|

市場調查報告書

商品編碼

1524195

全球空調市場:市場佔有率分析、產業趨勢/統計、成長預測(2024-2029)Global Air Conditioner - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

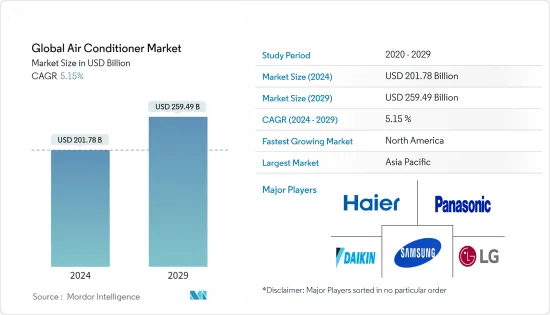

預計2024年全球空調市場規模為2017.8億美元,預計2029年將達2,594.9億美元,預測期(2024-2029年)複合年成長率為5.15%。

全球氣溫和濕度水平不斷上升,以及空調作為公共事業而非奢侈品的認知度不斷提高,預計將推動空調業務的顯著成長。由於配備空氣淨化系統和逆變器的型號等高性能空調的推出,空調市場預計在預測期內將成長。

全球供應鏈和市場需求受到了 COVID-19 疫情的影響。中國在空調市場中佔有重要地位。我們也向許多國家出口製造成品所需的各種原料。中國的企業倒閉迫使其他美國和歐洲空調製造商暫時停止最終產品生產。受此影響,市場供需失衡進一步擴大。

推動智慧空調市場的主要成長要素是智慧設備的日益普及,這些設備可以將傳統的遠端控制空調轉變為智慧設備。由於購物中心、辦公大樓和工業的開發許可率提高,預計箱型冷氣將適度成長,而住宅標準的提高將推動室內空調的需求。

空調市場趨勢

全球空調需求不斷擴大

全球空調需求的擴張是由多種因素共同推動的。由於氣候變遷和城市熱島效應導致的全球氣溫上升,增加了對空調的需求,以維持舒適的室內環境,特別是在炎熱的夏季。快速的都市化,特別是在新興經濟體,導致保溫現象普遍存在的都市區人口密度增加,進一步增加了住宅、商業和機構建築對空調的需求。人們對空調的舒適性和健康益處的了解不斷增加,包括改善室內空氣品質、管理濕度和緩解與炎熱相關的健康狀況,從而推動了住宅和商業環境對空調系統的需求。

辦公大樓、零售空間、醫療設施、資料中心和製造工廠對空調的需求不斷成長,推動市場成長,因為公司優先考慮員工舒適度、生產力和設備冷卻。政府努力提高能源效率和減少溫室氣體排放,透過法規、獎勵和能源效率標準鼓勵採用節能空調系統,這推動了市場需求。

亞太地區主導空調市場

快速都市化、氣溫上升、可支配收入增加以及對舒適解決方案的需求不斷增加等因素使亞太地區成為世界領先的市場之一。該地區由中國、印度、印尼和日本等人口稠密的國家組成。這些國家的人口成長和都市化不斷加快,住宅、商業和教育領域對空調系統的需求不斷增加。氣候變遷加劇了氣溫上升,推動了該地區對空調解決方案的需求。東南亞和南亞國家氣候炎熱潮濕,對提供舒適冷卻的空調系統的需求不斷增加。

推動市場成長的是空調系統的技術進步,例如變頻技術、智慧連網型功能和節能設計。這些進步提高了能源效率,降低了營業成本,並改善了用戶體驗,從而提高了採用率。例如,大金、三菱電機和Panasonic等公司提供採用變頻技術和智慧功能的先進空調系統,吸引了亞太地區的消費者。為了鼓勵採用節能模式,亞太地區許多國家都推出了能源效率標準和空調系統標籤計畫。例如,印度政府推出了節能建築規範(ECBC)和能源效率局(BEE)星級評定計劃,以推廣節能空調系統。

空調市場產業概況

空調市場競爭激烈。無數的選手在世界各地參加比賽。競爭格局的特點是成熟的跨國公司和區域參與者,每個公司都尋求透過技術創新、能源效率、產品功能和定價策略來實現其產品的差異化。主要參與者包括海爾集團、大金業、LG電子、三星電子、松下公司等。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態與洞察

- 市場概況

- 市場促進因素

- 氣溫上升和氣候變遷

- 逆變器技術、智慧功能、連網型功能等方面的創新。

- 市場限制因素

- 高能耗

- 初始成本和維護成本高

- 市場機會

- 節能空調系統的需求

- 空調系統與物聯網整合

- 價值鏈分析

- 產業吸引力波特五力分析

- 新進入者的威脅

- 買方議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭公司之間的敵對關係

- 洞察產業技術進步

- COVID-19 對市場的影響

第5章市場區隔

- 按類型

- 窗型冷氣

- 分離式/多聯機空調

- 箱型冷氣

- 可變冷媒流量 (VRF)

- 中央空調

- 其他

- 依技術

- 逆變器

- 非逆變器

- 按最終用戶

- 住宅

- 商業的

- 按分銷管道

- 多品牌商店

- 專賣店

- 網路商店

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 北美其他地區

- 歐洲

- 英國

- 德國

- 法國

- 俄羅斯

- 義大利

- 西班牙

- 其他歐洲國家

- 亞太地區

- 印度

- 中國

- 日本

- 澳洲

- 其他亞太地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東/非洲

- 阿拉伯聯合大公國

- 南非

- 其他中東/非洲

- 北美洲

第6章 競爭狀況

- 市場集中度概況

- 公司簡介

- Haier Group

- Daikin Industries

- LG Electronics

- Samsung Electronics

- Panasonic Corporation

- Mitsubishi Electric Corporation

- Carrier

- Hitachi Ltd.

- Whirlpool Corporation

- Toshiba Corporation*

第7章 市場機會及未來趨勢

第 8 章 免責聲明與出版商訊息

The Global Air Conditioner Market size is estimated at USD 201.78 billion in 2024, and is expected to reach USD 259.49 billion by 2029, growing at a CAGR of 5.15% during the forecast period (2024-2029).

The rising global temperatures and humidity levels and the growing recognition of air conditioners as a utility rather than luxury goods are predicted to drive significant growth in the air conditioning (AC) business. Driven by the introduction of sophisticated air conditioners, including models equipped with air purification systems and inverters, the AC market is anticipating growth in the forecast period.

The worldwide supply chain and market demand were both affected by the COVID-19 outbreak. China plays a significant role in the air conditioner market. Still, it also exports a variety of input supplies, which are needed to make finished items, to a wide range of nations. Due to the closure of their operations in China, other American and European air conditioning manufacturers have been forced to stop producing final goods temporarily. As a result, the market's imbalance between supply and demand widened.

The primary growth factor driving the smart air conditioner market is the growing adoption of smart devices that can transform traditional remote-controlled air conditioners into smart devices. While packaged air conditioners are expected to expand at a moderate rate due to rising permit rates for the development of malls, offices, and industries, the demand for room air conditioners is being driven by improvements in housing standards.

Air Conditioner Market Trends

Growing Demand for Air Conditioners Globally

The growing demand for air conditioners worldwide is propelled by a convergence of factors. Increasing global temperatures, attributed to climate change and urban heat island effects, are driving the need for air conditioning to maintain comfortable indoor environments, especially during hot summer months. Rapid urbanization, particularly in emerging economies, is leading to higher population densities in urban areas where heat retention is common, further increasing the demand for air conditioning in residential, commercial, and institutional buildings. The demand for air conditioning systems in both residential and commercial settings is being driven by the increased knowledge of the comfort and health benefits of air conditioning, including enhanced indoor air quality, humidity management, and relief from heat-related health conditions.

The increasing demand for air conditioning in office buildings, retail spaces, healthcare facilities, data centers, and manufacturing plants is driving market growth as businesses prioritize employee comfort, productivity, and equipment cooling. Government initiatives that aim to improve energy efficiency and reduce greenhouse gas emissions are encouraging the adoption of energy-efficient air conditioning systems through regulations, incentives, and energy efficiency standards, thereby driving market demand.

Asia-Pacific Dominating the Air Conditioner Market

Factors such as rapid urbanization, rise in temperatures, increase in disposable income, and increased demand for comfort solutions are driving the Asia-Pacific region to be one of the major markets worldwide. The region comprises some of the most densely populated countries, including China, India, Indonesia, and Japan. Increased population growth and urbanization in these countries have led to an increase in demand for air conditioning systems in the residential, business, and educational sectors. Rising temperatures, exacerbated by climate change, are driving the region's need for air conditioning solutions. Southeast and South Asian countries experience scorching and humid climates, leading to higher demand for air conditioning systems to provide comfortable cooling.

The growth of the market is driven by technological advances in air conditioning systems, such as inverter technology, intelligent and connected features, and energy-efficient designs. These advancements improve energy efficiency, reduce operating costs, and enhance user experience, leading to higher adoption rates. For example, companies like Daikin, Mitsubishi Electric, and Panasonic offer advanced air conditioning systems with inverter technology and smart features that appeal to consumers in the Asia-Pacific region. In order to encourage the adoption of energy-efficient models, a number of countries in the Asia-Pacific region have introduced Energy Efficiency Standards and Air Conditioning System Labelling Programmes. For example, the Indian government has introduced the Energy Conservation Building Code (ECBC) and the Bureau of Energy Efficiency (BEE) star rating program to promote energy-efficient air conditioning systems.

Air Conditioner Market Industry Overview

The market for air conditioners is highly competitive. There are a number of players competing around the world. The competitive landscape is characterized by both established multinational corporations and regional players, each striving to differentiate their products through innovation, energy efficiency, product features, and pricing strategies. Major players include Haier Group, Daikin Industries, LG Electronics, Samsung Electronics, and Panasonic Corporation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS AND INSIGHTS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Temperatures and Climate Change

- 4.2.2 Technological Innovations such as Inverter Technology, Smart and Connected Features

- 4.3 Market Restraints

- 4.3.1 High Energy Consumption

- 4.3.2 High Initial and Maintenance Costs

- 4.4 Market Opportunities

- 4.4.1 Demand for Energy-Efficient Air Conditioning Systems

- 4.4.2 Integration of Air Conditioning Systems with loT

- 4.5 Value Chain Analysis

- 4.6 Industry Attractiveness: Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Insights into Technological Advancements in the Industry

- 4.8 Impact of COVID-19 on the Market

5 MARKET SEGMENTATION

- 5.1 By Type

- 5.1.1 Window AC

- 5.1.2 Split and Multi-Split AC

- 5.1.3 Packaged AC

- 5.1.4 Variable Refrigerant Flow (VRF)

- 5.1.5 Central AC

- 5.1.6 Others

- 5.2 By Technology

- 5.2.1 Inverter

- 5.2.2 Non-Inverter

- 5.3 By End-User

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.4 By Distribution Channel

- 5.4.1 Multi-Brand stores

- 5.4.2 Exclusive Stores

- 5.4.3 Online Stores

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Russia

- 5.5.2.5 Italy

- 5.5.2.6 Spain

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 India

- 5.5.3.2 China

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle-East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration Overview

- 6.2 Company Profiles

- 6.2.1 Haier Group

- 6.2.2 Daikin Industries

- 6.2.3 LG Electronics

- 6.2.4 Samsung Electronics

- 6.2.5 Panasonic Corporation

- 6.2.6 Mitsubishi Electric Corporation

- 6.2.7 Carrier

- 6.2.8 Hitachi Ltd.

- 6.2.9 Whirlpool Corporation

- 6.2.10 Toshiba Corporation*

7 MARKET OPPORTUNTIES AND FUTURE TRENDS

8 DISCLAIMER AND ABOUT US

中國的空調市場:2024年

中國的空調市場:2024年 空調管道市場報告:2030 年趨勢、預測與競爭分析

空調管道市場報告:2030 年趨勢、預測與競爭分析 空調系統市場:按類型、最終用途分類 - 2025-2030 年全球預測

空調系統市場:按類型、最終用途分類 - 2025-2030 年全球預測 空調市場:按類型、容量、安裝類型、冷媒類型、應用、分銷管道 - 2025-2030 年全球預測

空調市場:按類型、容量、安裝類型、冷媒類型、應用、分銷管道 - 2025-2030 年全球預測 智慧空調市場 - 全球產業規模、佔有率、趨勢、機會和預測,按類型、應用、銷售通路、地區和競爭細分,2019-2029F

智慧空調市場 - 全球產業規模、佔有率、趨勢、機會和預測,按類型、應用、銷售通路、地區和競爭細分,2019-2029F 空調設備市場:按產品類型、冷凍能力、技術、分銷管道、安裝類型、最終用戶 - 2025-2030 年全球預測

空調設備市場:按產品類型、冷凍能力、技術、分銷管道、安裝類型、最終用戶 - 2025-2030 年全球預測 盒式空調市場機會、成長動力、產業趨勢分析與預測 2024 - 2032

盒式空調市場機會、成長動力、產業趨勢分析與預測 2024 - 2032 空調設備:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029)

空調設備:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029) 空調座椅市場報告:2030 年趨勢、預測與競爭分析

空調座椅市場報告:2030 年趨勢、預測與競爭分析 全球分離式空調市場評估:按產品類型、按容量、按技術、按價格範圍、按最終用戶、按分銷管道、按地區、機會、預測,2017-2031 年

全球分離式空調市場評估:按產品類型、按容量、按技術、按價格範圍、按最終用戶、按分銷管道、按地區、機會、預測,2017-2031 年