|

市場調查報告書

商品編碼

1523352

全球汽車印刷電路基板(PCB)市場:市場佔有率分析、產業趨勢/統計、成長預測(2024-2029)Automotive Printed Circuit Board (PCB) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

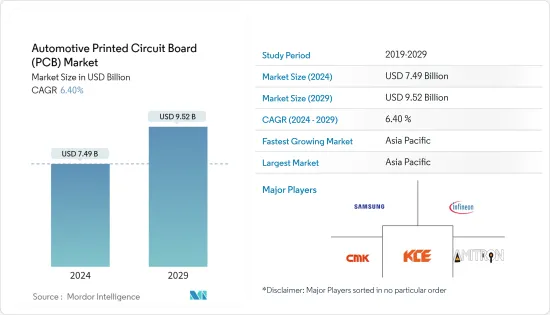

2024年全球汽車印刷電路基板(PCB)市場規模將達到74.9億美元,2024-2029年預測期間複合年成長率為6.40%,預計2029年將達到95.2億美元。

汽車電氣系統使用的增加、對汽車駕駛員舒適性和安全性的需求不斷成長以及汽車行業的顯著擴張預計將成為預測期內市場成長的主要驅動力。

此外,隨著汽車自動化的廣泛普及以及全球聯網汽車需求的不斷成長,汽車 PCB 的需求預計在預測期內將大幅成長。

人工智慧 (AI)、雲端和物聯網設備的整合改善和增強了車輛和車輛間通訊。情緒識別、行為識別和個人助理等人工智慧技術正在推動安全性和車輛即市場等場景的成長,這反過來又可能推動對汽車電力電子元件的需求。這樣,就進一步促進了目標市場的發展。

從長遠來看,工業巨頭加大研發投入、電動和混合動力汽車銷量增加以及聯網汽車需求上升將創造汽車和交通產業的需求,汽車印刷基板的銷售將快速成長。

市場主要企業正在擴大產能,以滿足汽車印刷電路基板日益成長的需求。

Denkai America Inc.於2022年7月宣布,將投資4.3億美元在喬治亞奧古斯塔建立北美總部和製造工廠。該製造工廠將包括一條價值 1.5 億美元的生產線,用於生產電動車電池用 ED 銅箔。 2022年3月,Ather Energy與富士康科技集團子公司Bharat FIH簽署協議,由Bharat FIH在印度開發製造Ather Energy的電氣元件,包括印刷基板(PCB)。

汽車印刷基板(PCB)市場趨勢

電動車銷量的擴大推動市場成長

中國、印度和歐洲等許多汽車大國的政府都致力於提高電動車的銷量,以實現 2015 年《巴黎氣候變遷協議》的碳減排目標,這些市場都在採用電動車。獎勵和政策不斷推動。

儘管去年整體疲軟,但2022年全球整體電動車銷量將比2021年成長約60%,首次超過1,000萬輛。因此,根據國際能源總署 (IEA) 的數據,到 2022 年,全球購買的七分之一的乘用車將是電動車。然而,到 2023 年,電動車的表現可能會繼續跑贏大盤。 2023年第一季電動車銷量超過230萬輛,較去年同期成長約25%。 2023年,預計電動車銷量將達到1,400萬輛,較去年同期成長35%。

亞太和歐洲多個國家已宣布計劃在 2040 年禁止銷售新型內燃機汽車,轉而電池式電動車。油價上漲、污染程度上升、環保意識不斷增強,以及政府為推廣電動車所採取的眾多激勵措施,正在導致全球電動車銷售的健康成長。

在中國,2022年電動車銷量達366萬輛(截至9月),與前一年同期比較成長119%。在印度,2022年電動車銷量達390,399輛(截至7月),與前一年同期比較同期成長333%。

電動渦輪增壓器(也稱為電動輔助渦輪增壓器或電子渦輪增壓器)的出現是最近的趨勢。這些系統利用馬達來提高渦輪增壓器的性能,並透過改善瞬態響應來減少渦輪遲滯。

汽車 PCB 控制電池的所有功能,電池是電動車的核心零件。由此可見,電動車銷量的大幅成長已成為全球汽車PCB產業成長的巨大推動力。

對乘用車的需求不斷成長以及人們對電動車的意識不斷增強,導致主要企業提高了其設備的產能。例如

2023年5月,現代汽車印度有限公司宣布將投資2,000億印度盧比加強在印度各地的電動車製造設施。

電動車的上升趨勢預計將推動未來市場的成長。

預計亞太地區在預測期內將大幅成長

亞太地區是最主要的市場,其次是北美和歐洲。

亞太地區是世界上最大的汽車生產國的所在地:印度、中國、日本和韓國。印度和中國是全球最大的電動車市場之一,佔全球電動車銷量的近60%,使亞太地區成為汽車印刷線路板最賺錢的市場。該地區的大多數汽車中都有汽車印刷電路基板,因為它們控制著電動車的基本功能。

中國是全球最大的電動車生產國和消費國。國內需求受到銷售目標、有利的立法和城市空氣品質目標的支持。

中國對電動和混合動力汽車製造商實施配額,要求其銷量至少佔新車銷量的 10%。此外,北京每月僅發放1萬輛內燃機汽車登記許可證,鼓勵民眾轉換電動車。隨著汽車銷售的增加和都市化的快速發展,中國決定減少汽車排放。同時,它正在尋求透過增加電動車的需求和銷售來減少對石油進口的依賴。

出口到其他國家的汽車產量增加,以及電動車在中國的普及,預計將推動中國電力電子和印刷電路板需求的主要因素。

歐洲和北美也擁有大量汽車OEM,汽車產業電氣化不斷推進,使這些地區成為電動車銷售量高的主要市場。因此,隨著各公司在該領域的創新,預計電動車領域的汽車印刷線路板市場將在預測期內成長。例如,2022 年 6 月,PCB Technologies 推出了 iNPACK,這是一種系統級封裝(SIP) 解決方案,可提高訊號完整性並顯著減少不必要的電感效應。此 SIP 解決方案可用於汽車、消費性電子和醫療設備產業的各種應用。

汽車印刷電路基板(PCB)產業概述

汽車印刷電路基板(PCB)市場適度整合。該市場的特點是存在與每個地區的主要汽車OEM簽訂長期供應合約的全球和本地公司。這些參與者還進行合資、併購、新產品發布和產品開拓,以擴大其品牌組合併鞏固其市場地位。

主導全球市場的一些主要企業包括三星電機有限公司、英飛凌公司、CMK公司、KCE電子有限公司和Amitron公司。許多參與者正在擴大其製造能力,以確保其市場地位並保持市場領先地位。例如,2023年2月,Elna PCB Malaysia Sdn Bhd宣布將在馬來西亞檳城建造新的PCB製造工廠,並於2024年開始量產。該新廠的設備、廠房、機械和建設已預留 10 億令吉的投資預算,將於 2022 年 12 月開始實施。這家新工廠將生產用於汽車和電子設備的印刷電路板。

2022年4月,英飛凌科技公司完全子公司PT英飛凌科技巴淡島(印尼)宣布,將在2024年之前擴大在印尼的後端產能。透過此次擴建,巴淡島工廠將成為英飛凌科技公司繼馬來西亞馬六甲工廠(汽車 PCB)後的第二大工廠。此外,2022 年 6 月,義法半導體推出了適用於汽車和工業應用的新型基於高電壓印刷電路基板的運算放大器。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 研究成果

- 研究場所

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 市場概況

- 市場促進因素

- 由於電動車銷量增加,對汽車 PCB 的需求增加

- 市場限制因素

- 複雜的設計和整合挑戰

- 價值鏈/供應鏈分析

- 波特五力分析

- 新進入者的威脅

- 買家/消費者的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭公司之間敵對關係的強度

第5章市場區隔

- 按車型

- 客車

- 商用車

- 依推進類型

- 內燃機

- 電動式

- 按類型

- 單層

- 雙層

- 多層

- 按用途

- ADAS

- 身體舒適度

- 資訊娛樂系統

- 動力傳動系統零件

- 其他

- 按地區

- 北美洲

- 美國

- 加拿大

- 北美其他地區

- 歐洲

- 德國

- 英國

- 法國

- 歐洲其他地區

- 亞太地區

- 印度

- 中國

- 日本

- 韓國

- 其他亞太地區

- 其他地區

- 巴西

- 阿拉伯聯合大公國

- 其他國家

- 北美洲

第6章 競爭狀況

- 供應商市場佔有率

- 公司簡介

- Infineon Technologies AG

- Samsung Electro Mechanics

- CMK Corporation

- Amitron Corporation

- KCE Group

- Daeduck Phil. Inc.

- MEIKO ELECTRONICS Co. Ltd

- CHIN POON Industrial Co. Ltd

- Unimicron Group

- STMicroelectronics NV

- Tripod Technologies

第7章 市場機會及未來趨勢

The Automotive Printed Circuit Board Market size is estimated at USD 7.49 billion in 2024, and is expected to reach USD 9.52 billion by 2029, growing at a CAGR of 6.40% during the forecast period (2024-2029).

The increasing use of electrical systems in cars and the expanding need for driver comfort and safety in vehicles, coupled with significant expansion of the automotive sector, are anticipated to act as major driving factors for market growth during the forecast period.

Furthermore, with the increasing popularity of vehicle automation and the growing demand for connected cars across the world, the demand for automotive PCBs is expected to grow significantly during the forecast period.

The integration of Artificial Intelligence (AI), cloud, and IoT-enabled devices to improve and enhance vehicle and vehicle-to-infrastructure communication. AI-powered technologies, such as emotional and behavioral recognition and personal assistants, have been fueling the growth of safety and scenarios, such as Vehicle As A Marketplace, which in turn is likely to enhance the demand for power electronics components in vehicles. Thus further propelling the target market.

Over the long term, increasing investments in R&D by major industry players and a rise in sales of electric and hybrid vehicles, as well as rising demand for connected vehicles fare creating demand in the automotive and transportation industry with a surge in sales of automotive printed circuit boards.

Key players in the market are expanding their production capacity to cater to the increased demand for automotive printed circuit boards. For instance,

In July 2022, Denkai America Inc. announced that it would invest USD 430 million in Augusta, Georgia, to set up its North American HQ and manufacturing facility. The manufacturing facility will include a USD 150 million production line to manufacture ED copper foils for EV batteries. In March 2022, Ather Energy and Bharat FIH, a Foxconn Technology Group subsidiary, signed an agreement wherein Bharat FIH will develop and manufacture electric components for Ather Energy, including printed circuit boards (PCBs), in India.

Automotive Printed Circuit Board Market Trends

Growing Electric Vehicles Sales Driving the Market Growth

Many governments in some of the largest automotive markets like China, India, and Europe are relentlessly promoting the adoption of electric vehicles through various government incentives and policies aimed at boosting the sales of EVs to meet the carbon reduction goals under the Paris Climate Change Accord 2015 to which all these markets are signatories.

Sales of electric cars increased by around 60% in 2022 globally when compared to 2021, surpassing 10 million for the first time, even though car sales broadly were soft last year. As a result, one in every seven passenger cars bought globally in 2022 was an EV, according to the International Energy Agency (IEA). Nonetheless, electric vehicles are likely to outperform in 2023 as well. More than 2.3 million electric cars have been sold during the first quarter of 2023, which translates to a growth of about 25%, which is more than in comparison to the same period last year. In 2023, 14 million electric car sales are expected, representing 35% year-on-year growth; this will increase the market share of electric cars up to 18% in total car sales.

Various countries in Asia-Pacific and Europe have announced that they will ban the sales of new ICE vehicles by 2040 in favor of battery electric vehicles. Rising oil prices, growing pollution levels, increasing environmental consciousness, and a number of government incentives to promote electromobility are all contributing to very healthy growth in sales of EVs around the world. For instance,

In China, EV sales rose to 3.66 million units in 2022 (till September), posting a YoY growth of 119%, while in India, EV sales stood at 390,399 units (till July) in 2022, registering a YoY increase of 333%.

The emergence of electric turbochargers, also known as electrically assisted turbochargers or e-turbochargers, is a recent development. These systems utilize electric motors to enhance turbocharger performance and improve transient response, thereby reducing turbo lag.

An automotive PCB controls all the functions of a battery, which is the core component of an EV. Thus, the massive growth in sales of EVs is providing a very high impetus to the growth of the automotive PCB industry worldwide.

Owing to the increase in the demand for passenger cars and the growing awareness of electric mobility, significant players are ramping up the production capacity of their facilities. For instance,

In May 2023, Hyundai Motor India Limited announced an investment of INR 200 billion to enhance its electric vehicle manufacturing facility across India.

The increase in the trend of electric vehicles is expected to drive market growth in the future.

Asia-Pacific Region Anticipated to Grow at a Significant Level During the Forecast Period

The Asia-Pacific is the most dominant market, followed by North America and Europe.

Asia-Pacific is home to India, China, Japan, and South Korea, the world's largest automobile manufacturing countries. India and China are some of the world's largest markets for electric vehicles, contributing to almost 60% of worldwide electric vehicle sales, thus making Asia-Pacific the most lucrative market for automotive printed circuit boards. Automotive printed circuit boards are employed in the majority of these vehicles within the region to control the essential functions of an electric vehicle.

China is the largest manufacturer and consumer of electric vehicles in the world. Domestic demand is being supported by sales targets, favorable laws, and municipal air-quality targets. For instance,

China has imposed a quota on manufacturers of electric or hybrid vehicles, which must represent at least 10% of total new sales. Also, the city of Beijing only issues 10,000 permits for the registration of combustion engine vehicles per month to encourage its inhabitants to switch to electric vehicles. With increased vehicle sales and rapid urbanization, China is determined to reduce vehicle exhaust emissions. Meanwhile, the country intends to reduce its reliance on oil imports by increasing demand for and sales of electric vehicles.

An increase in vehicle production for exporting to other countries, along with the adoption of electric mobility in the country, are the key factors that are expected to boost the demand for power electronics and PCBs in China.

Europe and North America are also major markets due to the large presence of automotive OEMs and the rising electrification of the automotive industry, leading to high electric vehicle sales in these geographies. Thus, with companies coming up with innovations in this segment, the market for automotive Printed Circuit Boards is expected to grow over the forecast period for the electric vehicles segment. For instance, in June 2022, PCB Technologies launched iNPACK, a System-in-Package (SIP) solution that offers improved signal integrity and a significant reduction in unwanted inductance effects. The SIP solution can be utilized for a variety of applications in the automobile, consumer electronics, and medical devices industries.

Automotive Printed Circuit Board Industry Overview

The automotive PCB market is moderately consolidated. The market is characterized by the presence of some global and local players who have secured long-term supply contracts with major automotive OEMs in their respective regions. These players also engage in joint ventures, mergers and acquisitions, new product launches, and product development to expand their brand portfolios and cement their market positions.

Some of the major players dominating the global market are Samsung Electro-Mechanical Ltd, Infineon Corp., CMK Corp., KCE Electronics Ltd, and Amitron Corp. Many players are expanding their manufacturing capacity to secure their market position and stay ahead of the market curve. For instance, in February 2023, Elna PCB Malaysia Sdn Bhd announced a new PCB manufacturing plant in Penang, Malaysia, with mass production set to start in 2024. MYR's 1 billion investment budget has been set aside for the equipment, plant, and machinery, as well as the construction of this new plant that commenced in December 2022. This new plant will manufacture PCBs for automotive and electronic devices usage, among other products.

In April 2022, PT Infineon Technologies Batam, Indonesia, a wholly owned subsidiary of Infineon Technologies Corp, announced it would expand the backend production capacity in Indonesia by 2024. This expansion will see the Batam site become the second biggest one for Infineon Technologies Corp after their Melaka, Malaysia plant for automotive PCBs. Additionally, in June 2022, STMicroelectronics NV introduced a new high-voltage Printed Circuit board-based op amplifier for automotive and industrial applications.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising EV Sales to Fuel Automotive PCB Demand

- 4.3 Market Restraints

- 4.3.1 Complex Design and Integration Challenges

- 4.4 Value Chain / Supply Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Vehicle Type

- 5.1.1 Passenger Cars

- 5.1.2 Commercial Vehicles

- 5.2 By Propulsion Type

- 5.2.1 IC Engine

- 5.2.2 Electric

- 5.3 By Type

- 5.3.1 Single Layer

- 5.3.2 Double Layer

- 5.3.3 Multi-Layer

- 5.4 By Application

- 5.4.1 ADAS

- 5.4.2 Body and Comfort

- 5.4.3 Infotainment System

- 5.4.4 Powertrain Components

- 5.4.5 Other Applications

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 India

- 5.5.3.2 China

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 Rest of the World

- 5.5.4.1 Brazil

- 5.5.4.2 United Arab Emirates

- 5.5.4.3 Other Countries

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Infineon Technologies AG

- 6.2.2 Samsung Electro Mechanics

- 6.2.3 CMK Corporation

- 6.2.4 Amitron Corporation

- 6.2.5 KCE Group

- 6.2.6 Daeduck Phil. Inc.

- 6.2.7 MEIKO ELECTRONICS Co. Ltd

- 6.2.8 CHIN POON Industrial Co. Ltd

- 6.2.9 Unimicron Group

- 6.2.10 STMicroelectronics NV

- 6.2.11 Tripod Technologies

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

汽車印刷電路基板市場按類型、層類型、層壓材料、應用和最終用戶分類 - 2025 年至 2030 年全球預測

汽車印刷電路基板市場按類型、層類型、層壓材料、應用和最終用戶分類 - 2025 年至 2030 年全球預測 2025年全球汽車PCB市場報告

2025年全球汽車PCB市場報告 生物分解性印刷電路基板市場分析及預測至 2033 年:按類型、產品、材料類型、技術、應用、組件、最終用戶、流程和功能

生物分解性印刷電路基板市場分析及預測至 2033 年:按類型、產品、材料類型、技術、應用、組件、最終用戶、流程和功能 汽車 PCB 市場規模、佔有率、成長分析、按類型、按燃料類型、按自動駕駛水平、按應用、按最終用戶、按地區 - 行業預測,2024-2031 年汽車印刷電路基板市場:按類型、基板、應用、車型分類 - 2025-2030 年全球預測

汽車 PCB 市場規模、佔有率、成長分析、按類型、按燃料類型、按自動駕駛水平、按應用、按最終用戶、按地區 - 行業預測,2024-2031 年汽車印刷電路基板市場:按類型、基板、應用、車型分類 - 2025-2030 年全球預測 汽車用PCB市場,規模,佔有率,趨勢,產業分析報告:各類型,各車輛類型,各用途,各燃料類型,各銷售管道,各地區 - 市場預測,2025年~2034年

汽車用PCB市場,規模,佔有率,趨勢,產業分析報告:各類型,各車輛類型,各用途,各燃料類型,各銷售管道,各地區 - 市場預測,2025年~2034年 汽車用PCB繼電器的全球市場:車輛類別,繼電器類別,各用途,各功能,各地區,範圍及預測

汽車用PCB繼電器的全球市場:車輛類別,繼電器類別,各用途,各功能,各地區,範圍及預測 汽車PCB市場,按類型、車輛類型、應用、國家和地區 - 2024-2032年產業分析、市場規模、市場佔有率和預測全球汽車 PCB 市場規模(按類型、應用、最終用戶、地區、範圍和預測)

汽車PCB市場,按類型、車輛類型、應用、國家和地區 - 2024-2032年產業分析、市場規模、市場佔有率和預測全球汽車 PCB 市場規模(按類型、應用、最終用戶、地區、範圍和預測) 汽車用PCB繼電器的全球市場(2024年)

汽車用PCB繼電器的全球市場(2024年)