

- GSC GLASS LTD

- Guardian Industries Holdings

- Nippon Sheet Glass Co. Ltd

- Saint-Gobain

- Stevenage Glass Company Ltd

- Taiwan Glass Ind. Corp.

第7章 市場機會及未來趨勢

The Laminated Glass Market size is estimated at USD 20.62 billion in 2024, and is expected to reach USD 26.83 billion by 2029, growing at a CAGR of greater than 5% during the forecast period (2024-2029).

COVID-19 had a detrimental effect on the laminated glass market. Like many industries, the laminated glass market experienced a slowdown in the early stages of the pandemic. This occurred due to disruptions in supply chains, labor shortages, and decreased construction activity. As lockdown measures eased and construction activities resumed, the demand for laminated glass picked up. Construction projects that were delayed or put on hold due to the pandemic restarted, driving demand for glass products, including laminated glass, for use in residential, commercial, and infrastructure projects.

Key Highlights

- The increasing application of laminated glass in replacing bricks with structural glass in the construction sector and the advancement in technology are the key factors that are driving the laminated glass market.

- Laminated glass is more expensive than other regular windows because of the number of steps taken to produce it, which is likely to hamper market growth.

- Also, the rapid urbanization in developing countries and the rising demand for laminated glasses from the automotive sector are expected to provide various opportunities to market players.

- Due to the fact that countries like China, India, and Japan are critical consumers of laminated glass, Asia-Pacific has a high growth rate.

Laminated Glass Market Trends

Automotive Segment to Dominate the Market

- Laminated glass helps reduce noise transmission into the vehicle cabin, enhancing comfort for passengers. As consumers increasingly prioritize comfort and a quieter driving experience, automakers utilize laminated glass to improve acoustic insulation.

- Laminated glass can incorporate interlayers that provide UV protection, reducing the fading of interior materials and protecting occupants from harmful UV radiation. This feature is essential for regions with intense sunlight exposure.

- The increasing popularity of electric vehicles (EVs) offers opportunities for laminated glass manufacturers. EV manufacturers often prioritize advanced features and technologies to differentiate their products, including the use of laminated glass for safety, comfort, and energy efficiency.

- According to the estimate released by the International Energy Agency (IEA), in 2022, sales of battery electric vehicles reached 7.3 million, up from around 4.6 million in 2021. Factors such as increased consumer interest in sustainable transport and governmental legislation that aims to reduce direct air pollution have led to a rise in the sale of BEVs.

- Further, according to the estimate released by the IEA, in 2022, around 84.76% of global electric vehicles were sold, resulting from the domestic production of these vehicles. This represented nearly 9 million sales, compared to 1.6 million units sold from international trade that year.

- According to the latest estimate published by the Bureau of Economic Analysis (BEA), the annual passenger car sales in the United States were 3.12 million units in 2023, which increased from 2.86 million units in 2022.

- Consequently, the market is expected to register growth during the forecast period due to the abovementioned factors.

Asia-Pacific to Dominate the Market

- Asia-Pacific has experienced rapid population growth and urbanization, driving demand for construction and infrastructure development. Laminated glass is widely used in building facades, windows, doors, and skylights in commercial, residential, and institutional buildings across the region.

- It is home to some of the world's fastest-growing economies, leading to significant investments in construction projects. Laminated glass is a preferred choice for architects and builders due to its safety, security, and aesthetic properties. The construction of skyscrapers, shopping malls, hotels, and residential complexes in cities like Shanghai, Beijing, Singapore, and Mumbai fuels the demand for laminated glass.

- Furthermore, according to the latest estimate published by the National Bureau of Statistics of China, in 2022, the construction industry in China generated an output of over CNY 31 trillion.

- Asia-Pacific is the largest automotive market globally, leading in automobile production and sales. Laminated glass is majorly used in automotive windshields for safety and noise reduction. The region's automotive industry's growth further contributes to the demand for laminated glass.

- According to the latest estimate published by the China Association of Automobile Manufacturers (CAAM), China produced approximately 210,000 commercial vehicles and 996,000 passenger cars as of April 2022. The industry produced a total of 1.2 million vehicles during the month.

- According to the estimate released by the Ministry for Economy, Trade, and Industry (Meti), Japan, in 2022, the production value of motor vehicles by the automotive industry in Japan was approximately JPY 19.29 trillion (USD 0.13 trillion), increasing from around JPY 17.65 trillion (USD 0.12 trillion) in the previous year.

- In the coming years, all of this is expected to have a significant impact on the growth of the region's market.

Laminated Glass Industry Overview

The laminated glass market is partially consolidated in nature. Some of the major players in the market (not in any particular order) include Saint-Gobain, AGC Glass Europe, Guardian Industries Holdings, Nippon Sheet Glass Co. Ltd, and Fuyao Glass Industry Group Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Application in Replacement of Bricks with Structural Glass

- 4.1.2 Advancements in Technology

- 4.2 Restraints

- 4.2.1 High Cost of Manufacturing

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 By Type

- 5.1.1 Polyvinyl Butyral (PVB)

- 5.1.2 Sentryglas Plus (SGP)

- 5.1.3 Ethylene-vinyl Acetate (EVA)

- 5.1.4 Other Types (Ionoplast, Fire-Rated Laminated Glass)

- 5.2 By End-user Industry

- 5.2.1 Automotive

- 5.2.2 Building and Construction

- 5.2.3 Electronics

- 5.2.4 Other End-user Industries (Security and Defense)

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Thailand

- 5.3.1.6 Malaysia

- 5.3.1.7 Indonesia

- 5.3.1.8 Vietnam

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Turkey

- 5.3.3.7 Russia

- 5.3.3.8 NORDIC Countries

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Nigeria

- 5.3.5.4 Egypt

- 5.3.5.5 Qatar

- 5.3.5.6 United Arab Emirates

- 5.3.5.7 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/ Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 AGC Inc.

- 6.4.2 Asahi India Glass Limited

- 6.4.3 CARDINAL GLASS INDUSTRIES INC.

- 6.4.4 Central Glass Co. Ltd

- 6.4.5 Fuyao Group

- 6.4.6 GSC GLASS LTD

- 6.4.7 Guardian Industries Holdings

- 6.4.8 Nippon Sheet Glass Co. Ltd

- 6.4.9 Saint-Gobain

- 6.4.10 Stevenage Glass Company Ltd

- 6.4.11 Taiwan Glass Ind. Corp.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Urbanization in Developing Countries

- 7.2 Rising Demand from the Automotive Sector

2025 年全球層壓玻璃市場報告

2025 年全球層壓玻璃市場報告 夾層玻璃市場:按中間膜、最終用途產業分類 - 2025-2030 年全球預測

夾層玻璃市場:按中間膜、最終用途產業分類 - 2025-2030 年全球預測 雙層玻璃市場:按材料、墊片厚度、應用、最終用途分類 - 2025-2030 年全球預測

雙層玻璃市場:按材料、墊片厚度、應用、最終用途分類 - 2025-2030 年全球預測 全球嵌裝玻璃市場:按類型、產品、應用和最終用戶分類 - 預測 2025-2030 年

全球嵌裝玻璃市場:按類型、產品、應用和最終用戶分類 - 預測 2025-2030 年 商用雙層玻璃市場:依產品類型、最終用戶產業、隔熱類型、玻璃類型、銷售管道- 2025-2030 年全球預測

商用雙層玻璃市場:依產品類型、最終用戶產業、隔熱類型、玻璃類型、銷售管道- 2025-2030 年全球預測 夾層玻璃市場- 按類型(透明玻璃、有色玻璃、反射玻璃)、按中間層(聚乙烯醇縮丁醛、Sentryglas plus、乙烯-醋酸乙烯酯)、按應用、最終用途行業及預測,2024 - 2032年

夾層玻璃市場- 按類型(透明玻璃、有色玻璃、反射玻璃)、按中間層(聚乙烯醇縮丁醛、Sentryglas plus、乙烯-醋酸乙烯酯)、按應用、最終用途行業及預測,2024 - 2032年 夾層玻璃市場 - 全球產業規模、佔有率、趨勢、機會和預測(按材料類型、按應用、最終用途產業、地區、競爭預測和機會細分,2018-2028 年)

夾層玻璃市場 - 全球產業規模、佔有率、趨勢、機會和預測(按材料類型、按應用、最終用途產業、地區、競爭預測和機會細分,2018-2028 年) 雙層中空玻璃市場(材料:玻璃、邊框和墊片、密封膠及其他;厚度:小於 10 毫米、10 毫米至 12 毫米和大於 12 毫米) - 2023-2031 年全球行業分析、規模、佔有率、成長、趨勢和預測

雙層中空玻璃市場(材料:玻璃、邊框和墊片、密封膠及其他;厚度:小於 10 毫米、10 毫米至 12 毫米和大於 12 毫米) - 2023-2031 年全球行業分析、規模、佔有率、成長、趨勢和預測![夾層玻璃市場:趨勢、機遇、競爭對手分析 [2023-2028]](/sample/img/cover/42/1284990.png) 夾層玻璃市場:趨勢、機遇、競爭對手分析 [2023-2028]

夾層玻璃市場:趨勢、機遇、競爭對手分析 [2023-2028]