|

市場調查報告書

商品編碼

1523356

無氧銅:市場佔有率分析、產業趨勢/統計、成長預測(2024-2029)Oxygen Free Copper - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

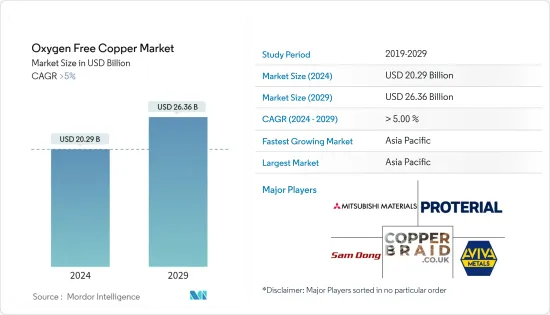

無氧銅市場規模預計2024年為202.9億美元,預計2029年將達到263.6億美元,在預測期內(2024-2029年)複合年成長率超過5%。

COVID-19 大流行減緩了生產和運輸,導致半導體短缺,並對無氧銅市場產生了負面影響。由於遏制措施和經濟中斷,電子和汽車等行業也被迫放慢生產速度。目前市場正從疫情中恢復。預計2022年市場將達到疫情前水準並持續穩定成長。

半導體對無氧銅的需求不斷成長正在推動預測期內的市場成長。

然而,銅的高成本預計將阻礙所研究市場的成長。

無氧銅在各種電子產品中的不斷成長的應用可能會在未來五年為無氧銅市場提供機會。

亞太地區在全球佔據主導地位,中國和印度等國家的消費不斷增加。

無氧銅市場趨勢

電氣電子產業主導市場

- 電氣和電子產業將成為主導市場的領域,因為它廣泛用於半導體和超導體的生產。

- 無氧銅通常用於半導體和超導性製造等製造應用以及需要等離子體沉澱的粒子加速器等高真空系統。

- 氧氣和其他雜質可能會與系統中使用的材料發生不良的化學反應。

- 無氧銅用途廣泛,包括印刷電路基板、微波管、真空電容器、真空斷路器、真空密封件、波導以及廣播電視發送器和磁控管的真空管,因此消費量較低。

- 全球電子設備數量迅速增加,例如行動電話、智慧型裝置、平板電腦和電視機,可能會在預測期內推動無氧銅的需求。如上所述,電氣和電子行業使用量的增加和應用範圍的擴大預計將成為市場成長的驅動力。

- 根據日本電子情報技術產業協會(JEITA)預計,2022年全球電子資訊科技產業產值預估為34,368億美元,而2021年為34,159億美元,與前一年同期比較成長1%。此外,預計2023年將達35,266億美元,與前一年同期比較成長3%。

- 此外,根據電子與資訊科技部的數據,2022 會計年度印度消費性電子產品(電視、配件、音訊)產值將超過 7,450 億印度盧比(94.6 億美元),支撐市場成長。

- 上述因素預計將在預測期內推動無氧銅市場。

亞太地區主導市場

- 中國、日本和印度等亞太新興國家對電子半導體裝置的需求不斷成長,預計亞太市場將成為預測期內最大、成長最快的市場。

- 整個亞太地區對智慧型手機、個人電腦、筆記型電腦和其他醫療電子產品等消費性設備的需求正在快速成長,其中印度、日本和中國對市場成長做出了巨大貢獻。

- 根據工業和資訊化部(MIIT)統計,中國是全球最大的消費性電子生產國,全球佔有率超過60%。

- 根據日本電子情報技術產業協會(JEITA)預測,2022年日本電子產業國內產值預估為111,243億日圓(約851.9億美元),年成長與前一年同期比較2%。預計2023年日本電子業的國內產值將達到114,029億日圓(約873.2億美元),年成長與前一年同期比較3%。

- 在高能源需求的支持下,亞太地區能源產業也蓬勃發展。快速成長的工業部門是推動該地區能源需求的主要因素之一,這支持了預測期內的市場成長。

- 亞太地區火力發電產業錄得成長,其中中國是該產業成長的主要推手。中國擁有的燃煤發電廠數量比世界上任何其他國家或地區都多。截至2022年7月,中國當地已運作燃煤發電廠1,118座。這大約是排名第二的印度的四倍。中國煤炭發電量佔全球一半以上。

- 上述因素預計將導致預測期內該地區無氧銅消費需求的增加。

無氧銅行業概況

無氧銅市場較為分散。研究的市場主要參與者包括(排名不分先後)Copper Braid Products、Mitsubishi Materials、Aviva Metals、PROTERIAL Ltd 和 Sam Dong。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第1章簡介

- 調查先決條件

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 促進因素

- 半導體需求增加

- 汽車領域需求增加

- 其他司機

- 抑制因素

- 銅成本高

- 其他阻礙因素

- 產業價值鏈分析

- 波特五力分析

- 新進入者的威脅

- 買方議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭程度

第5章市場區隔(以金額為準的市場規模)

- 年級

- CU-OF

- CU-OFE

- 產品

- 金屬絲

- 條

- 匯流排,棒

- 其他(管材、管道等)

- 最終用戶產業

- 電力/電子

- 車

- 產業

- 其他(發電、航太等)

- 地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 馬來西亞

- 泰國

- 印尼

- 越南

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 北歐國家

- 土耳其

- 俄羅斯

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 哥倫比亞

- 南美洲其他地區

- 中東/非洲

- 沙烏地阿拉伯

- 南非

- 奈及利亞

- 卡達

- 埃及

- 阿拉伯聯合大公國

- 其他中東/非洲

- 亞太地區

第6章 競爭狀況

- 併購、合資、聯盟、協議

- 市場佔有率(%)/排名分析

- 主要企業策略

- 公司簡介

- Aviva Metals

- Citizen Metalloys Ltd

- Copper Braid Products

- Cupori

- Farmers Copper LTD

- FURUKAWA ELECTRIC CO. LTD

- KGHM

- KME GERMANY GMBH

- Metrod Holdings Berhad

- Sam Dong

- Lacroix+Kress GmbH

- Mitsubishi Materials Corporation

- PROTERIAL Ltd

第7章 市場機會及未來趨勢

The Oxygen Free Copper Market size is estimated at USD 20.29 billion in 2024, and is expected to reach USD 26.36 billion by 2029, growing at a CAGR of greater than 5% during the forecast period (2024-2029).

The market was negatively impacted by the COVID-19 pandemic as there was a slowdown in production and mobility, which caused a shortage of semiconductors, which negatively impacted the market for oxygen-free copper. Also, industries such as electronics, automotive, etc., were forced to delay their production due to containment measures and economic disruptions. Currently, the market has recovered from the pandemic. The market reached pre-pandemic levels in 2022, and it is expected to grow steadily in the future.

Increasing demand for oxygen-free copper from semiconductors has been driving the market growth during the forecast period.

However, the high cost of copper is anticipated to hinder the growth of the studied market.

Growing oxygen-free copper applications in a wide range of electronics are likely to provide opportunities for the oxygen-free copper market over the next five years.

The Asia-Pacific region is dominated across the world, with increasing consumption from countries like China and India.

Oxygen Free Copper Market Trends

Electrical and Electronics Industry to Dominate the Market

- The electrical and electronics industry stands to be the dominating segment owing to wide consumption in the manufacturing of semiconductors and superconductors.

- Oxygen-free copper is commonly used in manufacturing applications such as the manufacture of semiconductors and superconductors and high-vacuum systems such as particle accelerators requiring plasma deposition.

- The use of oxygen-free materials is critical in these applications, as the presence of oxygen or some other impurity contributes to unwanted chemical reactions with the materials used in the system.

- Oxygen-free copper is witnessing growth in consumption due to its wide application in printed circuit boards, microwave tubes, vacuum capacitors, vacuum interrupters, vacuum seals, waveguides, and vacuum tubes for radio and TV transmitters and magnetrons.

- The exponential growth in the number of electronic gadgets across the globe, such as mobile phones, smart devices, tablets, and TV sets, is expected to drive the demand for oxygen-free copper over the forecast period. Thus, the increasing usage and widening arena of application in the electrical and electronics industry is expected to drive market growth.

- According to the Japan Electronics and Information Technology Industries Association (JEITA), the production by the global electronics and IT industry was estimated at USD 3,436.8 billion in 2022, registering a growth rate of 1% year-on-year, compared to USD 3,415.9 billion in 2021. Moreover, the industry is expected to reach USD 3,526.6 billion, with a growth rate of 3% year-on-year in 2023.

- Moreover, according to the Ministry of Electronics and Information Technology, the production value of consumer electronics (TV, accessories, and audio) across India was above INR 745 billion (USD 9.46 billion) in fiscal year 2022, thus supporting the growth of the market.

- All the aforementioned factors are expected to drive the oxygen-free copper market during the forecast period.

Asia-Pacific Region to Dominate the Market

- The Asia-Pacific market is expected to be the largest and fastest-growing market over the forecast period, owing to the increasing demand for electronic semiconductor devices in developing countries of Asia-Pacific, such as China, Japan, and India.

- Demand for consumer devices, such as smartphones, PCs, laptops, and other medical electronics products, is growing rapidly through the Asia-Pacific region, with India, Japan, and China contributing majorly to the market growth.

- According to the Ministry of Industry and Information Technology (MIIT), China is the world's largest producer of consumer electronics, with a global share of more than 60%.

- Furthermore, Japan is one of the largest producers of electronics; as per the Japan Electronics and Information Technology Industries Association (JEITA), the domestic production by the Japanese electronics industry was estimated at JPY 11,124.3 billion (~USD 85.19 billion) in 2022, witnessing a growth rate of 2% compared to the previous year. The domestic production by the Japanese electronics industry is likely to reach JPY 11,402.9 billion (~USD 87.32 billion) by 2023, registering a growth rate of 3% year-on-year.

- The Asia-Pacific energy sector is also thriving, owing to the high demand for energy. The rapidly growing industrial sector is one of the key factors driving the energy demand in the region, which in turn is supporting the market growth during the forecast period.

- The Asia-Pacific thermal sector is registering growth, with China primarily driving the growth of the sector. China has the most coal-fired power plants of any country or territory in the world. On the Chinese Mainland, as of July 2022, there were 1,118 operational coal power plants. This is approximately four times the number of such power plants in India, which came in second place. China accounts for more than half of the world's coal electricity generation.

- The aforementioned factors are anticipated to contribute to the increasing demand for oxygen-free copper consumption in the region during the forecast period.

Oxygen Free Copper Industry Overview

The oxygen-free copper market is fragmented in nature. The major players in the studied market (not in any particular order) include Copper Braid Products, Mitsubishi Materials Corporation, Aviva Metals, PROTERIAL Ltd, and Sam Dong.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand from Semiconductor

- 4.1.2 Increasing Demand from Automotive Sector

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 High Cost of Copper

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Grade

- 5.1.1 CU-OF

- 5.1.2 CU-OFE

- 5.2 Product

- 5.2.1 Wires

- 5.2.2 Strips

- 5.2.3 Busbars and Rods

- 5.2.4 Other Products (Tubes and Pipes, Etc.)

- 5.3 End-user Industry

- 5.3.1 Electrical and Electronics

- 5.3.2 Automotive

- 5.3.3 Industrial

- 5.3.4 Other End-user Industries (Power Generation, Aerospace, Etc.)

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Malaysia

- 5.4.1.6 Thailand

- 5.4.1.7 Indonesia

- 5.4.1.8 Vietnam

- 5.4.1.9 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 NORDIC Countries

- 5.4.3.7 Turkey

- 5.4.3.8 Russia

- 5.4.3.9 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Nigeria

- 5.4.5.4 Qatar

- 5.4.5.5 Egypt

- 5.4.5.6 UAE

- 5.4.5.7 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share(%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Aviva Metals

- 6.4.2 Citizen Metalloys Ltd

- 6.4.3 Copper Braid Products

- 6.4.4 Cupori

- 6.4.5 Farmers Copper LTD

- 6.4.6 FURUKAWA ELECTRIC CO. LTD

- 6.4.7 KGHM

- 6.4.8 KME GERMANY GMBH

- 6.4.9 Metrod Holdings Berhad

- 6.4.10 Sam Dong

- 6.4.11 Lacroix + Kress GmbH

- 6.4.12 Mitsubishi Materials Corporation

- 6.4.13 PROTERIAL Ltd

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing Oxygen-free Copper Application in Wide Range of Electronics

- 7.2 Other Opportunities