|

市場調查報告書

商品編碼

1536811

資安管理服務-市場佔有率分析、產業趨勢/統計、成長預測(2024-2029)Managed Security Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

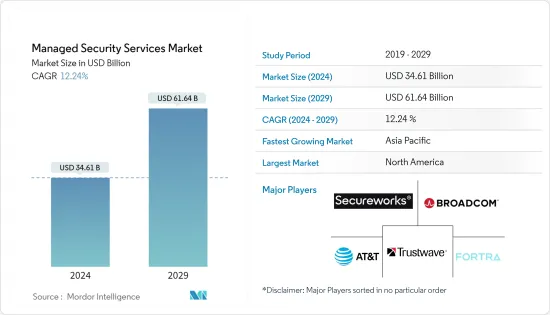

資安管理服務市場規模預計到 2024 年為 346.1 億美元,預計到 2029 年將達到 616.4 億美元,在預測期內(2024-2029 年)複合年成長率為 12.24%。

該市場的成長是由雲端儲存的日益普及、巨量資料分析的出現以及由於物聯網的採用而導致的IT基礎設施日益複雜性所推動的。然而,這些進步也透過擴大攻擊面而增加了網路威脅的風險。

主要亮點

- 資安管理服務將網路安全外包給專業提供者。由於維護強大的安全基礎設施的複雜性以及專家監督的需要,組織通常選擇資安管理服務提供者 (MSSP)。資料外洩成本的上升進一步強調了這種需求,如附圖所示。儘管傳統安全解決方案已經發展,但偵測新的非檔案式威脅仍然很困難,從而推動了對資安管理服務的需求。

- 全球數位化趨勢為網路犯罪分子提供了利用線上系統、網路和基礎設施弱點的機會。這對世界各地的政府、企業和個人有重大的經濟和社會影響。網路釣魚、勒索軟體和資料外洩已經是常見的網路威脅,但新型網路犯罪不斷出現。

- 數位轉型時代刺激了資料密集型應用和技術的擴展,導致企業產生和處理的資料的數量、速度和種類顯著激增。隨著組織利用巨量資料、人工智慧和機器學習的潛力,保護這項寶貴資產變得至關重要。隨著對資料集中方法的日益依賴,組織必須管理包含敏感資訊的大型資料集,這凸顯了對強大網路安全措施的需求。

- 隨著網路威脅變得更加複雜,公司擴大外包其安全業務。選擇建立內部安全營運中心 (SOC) 還是委託它會產生重大影響。因為滲透業務系統的單一惡意程式碼案例可能會給整個組織帶來災難。

- COVID-19 大流行不僅擾亂了全球業務,而且數位化轉型的推動也加速了私營和政府部門網路犯罪活動的活性化。這次疫情導致的網路攻擊激增,為端點偵測和回應解決方案打開了大門,以幫助降低網路風險。因此,這些解決方案的市場在大流行期間和之後都顯示出成長。

- 此外,網路流量的增加顯著增加了各種企業遭受網路攻擊的風險,因此需要實施資安管理服務。防火牆管理和端點安全的進步,加上疫情爆發以來網路攻擊的激增,進一步推動了資安管理服務市場。

資安管理服務市場的趨勢

BFSI 領域作為最終用戶產業正在快速發展

- 資安管理服務可能會主導 BFSI 領域,主要是因為它們在保護敏感資料和增強整體安全性方面發揮作用。這些服務在 BFSI 領域的主要優勢在於,它們提供全天候監控,並在發生違規情況時實現快速事件回應和補救。

- 由於 BFSI 部門專注於保護客戶資料,資安管理服務的採用量顯著增加。此舉旨在加強線上服務的安全性,抵禦網路攻擊的興起。

- 在當今的數位環境中,BFSI 公司必須採用先進的即時安全措施。這包括端點檢測和回應(EDR)、生物識別技術、雲端安全、程式碼審核、嵌入式系統安全評估、整合安全解決方案、網路情報、多因素身份驗證、安全培訓、行為分析等。

- 在世界各地的金融機構都在加強網路威脅預防策略的同時,印度 BFSI 正在強調網路安全的重要性和影響。安全漏洞、資料竊取和密碼外洩等常見網路攻擊給這些公司帶來了重大擔憂。隨著新技術和熟練犯罪者不斷發展的網路犯罪格局凸顯了印度 BFSI 領域當前網路安全方法的局限性。

- 分散式阻斷服務 (DDoS) 攻擊在 BFSI 領域迅速增加,使得資安管理服務變得越來越重要,尤其是在 DDoS 緩解領域。 2023 年 9 月,領先的網路安全供應商 Akamai 成功挫敗了針對美國金融機構的大規模 DDoS 攻擊。這一事件凸顯了 BFSI 威脅的升級,塑造了防禦 DDoS 攻擊的資安管理服務市場。

- 隨著惡意軟體類型的發展,對檢測解決方案的需求也不斷成長。據 Zimperium 稱,截至 2023 年,Godfather 銀行惡意軟體有 1,171 個變種。截至 2023 年,Nexus 惡意軟體排名第一,約有 500 種變種,Saderat 排名第一,約有 300 種變種。總體而言,排名前五的惡意軟體家族有 50 多個變體。

- BFSI 領域網路攻擊的頻率不斷增加,增加了資安管理服務的需求。在日益互聯的數位化金融生態系統中,這些服務在保護金融系統、客戶資料和相關人員之間的信任方面發揮關鍵作用。這種不斷成長的需求預計將在未來幾年推動市場成長。

預計北美將佔據較大市場佔有率

- 北美地區正在經歷新興技術的重大整合,簡化 IT 功能的需求正在迅速增加。該地區越來越多的企業發現,在資安管理服務提供者的幫助下可以更輕鬆地滿足這一需求,這將推動未來的業務成長。

- 在美國,智慧型手機和平板裝置越來越普及,BYOD(自帶裝置)政策推廣的可能性很高。該全部區域不斷上升的設備普及率和強大的網路連接正在推動組織採用 BYOD 政策,增加業務生態系統中的網路攻擊風險,並推動該地區未來對資安管理服務的需求。

- 此外,物聯網在各個行業和部門的快速整合預計將提高這些智慧設備的普及率。預計這將推動資安管理服務的採用和實施,從而刺激市場成長。

- 多重雲端環境的使用在美國正在迅速擴大,客戶主要依賴一種雲,偶爾使用其他雲。資安管理服務提供者 (MSSP) 可以透過提供基於消費的定價模式來利用這一機會。

- 此外,美國預計將擴大利用公共雲端和 IT 營運管理 (ITOM) 工具的託管服務,推動雲端和本地 ITOM 訂閱業務設計的成長。儘管如此,本地部署預計將成為最常見的交付方法。

- 該地區還面臨大量的 DDoS 攻擊,這些攻擊可能會隨著多個最終用戶產業的增加而增加,進一步增加對 DDoS 防護解決方案的需求。此外,該地區的網路攻擊正在迅速增加,尤其是在美國。該地區的數字龐大,主要是由於連網設備數量的快速成長。

資安管理服務產業概述

由於跨國公司和中小企業的存在,資安管理服務市場高度分散。該市場的主要參與者包括 AT&T Inc.、SecureWorks Corp.、Broadcom Inc.、Trustwave Holdings Inc. (Chertoff Group) 和 Fortra LLC。市場參與者正在採取聯盟和收購等策略來加強其產品供應並獲得永續的競爭優勢。

- 2023 年 11 月 - AT&T 宣布達成協議,創建獨立管理的保全服務業務,並由芝加哥投資者 WillJam Ventures 參股該業務。新的網路安全合資企業將持有託管安全業務、精選安全軟體解決方案和安全諮詢資源。

- 2023 年 10 月 - Trustwave Holdings Inc. 宣布推出適用於 Microsoft Sentinel 的 Trustwave 託管 SIEM。 Trustwave 的最新服務旨在協助使用 Microsoft Sentinel 的企業改善安全功能、最佳化投資收益並加快回應時間。

其他好處:

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場洞察

- 市場概況

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 買方議價能力

- 新進入者的威脅

- 競爭公司之間的敵對關係

- 替代品的威脅

第5章市場動態

- 市場促進因素

- 網路犯罪增加、數位破壞和合規要求提高

- 對早期威脅偵測和情報的需求推動了市場成長

- 市場限制因素

- 保全服務意識缺失阻礙因素市場拓展

- MSSP領域的演變和主要趨勢

- COVID-19 對市場的影響

第6章 市場細分

- 依部署類型

- 本地

- 雲

- 按解決方案類型

- 入侵偵測/預防

- 威脅防禦

- 分散式阻斷服務

- 防火牆管理

- 端點安全

- 風險評估

- 資安管理服務提供者

- IT服務供應商

- 安全管理專家

- 電信服務供應商

- 按最終用戶產業

- BFSI

- 政府/國防

- 零售

- 製造業

- 醫療保健/生命科學

- 資訊科技和電訊

- 其他最終用戶產業

- 按地區

- 北美洲

- 歐洲

- 亞洲

- 澳洲/紐西蘭

- 拉丁美洲

- 中東/非洲

第7章 競爭格局

- 公司簡介

- AT&T Inc.

- Secureworks Corp.

- Broadcom Inc.

- Trustwave Holdings Inc.(the Chertoff Group)

- Fortra LLC

- IBM Corporation

- Verizon Communications Inc.

- Lumen Technologies Inc.

- BAE Systems PLC

- Atos SE

- Capgemini SE

- Wipro Limited

- Fujitsu Limited(Fujitsu Group)

第8章供應商定位分析

第9章投資分析及市場展望

The Managed Security Services Market size is estimated at USD 34.61 billion in 2024, and is expected to reach USD 61.64 billion by 2029, growing at a CAGR of 12.24% during the forecast period (2024-2029).

The market's growth can be attributed to the rising adoption of cloud storage, the emergence of big data analytics, and the increasing complexity of IT infrastructures due to IoT adoption. However, these advancements also heighten the risk of cyber threats, given the expanded attack surface.

Key Highlights

- Managed security services involve outsourcing network security to specialized providers. Organizations often opt for managed security service providers (MSSPs) due to the complexity of maintaining a robust security infrastructure and the need for expert monitoring. This need is further underscored by the rising costs of data breaches, as evident from the accompanying graph. While traditional security solutions have evolved, they still struggle to detect newer, non-file-based threats, fueling the demand for managed security services.

- The global digitalization trend has provided cybercriminals with opportunities to exploit weaknesses in online systems, networks, and infrastructure. This has had significant economic and social repercussions on governments, businesses, and individuals worldwide. While phishing, ransomware, and data breaches are already prevalent cyber threats, new types of cybercrimes continue to emerge.

- The digital transformation era has fueled the expansion of data-intensive applications and technologies, resulting in a significant surge in the volume, velocity, and variety of data generated and processed by businesses. As organizations harness the potential of Big Data, artificial intelligence, and machine learning, securing this valuable asset becomes paramount. With the growing reliance on data-intensive approaches, organizations must manage large datasets containing sensitive information, underscoring the need for robust cybersecurity measures.

- The rising complexity of cyber threats is driving organizations to increasingly outsource their security operations. Choosing between an internal or outsourced Security Operations Center (SOC) carries significant consequences, as a single instance of malicious code infiltrating a business system can now spell the demise of the entire organization.

- The COVID-19 pandemic has not only disrupted businesses globally but has also expedited the rise of cybercriminal activities, both in private enterprises and government sectors, due to the push for digital transformation. This surge in cyberattacks during the pandemic has opened up avenues for endpoint detection and response solutions, given their effectiveness in mitigating cyber risks. As a result, the market for these solutions witnessed growth both during and after the pandemic.

- Additionally, the heightened internet traffic has significantly amplified the risk of cyberattacks across various businesses, necessitating the adoption of managed security services. The market for managed security services has further been propelled by advancements like firewall management and endpoint security, coupled with the surge in cyberattacks since the onset of the pandemic.

Managed Security Services Market Trends

BFSI Sector to be the Fastest-growing End-user Industry

- Managed security services are set to dominate the BFSI sector, primarily due to their role in safeguarding sensitive data and bolstering overall security. A key advantage of these services in the BFSI space is their round-the-clock monitoring, enabling swift incident response and remediation in case of breaches.

- Given the BFSI sector's focus on safeguarding client data, there has been a notable surge in the adoption of managed security services. This move is aimed at bolstering the security of online services against the rising tide of cyberattacks.

- In today's digital landscape, BFSI firms must employ advanced real-time security measures. These include endpoint detection and response (EDR), biometric technology, cloud security, code audit, embedded system security assessment, integrated security solutions, cyber intelligence, multi-factor authentication, security training, and behavioral analytics, among others.

- While financial institutions worldwide are enhancing their cyber threat prevention strategies, BFSI entities in India are grappling with the significance and repercussions of cybersecurity. Common cyberattacks like security breaches, data thefts, and password compromises pose significant concerns for these firms. The evolving cybercrime landscape, with its new techniques and skilled perpetrators, underscores the limitations of current cybersecurity approaches in India's BFSI realm.

- The BFSI sector is witnessing a surge in distributed denial of service (DDoS) attacks, amplifying the significance of managed security services, particularly in the realm of DDoS mitigation. Notably, in September 2023, Akamai, a leading cybersecurity provider, successfully thwarted a major DDoS attack on a US financial institution. This incident underscores the escalating threat landscape for BFSIs, creating a ripe market for managed security services to fortify against DDoS assaults.

- As malware types evolve, the need for detection solutions intensifies. According to Zimperium, in 2023, the banking malware Godfather had 1,171 known variants. As of 2023, Nexus malware ranked first, with approximately 500 variants, while Saderat had around 300 types. Overall, the top five malware families had over 50 variants.

- The mounting frequency of cyberattacks in the BFSI sector is driving up the demand for managed security services. These services play a pivotal role in safeguarding financial systems, customer data, and the overall trust of stakeholders in an increasingly interconnected and digitized financial ecosystem. This heightened demand is poised to propel the market growth in the coming years.

North America is Expected to Hold Significant Market Share

- The North American region has been witnessing a significant integration of modern technology, and the need for streamlined IT functions is growing rapidly, with an increasing number of businesses in the region finding it easy to keep pace with that with the help of managed security service providers, which is driving the business growth in the future.

- The penetration of smartphones and tablets is increasing in the United States, which will likely drive the bring your own device (BYOD) policy. The increasing penetration of devices and strong network connectivity across the region are expected to encourage organizations to adopt BYOD policies, raising the risk of cyberattacks in the business ecosystems and supporting the demand for managed security services in the region in the future.

- Furthermore, the penetration of these smart devices is expected to increase due to the rapid integration of IoT across various industries and sectors. This is expected to propel the adoption and incorporation of managed security services, thereby fueling the market's growth.

- The use of multi-cloud environments is experiencing massive growth in the United States, wherein clients rely majorly on one cloud while using the other sporadically. Here, managed security service providers (MSSPs) can avail of the opportunity by offering consumption-based pricing models.

- Moreover, in the United States, public cloud and managed services are expected to be leveraged more often for IT operations management (ITOM) tools, encouraging the growth of the subscription business design for both cloud and on-premises ITOM. Despite this, on-premises deployments are expected to be the most popular delivery method.

- The region also faces a significant number of DDoS attacks, which are likely to increase with respect to multiple end-user industries, further driving the demand for DDoS protection solutions. Moreover, cyberattacks in the region, especially in the United States, are increasing rapidly. They are reaching high numbers, primarily due to the rapidly increasing number of connected devices in the region.

Managed Security Services Industry Overview

The managed security services market is highly fragmented due to the presence of both global players and small- and medium-sized enterprises. Some of the major players in the market are AT&T Inc., SecureWorks Corp., Broadcom Inc., Trustwave Holdings Inc. (the Chertoff Group), and Fortra LLC. Players in the market are adopting strategies such as partnerships and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

- November 2023 - AT&T announced an agreement to create a standalone managed cybersecurity services business and a capital investment in that business from a Chicago-based investor - WillJam Ventures. Expected to close in 1Q24, the newly managed cybersecurity joint venture will hold associated managed security operations, select security software solutions, and security consulting resources.

- October 2023 - Trustwave Holdings Inc. announced the launch of Trustwave Managed SIEM for Microsoft Sentinel. Trustwave's latest offering is designed to help businesses using Microsoft Sentinel with improved security capabilities, optimized return on investment, and rapid response times.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Intensity of Competitive Rivalry

- 4.2.5 Threat of Substitutes

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rising Cyber Crime, Digital Disruption, and Increased Compliance Demands

- 5.1.2 Need for Threat Detection and Intelligence at an Early Stage Driving the Market Growth

- 5.2 Market Restraints

- 5.2.1 Lack of Awareness of Security Services is Discouraging the Market Expansion

- 5.3 Evolution and Key Trends in the MSSP Space

- 5.4 Impact of COVID-19 on the Market

6 MARKET SEGMENTATION

- 6.1 By Deployment Type

- 6.1.1 On-premise

- 6.1.2 Cloud

- 6.2 By Solution Type

- 6.2.1 Intrusion Detection and Prevention

- 6.2.2 Threat Prevention

- 6.2.3 Distributed Denial of Services

- 6.2.4 Firewall Management

- 6.2.5 End-point Security

- 6.2.6 Risk Assessment

- 6.3 By Managed Security Service Provider

- 6.3.1 IT Service Providers

- 6.3.2 Managed Security Specialist

- 6.3.3 Telecom Service Provider

- 6.4 By End-user Industry

- 6.4.1 BFSI

- 6.4.2 Government and Defense

- 6.4.3 Retail

- 6.4.4 Manufacturing

- 6.4.5 Healthcare and Life Sciences

- 6.4.6 IT and Telecom

- 6.4.7 Other End-user Verticals

- 6.5 By Geography***

- 6.5.1 North America

- 6.5.2 Europe

- 6.5.3 Asia

- 6.5.4 Australia and New Zealand

- 6.5.5 Latin America

- 6.5.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles*

- 7.1.1 AT&T Inc.

- 7.1.2 Secureworks Corp.

- 7.1.3 Broadcom Inc.

- 7.1.4 Trustwave Holdings Inc. (the Chertoff Group)

- 7.1.5 Fortra LLC

- 7.1.6 IBM Corporation

- 7.1.7 Verizon Communications Inc.

- 7.1.8 Lumen Technologies Inc.

- 7.1.9 BAE Systems PLC

- 7.1.10 Atos SE

- 7.1.11 Capgemini SE

- 7.1.12 Wipro Limited

- 7.1.13 Fujitsu Limited (Fujitsu Group)

8 VENDOR POSITIONING ANALYSIS

9 INVESTMENT ANALYSIS AND MARKET OUTLOOK

全球託管安全服務市場:產業分析、規模、佔有率、成長、趨勢、預測(2024-2033)

全球託管安全服務市場:產業分析、規模、佔有率、成長、趨勢、預測(2024-2033) 資安管理服務市場:按產品類型、部署和行業分類 - 2025-2030 年全球預測

資安管理服務市場:按產品類型、部署和行業分類 - 2025-2030 年全球預測 到 2030 年資安管理服務市場預測:按安全類型、公司規模、部署類型、應用程式、最終用戶和地區進行的全球分析

到 2030 年資安管理服務市場預測:按安全類型、公司規模、部署類型、應用程式、最終用戶和地區進行的全球分析 託管安全服務市場 - 全球產業規模、佔有率、趨勢、機會和預測,按安全性、服務、企業規模、垂直行業、地區和競爭細分,2019-2029F

託管安全服務市場 - 全球產業規模、佔有率、趨勢、機會和預測,按安全性、服務、企業規模、垂直行業、地區和競爭細分,2019-2029F 全球資安管理服務市場:市場規模、佔有率、趨勢分析報告 - 按公司規模、按服務、按安全、按行業、按地區、展望、預測,2024-2031年

全球資安管理服務市場:市場規模、佔有率、趨勢分析報告 - 按公司規模、按服務、按安全、按行業、按地區、展望、預測,2024-2031年 全球資安管理服務(MSS) 市場,2024-2028

全球資安管理服務(MSS) 市場,2024-2028 託管安全服務市場:依類型、安全類型、部門、地區劃分 - 到2030年的全球預測

託管安全服務市場:依類型、安全類型、部門、地區劃分 - 到2030年的全球預測 2024-2026 年美洲資安管理服務市場成長機會

2024-2026 年美洲資安管理服務市場成長機會 歐洲資安管理服務(MSS) 市場的成長機會

歐洲資安管理服務(MSS) 市場的成長機會 2023-2030 年全球託管安全服務市場規模研究與預測(依安全類型、服務、企業規模、垂直產業和區域分析)

2023-2030 年全球託管安全服務市場規模研究與預測(依安全類型、服務、企業規模、垂直產業和區域分析)