|

市場調查報告書

商品編碼

1850067

汽車懸吊系統:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)Automotive Suspension System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

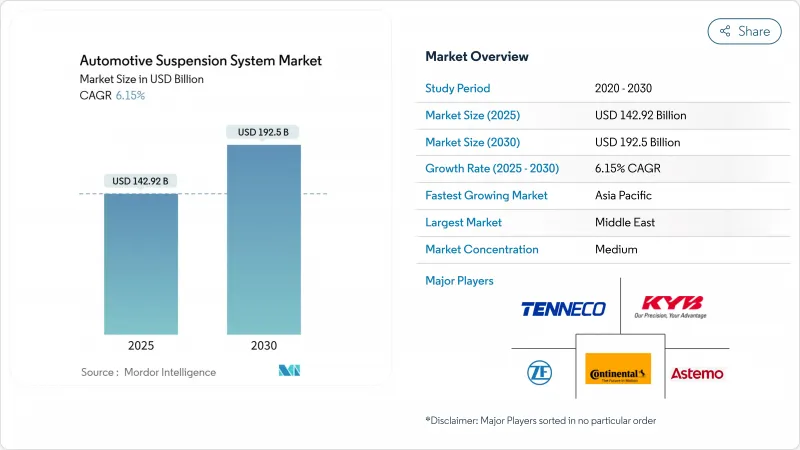

預計到 2025 年,汽車懸吊系統市場規模將達到 1,429.2 億美元,到 2030 年將達到 1,925 億美元,年複合成長率為 6.15%。

此次市場擴張反映了各地區底盤部件的重塑,而這主要得益於電氣化、軟體定義車輛架構以及日益嚴格的安全法規。汽車製造商正從純機械佈局轉向電子控制的半主動和主動設計,以平衡乘坐舒適性、能量回收以及電池電動平台的封裝限制。感測器、控制單元和雲端連接是懸吊策略的核心,能夠實現持續的效能更新。同時,稀土材料和半導體供應鏈的不確定性迫使重新設計降低材料密集度並實現多元化。在此背景下,能夠將機械技術與先進的電子、軟體和數據分析相結合的廠商將繼續在汽車懸吊系統市場中佔據優勢。

全球汽車懸吊系統市場趨勢與洞察

對更佳駕乘體驗和操控性能的需求日益成長

消費者對靜謐無振動車廂的期望日益提高,促使汽車製造商在所有價格分佈中都加入了即時阻尼控制技術。磁流變阻尼器可在毫秒內調節流體黏度,這項技術已在MagneRide等系統中實用化。電動車對這項技術的關注更為顯著,因為沒有引擎噪音,即使是最輕微的懸吊顛簸也會傳遞給車內乘客。共享出行車隊和自動駕駛原型車則增加了另一層監控,因為乘客在駕駛過程中會更敏銳地感知到乘坐舒適性。供應商正透過整合加速計、行程感測器和邊緣處理器來應對這一需求,從而在最大限度降低能耗的同時,調節每個車輪的阻尼。

以電氣化主導的底盤重新設計

電池組雖然降低了車輛的重心,但也增加了數百公斤的重量,因此懸吊工程師採用了複合材料連桿和中空穩定器來抵消增加的重量,同時又不影響強度。對靜電再生阻尼器的研究表明,其尖峰時段能源回收可達45%,與車輛的能量管理邏輯相結合,相當於每公里減少5.25克二氧化碳排放。

智慧懸吊架構的初始成本和生命週期成本都很高

主動式系統結合了馬達、電磁閥、加速感應器和網域控制器等組件,與被動式系統相比,每輛車的成本會增加數百美元。除非受到強制要求或獲得巨額補貼,否則汽車製造商不願在利潤微薄、銷售量龐大的主流細分市場中捆綁這些成本。此外,主動式系統還會增加總擁有成本,因為服務提供者需要專門的診斷工具和校準鑽機。這些經濟因素限制了主動式系統的應用,使其僅限於高階車型,即使底層技術日趨成熟,也難以在大眾市場中廣泛應用。

細分市場分析

到2024年,減震器的市佔率將達到39.07%,鞏固了其作為能量耗散核心元件的持久地位。然而,電控系統和感測器將以9.82%的複合年成長率實現最快成長,這主要得益於ADAS整合、邊緣處理能力的提升以及雲端更新的普及。汽車懸吊系統市場受益於如今整合多種安全功能的控制模組,這些模組支援空中校準,並減少了硬體升級的需求。因此,到2030年,電子驅動的汽車懸吊系統市場規模預計將在2024年的基準上翻倍。雖然螺旋彈簧和鋼板彈簧在商用運輸領域仍然佔據主導地位(因為耐用性比技術先進性更重要),但空氣彈簧正在豪華轎車和高頂廂式貨車領域不斷擴大市場佔有率。

軟體定義的車輛藍圖協調來自車輪行程感測器、荷重元和轉向編碼器的數據,將控制單元轉換為符合ASIL-D安全標準的模組化電腦節點。人工智慧驅動的預測演算法將雲端獲取的路面資訊回饋到阻尼策略中,從而實現對複雜路面的主動控制,並提升乘客舒適度。機械部件與數位智慧的融合加劇了能夠大規模生產兩者的供應商之間的競爭,推動了汽車懸吊系統市場的發展。

由於結構簡單、運作成本低,被動式懸吊系統預計在2024年仍將佔據汽車懸吊系統市場65.28%的佔有率。然而,半主動式懸吊系統預計將以12.04%的複合年成長率成長,因為它們能夠在不增加全主動式懸吊系統能耗和零件數量的情況下,顯著提升乘坐舒適性。這種趨勢也推動了新型轉向系統的研發,例如採埃孚(ZF)的EasyTurn車橋,該車橋可實現高達80度的方向盤鎖,從而提升車輛在城市道路上的操控靈活性。

磁流變閥和電子機械閥能夠實現毫秒級的阻尼力變化,從而在高速行駛過程中有效抑制車身側傾和俯仰。結合基於群眾外包路面坑洞地圖的預測分析,半主動懸吊系統能夠達到接近主動懸吊系統的性能水準。隨著電池能量密度的提升和再生減震器對運行損耗的補償,主動懸吊系統在預測期內有望獲得更廣泛的應用,但由於半主動懸吊系統具有更優的性價比,預計仍將佔據汽車懸吊系統市場成長的大部分佔有率。

區域分析

到2024年,亞太地區將佔據全球汽車懸吊系統市場48.96%的佔有率,這主要得益於中國龐大的市場規模和印度產能的快速擴張。北京的新能源汽車補貼政策和嚴格的乘坐舒適性標準正在推動大眾市場轎車採用半主動阻尼技術。同時,印度汽車製造商正在輕型商用車中採用輕量化複合材料彈簧,以提高負載效率。印度政府的各項舉措,例如“2047年汽車發展規劃”,支持高價值底盤總成的本地化生產,從而增強了區域供應鏈的韌性。日本和韓國的供應商則提供精密閥門、智慧襯套和軟體堆疊等產品,豐富了先進懸吊套件出口到全球的生態系統。

中東和非洲地區正以7.65%的複合年成長率成長,並逐漸成為高階SUV和商用車的需求中心,這些車輛必須能夠承受沙漠的酷熱和崎嶇的地形。海灣航空公司向賽車運動娛樂領域多元化發展,以及對沙烏地阿拉伯大獎賽的投資,推動了對能夠應對嚴苛熱負荷的高性能減震器技術的需求。供應商正積極回應,推出專為磨蝕性沙地環境設計的專用密封件、長行程氣囊和耐腐蝕塗層。本地化計劃和自由貿易區的實施降低了進口關稅,提升了該地區對汽車懸吊系統一級製造商的吸引力。

北美和歐洲市場憑藉著監管政策和高階車型的集中度,保持著強勁的市場佔有率。美國《通膨降低法案》提供的電池補貼將推動對輕量化多連桿後軸的需求,這種後軸能夠保護電動皮卡中安裝在底盤上的電池組。歐洲對「零願景」(Vision Zero)和「通用安全法規II」(General Safety Regulation II)的重視,已將半主動阻尼和高度控制納入其認證清單,有效地將智慧懸吊確立為汽車製造商的合規要求。憑藉成熟的供應鏈、先進的模擬基礎設施和完善的測試場地,這兩個地區持續樹立性能和安全標桿,並對全球汽車懸吊系統市場產生深遠影響。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 對更佳駕乘體驗和操控性能的需求日益成長

- 重新設計的底盤以適應電氣化(輕量化自我調整懸吊)

- 加強對ADAS聯動底盤安全性的監管

- 新興國家SUV和豪華車銷售激增

- 透過訂閱式無線升級解鎖主動懸吊功能

- 3D列印複合材料懸吊零件可降低模具成本

- 市場限制

- 智慧懸吊架構的初始成本和生命週期成本都很高

- 惡劣條件下的可靠性與維護挑戰

- 網路安全和功能安全合規的負擔

- 稀土元素磁流變液和半導體感測器的供應瓶頸

- 價值/供應鏈分析

- 監管環境

- 技術展望

- 波特五力模型

- 供應商的議價能力

- 買方/消費者的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 依組件類型

- 螺旋彈簧

- 鋼板彈簧

- 空氣彈簧

- 避震器

- 穩定器/防傾桿

- 懸臂和連桿

- 電控系統和感測器

- 其他部件

- 按懸吊懸吊系統類型

- 被動懸吊

- 半主動懸吊

- 主動懸浮

- 按幾何/建築

- 麥花臣式懸臂梁

- 雙橫臂

- 多鏈路

- 扭梁/扭轉梁

- 其他形狀

- 按車輛類型

- 搭乘用車

- 輕型商用車

- 大型商用車輛

- 按銷售管道

- OEM

- 售後市場

- 透過推廣

- 內燃機車輛

- 電動和混合動力汽車

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 亞太其他地區

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

- 埃及

- 土耳其

- 其他中東和非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Continental AG

- ZF Friedrichshafen AG

- Tenneco Inc.

- KYB Corporation

- Hitachi Astemo Ltd.

- Thyssenkrupp AG

- Mando Corporation

- Marelli Corporation

- Hyundai Mobis Co. Ltd.

- BWI Group

- Sogefi SpA

- Parker LORD Corporation

- Benteler International AG

- Fox Factory Holding Corp.

- Hendrickson International

- Ohlins Racing AB

- Showa Corporation

- Multimatic Inc.

- SAF-HOLLAND SE

- WABCO(ZF CVS)

第7章 市場機會與未來展望

The Automotive Suspension Systems Market is valued at USD 142.92 billion in 2025 and is forecast to reach USD 192.50 billion by 2030, advancing at a 6.15% CAGR.

The expansion reflects how electrification, software-defined vehicle architectures, and tightening safety mandates reshape chassis components in every region. Automakers are switching from purely mechanical layouts to electronically controlled semi-active and active designs that balance ride comfort, energy recuperation, and packaging constraints in battery-electric platforms. Sensors, control units, and cloud connectivity now center suspension strategies, enabling continuous performance updates delivered over the air. At the same time, supply-chain uncertainty in rare-earth materials and semiconductors is forcing redesigns that lessen material intensity and diversify sourcing. Against this backdrop, the automotive suspension systems market continues to reward players capable of blending mechanical know-how with advanced electronics, software, and data analytics.

Global Automotive Suspension System Market Trends and Insights

Increasing Demand for Enhanced Ride Comfort and Handling

Rising consumer expectations for quiet, vibration-free cabins push automakers to embed real-time damping control across all price points. Magnetorheological dampers modulate fluid viscosity within milliseconds, a capability commercialized in systems such as MagneRide that first appeared in luxury models and now migrate into high-volume crossovers. Electric vehicles magnify this focus because the absence of engine noise exposes even slight suspension harshness to occupants. Shared-mobility fleets and autonomous prototypes add another layer of scrutiny, as passengers disengaged from driving become acutely aware of ride quality. Suppliers respond by integrating accelerometers, stroke sensors, and edge processors that adjust damping on a wheel-by-wheel basis while minimizing energy draw.

Electrification-Driven Chassis Redesign

Battery packs lower a vehicle's center of gravity but add hundreds of kilograms, prompting suspension engineers to adopt composite links and hollow stabilizer bars that counteract mass increases without compromising strength. Research on electro-hydrostatic regenerative dampers shows 45% peak energy recovery, equating to 5.25 g/km CO2 savings when integrated with vehicle energy-management logic.

High Upfront & Lifecycle Cost of Smart Suspension Architectures

Active systems combine motors, solenoid valves, acceleration sensors, and domain controllers, inflating the bill-of-materials by several hundred USD per vehicle compared with passive setups. OEMs hesitate to bundle such costs in mainstream segments with thin margins unless mandated or heavily subsidized. Total ownership expenses also rise, as specialized diagnostic tools and calibration rigs become necessary for service providers. These economics restrict penetration to premium trims, slowing mass-market adoption even when the underlying technology matures.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Push for ADAS-Linked Chassis Safety

- Rapid SUV & Premium-Vehicle Sales in Emerging Economies

- Rare-earth MR-fluid and Semiconductor Sensor Supply Bottlenecks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The 39.07% share held by shock absorbers in 2024 confirms their enduring role as the core energy-dissipation element. Yet, electronic control units and sensors are the fastest climbers at a 9.82% CAGR, supported by ADAS integration, edge-processing power gains, and the pivot toward cloud-linked updates. The automotive suspension systems market benefits from control modules that now host multiple safety functions, allowing OTA calibration and reducing the need for hardware revisions. As a result, the automotive suspension systems market size attributed to electronics is on track to double its 2024 baseline by 2030. Coil and leaf springs remain prevalent in commercial transport where durability outweighs finesse, while air springs gain share in luxury sedans and high-roof vans.

Software-defined vehicle roadmaps turn control units into modular compute nodes that meet ASIL-D safety levels while orchestrating data from wheel-travel sensors, load cells, and steering encoders. AI-assisted predictive algorithms feed cloud-derived road information into damping strategies, delivering proactive control and elevating occupant comfort even on unpredictable surfaces. This convergence between mechanical parts and digital intelligence reinforces the competitive moat of suppliers capable of manufacturing both domains at scale, propelling the automotive suspension systems market forward

Passive configurations retained a 65.28% share of the automotive suspension systems market size in 2024 due to simplicity and low running costs. Semi-active setups, however, are registering an 12.04% CAGR because they deliver meaningful ride gains without the energy draw and component count of fully active designs. Their adoption also underpins new steering innovations such as ZF's EasyTurn axle, which increases steering lock to 80 degrees, improving urban agility.

Magnetorheological and electromechanical valves allow millisecond-scale damping shifts that flatten body roll and pitch during high-speed maneuvers. Paired with predictive analytics drawn from cloud-sourced pothole maps, semi-active systems achieve near-active performance envelopes. Over the forecast horizon, active suspensions may gain greater visibility as battery energy density rises and regenerative dampers offset operational losses, but semi-active designs are expected to capture the bulk of incremental volume thanks to favorable cost-benefit ratios within the automotive suspension systems market.

The Automotive Suspension Systems Market Report is Segmented by Component Type (Coil Spring, Leaf Spring, and More), Suspension System Type (Passive Suspension and More), Geometry (MacPherson Strut, Double Wishbone, and More), Vehicle Type (Passenger Cars, LCV, and More), Sales Channel (OEM and Aftermarket), Propulsion (ICE and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Geography Analysis

Asia-Pacific anchors the automotive suspension systems market with a 48.96% share in 2024, underpinned by China's scale and India's rapid capacity additions. Beijing's new-energy-vehicle subsidies and stringent ride-comfort benchmarks drive the adoption of semi-active damping in mass-market sedans. At the same time, Indian OEMs integrate lightweight composite springs to improve payload efficiency in small commercial trucks. Government schemes such as India's Automotive Mission Plan 2047 support local production of high-value chassis assemblies, reinforcing regional supply resilience. Japanese and South Korean suppliers contribute precision valves, smart bushings, and software stacks, lending depth to an ecosystem that now exports advanced suspension kits worldwide.

The Middle East and Africa, advancing at 7.65% CAGR, is emerging as a focal point for premium-SUV and commercial-vehicle demand that must withstand desert heat and rugged terrain. Gulf airlines' diversification into motorsport entertainment and Saudi Arabia's Grand Prix investments spur interest in high-performance damper technology capable of coping with severe thermal loads. Suppliers respond with specialized seals, long-stroke air bellows, and corrosion-resistant coatings designed for abrasive sand environments. Localization programs and free-trade zones lower import duties, enhancing the region's appeal for tier-1 manufacturing lines within the automotive suspension systems market.

North America and Europe maintain strong value shares through regulatory pull and premium-model concentration. The U.S. Inflation Reduction Act's domestic-battery incentives amplify demand for lightweight multi-link rear axles that protect floor-mounted packs in electric pickups. Europe's focus on Vision Zero and General Safety Regulation II embeds semi-active damping and ride-height control into homologation checklists, making intelligent suspensions a de facto requirement for OEM compliance. Mature supply chains, advanced simulation infrastructure, and robust test tracks ensure both regions continue to set performance and safety benchmarks that ripple across the global automotive suspension systems market.

- Continental AG

- ZF Friedrichshafen AG

- Tenneco Inc.

- KYB Corporation

- Hitachi Astemo Ltd.

- Thyssenkrupp AG

- Mando Corporation

- Marelli Corporation

- Hyundai Mobis Co. Ltd.

- BWI Group

- Sogefi SpA

- Parker LORD Corporation

- Benteler International AG

- Fox Factory Holding Corp.

- Hendrickson International

- Ohlins Racing AB

- Showa Corporation

- Multimatic Inc.

- SAF-HOLLAND SE

- WABCO (ZF CVS)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing demand for enhanced ride comfort & handling

- 4.2.2 Electrification-driven chassis redesign (lightweight adaptive suspensions)

- 4.2.3 Regulatory push for ADAS-linked chassis safety

- 4.2.4 Rapid SUV & premium-vehicle sales in emerging economies

- 4.2.5 Subscription-based OTA upgrades unlocking active-suspension features

- 4.2.6 3-D printed composite suspension parts reducing tooling cost

- 4.3 Market Restraints

- 4.3.1 High upfront & lifecycle cost of smart suspension architectures

- 4.3.2 Reliability & maintenance challenges in harsh conditions

- 4.3.3 Cyber-security & functional-safety compliance burden

- 4.3.4 Rare-earth MR-fluid & semiconductor sensor supply bottlenecks

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD) and Volume (Units))

- 5.1 By Component Type

- 5.1.1 Coil Springs

- 5.1.2 Leaf Springs

- 5.1.3 Air Springs

- 5.1.4 Shock Absorbers

- 5.1.5 Stabilizer / Anti-roll Bars

- 5.1.6 Suspension Arms & Links

- 5.1.7 Electronic Control Units & Sensors

- 5.1.8 Other Components

- 5.2 By Suspension System Type

- 5.2.1 Passive Suspension

- 5.2.2 Semi-Active Suspension

- 5.2.3 Active Suspension

- 5.3 By Geometry / Architecture

- 5.3.1 MacPherson Strut

- 5.3.2 Double Wishbone

- 5.3.3 Multi-Link

- 5.3.4 Torsion Beam / Twist Beam

- 5.3.5 Other Geometries

- 5.4 By Vehicle Type

- 5.4.1 Passenger Cars

- 5.4.2 Light Commercial Vehicles

- 5.4.3 Heavy Commercial Vehicles

- 5.5 By Sales Channel

- 5.5.1 OEM

- 5.5.2 Aftermarket

- 5.6 By Propulsion

- 5.6.1 Internal-Combustion-Engine Vehicles

- 5.6.2 Electric & Hybrid Vehicles

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 South America

- 5.7.2.1 Brazil

- 5.7.2.2 Argentina

- 5.7.2.3 Rest of South America

- 5.7.3 Europe

- 5.7.3.1 Germany

- 5.7.3.2 United Kingdom

- 5.7.3.3 France

- 5.7.3.4 Italy

- 5.7.3.5 Spain

- 5.7.3.6 Russia

- 5.7.3.7 Rest of Europe

- 5.7.4 Asia-Pacific

- 5.7.4.1 China

- 5.7.4.2 India

- 5.7.4.3 Japan

- 5.7.4.4 South Korea

- 5.7.4.5 Rest of Aisa-Pacific

- 5.7.5 Middle East and Africa

- 5.7.5.1 Middle East

- 5.7.5.1.1 Saudi Arabia

- 5.7.5.1.2 United Arab Emirates

- 5.7.5.1.3 South Africa

- 5.7.5.1.4 Egypt

- 5.7.5.1.5 Turkey

- 5.7.5.1.6 Rest of Middle East and Africa

- 5.7.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products & Services, and Recent Developments)

- 6.4.1 Continental AG

- 6.4.2 ZF Friedrichshafen AG

- 6.4.3 Tenneco Inc.

- 6.4.4 KYB Corporation

- 6.4.5 Hitachi Astemo Ltd.

- 6.4.6 Thyssenkrupp AG

- 6.4.7 Mando Corporation

- 6.4.8 Marelli Corporation

- 6.4.9 Hyundai Mobis Co. Ltd.

- 6.4.10 BWI Group

- 6.4.11 Sogefi SpA

- 6.4.12 Parker LORD Corporation

- 6.4.13 Benteler International AG

- 6.4.14 Fox Factory Holding Corp.

- 6.4.15 Hendrickson International

- 6.4.16 Ohlins Racing AB

- 6.4.17 Showa Corporation

- 6.4.18 Multimatic Inc.

- 6.4.19 SAF-HOLLAND SE

- 6.4.20 WABCO (ZF CVS)

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

汽車懸吊市場 - 全球產業規模、佔有率、趨勢、機會、預測:按零件類型、車輛類型、類型、地區和競爭對手分類,2021-2031年

汽車懸吊市場 - 全球產業規模、佔有率、趨勢、機會、預測:按零件類型、車輛類型、類型、地區和競爭對手分類,2021-2031年 2026-2034年全球汽車懸吊系統市場規模、佔有率、趨勢和成長分析報告

2026-2034年全球汽車懸吊系統市場規模、佔有率、趨勢和成長分析報告 汽車雙橫臂懸吊系統市場:按車輛類型、零件類型、技術、材料、傳動系統和應用分類-2026-2032年全球市場預測

汽車雙橫臂懸吊系統市場:按車輛類型、零件類型、技術、材料、傳動系統和應用分類-2026-2032年全球市場預測 2026年全球汽車懸吊系統市場報告汽車懸吊市場:按懸吊類型、零件、技術、車輛類型、最終用戶和銷售管道分類-2026年至2032年全球市場預測CDC懸吊市場按車輛類型、控制機制、技術類型、組件和分銷管道分類,全球預測,2026-2032年汽車懸吊系統市場規模、佔有率、成長率及全球市場分析:按類型、應用和地區的洞察,2026-2034年預測

2026年全球汽車懸吊系統市場報告汽車懸吊市場:按懸吊類型、零件、技術、車輛類型、最終用戶和銷售管道分類-2026年至2032年全球市場預測CDC懸吊市場按車輛類型、控制機制、技術類型、組件和分銷管道分類,全球預測,2026-2032年汽車懸吊系統市場規模、佔有率、成長率及全球市場分析:按類型、應用和地區的洞察,2026-2034年預測 汽車懸吊系統市場:按車輛、銷售管道、系統、懸吊類型、零件、國家和地區分類-全球產業分析、市場規模、市場佔有率和預測(2025-2032 年)商用車懸吊系統市場 - 全球產業規模、佔有率、趨勢、機會及預測(按車輛類型、零件類型、類型、地區和競爭格局分類,2021-2031年)懸吊市場 - 全球產業規模、佔有率、趨勢、機會及預測(按組件類型、車輛類型、類型、地區和競爭格局分類),2021-2031年

汽車懸吊系統市場:按車輛、銷售管道、系統、懸吊類型、零件、國家和地區分類-全球產業分析、市場規模、市場佔有率和預測(2025-2032 年)商用車懸吊系統市場 - 全球產業規模、佔有率、趨勢、機會及預測(按車輛類型、零件類型、類型、地區和競爭格局分類,2021-2031年)懸吊市場 - 全球產業規模、佔有率、趨勢、機會及預測(按組件類型、車輛類型、類型、地區和競爭格局分類),2021-2031年