|

市場調查報告書

商品編碼

1536816

雙酚(BPA):市場佔有率分析、產業趨勢/統計、成長預測(2024-2029)Bisphenol A (BPA) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

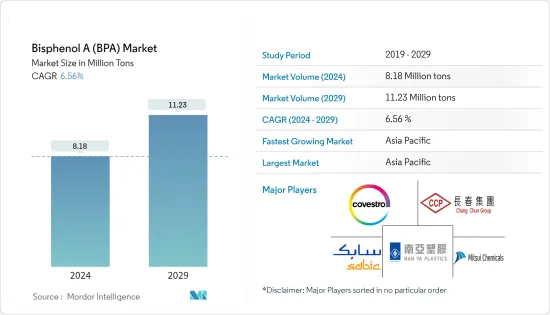

預計2024年全球雙酚(BPA)市場規模為818萬噸,預計2029年將達1123萬噸,2024-2029年預測期間複合年成長率為6.56%。

主要亮點

- 從中期來看,聚碳酸酯產業需求的成長和環氧樹脂生產需求的增加可能會推動雙酚(BPA)的需求。

- 然而,食品和飲料行業對雙酚 (BPA) 使用的日益嚴格的監管是所研究市場成長的主要限制因素。

- 同時,生物基雙酚(BPA)的潛在市場需求可能會在未來幾年創造利潤豐厚的市場機會。

- 亞太地區在市場上佔據主導地位,預計在預測期內仍將保持最高的複合年成長率。

雙酚(BPA)市場趨勢

聚碳酸酯樹脂需求增加

- 聚碳酸酯主要是透過雙酚(BPA)和碳醯氯的界面反應生產的。在所有其他應用領域中,聚碳酸酯樹脂的應用導致了雙酚(BPA)的巨大市場需求。

- 雙酚(BPA)在增強聚碳酸酯樹脂性能方面發揮重要作用。 BPA 有助於提高聚碳酸酯樹脂的強度和耐久性。含有 BPA 的聚碳酸酯以其抗衝擊性而聞名,使其適用於安全玻璃、防彈窗和醫療設備等應用。

- 含有BPA的聚碳酸酯具有較高的玻璃化轉變溫度,可以承受高溫而不變形或熔化。這項特性使其成為食品容器和可重複使用水瓶的理想選擇。

- 聚碳酸酯天然透明,BPA 有助於維持這種透明度。因此,可以製造透明容器和透鏡。

- 聚碳酸酯是一種高性能熱塑性塑膠,廣泛用於建築應用。使用聚碳酸酯製造的板材廣泛用作各種窗戶和天窗應用中的玻璃替代品。此外,它還用於桶形拱頂、不透明覆層層板、座艙罩、建築幕牆和標誌、半透明牆壁、體育場屋頂、百葉窗和屋頂圓頂。

- 近年來,聚碳酸酯材料在溫室中的使用增加。德國、法國、荷蘭、西班牙等歐洲國家都有大面積的溫室種植。

- 聚碳酸酯市場的主要企業包括三菱工程塑膠公司、科思創公司、SABIC、樂天化學公司和帝人有限公司。這些公司正在大力投資併購和擴張,預計將推動聚碳酸酯中雙酚A的需求。例如,2024 年 3 月,全球領先的優質聚合物材料生產商之一科思創股份公司 (Covestro AG) 在比利時安特衛普運作了第一家工廠,以工業規模生產聚碳酸酯共聚物。

- 2023年9月,沙烏地阿拉伯化學巨頭SABIC和中國石油燃氣公司中國石化宣布,其合資企業中國石化SABIC天津石化(SSTPC)將建造一座新的聚碳酸酯(PC)工廠。新的PC工廠產能為每年260噸,是SABIC在中國PC成長策略的核心,並為與全球和本地客戶提供進一步的合作機會。

- 2023年3月,科思創擴大了在泰國的聚碳酸酯薄膜產能。聚碳酸酯薄膜主要用於身分證、汽車顯示器以及電氣和電子應用。這使得該公司的額外產能達到每年10萬噸以上。

- 因此,預計上述因素將影響預測期內聚碳酸酯應用中雙酚A的需求。

亞太地區預計將主導市場

- 亞太地區是各個終端用戶產業中最大的雙酚 (BPA) 生產國和消費國。因此,預計它將主導市場。

- 近年來,受各種經濟和產業因素的影響,全國各地對新型雙酚(BPA)生產裝置的投資增加趨勢明顯。例如,2024年1月,台塑集團子公司南亞塑膠位於中國寧波的BPA生產工廠重新啟動營運。該廠每年生產約 17 萬噸 BPA。本公司生產的BPA主要用於聚碳酸酯樹脂。

- 由於雙酚 A 在汽車、電子和建築等行業的使用不斷增加,中國對聚碳酸酯樹脂和塑膠產品中的雙酚 A 的需求不斷增加。 2023 年 9 月,沙烏地化學公司 SABIC 和中國石油燃氣公司中國石化宣布透過其合資企業中國石化 SABIC 天津石化 (SSTPC)推出新的聚碳酸酯 (PC) 工廠。 SABIC 在 SSTPC 生產的 PC 材料組合將以 Lexan 樹脂品牌銷售。

- 印度長期以來一直進口BPA,價格波動和區域間貿易問題給印度BPA市場帶來挑戰。政府和一些公司已採取措施在印度生產雙酚 A。例如,Deepak Chem Tech Limited於2024年2月與古吉拉突邦政府簽署了合作備忘錄,擬在古吉拉突邦Dahej建立計劃,投資金額約為900億印度盧比。該公司計劃建造聚碳酸酯樹脂等先進聚合物樹脂的全球生產設施。

- 近年來,由於競爭激烈、收益微薄,日本BPA生產工廠出現倒閉趨勢,對產業造成重大影響。例如,日本三菱化學於 2024 年 2 月宣布,計劃在 2024 年 3 月底前永久停止其位於日本南部福岡縣黑崎工廠的 BPA 生產,主要原因是來自中國的供應過剩。該廠每年生產約 12 萬噸 BPA。

- 因此,上述因素預計將影響亞太地區對BPA的需求。

雙酚 (BPA) 產業概覽

雙酚 (BPA) 市場因其性質而部分整合。市場主要企業(排名不分先後)包括科思創公司、SABIC、長春集團、三井化學公司和南亞塑膠公司。

其他好處:

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 調查先決條件

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 促進因素

- 聚碳酸酯領域需求快速成長

- 環氧樹脂需求增加

- 抑制因素

- 食品和飲料行業的法規收緊

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 買方議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

- 原料分析

- 技術簡介

- 貿易概況

- 價格概覽

- 監理政策分析

第5章市場區隔(市場規模:基於數量)

- 按用途

- 聚碳酸酯樹脂

- 環氧樹脂

- 不飽和聚酯樹脂

- 阻燃劑

- 其他用途

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 東南亞國協

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 義大利

- 法國

- 西班牙

- 歐洲其他地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東/非洲

- 沙烏地阿拉伯

- 南非

- 其他中東/非洲

- 亞太地區

第6章 競爭狀況

- 合併、收購、合資、合作夥伴關係和協議

- 市場佔有率(%)分析

- 主要企業策略

- 公司簡介

- Altivia Petrochemicals

- Chang Chun Group

- China National Bluestar(Group)Co. Ltd

- China Petroleum & Chemical Corporation(SINOPEC)

- Covestro AG

- Dow

- Hexion

- Idemitsu Kosan Co. Ltd

- Kumho P&B Chemicals Inc.

- LG Chem

- Lihua Yiweiyuan Chemical Co. Ltd

- Mitsubishi Chemical Corporation

- Mitsui Chemicals Inc.

- Nan Ya Plastics Industry Co. Ltd

- Nippon Steel Chemical & Material Co. Ltd

- PTT Phenol Company Limited

- SABIC

- Samyang Holdings Corporation

- Teijin Limited

- Zhejiang Petroleum & Chemical Co. Ltd

第7章 市場機會及未來趨勢

- 生物基BPA的潛在市場需求

簡介目錄

Product Code: 48890

The Bisphenol A Market size is estimated at 8.18 Million tons in 2024, and is expected to reach 11.23 Million tons by 2029, growing at a CAGR of 6.56% during the forecast period (2024-2029).

Key Highlights

- In the medium term, soaring demand from the polycarbonate sector and increasing demand for epoxy resin production are likely to drive the demand for Bisphenol-A.

- However, increasing regulations in the food and beverage industry on the use of Bisphenol-A pose major restraints to the growth of the market studied.

- On the other hand, potential market demand for bio-based Bisphenol-A is likely to create lucrative market opportunities in the coming years.

- Asia-Pacific is expected to dominate the market and is anticipated to witness the highest CAGR during the forecast period.

Bisphenol-A Market Trends

Increasing Demand for Polycarbonate Resins

- Polycarbonate is mainly formed after the reaction of Bisphenol-A with carbonyl chloride in an interfacial process. Among all other application areas, polycarbonate resin application provides a significant market demand for Bisphenol-A (BPA).

- Bisphenol-A plays a critical role in enhancing the properties of polycarbonate resins. BPA contributes to the strength and durability of polycarbonate plastics. Polycarbonates made with BPA are known for their impact resistance, which makes them suitable for applications such as safety glasses, bulletproof windows, and medical devices.

- Polycarbonates containing BPA have a high glass transition temperature, meaning they can withstand high temperatures without warping or melting. This property makes them ideal for food containers and reusable water bottles.

- Polycarbonates are naturally transparent, and BPA helps to maintain this clarity. This allows the production of clear containers and lenses.

- Polycarbonates are high-performing thermoplastics that are widely used in construction applications. Sheets manufactured using Polycarbonates are widely used as a substitute for glass in a variety of window and skylight applications. Additionally, they are used as barrel vaults, opaque cladding panels, canopies, facades and signage, translucent walls, sports stadium roofs, louvers, and roof domes.

- The application of polycarbonate materials in greenhouses has increased in recent years. European countries, such as Germany, France, the Netherlands, and Spain, have larger areas for greenhouse cultivation.

- Some of the key companies in the polycarbonate market include Mitsubishi Engineering-Plastics Corporation, Covestro AG, SABIC, Lotte Chemical Corporation, and Teijin Limited. These companies are investing heavily in mergers, acquisitions, and expansion, which are projected to boost the demand for BPA in polycarbonates. For instance, in March 2024, Covestro AG, one of the world's leading manufacturers of high-quality polymer materials, inaugurated its first plant to produce polycarbonate copolymers on an industrial scale at its Antwerp, Belgium site.

- In September 2023, Saudi Arabian chemical giant SABIC and Chinese oil and gas corporation Sinopec announced the launch of a new polycarbonate (PC) plant through their joint venture named Sinopec SABIC Tianjin Petrochemical (SSTPC). With an annual designed capacity of 260 kilotons, the new PC plant is intended as a central piece of SABIC's PC growth strategy in China, providing opportunities for further collaborations with global and local customers.

- In March 2023, Covestro expanded its production capacity for polycarbonate films in Thailand, primarily used in identity documents, automotive displays, and electrical and electronic applications. With these developments, the company's additional capacity now exceeds 100,000 metric tons annually.

- Therefore, the factors mentioned above are expected to impact the demand for BPA in polycarbonate applications during the forecast period.

Asia-Pacific is Expected to Dominate the Market

- Asia-Pacific is the largest manufacturer and consumer of Bisphenol-A (BPA) in different end-user industries. Hence, it is expected to dominate the market.

- In recent years, there has been a noticeable trend of increasing investments in new Bisphenol-A (BPA) production facilities across China, driven by various economic and industrial factors. For instance, in January 2024, Nan Ya Plastics, a subsidiary of Formosa Group, restarted operations of the BPA production plant in Ningbo, China. This plant produces about 170,000 tons of BPA per annum. The BPA produced by the company is majorly used in the polycarbonate resins that the company produces.

- The demand for BPA in polycarbonate resins and plastic products in China is growing due to its expanding use in industries like automotive, electronics, and construction. In September 2023, Saudi Arabian chemical company SABIC and Chinese oil and gas corporation Sinopec announced the launch of a new polycarbonate (PC) plant through their joint venture, Sinopec SABIC Tianjin Petrochemical (SSTPC). SABIC's portfolio of PC materials produced at SSTPC is marketed under its Lexan resin brand.

- India has been importing BPA for a long time, and the fluctuations in prices and trade issues among the regions are creating a problem for the Indian BPA market. The government and a few companies have taken initiatives to manufacture BPA in India. For instance, in February 2024, Deepak Chem Tech Limited signed an MoU with the government of Gujarat with an intent to invest around INR 90,000 million to establish projects at Dahej, Gujarat. The company plans to build world-scale production facilities for advanced polymer resins, such as polycarbonate resins.

- In recent years, Japan has seen a trend of BPA manufacturing plants closing down due to intense competition and low profitability, significantly impacting the industry. For instance, in February 2024, Japan's Mitsubishi Chemical planned to permanently halt the production of BPA by the end of March 2024 at its Kurosaki plant in south Japan's Fukuoka prefecture, citing oversupply, mainly from China. This plant produces about 120,000 tons of BPA per annum.

- Hence, the above-mentioned factors are expected to impact the demand for BPA in Asia-Pacific.

Bisphenol A Industry Overview

The Bisphenol-A (BPA) market is partially consolidated in nature. Some of the key players (not in any particular order) in the market include Covestro AG, SABIC, Chang Chun Group, Mitsui Chemical Inc., and Nan Ya Plastics Corporation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Soaring Demand from Polycarbonate Sector

- 4.1.2 Increasing Demand from Epoxy Resin Production

- 4.2 Restraints

- 4.2.1 Increasing Regulations in the Food and Beverage Industry

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

- 4.5 Feedstock Analysis

- 4.6 Technological Snapshot

- 4.7 Trade Overview

- 4.8 Price Overview

- 4.9 Regulatory Policy Analysis

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 By Application

- 5.1.1 Polycarbonate Resins

- 5.1.2 Epoxy Resins

- 5.1.3 Unsaturated Polyester Resins

- 5.1.4 Flame Retardants

- 5.1.5 Other Applications

- 5.2 By Geography

- 5.2.1 Asia-Pacific

- 5.2.1.1 China

- 5.2.1.2 India

- 5.2.1.3 Japan

- 5.2.1.4 South Korea

- 5.2.1.5 ASEAN Countries

- 5.2.1.6 Rest of Asia-Pacific

- 5.2.2 North America

- 5.2.2.1 United States

- 5.2.2.2 Canada

- 5.2.2.3 Mexico

- 5.2.3 Europe

- 5.2.3.1 Germany

- 5.2.3.2 United Kingdom

- 5.2.3.3 Italy

- 5.2.3.4 France

- 5.2.3.5 Spain

- 5.2.3.6 Rest of Europe

- 5.2.4 South America

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 Rest of South America

- 5.2.5 Middle East and Africa

- 5.2.5.1 Saudi Arabia

- 5.2.5.2 South Africa

- 5.2.5.3 Rest of Middle East and Africa

- 5.2.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers, Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%) Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Altivia Petrochemicals

- 6.4.2 Chang Chun Group

- 6.4.3 China National Bluestar (Group) Co. Ltd

- 6.4.4 China Petroleum & Chemical Corporation (SINOPEC)

- 6.4.5 Covestro AG

- 6.4.6 Dow

- 6.4.7 Hexion

- 6.4.8 Idemitsu Kosan Co. Ltd

- 6.4.9 Kumho P&B Chemicals Inc.

- 6.4.10 LG Chem

- 6.4.11 Lihua Yiweiyuan Chemical Co. Ltd

- 6.4.12 Mitsubishi Chemical Corporation

- 6.4.13 Mitsui Chemicals Inc.

- 6.4.14 Nan Ya Plastics Industry Co. Ltd

- 6.4.15 Nippon Steel Chemical & Material Co. Ltd

- 6.4.16 PTT Phenol Company Limited

- 6.4.17 SABIC

- 6.4.18 Samyang Holdings Corporation

- 6.4.19 Teijin Limited

- 6.4.20 Zhejiang Petroleum & Chemical Co. Ltd

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Potential Market Demand for Bio-Based BPA

02-2729-4219

+886-2-2729-4219

雙酚 A 市場:按類型、應用分類 - 2025-2030 年全球預測

雙酚 A 市場:按類型、應用分類 - 2025-2030 年全球預測 雙酚 S 市場:按產品類型、應用、最終用途產業、銷售管道- 2025-2030 年全球預測

雙酚 S 市場:按產品類型、應用、最終用途產業、銷售管道- 2025-2030 年全球預測 全球雙酚A產業預測(~2028年)- 生產能力和設備投資預測,運作中·計劃完畢的所有工廠詳細內容

全球雙酚A產業預測(~2028年)- 生產能力和設備投資預測,運作中·計劃完畢的所有工廠詳細內容 雙酚A市場規模、佔有率、趨勢分析報告:按應用、地區、細分市場預測,2024-2030年

雙酚A市場規模、佔有率、趨勢分析報告:按應用、地區、細分市場預測,2024-2030年 雙酚 S 市場報告:2030 年趨勢、預測與競爭分析

雙酚 S 市場報告:2030 年趨勢、預測與競爭分析 雙酚A全球市場2024-2028

雙酚A全球市場2024-2028 雙酚 A 全球市場分析:工廠產能、產量、利用率、需求和供應、最終用戶行業、銷售渠道、區域需求、公司份額、對外貿易 (2015-2032)

雙酚 A 全球市場分析:工廠產能、產量、利用率、需求和供應、最終用戶行業、銷售渠道、區域需求、公司份額、對外貿易 (2015-2032) 雙酚A市場,按應用,按地區

雙酚A市場,按應用,按地區