|

市場調查報告書

商品編碼

1524096

現場可程式閘陣列(FPGA):市場佔有率分析、產業趨勢/統計、成長預測 (2024-2029)Field Programmable Gate Array (FPGA) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

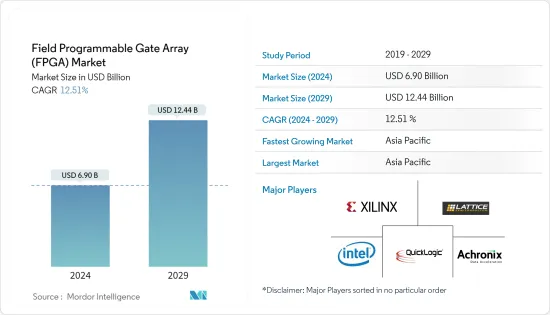

現場可程式閘陣列(FPGA)市場規模預計2024年為69億美元,預計2029年將達到124.4億美元,在預測期內(2024-2029年)複合年成長率預計為12.51%。

*FPGA 可以定義為可程式設計的積體電路,使客戶能夠在製造過程後重新配置硬體以滿足特定的用例要求,允許遠端執行功能升級和錯誤修復,從而使其在實際應用中可行,從而推動市場成長。 FPGA 包含具有可程式硬體結構的電路。與 ASIC 和圖形處理單元 (GPU) 不同,FPGA 晶片內的電路不是硬蝕刻的,並且可以在必要時重新編程。這項特性使得 FPGA 適合作為 ASIC 的替代品,而 ASIC 需要較長的開發時間和較高的設計和製造投資,從而支持預測期內的市場需求。

*FPGA 在科技產業中用於機器學習和深度學習。微軟研究院展示了過去十年中首批使用 FPGA 的人工智慧使用案例之一,作為該公司加快網路搜尋速度的努力的一部分。 FPGA 結合了可編程性、速度和靈活性,可提供高效能,而無需開發客製化專用積體電路 ( 自訂) 的高成本和複雜性。 FPGA 也用於微軟的搜尋引擎Bing,展示了 FPGA 在深度學習應用上的實用性。據該公司稱,Bing 使用 FPGA 加速搜尋排名,吞吐量提高了 50%,這表明 GPGA IC 在市場上的應用不斷成長。

*此外,FPGA 可實現整合 AI 的硬體客製化,並可透過程式設計提供類似 ASIC 和 GPU 的行為。 FPGA 的可重新配置和可程式設計特性使其非常適合快速發展的人工智慧環境,使設計人員能夠快速測試演算法並將其快速推向市場。與 ASIC 相比,高功耗限制了市場成長。能源效率一直是各行業關注的重點。電子設備產業一直在尋找低功耗的設備。 FPGA 功耗較高,程式設計師無法控制功耗最佳化。

*然而,由於其先進的功能,FPGA設計面臨架構複雜性和高功耗的挑戰。此外,FPGA 的成本高於其他選項,使得中小型企業更難使用它們,從而為 FGPA 的採用帶來未來的市場挑戰。

*由於 COVID-19 大流行和其他宏觀經濟趨勢,包括數位經濟和智慧城市等全球發展,政府、企業和學術界對資料中心、人工智慧和機器學習的需求正在快速成長。這種成長對 FPGA 需求產生了正面影響。預計 FPGA 在預測期內將保持相同的成長速度,從而促進 FPGA 在各個最終用戶產業中的普遍影響和重要性。

FPGA市場趨勢

消費性電子領域預計將推動市場成長

*消費性電子產品不斷添加功能並整合新技術,以提高視訊連接、品質和人工智慧 (AI) 功能。透過回應這些創新並增加消費性電子製造商的時間壓力,FPGA 的敏捷性和可自訂性將支持高需求消費性電子產品的成長。

*智慧家居消費性電子產品的出現正在成為家庭的新常態,管理安全、照明、網路消費電子、戶外灌溉、氣候、娛樂系統等、智慧型手機、數位顯示器、家庭網路設備、機上盒盒子等,FPGA在功能豐富的消費設備開發中的應用正在創造市場成長機會並推動市場成長。

*此外,消費性電子產品中影像/音訊處理、影像識別和訊號處理等 FPGA 應用的需求不斷增加。 FPGA 還可用於實現最新消費電子產品中安全通訊所必需的加密和解密演算法,隨著全球電子設備遭受網路攻擊的風險增加,推動市場成長。

*市場正在經歷強勁成長,部分原因是消費性電子製造商優先考慮合作和投資來開發 FPGA 解決方案市場。例如,2023年12月,三星電子和韓國網路巨頭Naver宣布投資基於FPGA(現場可程式閘陣列)的節能晶片,這是一種人工智慧半導體解決方案,專為Naver的大語言模型HyperCLOVA X量身訂做。我們已經與.

*FPGA 的平行處理架構允許複雜的音訊演算法以最小的延遲執行。這使得音訊訊號能夠快速處理並到達聽眾的耳朵,沒有任何明顯的延遲,從而產生無縫和身臨其境的音訊體驗,滿足全球消費性電子產品不斷成長的需求。此外,在智慧型手機中,FPGA 在電源效率方面發揮重要作用。 FPGA可以透過改變電路佈局來智慧控制功率並動態調整功耗,隨著智慧型手機數量的增加,這正在推動市場成長。

亞太地區預計將佔據主要市場佔有率

*亞太地區是 FPGA 產業參與者的關鍵區域。亞太地區擁有中國、印度、韓國、台灣等多個國家,近年來消費性電子產業成長迅速。因此,該地區的 FPGA 需求被視為一個影響點。

*根據SEMI(半導體設備與材料國際)的數據,中國在半導體設備的支出最多,其次是韓國、台灣和日本。此外,預計中國大陸今年將繼續保持其半導體製造設備支出的首位,而台灣地區預計將在 2024 年重返榜首。此外,中國政府鼓勵國家龍頭企業和頂尖數位公司發展國內半導體製造能力,以恢復中國對海外半導體需求的依賴平衡。這些努力可能會進一步提振半導體市場並推動 FPGA 需求。

*5G 的採用在網路和裝置領域均呈現成長動能。近年來,中國通訊業經歷了快速發展,預計這種情況將持續到2025年。人口、通訊服務和智慧型手機使用的成長正在刺激該行業的發展。優質連結和內容服務佔據了中國市場發展的大部分。

*此外,FPGA(現場可程式閘陣列)在半導體領域引起了廣泛關注。 FPGA是一種獨特的矽晶片,其特點是適應性強、功能先進。 FPGA 可可程式設計並能夠進行高速並行處理,使其成為各種應用的理想選擇,包括資料中心、汽車、通訊、航太和國防工業,以及印度等新興經濟體半導體製造業的發展。製造計劃,我們正在支持亞太地區市場的發展。

*中國正在為FPGA市場擴張鋪路。隨著該國作為消費電子產品的國際製造商佔據重要地位,需求不斷成長。中國是全球最大的製造地,生產全球36%的電子產品,包括智慧型手機、電腦、雲端伺服器和通訊基礎設施,成為全球電子供應鏈中最重要的節點。人工智慧在中國的普及,為中國消費性電子市場帶來了新的發展可能性。智慧家庭和物聯網 (IoT) 可能在未來十年為 FPGA 製造商帶來巨大的發展潛力。

FPGA產業概況

FPGA 市場適度分散,主要參與者包括 Xilinx Inc.、Lattice Semiconductor Corporation、Quicklogic Corporation、Intel Corporation 和 Achronix Semiconductor Corporation。市場上的競爭對手正在採取聯盟、擴張和收購等策略來加強其產品供應並獲得永續的競爭優勢。

*2023 年12 月- 英特爾擴展其英特爾Agilex FPGA 產品組合以滿足不斷成長的客戶需求,並擴展其可編程解決方案組(PSG) 產品陣容以提供客製化解決方案,包括增強的人工智慧功能。滿足不斷成長的工作負載需求,降低整體擁有成本。

*2023 年 10 月 - 萊迪思半導體宣布將在馬自達汽車公司新款 CX-60 和 CX-90 的高級駕駛體驗中使用萊迪思 FPGA。馬自達的跨界 SUV 利用多個基於低功耗晶格 FPGA 的介面橋接解決方案,提供更全面的偵測範圍、更高的偵測精度和空間感知能力,同時不會降低車輛性能。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第1章簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場洞察

- 市場概況

- 產業價值鏈分析

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 競爭公司之間的敵對關係

- 替代品的威脅

- 宏觀經濟走勢對產業的影響

第5章市場動態

- 市場促進因素

- 物聯網需求增加

- 市場限制因素

- 與 ASIC 相比功耗較高

第6章 市場細分

- 按配置

- 高階FPGA

- 中階FPGA/低階 FPGA

- 依架構

- 基於SRAM的FPGA

- 基於耐熔熔絲的 FPGA

- 基於快閃記憶體的FPGA

- 按最終用戶產業

- 資訊科技/通訊

- 消費性電子產品

- 車

- 產業

- 軍事/航太

- 其他

- 按地區

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 其他亞太地區

- 拉丁美洲

- 巴西

- 阿根廷

- 墨西哥

- 其他拉丁美洲

- 中東/非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

- 其他中東/非洲

- 北美洲

第7章 競爭格局

- 公司簡介

- Xilinx Inc.

- Lattice Semiconductor Corporation

- Quicklogic Corporation

- Intel Corporation

- Achronix Semiconductor Corporation

- GOWIN Semiconductor Corporation

- Microchip Technology Incorporated

- Efinix Inc.

第8章供應商市場佔有率分析

第9章投資分析

第10章投資分析市場的未來

The Field Programmable Gate Array Market size is estimated at USD 6.90 billion in 2024, and is expected to reach USD 12.44 billion by 2029, growing at a CAGR of 12.51% during the forecast period (2024-2029).

* The Field Programmable Gate Arrays can be defined as Integrated Circuits, which can be reprogrammable, enabling customers the ability to reconfigure the hardware to meet specific use case requirements after the manufacturing process, allowing for feature upgrades and bug fixes to be performed in remote deployment conditions, driving the growth of the market. Field programmable gate arrays (FPGAs) incorporate circuits with a programmable hardware fabric. Unlike ASICs or graphics processing units (GPUs), the circuitry inside an FPGA chip is not hard etched; it can be reprogrammed as required. This capability makes FPGAs a suitable alternative to ASICs, which need a long development time and a significant investment to design and fabricate, supporting its market demand during the forecast period.

* FPGAs are used in the technology industry for machine learning and deep learning. Microsoft Research displayed one of the first use cases of AI on FPGAs in the last decade as part of the company's efforts to speed up web searches. FPGAs provide a combination of programmability, speed, and flexibility, delivering performance without high cost and complexity to develop custom application-specific integrated circuits (ASICs). Microsoft's Bing search engine also uses FPGAs in production, indicating their value for deep learning applications. According to the company, Bing realized a 50% increase in throughput using FPGAs to accelerate search ranking, showing the increasing application of GPGA ICs in the market.

* In addition, FPGAs deliver hardware customization with integrated AI and can be programmed to provide behavior like an ASIC or a GPU. The reconfigurable, reprogrammable nature of an FPGA makes itself well suited for a rapidly evolving AI landscape, enabling designers to test algorithms quickly and get to market fast. High Power Consumption Compared to ASIC, which is restraining the market growth. Energy efficiency has always been a significant concern across various industries. Industries incorporating electronic devices always seek low-power-consuming devices. In FPGAs, power consumption is higher, and programmers do not have any control over power optimization.

* However, designing FPGA presents a significant challenge due to the complexity of the architecture and the high-power consumption due to its advanced capabilities. Additionally, the cost of these FPGAs is higher than other alternatives, making them less accessible to small and medium-sized businesses, creating a future market challenge for the FGPAs's adoption.

* The demand for data centers, artificial intelligence, and machine learning across government, enterprises, and academic entities is witnessing exponential growth due to the COVID-19 pandemic and other Macroeconomic trends, including the development of digital economies, smart cities, and other factors worldwide. This growth has positively impacted the need for FPGAs. It is predicted that FPGAs will maintain the same pace in the forecasted period, helping spread the impact and significance of FPGAs in various end-user industries.

Field Programmable Gate Array (FPGA) Market Trends

Consumer Electronic Segment is Expected to Drive the Market Growth

* Consumer electronic products are improving and continually adding features and integrating new technologies to enhance video connectivity, quality, and artificial intelligence (AI) capabilities. Keeping up with these innovations and raising time pressure on consumer electronics manufacturers supports the demand for FPGAs due to their agility and customization-friendly features to support the growth of the high demand volume of consumer electronic products.

* The emergence of Smart home consumer electronic products is becoming the new norm, with homeowners managing security, lighting, networked appliances, outdoor irrigation, climate, and entertainment systems, creating an opportunity for market growth due to the application of FPGAs in developing feature-rich consumer devices such as smartphones, digital displays, home networking equipment, and set-top boxes, driving the market growth.

* Additionally, the applications of FPGAs for video and audio processing, image recognition, and signal processing are in growing demand in consumer electronic products. FPGAs can also be used to implement encryption and decryption algorithms, essential for secure communication in modern consumer electronics, fueling the market's growth in line with the increased risk of cyber-attacks on electronic devices worldwide.

* The market has been registering significant growth supported by the increasing priority of consumer electronics manufacturers to partner and invest in the development of FPGA solutions in the market. For instance, in December 2023, Samsung Electronics and South Korean internet giant Naver partnered to invest in an artificial intelligence semiconductor solution, the energy efficiencies chip based on a Field-Programmable Gate Array (FPGA) customized for Naver's HyperCLOVA X large language model, showing the importance of FPGA solutions development in the consumer electronic segments, which would support the market growth.

* FPGA's parallel processing architecture enables the execution of complex audio algorithms with minimal delay. This ensures that audio signals are processed swiftly and delivered to the listener's ears without perceptible lag, creating a seamless and immersive audio experience and supporting its demand with the growth of consumer electronic products worldwide. Additionally, in smartphones, FPGAs play a crucial role in power efficiency. They can intelligently control power by rearranging their circuitry to dynamically adjust power consumption, fueling the market growth with the increasing number of smartphones.

Asia-Pacific is Expected to Hold a Significant Market Share

* Asia-Pacific is a significant region for the players operating in the FPGA industry. Within the Asia Pacific, many nations, including China, India, South Korea, Taiwan, and others, have seen an enormous increase in the consumer electronics industry in the past few years. As a result, the demand for FPGAs in the area is seen as an influence point.

* According to the Semiconductor Equipment and Material International (SEMI), China is a significant spender on semiconductor equipment, followed by South Korea, Taiwan, and Japan. Furthermore, China is expected to maintain the top position in semiconductor equipment spending this year, while Taiwan is anticipated to regain the lead in 2024. In addition, the Chinese government encouraged its national champions and top digital enterprises to develop their domestic semiconductor manufacturing capacities to rebalance China's reliance on overseas semiconductor demand. Such an initiative may further boost the semiconductor market, propelling the demand for FPGA.

* The 5G adoption is rising in momentum for both the network and device domains. The Chinese telecom sector has experienced rapid evolution in recent years, which is expected to continue until 2025. Increased population, communication services, and smartphone use fuel the industry's development. Premium connectivity and content services in China account for the majority of the market development in the country.

* Additionally, Field Programmable Gate Arrays (FPGAs) have gained substantial attention within the semiconductor sector. FPGAs are unique silicon chips characterized by their adaptability and advanced features. Their reprogrammable nature and high-speed parallel processing capabilities make them ideal for various applications in data centers, automotive, telecommunications, aerospace, and defense industries, supporting the growth of the market in developing economies, including India, in line with the development of semiconductor manufacturing and make in India programs of the country, which can fuel the market growth in Asia-Pacific.

* China is paving the way for the FPGA market to expand. The country's demand is extending due to its significant position as the international manufacturer of consumer electronics gadgets. China is the world's largest manufacturing hub, producing 36% of the world's electronics, including smartphones, computers, cloud servers, and telecom infrastructure, establishing the country as the global electronics supply chain's most important node. The popularity of AI in China has opened up new development potential for the Chinese consumer electronics market. Smart homes and IoT (Internet of Things) will likely be significant development potential for manufacturers of FPGA in the next decade.

Field Programmable Gate Array (FPGA) Industry Overview

The Field Programmable Gate Array (FPGA) Market is moderately fragmented, with the presence of major players like Xilinx Inc., Lattice Semiconductor Corporation, Quicklogic Corporation, Intel Corporation, and Achronix Semiconductor Corporation. Players in the market are adopting strategies such as partnerships, expansions, and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

* December 2023 - Intel planned to expand its Intel Agilex FPGA portfolio to address customers' growing needs, broaden its Programmable Solutions Group (PSG) offerings to handle the increased demand for customized workloads, including enhanced AI capabilities, and provide lower total cost of ownership (TCO) and more complete solutions.

* October 2023 - Lattice Semiconductor announced its Lattice FPGAs would be used in the advanced driver experiences on Mazda Motor Corporation's new CX-60 and CX-90 models. The Mazda crossover SUVs leverage the interface bridging solution based on multiple low-power Lattice FPGAs to provide a safety-critical Advanced Driver Assistance System, including a more comprehensive detection range, improved detection accuracy, and spatial recognition performance without decreasing vehicle performance.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Intensity of Competitive Rivalry

- 4.3.5 Threat of Substitutes

- 4.4 Impact of Macro Economic trends on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Demand for IoT

- 5.2 Market Restraints

- 5.2.1 High Power Consumption Compared to ASIC

6 MARKET SEGMENTATION

- 6.1 By Configuration

- 6.1.1 High-end FPGA

- 6.1.2 Mid-range FPGA/Low-end FPGA

- 6.2 By Architecture

- 6.2.1 SRAM-based FPGA

- 6.2.2 Anti-fuse Based FPGA

- 6.2.3 Flash-based FPGA

- 6.3 By End-user Industry

- 6.3.1 IT and Telecommunication

- 6.3.2 Consumer Electronics

- 6.3.3 Automotive

- 6.3.4 Industrial

- 6.3.5 Military and Aerospace

- 6.3.6 Other End-user Industries

- 6.4 By Geography

- 6.4.1 North America

- 6.4.1.1 United States

- 6.4.1.2 Canada

- 6.4.2 Europe

- 6.4.2.1 Germany

- 6.4.2.2 United Kingdom

- 6.4.2.3 France

- 6.4.2.4 Rest of Europe

- 6.4.3 Asia-Pacific

- 6.4.3.1 China

- 6.4.3.2 Japan

- 6.4.3.3 India

- 6.4.3.4 South Korea

- 6.4.3.5 Rest of the Asia-Pacific

- 6.4.4 Latin America

- 6.4.4.1 Brazil

- 6.4.4.2 Argentina

- 6.4.4.3 Mexico

- 6.4.4.4 Rest of Latin America

- 6.4.5 Middle East and Africa

- 6.4.5.1 United Arab Emirates

- 6.4.5.2 Saudi Arabia

- 6.4.5.3 South Africa

- 6.4.5.4 Rest of Middle East and Africa

- 6.4.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Xilinx Inc.

- 7.1.2 Lattice Semiconductor Corporation

- 7.1.3 Quicklogic Corporation

- 7.1.4 Intel Corporation

- 7.1.5 Achronix Semiconductor Corporation

- 7.1.6 GOWIN Semiconductor Corporation

- 7.1.7 Microchip Technology Incorporated

- 7.1.8 Efinix Inc.

8 VENDOR MARKET SHARE ANALYSIS

9 INVESTMENT ANALYSIS

10 FUTURE OF THE MARKET

2024-2032 年按技術(EEPROM、反熔絲、SRAM、快閃記憶體等)、應用(資料處理、消費性電子產品、工業、軍事和航太、汽車、電信等)和地區分類的嵌入式 FPGA 市場報告

2024-2032 年按技術(EEPROM、反熔絲、SRAM、快閃記憶體等)、應用(資料處理、消費性電子產品、工業、軍事和航太、汽車、電信等)和地區分類的嵌入式 FPGA 市場報告 到 2030 年現場可程式閘陣列(FPGA) 市場預測:按產品類型、配置類型、節點大小、技術、應用、最終用戶和地區進行的全球分析

到 2030 年現場可程式閘陣列(FPGA) 市場預測:按產品類型、配置類型、節點大小、技術、應用、最終用戶和地區進行的全球分析 2024-2028 年全球現場可程式閘陣列(FPGA) 市場

2024-2028 年全球現場可程式閘陣列(FPGA) 市場 現場可程式閘陣列市場:按配置、架構、類型、製程節點和最終用戶分類 - 2024-2030 年全球預測

現場可程式閘陣列市場:按配置、架構、類型、製程節點和最終用戶分類 - 2024-2030 年全球預測 全球FPGA市場發展趨勢分析

全球FPGA市場發展趨勢分析 FPGA市場規模,佔有率,預測,趨勢分析:依程式技術,配置,節點大小,領域,地區-2031年之前的全球預測

FPGA市場規模,佔有率,預測,趨勢分析:依程式技術,配置,節點大小,領域,地區-2031年之前的全球預測 嵌入式FPGA(現場可程式閘陣列)2024 年全球市場報告

嵌入式FPGA(現場可程式閘陣列)2024 年全球市場報告 2024-2032 年按架構、配置、最終用途產業和地區分類的現場可程式閘陣列市場報告

2024-2032 年按架構、配置、最終用途產業和地區分類的現場可程式閘陣列市場報告 嵌入式 FPGA (eFPGA) 市場,按技術、按應用、按國家和地區分類 - 2024-2032 年行業分析、市場規模、市場佔有率和預測

嵌入式 FPGA (eFPGA) 市場,按技術、按應用、按國家和地區分類 - 2024-2032 年行業分析、市場規模、市場佔有率和預測 2024 年現場可程式閘陣列全球市場報告

2024 年現場可程式閘陣列全球市場報告