|

市場調查報告書

商品編碼

1536843

CO氣體感測器:市場佔有率分析、產業趨勢/統計、成長預測(2024-2029)CO Gas Sensors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

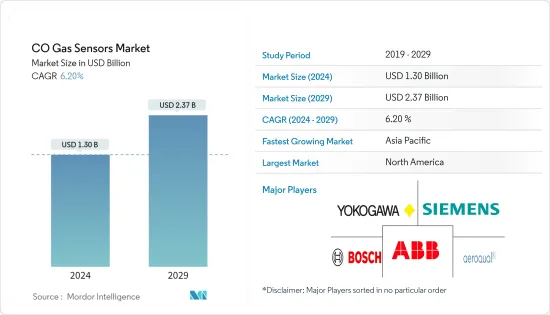

預計2024年全球CO氣體感測器市場規模將達到13.7億美元,2024-2029年預測期間複合年成長率為6.20%,2029年將達到23.7億美元。

各行業有多種應用,有些產業使用二氧化碳氣體進行與製程相關的操作,而有些產業則將其作為特定產品排放。工業界遵循嚴格的法規,以確保安全的工作環境並避免危及工人生命的接觸。此類法規對於快速、早期引入一氧化碳氣體警報器和偵測器極為重要。這直接影響了工業界對CO氣體感測器日益成長的需求。

這些感測器在一氧化碳水平升至危險濃度時提供早期預警,在拯救生命方面發揮關鍵作用。這些感測器提醒人們潛在的危險,並實現快速疏散和干涉,防止一氧化碳中毒和死亡。

確保職場安全的政府法規主要推動一氧化碳氣體感測器市場的成長。例如,英國、德國和法國實施了各種法規,以避免向大氣中釋放危險氣體。化學工業氣體具有低閃點、較低的爆炸極限 (LEL) 和頻譜的可燃性/可燃性。另一方面,透過持續使用此類氣體感測器和監視器,可以將這些氣體造成的危險降至最低。

此外,工業物聯網正在各個地區取得進展。客戶對物聯網一氧化碳氣體探測器的興趣日益濃厚,企業參與者正在致力於推出針對物聯網解決方案量身定做的產品系列。持續即時監控和排放氣體檢測的需求需要無線感測器,預計未來幾年將推動對二氧化碳氣體探測器的需求。

此外,產品小型化促進了可攜式氣體感測器設備的發展,提供了便攜靈活性。這些行業專注於採用自動化和收集所有資料。這些要求推動了對具有雙向通訊功能的無線感測器的需求。

然而,缺乏監管要求降低了採用這些感測器的緊迫性並限制了市場成長。雖然CO氣體感測器已經有了很大的改進,但它們也存在技術限制。例如,一些感測器難以檢測低水平的一氧化碳,使用壽命有限,並且需要頻繁校準。這些技術限制預計將阻礙一氧化碳氣體感測器市場的發展。

此外,俄羅斯和烏克蘭之間的戰爭正在影響半導體和電子元件供應鏈,這是生產半導體和電子元件(包括感測器)的原料的重要供應商。衝突可能會擾亂供應鏈,導致這些材料短缺和價格上漲,從而影響一氧化碳 (CO) 氣體感測器製造商,並導致最終用戶的成本更高。

一氧化碳氣體感測器市場趨勢

石化產業推動成長

- 一氧化碳感測器正在迅速引入液化石油氣和液化天然氣領域。這是因為這些產業需要在氣體儲存、生產和運輸的每個階段進行檢查。此外,隨著全球天然氣產量的增加,對加工設施安全保障的需求也增加。根據MOSPI統計,石化產品佔印度同年能源消費量總量的37%。

- 目前的TWA僅5,000 ppm,二氧化碳的重量是空氣的兩倍以上。目前使用的濃度為 40,000 ppm,即 IDLH 體積的 4%。接觸有毒物質的症狀包括頭痛、呼吸困難、心率加速和抽搐。

- 在石化產業,石油回收和尿素/甲醇生產需要使用感測器來監測二氧化碳氣體,這些感測器會連續檢測二氧化碳濃度,並在氣體達到有毒水平時發出持續的警報命令。

- 它也用於檢測氣體洩漏和監測空氣品質。一氧化碳感測器可以與其他設備(例如紅外線成像器和攝影機)結合使用,以幫助確定氣體洩漏的來源。

預計北美將佔據較大市場佔有率

- 該地區正在大力投資市場成長。工業安全措施的增加、工業領域應用的增加以及全部區域因二氧化碳導致的死亡人數不斷增加,都進一步增加了對二氧化碳氣體感測器的需求。

- 據安大略省消防隊長協會稱,加拿大各地每年有 50 多人死於一氧化碳中毒。人們在冬天經常使用燃油器具取暖,寒冷的天氣條件是導致死亡的主要原因。因此,使用一氧化碳 (CO) 氣體感測器是有益的。這些電器產品可能會在不知不覺中使您家中的二氧化碳氣體濃度達到危險水平。 CO氣體感測器主要用於一氧化碳偵測器和警報器。

- 根據 IEA 的《2022 年年度能源展望》,預計到 2050 年,石油和天然氣將成為美國消耗最多的能源。相比之下,可再生成長最快。太陽能和風力發電的獎勵不斷增加,技術成本不斷下降,與天然氣發電的競爭日益激烈。預計這些舉措將在預測期內增加對二氧化碳氣體感測器的需求。

- 在預測期內,北美將成為一個有利的市場,因為製造商正在對新環保產品的研發活動進行巨額投資。

- 該地區的許多州和地方都有法律要求在住宅和其他建築物中安裝一氧化碳氣體感測器,以預防一氧化碳中毒。由於與感測器設備相關的所有法規,該地區對 CO 氣體感測器的需求顯著增加。

- 近期,多起一氧化碳中毒事件發生。加拿大安大略省有9人被送往醫院,亞伯達1人在車內死亡。有鑑於此,加拿大衛生署警告加拿大人在家中和其他地方保持警惕,並注意一氧化碳的危險。此類事件可能會推動北美二氧化碳氣體感測器的需求。

一氧化碳氣體感測器產業概況

一氧化碳氣體感測器市場已成為半固體,在過去三十年中獲得了競爭力,並由多個主要企業組成。從市場佔有率來看,目前該市場由少數主要企業主導。然而,隨著燃氣洩漏事件導致的技術創新和安全法規的增加,市場參與者正在進行策略創新,以提供這些符合法規和政策的感測器。

2024 年 4 月:霍尼韋爾宣布成為「沙烏地阿拉伯製造」舉措中的首家氣體探測器製造商,重申其致力於促進沙烏地阿拉伯在地化和經濟多元化的決心。該公司將在其達曼工廠本地組裝和校準三種氣體檢測解決方案。在這些解決方案中, Honeywell Max XT II 是一款可攜式多氣體偵測儀,工作人員使用它來檢測危險環境中的硫化氫和一氧化碳等氣體。

2023 年 10 月,ABB 宣布擴大與帝國學院的碳捕獲合作,以支持未來的勞動力和能源轉型。 ABB 旨在透過在實際應用中展示最新技術如何幫助最佳化工廠性能並在緊急情況下管理安全,為學生提供操作工業流程所需的技能。

其他好處

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章 簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場洞察

- 市場概況

- 產業價值鏈分析

- 產業吸引力-波特五力分析

- 新進入者的威脅

- 買方議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭公司之間敵對關係的強度

- 宏觀經濟走勢對市場的影響

第5章市場動態

- 市場促進因素

- 確保職場安全的政府法規

- 廢氣法規的需求日益增加

- 市場限制因素

- 中小企業安全意識缺失

- 低維護成本和產品差異化

第6章 市場細分

- 依技術

- 半導體感測器

- 電化學感測器

- 固態/MOS感測器

- PID

- 催化型

- 紅外線的

- 按用途

- 醫療保健

- 石化

- 建築自動化

- 工業的

- 環境

- 車

- 其他用途

- 按地區

- 北美洲

- 歐洲

- 亞洲

- 澳洲/紐西蘭

- 拉丁美洲

- 中東/非洲

第7章 競爭格局

- 公司簡介

- Aeroqual Ltd

- ABB Ltd

- Siemens AG

- Yokogawa Electric Corporation

- Robert Bosch GmbH

- GfG Europe Ltd

- Alphasense

- Dynament Ltd

- NGK Insulators Ltd

- Trolex Ltd

- Honeywell

第8章投資分析

第9章 市場的未來

The CO Gas Sensors Market size is estimated at USD 1.30 billion in 2024, and is expected to reach USD 2.37 billion by 2029, growing at a CAGR of 6.20% during the forecast period (2024-2029).

Industries have different applications, with some industries using CO gas for their process-related works and other sectors releasing it as a byproduct. To ensure a secure working environment and avoid any life-threatening exposure to the workers, stringent regulations are followed in the industries. These regulations have been critical in the high-paced and early adoption of CO gas alarms and detectors. Thus, this has directly impacted the increased demand for CO gas sensors in industries.

These sensors play a vital role in safeguarding human lives by providing early warnings when carbon monoxide levels rise to hazardous concentrations. These sensors enable swift evacuation and intervention by alerting people to potential dangers and preventing carbon monoxide poisoning and fatalities.

Government regulations to ensure workplace safety primarily increase the growth of the carbon monoxide gas sensors market. For instance, the United Kingdom, Germany, and France have all implemented various rules to avoid the release of dangerous gasses into the atmosphere. Chemical industrial gasses are employed at low flashpoints with lower explosive limits (LEL) and a broad flammable/combustible spectrum. On the other hand, hazards induced by such gases can be minimized by continually using these gas sensors and monitors.

Additionally, the IIoT is advancing in various regions. Customers are becoming more interested in IoT carbon monoxide gas detectors, and players in the enterprise are working on launching a product range tailored to IoT solutions. The necessity for wireless sensors owing to the requirement of constant and real-time monitoring and detection of emissions is anticipated to drive up demand for CO gas detectors in the coming years.

Further, product miniaturization has helped develop portable gas sensor devices that provide carrying flexibility. In these industries, there is a high focus on adopting automation and collecting all the data. Such a requirement has resulted in increased demand for wireless sensors that are enabled with two-way communication features.

However, the absence of regulatory requirements limits market growth as the urgency to adopt these sensors decreases. CO gas sensors have improved significantly, but there are certain technological limitations. For example, some sensors have difficulty detecting low levels of carbon monoxide, have a limited lifespan, and require frequent calibration. These technical limitations are expected to hinder the carbon monoxide gas sensor market.

Additionally, the Russia-Ukraine war is impacting the supply chain of semiconductors and electronic components, being a significant supplier of raw materials for producing semiconductors and electronic components, including sensors. The dispute has disrupted the supply chain, causing shortages and price increases for these materials, impacting carbon monoxide (CO) gas sensor manufacturers and potentially leading to higher costs for end users.

Carbon Monoxide Gas Sensors Market Trends

The Petrochemical Segment to Witness Growth

- Carbon monoxide sensors are being rapidly deployed in the LPG and LNG sectors since these industries require a check at every stage of gas storage, production, or transportation. The demand for safety and security at processing installations has also been increasing while natural gas production is growing worldwide. The growth of this segment is expected to be driven by the continued increase in gas products, and according to MOSPI, petrochemicals accounted for 37% of India's total energy consumption that year.

- With a current TWA of only 5,000 ppm, carbon dioxide is more than twice as heavy as air. Currently, 40,000 ppm or 4% by volume of IDLH is in use. Toxic exposure symptoms are headache, trouble breathing, increased heart rate, and convulsions.

- In the petrochemical industry, oil recovery and urea and methanol production require CO2 gas monitoring with a sensor that continuously detects CO2 levels and issues constant alarm commands when the gas is in toxic quantities.

- They are also used to detect gas leaks and monitor air quality. Carbon monoxide sensors can be used with other instruments, such as a thermal imager or an infrared camera, to help identify the source of the gas leak.

North America is Expected to Hold Significant Market Share

- The region is investing significantly in market growth. The rising industrial safety measures, increasing applications in the industrial sector, and an increasing number of deaths due to CO across the region further create demand for CO gas sensors.

- In addition, according to the Ontario Association of Fire Chiefs, more than 50 people die yearly from CO poisoning across Canada; as people use fuel-burning appliances more often to keep warm in winter, the deaths are mainly due to cold weather conditions. As a result, adopting carbon monoxide (CO) gas sensors is beneficial, as these appliances can unknowingly cause dangerous levels of CO gas to build up in the home. The CO gas sensors are primarily used in carbon monoxide detectors and alarms.

- According to IEA's Annual Energy Outlook 2022, petroleum and natural gas are expected to be the most-consumed power sources in the United States through 2050. In contrast, renewable energy is expected to be the fastest growing. The increasing incentives for solar and wind energy and declining technology costs support robust competition with natural gas for electricity generation. Such initiatives will drive the demand for CO gas sensors during the forecast period.

- North America will be a lucrative market during the forecast period due to huge investments by manufacturers in R&D activities concerning new environmentally friendly products.

- There are laws in many states and provinces of the region that require CO gas sensors to be installed in homes and other buildings as a precautionary measure against carbon monoxide poisoning. The demand for CO gas sensors in the region has increased significantly owing to all regulations relating to sensor devices.

- There have been a few incidents of CO poisoning recently. Nine people were sent to a hospital in Ontario, Canada, and one person died in a vehicle in Alberta. In light of such events, Health Canada is warning Canadians to be alert in their homes and elsewhere and aware of carbon monoxide's dangers. Such events will drive North America's demand for CO gas sensors.

Carbon Monoxide Gas Sensors Industry Overview

The carbon monoxide gas sensors market is semi-consolidated, has gained a competitive edge in the past three decades, and consists of several major players. In terms of market share, few of the prominent players currently dominate the market. However, with increasing innovations and safety regulations due to gas leakage incidents, the companies in the market are strategically innovating in providing these sensors, which meet the rules and policies.

April 2024: Honeywell announced that it will be the first gas detector manufacturer in the 'Made in Saudi' initiative, reaffirming its dedication to fostering localization and economic diversification in Saudi Arabia. It will locally assemble and calibrate three distinct gas detection solutions at its Dammam facility. Among these solutions is the Honeywell BW Max XT II, portable multi-gas detector workers use to detect gases like hydrogen sulfide and carbon monoxide in hazardous environments.

October 2023: ABB announced extending its carbon capture collaboration to support the future workforce and energy transition with Imperial College. ABB aims to equip the students with the skills needed to run industrial processes by demonstrating how the latest technology can help optimize plant performance and safely manage emergencies in real-life applications.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Impact of Macroeconomic Trends on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Government Regulations to Ensure Safety in Work Places

- 5.1.2 Increasing Need for Emission Control Standards

- 5.2 Market Restraints

- 5.2.1 Lack of Awareness of Safety Gains in SME

- 5.2.2 Cost of Maintenance and Low Product Differentiation

6 MARKET SEGMENTATION

- 6.1 By Technology

- 6.1.1 Semiconductor Sensor

- 6.1.2 Electrochemical Sensor

- 6.1.3 Solid State/MOS Sensor

- 6.1.4 PID

- 6.1.5 Catalytic

- 6.1.6 Infrared

- 6.2 By Application

- 6.2.1 Medical

- 6.2.2 Petrochemical

- 6.2.3 Building Automation

- 6.2.4 Industrial

- 6.2.5 Environmental

- 6.2.6 Automotive

- 6.2.7 Other Applications

- 6.3 By Geography***

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia

- 6.3.4 Australia and New Zealand

- 6.3.5 Latin America

- 6.3.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles*

- 7.1.1 Aeroqual Ltd

- 7.1.2 ABB Ltd

- 7.1.3 Siemens AG

- 7.1.4 Yokogawa Electric Corporation

- 7.1.5 Robert Bosch GmbH

- 7.1.6 GfG Europe Ltd

- 7.1.7 Alphasense

- 7.1.8 Dynament Ltd

- 7.1.9 NGK Insulators Ltd

- 7.1.10 Trolex Ltd

- 7.1.11 Honeywell

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

低功耗/小型氣體感測器市場:按氣體類型、範圍、目標氣體、類型和應用 - 2025-2030 年全球預測

低功耗/小型氣體感測器市場:按氣體類型、範圍、目標氣體、類型和應用 - 2025-2030 年全球預測 氣體感測器市場:按技術、氣體類型、連接性和最終用途分類 – 2025-2030 年全球預測

氣體感測器市場:按技術、氣體類型、連接性和最終用途分類 – 2025-2030 年全球預測 石油和天然氣感測器市場:按類型、連接性和應用分類 - 2025-2030 年全球預測

石油和天然氣感測器市場:按類型、連接性和應用分類 - 2025-2030 年全球預測 全球一氧化碳偵測器市場:按類型、應用、感測器技術、最終用戶、分銷管道 - 預測 2025-2030

全球一氧化碳偵測器市場:按類型、應用、感測器技術、最終用戶、分銷管道 - 預測 2025-2030 氣體感測器市場規模、佔有率、成長分析:按類型、連接性別、技術、地區 - 產業預測,2024-2031 年

氣體感測器市場規模、佔有率、成長分析:按類型、連接性別、技術、地區 - 產業預測,2024-2031 年 氣體感測器:市場佔有率分析、行業趨勢和統計、成長預測(2024-2029)

氣體感測器:市場佔有率分析、行業趨勢和統計、成長預測(2024-2029) 臭氧感測器市場報告:2030 年趨勢、預測和競爭分析

臭氧感測器市場報告:2030 年趨勢、預測和競爭分析 氣體感測器全球市場,2024-2028

氣體感測器全球市場,2024-2028 氮氧化物感測器市場、機會、成長動力、產業趨勢分析與預測,2024-2032

氮氧化物感測器市場、機會、成長動力、產業趨勢分析與預測,2024-2032 到 2030 年氣體感測器市場預測:按產品、輸出類型、氣體類型、技術、連接性、最終用戶和地區進行的全球分析

到 2030 年氣體感測器市場預測:按產品、輸出類型、氣體類型、技術、連接性、最終用戶和地區進行的全球分析