|

市場調查報告書

商品編碼

1687458

智慧廢棄物管理:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)Smart Waste Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

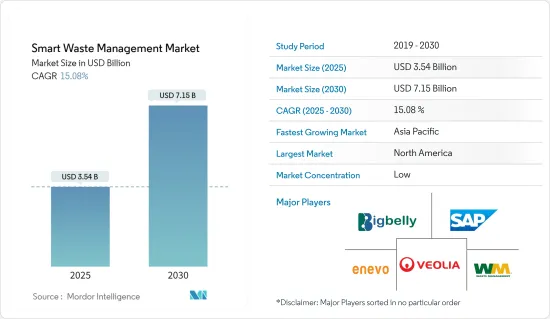

智慧廢棄物管理市場在 2025 年的價值預估為 35.4 億美元,預計到 2030 年將達到 71.5 億美元,在市場估計和預測期(2025-2030 年)內的複合年成長率為 15.08%。

智慧廢棄物管理使用廢棄物上的感測器來即時監控市政廢棄物收集服務的狀態並決定何時清空或裝滿垃圾箱。此外,可以追蹤感測器和資料庫收集的歷史資訊,並將其用於識別和增強駕駛路線和裝載模式,從而降低營運成本。透過遠端監控和基於物聯網的垃圾箱,有效的垃圾收集變得更加實用。都市化和快速工業化是智慧廢棄物管理市場的兩大驅動力。因此,市政和工業部門的廢棄物量不斷增加。隨著環保意識的增強,日常廢棄物收集和處理也變得越來越頻繁。

主要亮點

- 智慧廢棄物管理對於智慧城市的發展至關重要(與水資源管理、交通管理、能源管理等),以改善都市區生活方式。各個地區擴大採用創新城市舉措,推動了智慧廢棄物管理市場的成長。廢棄物管理產業涵蓋收集、處理、運輸和回收等多種活動。該行業在廢棄物管理的各個階段都面臨效率問題。營運成本與廢棄物的收集和運輸成本相同,從而增加了智慧廢棄物管理的採用率。

- 近年來,由於人口成長和都市化的加快,全球對廢棄物管理的需求以及解決維護老化基礎設施的成本影響的需求成為智慧廢棄物管理市場成長的主要驅動力。

- 此外,配備即時廢棄物管理系統的一次性標籤、容器和吸塵器等產品也支援了智慧廢棄物管理市場的發展。廢棄物管理系統的使用日益增多也源自於人們對環境問題的日益關注。

- 然而,由於全球技術純熟勞工的短缺,大多數工人將不得不前往服務區解決問題,預計將增加維護成本。然而,在預測期內,對遠端系統管理的更多關注可能會減輕成本負擔。

智慧廢棄物管理市場趨勢

分析產業將經歷顯著成長

- 在科技進步和快速都市化的時代,廢棄物管理已成為世界各地城市面臨的關鍵挑戰。智慧廢棄物管理已成為一種有前景的解決方案。車隊管理在智慧廢棄物管理系統中發揮核心作用。

- 車隊管理解決方案通常指使用資料通訊、記錄和分析來增強車輛活動的控制的系統。 FMS 的服務範圍包括車隊和資產管理、營運管理、供應鏈管理和法規合規。透過實施車隊管理解決方案,您可以降低燃料成本和其他佔車輛營運費用的因素。這樣,FMS 提供的優勢有助於最大限度地降低車輛營運成本。

- 智慧廢棄物管理中的車隊管理涵蓋各種活動,例如廢棄物收集車輛的監控和追蹤、路線最佳化、維護安排和性能分析。愛立信預計,到2027年,近距離物聯網(IoT)設備的普及率將成長到250億,而廣域物聯網設備預計到2027年將達到54億,並將用於即時追蹤廢棄物收集車輛的位置和移動情況。

- 透過為這些車輛配備 GPS 設備和感測器,廢棄物管理部門可以深入了解業務效率,確定需要改進的領域,並立即應對收集過程中可能出現的任何問題。此外,將路線最佳化軟體整合到車隊管理系統中將使廢棄物管理部門能夠規劃更有效率的路線。

北美佔有最大市場佔有率

- 美國智慧城市擴大使用智慧廢棄物管理解決方案來解決廢棄物收集和處理問題,這有望促進市場銷售。此外,預計未來幾年各國對減少二氧化碳排放的嚴格規定將促進市場銷售。政府加大力度推動永續性和實現淨零廢棄物,也可能繼續刺激該領域的需求。

- 美國各個城市已經制定了戰略計畫。光是該國每年就產生約 2.3 億噸排放,其中大部分由私人營業單位處理。由於政府採取措施促進永續性,以及全部區域智慧城市措施的普及,美國預計將佔據智慧廢棄物管理市場的大部分佔有率。

- 工業領域產量的不斷成長帶來了對智慧管理解決方案的需求。化學製造業處理了超過一半(55%)的 TRI 化學廢棄物。美國經濟分析局預計,2022年化學品生產增加值將達到約5,013.9億美元,而2021年為4,475.5億美元,這意味著美國化學工業創造的價值顯著增加。

- 透過移民、自然成長和都市化,加拿大的人口一直穩定成長。隨著人口的成長,對商品、服務和基礎設施的整體需求也隨之增加,導致廢棄物產生量增加。據加拿大統計局稱,加拿大目前每年約有 50 萬移民,是世界上人均移民率最高的國家之一。截至2023年,加拿大永久移民人數將超過800萬,約佔加拿大總人口的20%。

- 加拿大企業正在尋找永續管理廢棄物並降低成本的新方法。這項變更包括整合感測器和其他雲端基礎的技術,以減少廢棄物並最佳化服務水準。為了減少溫室氣體排放,該公司也正在測量排放的廢棄物的碳排放。

- 該國正在努力消除政府業務、活動和會議中過度使用一次性塑膠,並購買更多可修復、再利用和回收的永續塑膠產品。到 2030 年,政府的目標是延長產品壽命,並從公共管理中清除至少 75% 的塑膠廢棄物。

智慧廢棄物管理市場概覽

智慧廢棄物管理市場比較分散。隨著智慧互聯產品功能的急劇擴展,各公司將競相追趕競爭對手,並可能最終放棄過於先進的產品。這種環境將會推高成本並侵蝕產業盈利。市場的主要企業包括 SAP SE、威立雅環境服務公司、Enevo、Waste Management Inc. 和 Bigbelly Inc.

- 2023年10月 - 威立雅贏得歷史性的20億歐元契約,用於處理香港的無害廢棄物,繼續推動該市的生態系統轉型和資源再生。威立雅集團在香港經營超過30年,擁有超過1,000名員工,致力於透過多項水、廢棄物和能源合約實現本地脫碳,以加速香港的生態轉型。

- 2023 年 9 月 – WM 在俄亥俄州克利夫蘭開設一個佔地 100,000 平方英尺的新回收設施。該設施配備了最新的技術,每天可處理多達 420 噸的回收材料。 WM 的新回收設施技術,包括玻璃回收設備、光學分類機、無包裝篩機和彈道分離器,旨在支持當地回收項目的發展和為使用回收材料作為原料製造新產品的客戶生產高品質的材料。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概況

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 新冠肺炎疫情及其他宏觀經濟因素對市場的影響

第5章 市場動態

- 市場促進因素

- 垃圾量增加推動市場

- 智慧城市的普及將振興市場

- 市場挑戰

- 實施成本高

第6章 技術簡介

- 技術概述

- 創新技術革新廢棄物管理

- 智慧廢棄物管理階段 - 按連接器分類

- 智慧廢棄物管理市場中的感測器應用

- 智慧廢棄物管理階段

- 智慧收藏

- 智慧處理

- 智慧型能源回收

- 智慧處置

第7章 市場區隔

- 按解決方案

- 車隊管理

- 遠端監控

- 分析

- 廢棄物類型

- 工業廢棄物

- 住宅廢棄物

- 按地區

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 亞洲

- 印度

- 中國

- 澳洲

- 日本

- 澳洲和紐西蘭

- 拉丁美洲

- 中東和非洲

- 北美洲

第8章 競爭格局

- 公司簡介

- SAP SE

- Veolia Environmental Services

- Enevo

- Waste Management Inc.

- Bigbelly Inc.

- Covanta Holding Corporation

- Evoeco

- Pepperl+Fuchs GmbH

- IBM Corporation

- BIN-e

第9章投資分析

第 10 章:市場的未來

The Smart Waste Management Market size is estimated at USD 3.54 billion in 2025, and is expected to reach USD 7.15 billion by 2030, at a CAGR of 15.08% during the forecast period (2025-2030).

Smart waste management directs the use of sensors in waste to observe the real-time status of municipal waste collection services and decide when bins should be emptied or filled. It also maintains track of past information collected by sensors and databases that can be utilized to pinpoint and enhance driver routes, fill patterns, and lower operating costs. Effective waste collection is more functional with remote monitoring and IoT-based waste bins. Urbanization and rapid industrialization are the two main drivers of the smart waste management market. Therefore, the volume of waste from the municipal and industrial sectors has grown. The routine collection and disposal of waste have risen due to rising environmental awareness.

Key Highlights

- Smart waste management is crucial in developing smart cities (along with water management, traffic management, energy management, etc.) to improve lifestyles in urban areas. The increasing adoption of innovative city initiatives across regions helps the smart waste management market's growth. The waste management industry involves diverse activities, such as collection, disposal, transportation, and recycling. The industry has been facing efficiency problems at different stages of waste management. The operational costs equal the collection and transport of the waste, thereby increasing the adoption of smart waste management.

- In recent years, owing to the growing population and urbanization, the global demand for waste management and the demand to address the cost implications of maintaining an aging infrastructure have been among the primary motivating factors for the smart waste management market's growth.

- Moreover, the development of the smart waste management market has been assisted by products like disposable tags, containers, and vacuum cleaners that contain real-time waste management systems. The rising usage of waste management systems also results from growing environmental concerns.

- However, the lack of skilled laborers worldwide is expected to increase maintenance costs as most of them have to travel down to the service areas and resolve issues. Nevertheless, the growing focus on remote management may reduce the cost burden during the forecast period.

Smart Waste Management Market Trends

Analytics Sector to Witness Major Growth

- Waste management has become a crucial issue for cities worldwide in the era of technological advancements and rapid urbanization. Smart waste management has emerged as a promising solution. Fleet management plays a central role in smart waste management systems.

- Fleet management solutions often refer to systems that offer greater control over fleet activities using data communications, logging, and analytics. FMS's various services include vehicle and asset management, operation management, supply chain management, and regulatory compliance. Deploying fleet management solutions reduces factors that account for a significant portion of fleet operation spending, such as fuel costs. Thus, by the benefits they provide, FMS minimizes the cost of fleet operation.

- Fleet management in smart waste management encompasses a range of activities, including monitoring and tracking waste collection vehicles, route optimization, maintenance scheduling, and performance analysis. One of the crucial components of fleet management in this context is using GPS and Internet of Things technologies; according to Ericsson, the adoption number of short-range Internet of Things (IoT) devices is forecast to increase to 25 billion by 2027. and wide-area IoT devices are predicted to reach 5.4 billion by 2027 and used to track the location and movement of waste collection vehicles in real-time

- By equipping these vehicles with GPS devices and sensors, waste management authorities can gain valuable insights into their operations' efficiency, identify improvement areas, and respond immediately to any issues that may arise during the collection process. Moreover, the integration of route optimization software into fleet management systems enables waste management authorities to plan more efficient routes.

North America Holds Largest Market Share

- Smart cities in the United States use smart waste management solutions more frequently to solve waste collection and disposal issues, which is expected to boost market sales. In addition, strict rules governing the reduction of carbon emissions across the country are anticipated to drive market sales in the coming years. The increasing government's efforts to promote sustainability and achieve net-zero waste will continue to drive up demand in the area.

- Cities in the United States are already implementing strategic programs. The country alone contributes most of the yearly waste produced, with around 230 million metric tons of trash, a significant chunk of which private entities handle. The United States is expected to account for a significant share of the smart waste management market due to government initiatives promoting sustainability and the penetration of smart city initiatives across the high urban concentration region.

- The industrial sector's increased production creates a demand for smart management solutions. The chemical manufacturing industry manages over half (55%) of all TRI chemical waste. According to the BEA, in 2022, the value added from producing chemical products reached approximately USD 501.39 billion, which was USD 447.55 billion in 2021. This demonstrates a substantial increase in the value generated by the chemical industry in the United States.

- Canada's population continues to grow steadily, driven by immigration, natural population increase, and urbanization. As the population expands, so does the overall demand for goods, services, and infrastructure, leading to increased waste generation. As per StatCan, currently, annual immigration in Canada amounts to almost 500,000 new immigrants, which is one of the highest rates per population of any country in the world. As of 2023, there were more than eight million immigrants with permanent residence living in Canada, roughly 20% of the total Canadian population.

- Companies in the country are finding new ways to manage waste sustainably while cutting costs. The changes include integrating sensors and other cloud-based technologies to reduce waste volumes and optimize service levels. Companies are also measuring the carbon footprint of the waste produced to reduce greenhouse gas emissions.

- The country is working towards eliminating the excessive use of single-use plastics in government operations, events, and meetings and purchasing more sustainable plastic products that can be repaired, reused, or repurposed. By 2030, the government aims to extend product life and remove at least 75% of plastic waste from public administrations.

Smart Waste Management Market Overview

The Smart Waste Management Market is fragmented. The vast expansion of capabilities in smart connected products may tempt companies to keep up with rivals and give away too much improved product performance. This environment escalates costs and erodes industry profitability. Some of the key players in the market are SAP SE, Veolia Environmental Services, Enevo, Waste Management Inc., and Bigbelly Inc.

- October 2023 - Veolia continues Hong Kong's ecological transformation and the regeneration of its resources, following the award of a historic EUR 2 billion contract to dispose of the city's non-hazardous waste. With a presence in Hong Kong for over 30 years and more than a thousand employees, the Group is working locally to decarbonize the city's activities through multiple water, waste, and energy contracts to accelerate the local ecological transformation.

- September 2023 - WM has opened a new 100,000-square-foot recycling facility in Cleveland, Ohio. The facility has the latest technology and can process up to 420 tonnes of recyclables daily. WM's new recycling facility technology, which includes glass recovery equipment, an optical sorter, a non-wrapping screen, and ballistic separators, is designed to support the growth of recycling programs in the region and the production of high-quality material for customers who use recycled material as raw material to create new products.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Impact of COVID-19 Aftereffects and Other Macroeconomic Factors on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Volumes of Waste to Boost the Market

- 5.1.2 Rising Adoption of Smart Cities to Flourish the Market

- 5.2 Market Challenges

- 5.2.1 High Costs of Implementation

6 Technology Snapshot

- 6.1 Technology Overview

- 6.2 Innovative Technologies Revolutionizing Waste Management

- 6.3 Smart Waste Management Stages - By Connectors

- 6.4 Application of Sensors in the Smart Waste Management Market

- 6.5 Smart Waste Management Stages

- 6.5.1 Smart Collection

- 6.5.2 Smart Processing

- 6.5.3 Smart Energy Recovery

- 6.5.4 Smart Disposal

7 MARKET SEGMENTATION

- 7.1 By Solution

- 7.1.1 Fleet Management

- 7.1.2 Remote Monitoring

- 7.1.3 Analytics

- 7.2 By Waste Type

- 7.2.1 Industrial Waste

- 7.2.2 Residential Waste

- 7.3 By Geography

- 7.3.1 North America

- 7.3.1.1 United States

- 7.3.1.2 Canada

- 7.3.2 Europe

- 7.3.2.1 Germany

- 7.3.2.2 United Kingdom

- 7.3.2.3 France

- 7.3.2.4 Spain

- 7.3.2.5 Italy

- 7.3.3 Asia

- 7.3.3.1 India

- 7.3.3.2 China

- 7.3.3.3 Australia

- 7.3.3.4 Japan

- 7.3.3.5 Australia and New Zealand

- 7.3.4 Latin America

- 7.3.5 Middle East and Africa

- 7.3.1 North America

8 COMPETITIVE LANDSCAPE

- 8.1 Company Profiles

- 8.1.1 SAP SE

- 8.1.2 Veolia Environmental Services

- 8.1.3 Enevo

- 8.1.4 Waste Management Inc.

- 8.1.5 Bigbelly Inc.

- 8.1.6 Covanta Holding Corporation

- 8.1.7 Evoeco

- 8.1.8 Pepperl+Fuchs GmbH

- 8.1.9 IBM Corporation

- 8.1.10 BIN-e

9 INVESTMENT ANALYSIS

10 FUTURE OF THE MARKET

2032 年廢棄物網際網路和人工智慧廢棄物追蹤市場預測:按組件、廢棄物類型、部署、技術、最終用戶和地區進行的全球分析

2032 年廢棄物網際網路和人工智慧廢棄物追蹤市場預測:按組件、廢棄物類型、部署、技術、最終用戶和地區進行的全球分析 2025年智慧廢棄物管理全球市場報告

2025年智慧廢棄物管理全球市場報告 智慧廢棄物管理市場按產品類型、廢棄物類型、製程類型、技術、最終用戶和部署模式分類 - 2025-2030 年全球預測智慧食品盒市場(按組件、產品類型、技術、應用和最終用戶分類)—2025 年至 2030 年全球預測

智慧廢棄物管理市場按產品類型、廢棄物類型、製程類型、技術、最終用戶和部署模式分類 - 2025-2030 年全球預測智慧食品盒市場(按組件、產品類型、技術、應用和最終用戶分類)—2025 年至 2030 年全球預測 全球智慧廢棄物管理市場規模(按廢棄物類型、方法、來源、區域覆蓋範圍和預測)

全球智慧廢棄物管理市場規模(按廢棄物類型、方法、來源、區域覆蓋範圍和預測) 智慧廢棄物管理市場規模、佔有率、趨勢及預測(按成分、廢棄物類型、方法、來源和地區),2025 年至 2033 年2032 年數位廢棄物管理解決方案市場預測:按組件、廢棄物類型、方法、技術、應用、最終用戶和地區進行的全球分析

智慧廢棄物管理市場規模、佔有率、趨勢及預測(按成分、廢棄物類型、方法、來源和地區),2025 年至 2033 年2032 年數位廢棄物管理解決方案市場預測:按組件、廢棄物類型、方法、技術、應用、最終用戶和地區進行的全球分析 智慧廢棄物管理市場(全球)(2025-2029)

智慧廢棄物管理市場(全球)(2025-2029) 區塊鏈廢棄物追蹤市場:到 2033 年的市場分析和預測 - 按類型、按產品、按服務、按技術、按組件、按應用、按流程、按部署、按最終用戶、按解決方案

區塊鏈廢棄物追蹤市場:到 2033 年的市場分析和預測 - 按類型、按產品、按服務、按技術、按組件、按應用、按流程、按部署、按最終用戶、按解決方案 智慧廢棄物管理市場規模、佔有率、成長分析,按廢棄物類型、方法、來源、地區 - 產業預測,2024-2031

智慧廢棄物管理市場規模、佔有率、成長分析,按廢棄物類型、方法、來源、地區 - 產業預測,2024-2031