|

市場調查報告書

商品編碼

1523350

全球高溫塗料市場:市場佔有率分析、產業趨勢/統計、成長預測(2024-2029)High Temperature Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

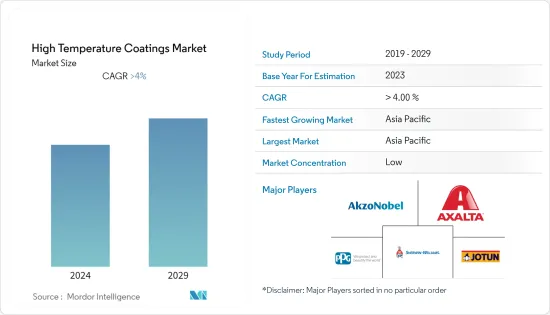

預計2024年全球高溫塗料市場規模將達到37.1億美元,並在2024-2029年預測期內以超過4%的複合年成長率成長,到2029年將達到47.3億美元。

高溫塗料市場受到 COVID-19 大流行的負面影響。多個國家實施了全國封鎖,嚴格的社會疏散措施對建築、汽車和石化行業產生了不利影響。然而,在COVID-19大流行之後,建築建設活動和汽車製造廠恢復營運,導致高溫塗料市場復甦。

主要亮點

- 石化產業需求的增加以及對無溶劑高溫塗料偏好的改變預計將推動目前的研究市場。

- 另一方面,嚴格的環境法規和原料價格的波動預計將阻礙市場成長。

- 新興經濟體和基礎設施計劃的成長預計將在預測期內為市場創造機會。

- 預計亞太地區將主導市場。由於中國、印度和日本等國家消費量的增加,預計在預測期內複合年成長率將保持最高。

高溫塗料市場趨勢

石化產業需求不斷成長

- 石化產業不斷面臨侵蝕、腐蝕、化學侵蝕、磨損和機械損壞等問題,這些問題會導致基礎設施和設備隨著時間的劣化。

- 高溫塗層設計可承受 150°C 至 800°C 的溫度。它有助於最大限度地減少熱損失、抑制隔熱材料下的腐蝕、保持熱疲勞並保持效率。

- 能源和石化行業由於使用熱處理設備、分離器、熔爐和加熱材料的運輸而成為重要的消費者。高溫塗層有助於減少能量損失並減少非生產時間。

- 在亞太地區,由於新石化廠的建設,耐熱塗料的需求不斷增加。例如,中國計畫並宣佈興建305座石化工廠,到2030年總產能約1.524億噸。此外,同期資本支出預計將達到915億美元。

- 同樣,在北美,由於各個最終用戶產業對石化產品的需求增加,石化產業錄得顯著成長。陸上/海上探勘和生產活動的成長、精製和石化廠的高速成長以及其他化工廠(包括製藥廠)的建設和現代化推動了該地區對高溫塗料的需求。

- 此外,根據VCI統計,石化產品出口額不斷增加,帶動耐熱塗料市場。 2022年,中國石化產品出口額達673億美元,成為全球第一大出口國。美國和荷蘭分居第二和第三位,出口額分別為438億美元和364億美元。

- 由於上述因素,石化產業對高溫塗料的需求預計在預測期內將會增加。

亞太地區主導市場

- 亞太地區是最大且成長最快的高溫塗料市場。高經濟成長率、製造業成長、低成本勞動力、外國投資增加、終端用戶產業需求增加以及全球生產從已開發國家轉移到新興國家是推動該地區市場成長的主要因素。

- 該地區建築、石化和汽車行業的不斷成長進一步推動了該地區對高溫塗料的需求。在汽車和石化工業中,高溫塗料被用作保護塗層。

- 中國是亞太地區最大的建築市場之一。根據中國國家統計局的數據,2022年中國建築產值將增加至31.2兆元(4.34兆美元),而2021年將達到29.31兆元人民幣(4.84兆美元)。此外,用作投資房產的住宅的需求正在增加。預計到2030年,中國的建築支出將達到約13兆美元,高溫塗料市場前景看好。

- 中國是該地區最大的汽車製造商。根據OICA(國際汽車製造商組織)預計,2022年中國汽車產量將達2,702萬輛,與前一年同期比較同期成長3%。

- 印度成為該地區第二大汽車製造商。根據OICA的數據,2022年汽車產量達到545萬輛,比2021年的439萬輛增加24%。因此,汽車產量的增加預計將提振汽車塗料的需求並帶動高溫塗料市場。

- 同樣,在印度,石化產業近年來也經歷了顯著成長。據化學和石化部稱,印度化學和石化(CPC)產業預計到2022年將達到1,780億美元,2025年將達到3,000億美元。因此,化學和石化行業的成長預計將推動該國對高溫塗料的需求。

- 由於上述因素,亞太地區預計對高溫塗料的需求在預測期內將大幅成長。

高溫塗料產業概況

高溫塗料市場分為幾個部分。該市場的主要企業包括(排名不分先後)Akzo Nobel NV、Axalta Coating Systems、Jotun、PPG Industries Inc. 和 The Sherwin-Williams Company。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第1章簡介

- 調查先決條件

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 促進因素

- 石化產業需求不斷成長

- 改變對無溶劑高溫塗料的偏好

- 其他司機

- 抑制因素

- 嚴格的環境法規

- 原物料價格波動

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 買方議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章市場區隔(市場規模:金額)

- 類型

- 環氧樹脂

- 矽膠

- 聚酯纖維

- 丙烯酸纖維

- 醇酸

- 其他類型(聚氨酯、乙烯基酯等)

- 科技

- 水性的

- 溶劑型

- 粉末

- 最終用戶產業

- 航太/國防

- 車

- 石油化學

- 建築/施工

- 其他最終用戶產業(船舶、水處理等)

- 地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 馬來西亞

- 泰國

- 印尼

- 越南

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 義大利

- 法國

- 西班牙

- 北歐的

- 土耳其

- 俄羅斯

- 歐洲其他地區

- 南美洲

- 巴西

- 阿根廷

- 哥倫比亞

- 南美洲其他地區

- 中東/非洲

- 奈及利亞

- 卡達

- 埃及

- UAE

- 沙烏地阿拉伯

- 南非

- 其他中東/非洲

- 亞太地區

第6章 競爭狀況

- 併購、合資、聯盟、協議

- 市場佔有率(%)/排名分析

- 主要企業策略

- 公司簡介

- Akzo Nobel NV

- Aremco

- Axalta Coating Systems

- Carboline

- Chemcote PTY LTD

- GENERAL MAGNAPLATE CORPORATION

- Hempel A/S

- Jotun

- PPG Industries Inc.

- The Sherwin-Williams Company

- Valspar

第7章 市場機會及未來趨勢

- 新興經濟體的成長和基礎建設計劃

- 其他機會

The High Temperature Coatings Market size is estimated at USD 3.71 billion in 2024, and is expected to reach USD 4.73 billion by 2029, growing at a CAGR of greater than 4% during the forecast period (2024-2029).

The high temperature coatings market had negatively affected by the COVID-19 pandemic. Due to nationwide lockdowns in several countries, strict social distancing measures negatively affected the building and construction, automotive, and petrochemical industries. However, post-COVID pandemic, the building construction activities and automotive manufacturing plants resumed their operations, which helped to revive the market for high-temperature coatings.

Key Highlights

- The growing demand from petrochemical industries and the shift in preference towards solvent-free high-temperature coatings is expected to drive the current studied market.

- On the flip side, the stringent environmental regulations and the volatility in raw material prices are expected to hinder the growth of the market.

- The growth of emerging economies and infrastructure projects is expected to create opportunities for the market during the forecast period.

- The Asia-Pacific region is expected to dominate the market. It is also expected to register the highest CAGR during the forecast period owing to the increasing consumption from countries such as China, India, and Japan.

High Temperature Coatings Market Trends

Growing Demand from Petrochemical Industry

- The petrochemical industry is constantly faced with problems like erosion, corrosion, chemical attack, wear, abrasion, and mechanical damage, which cause deterioration of infrastructure and equipment over time.

- High-temperature coatings are designed to withstand temperatures from 150°C to 800°C. It helps minimize heat losses, keep corrosion under insulation in check, maintain thermal fatigue, and maintain efficiency.

- Energy and Petrochemical industries are among the critical consumers owing to the use of heater-treaters, separators, furnaces, and the transport of heated materials. High-temperature coatings help decrease energy losses and reduce non-productive time.

- In the Asia-Pacific region, the demand for heat-resistant coatings is increasing with the development of new petrochemical plants. For instance, China has 305 planned and announced petrochemical plants, with a total capacity of about 152.4 mtpa by 2030. China is also expected to reach a capital expenditure of USD 91.5 billion over the same period.

- Similarly, in North America, the petrochemical industry registered a significant growth rate due to rising demand for petrochemicals from various end-user industries. The growth in onshore/offshore exploration and production activities, high growth observed in oil refineries and petrochemical plants, and the building and modernization of other chemical plants (which include pharmaceuticals) boosted the demand for high-temperature coatings in the region.

- Furthurmore according to VCI statistics the export value of petrochemicals is rising therbey driving the market for heat resistant coatings. China exported over USD 67.3 billion worth of petrochemicals in 2022, becoming the world's major exporting country. The United States and the Netherlands followed second and third, with an export value of USD 43.8 billion and USD 36.4 billion.

- Owing to the above-mentioned factors, the demand for high-temperature coatings from the petrochemical industry is expected to increase over the forecast period.

Asia-Pacific Region to Dominate the Market

- The Asia-Pacific region represents the largest and fastest-growing market for high-temperature coatings. High economic growth rate, growing manufacturing industries, low-cost labor, increasing foreign investments, increasing demand from end-user industries, and the global shift in production from developed countries to emerging countries in the region are some of the major factors leading to the growth of the market in the region.

- The escalating growth of the construction, petrochemical, and automotive industries in the region is further driving the demand for high-temperature coatings in the region. In the automotive and petrochemical industries the high temperature coatings are used as protective coatings.

- China is one of the largest construction markets in the Asia-Pacific region. According to the National Bureau of Statistics of China, the output value of construction works in the country accounted for CNY 31.2 trillion (USD 4.34 trillion) in 2022, as compared to CNY 29.31 trillion (USD 4.084 trillion) in 2021. Additionally, demand is increased for residences that are used as investment properties. China is expected to spend nearly USD 13 trillion on buildings by 2030, creating a positive market outlook for high temperature coatings.

- China is the largest automotive vehicle manufacturer in the region. According to OICA (The Organisation Internationale des Constructeurs d'Automobiles), automotive vehicle production in China reached a total of 27.02 million units in 2022, an increase of 3% over the previous year for the same period.

- India has become the second-largest automotive vehicle manufacturer in the region. According to OICA, the total production volume of automotive vehicles reached 5.45 million units in 2022, indicating a growth of 24% as compared to 4.39 million units registered in 2021. Thus, the increase in the production of automotive vehicles is expected to drive the demand for automotive coatings, thereby driving the market for high temperature coatings.

- Similarly in India the petrochemical industry registered a significant growth in recent years. According to the Department of Chemicals & Petrochemicals, India's chemical and petrochemical (CPC) industry registered USD 178 billion in 2022, and it is expected to reach USD 300 billion by 2025. Thus the growth in chemical and petrochemical industries is expected to drive the demand for high temperature coatings in the country.

- Owing to the above mentioned factors, the demand for high-temperature coatings in Asia-Pacific region is expected to grow considerably over the forecast period.

High Temperature Coatings Industry Overview

The high-temperature coatings market is partially fragmented in nature. Some of the major players in the market (not in any particular order) include Akzo Nobel N.V., Axalta Coating Systems, Jotun, PPG Industries Inc., and The Sherwin-Williams Company, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Demand from Petrochemical Industry

- 4.1.2 Shift in Preference Toward Solvent-Free High Temperature Coatings

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Stringent Environmental Regulations

- 4.2.2 Volatility in Raw Material Prices

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Type

- 5.1.1 Epoxy

- 5.1.2 Silicone

- 5.1.3 Polyester

- 5.1.4 Acrylic

- 5.1.5 Alkyd

- 5.1.6 Other Types (Polyurethane, Vinyl Ester, etc.)

- 5.2 Technology

- 5.2.1 Water based

- 5.2.2 Solvent based

- 5.2.3 Powder

- 5.3 End-user Industry

- 5.3.1 Aerospace and Defense

- 5.3.2 Automotive

- 5.3.3 Petrochemical

- 5.3.4 Building and Construction

- 5.3.5 Other End-user Industries (Marine, Water Treatment, etc.)

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Malaysia

- 5.4.1.6 Thailand

- 5.4.1.7 Indonesia

- 5.4.1.8 Vietnam

- 5.4.1.9 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 Italy

- 5.4.3.4 France

- 5.4.3.5 Spain

- 5.4.3.6 NORDIC

- 5.4.3.7 Turkey

- 5.4.3.8 Russia

- 5.4.3.9 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Nigeria

- 5.4.5.2 Qatar

- 5.4.5.3 Egypt

- 5.4.5.4 UAE

- 5.4.5.5 Saudi Arabia

- 5.4.5.6 South Africa

- 5.4.5.7 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Akzo Nobel N.V.

- 6.4.2 Aremco

- 6.4.3 Axalta Coating Systems

- 6.4.4 Carboline

- 6.4.5 Chemcote PTY LTD

- 6.4.6 GENERAL MAGNAPLATE CORPORATION

- 6.4.7 Hempel A/S

- 6.4.8 Jotun

- 6.4.9 PPG Industries Inc.

- 6.4.10 The Sherwin-Williams Company

- 6.4.11 Valspar

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 The Growth of Emerging Economies and Infrastructure Projects

- 7.2 Other Opportunities