|

市場調查報告書

商品編碼

1536875

黏劑:市場佔有率分析、產業趨勢/統計、成長預測(2024-2029)Hot-melt Adhesives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

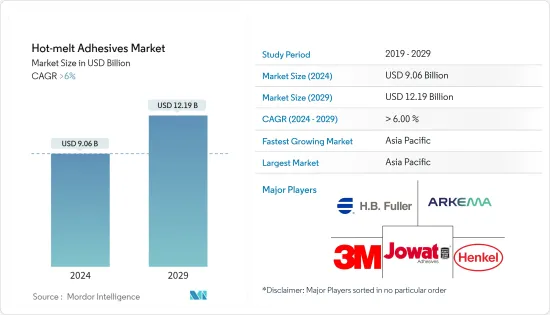

預計2024年全球黏劑市場規模將達90.6億美元,2024-2029年預測期間複合年成長率將超過6%,2029年將達到121.9億美元。

COVID-19 阻礙了黏劑市場。由於政府法規、消費者需求下降和供應鏈中斷,黏劑的各種最終用途行業,包括汽車製造、建築和不織布衛生用品,都經歷了生產放緩或停頓。由於封城措施和法規的放鬆,許多行業已經恢復營運,導致對黏劑的需求增加。

*包裝行業對黏劑需求的增加、建築行業需求的增加以及不織布衛生產品中黏劑的採用的增加預計將推動市場的發展。

*然而,原料價格的波動預計將阻礙黏劑市場的成長。

*汽車製造的擴張和建築技術的進步預計將在未來一段時間內提供機會。

*由於印度、日本和中國等經濟體快速成長,亞太地區預計將在未來幾年成為主導市場。

黏劑市場趨勢

紙張、紙板和包裝產業主導市場

*包裝產業是黏劑最大的消費者之一。這些黏劑廣泛用於黏合紙板、紙板、塑膠薄膜和箔片等包裝材料,適用於箱子和紙箱密封、托盤成型、標籤和層壓等應用。黏劑在工業中的大規模使用正在推動巨大的需求和市場主導地位。

*由於食品消費和各種應用的增加,包裝領域對黏劑的需求正在增加。例如,在印度,包裝是成長最快的行業之一。該行業在過去幾年中經歷了穩定成長,預計將迅速擴張,特別是在出口領域。

*例如,根據印度紙張工業協會 (IPMA) 報告的資料,在印度,2023 年 4 月至 12 月的紙張進口量增加了 37%,達到 147 萬噸。

*此外,根據德國聯邦統計局2023年3月發布的估計,2022年德國包裝產業收益的約46%來自紙包裝。近 34% 是塑膠包裝。

*此外,根據德國聯邦統計局2023年發布的估計,德國包裝業的收益約為350億歐元(379.4億美元)。與上年度的 296 億歐元(320.9 億美元)相比有所增加。

*食品和飲料業是包裝的主要消費者之一。隨著世界各地日益成長的趨勢,烘焙行業正在不斷發展,這推動了包裝產品的銷售。

*因此,由於上述因素,紙張、紙板和包裝行業對黏劑的需求預計將成長。

亞太地區主導市場

*亞太地區正在經歷快速的工業化、都市化和基礎設施發展,特別是在新興經濟體。這種成長正在推動建築、包裝、汽車和其他產業對黏劑的需求。

*亞太地區政府和私營部門正在投資各種基礎設施計劃,包括交通、公共工程以及住宅和商業設施的建設。黏劑用於各種建築應用,包括安裝壁板、地板材料、隔熱材料絕緣材料和重新屋頂,並且正在推動該地區建築業的需求。

*根據印度品牌股權基金會的數據,2023-2024年預算中基礎設施的資本投資將成長33%,達到約1,220億美元,佔GDP的3%。

*此外,為了吸引私人投資,印度政府正在開發多種途徑,特別是在道路和高速公路、機場、商業園區以及高等教育和技能開發領域。截至2023年5月,私人公司和創業投資已向印度企業投資35億美元,完成71筆交易。

*自2008年以來,中國一直是最大的紙包裝和紙板生產國。中國造紙工業協會調查顯示,2023年我國紙及紙板生產企業總數為2500家,全國紙及紙板產量12965萬噸,與前一年同期比較成長4.35% 。

*因此,上述因素預計將在預測期內推動該地區的黏劑市場。

黏劑產業概況

全球黏劑市場分散。市場上的主要企業包括(排名不分先後)3M、Jowat SE、漢高公司、阿科瑪和 HB Fuller。

其他好處:

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 調查先決條件

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 促進因素

- 包裝產業需求增加

- 建築業需求增加

- 其他司機

- 抑制因素

- 原物料價格波動

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章市場區隔(市場規模:金額)

- 樹脂型

- 乙烯醋酸乙烯酯

- 苯乙烯嵌段共聚物

- 熱塑性聚氨酯

- 其他樹脂類型

- 最終用戶產業

- 建築/施工

- 紙/紙板/包裝材料

- 木工/細木工

- 汽車/交通

- 鞋類/皮革

- 衛生保健

- 電氣/電子設備

- 其他最終用戶產業

- 地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 馬來西亞

- 泰國

- 印尼

- 越南

- 東南亞國協

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 土耳其

- 西班牙

- 俄羅斯

- 北歐的

- 歐洲其他地區

- 南美洲

- 巴西

- 阿根廷

- 哥倫比亞

- 南美洲其他地區

- 中東/非洲

- 沙烏地阿拉伯

- 南非

- 奈及利亞

- 埃及

- 卡達

- 阿拉伯聯合大公國

- 其他中東/非洲

- 亞太地區

第6章 競爭狀況

- 併購、合資、聯盟、協議

- 市場佔有率(%)**/排名分析

- 主要企業策略

- 公司簡介

- 3M

- Alfa International

- Arkema

- Ashland

- AVERY DENNISON CORPORATION

- Beardow Adams

- Dow

- DRYTAC

- Franklin International

- HB Fuller Company

- Henkel Corporation

- Hexcel Corporation

- Huntsman International LLC

- Jowat SE

- Mactac

- Master Bond Inc.

- Paramelt RMC BV

- Pidilite Industries Limited

- Sika AG

第7章 市場機會及未來趨勢

- 擴大汽車製造

- 建築技術的進步

The Hot-melt Adhesives Market size is estimated at USD 9.06 billion in 2024, and is expected to reach USD 12.19 billion by 2029, growing at a CAGR of greater than 6% during the forecast period (2024-2029).

COVID-19 hampered the hot melt adhesive market. Various end-use industries for hot melt adhesives, such as automotive manufacturing, construction, and nonwoven hygiene products, experienced slowdowns or shutdowns in production due to government-mandated restrictions, reduced consumer demand, and supply chain disruptions. With the easing of lockdown measures and restrictions, many industries have resumed operations, leading to increased demand for hot melt adhesives.

* Increasing demand for hot melt adhesives from the packaging industry, rising demand from the construction sector, and increased adoption of hot melt adhesives in nonwoven hygiene products are expected to drive the market.

* However, volatility in raw material prices is expected to hamper the growth of the hot melt adhesive market.

* Expansion in automotive manufacturing and the advancements in construction technologies are expected to provide opportunities in the upcoming period.

* Due to rapidly growing economies like India, Japan, and China, Asia-Pacific is expected to emerge as a dominant market in the coming years.

Hot Melt Adhesives Market Trends

Paper, Board, and Packaging Segment to Dominate the Market

* The packaging industry is one of the largest consumers of hot melt adhesives. These adhesives are widely used for bonding packaging materials such as paperboard, corrugated cardboard, plastic films, and foils in applications such as case and carton sealing, tray forming, labeling, and lamination. The industry's large-scale use of hot melt adhesives drives significant demand and market dominance.

* The demand for hot melt adhesives in the packaging sector is increasing due to increased food consumption and various applications. For instance, in India, packaging is one of the fastest-growing industries. The sector has witnessed steady growth over the past several years and is expected to expand rapidly, particularly in the export sector.

* For instance, in India, paper imports rose by 37% to 1.47 million tonnes from April to December 2023, according to data reported by The Indian Paper Manufacturers Association (IPMA).

* Further, according to the estimate published by the Statistisches Bundesamt in March 2023, in 2022, around 46 percent of the packaging industry revenue in Germany was generated by paper packaging. Almost 34 percent was made up of plastic packaging.

* Moreover, according to the estimate published by the Statistisches Bundesamt in 2023, the German packaging industry generated around EUR 35 billion (USD 37.94 billion) in revenue. This was an increase compared to the previous year at EUR 29.6 billion (USD 32.09 billion).

* The food and beverage sector is one of the major consumers of packaging. In order to cope with the increasing trend around the world, the bakery sector is growing, and this is driving sales of packaging products.

* Thus, the factors mentioned above are expected to grow the demand for hot melt adhesives from the paper, board, and packaging industries.

Asia-Pacific to Dominate the Market

* Asia-Pacific is experiencing rapid industrialization, urbanization, and infrastructure development, particularly in emerging economies in the region. This growth fuels the demand for hot melt adhesives in construction, packaging, automotive, and other industries, as these adhesives are essential for bonding materials and components in manufacturing and construction processes.

* Governments and private sectors in the Asia Pacific are investing in various infrastructure projects such as transportation, utilities, and residential and commercial construction. Hot melt adhesives are used in various construction applications, including paneling, flooring installation, insulation bonding, and roofing, driving the demand for these adhesives in the region's construction industry.

* According to the Indian Brand Equity Foundation, the capital investment in infrastructure is set to increase by 33%, amounting to about USD 122 billion, for the budget of 2023-24, and this accounts for 3% of GDP.

* Further, in order to attract private investment, the government of India has developed a number of ways, particularly for roads and highways, airports, business parks, and higher education and skills development sectors. Private Equity and Venture Capital Firms invested USD 3.5 billion in Indian companies between May 2023 with 71 deals.

* China has been the most extensive paper packaging and paperboard producer since 2008. According to a survey conducted by the China Paper Association, in 2023, the total number of paper and paperboard manufacturing enterprises in China stood at 2,500, with a nationwide paper and paperboard output of 129.65 Million tons, a 4.35% increase from the previous year.

* Thus, the above factors are expected to drive the hot-melt adhesives market in the region during the forecast period.

Hot-melt Adhesives Industry Overview

The global hot-melt adhesives market is fragmented in nature. Some of the major players in the market (not in any particular order) include 3M, Jowat SE, Henkel Corporation, Arkema, and H.B. Fuller, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand from Packaging Industry

- 4.1.2 Rising Demand from Construction Sector

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Volatility in Raw Material Prices

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size by Value)

- 5.1 Resin Type

- 5.1.1 Ethylene Vinyl Acetate

- 5.1.2 Styrenic Block Co-polymers

- 5.1.3 Thermoplastic Polyurethane

- 5.1.4 Other Resin Types (Polyolefin, polyamide)

- 5.2 End-user Industry

- 5.2.1 Building and Construction

- 5.2.2 Paper, Board, and Packaging

- 5.2.3 Woodworking and Joinery

- 5.2.4 Automotive and Transportation

- 5.2.5 Footwear and Leather

- 5.2.6 Healthcare

- 5.2.7 Electrical and Electronic Appliances

- 5.2.8 Other End-user Industries

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Malaysia

- 5.3.1.6 Thailand

- 5.3.1.7 Indonesia

- 5.3.1.8 Vietnam

- 5.3.1.9 ASEAN Countries

- 5.3.1.10 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Turkey

- 5.3.3.6 Spain

- 5.3.3.7 Russia

- 5.3.3.8 NORDIC

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Nigeria

- 5.3.5.4 Egypt

- 5.3.5.5 Qatar

- 5.3.5.6 UAE

- 5.3.5.7 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share(%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 3M

- 6.4.2 Alfa International

- 6.4.3 Arkema

- 6.4.4 Ashland

- 6.4.5 AVERY DENNISON CORPORATION

- 6.4.6 Beardow Adams

- 6.4.7 Dow

- 6.4.8 DRYTAC

- 6.4.9 Franklin International

- 6.4.10 H.B. Fuller Company

- 6.4.11 Henkel Corporation

- 6.4.12 Hexcel Corporation

- 6.4.13 Huntsman International LLC

- 6.4.14 Jowat SE

- 6.4.15 Mactac

- 6.4.16 Master Bond Inc.

- 6.4.17 Paramelt RMC B.V.

- 6.4.18 Pidilite Industries Limited

- 6.4.19 Sika AG

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Expansion in Automotive Manufacturing

- 7.2 Advancements in Construction Technologies

2024年全球聚醯胺熱熔膠市場報告

2024年全球聚醯胺熱熔膠市場報告 2025-2033 年日本熱熔膠市場報告(依樹脂類型、產品形式、應用和地區)

2025-2033 年日本熱熔膠市場報告(依樹脂類型、產品形式、應用和地區) 建築膠帶市場:按技術、樹脂類型、應用和最終用途分類 – 2025-2030 年全球預測

建築膠帶市場:按技術、樹脂類型、應用和最終用途分類 – 2025-2030 年全球預測 熱熔膠市場:依樹脂類型、形狀、通路、應用分類 - 黏劑年全球預測

熱熔膠市場:依樹脂類型、形狀、通路、應用分類 - 黏劑年全球預測 熱熔膠帶市場:按產品、黏合樹脂、背襯材料、膠帶、應用 - 2025-2030 年全球預測

熱熔膠帶市場:按產品、黏合樹脂、背襯材料、膠帶、應用 - 2025-2030 年全球預測 紫外線固化丙烯酸膠帶市場:按產品和應用分類的全球預測 - 2025-2030

紫外線固化丙烯酸膠帶市場:按產品和應用分類的全球預測 - 2025-2030 PA 熱熔膠黏劑市場:趨勢、預測、競爭分析(~2030 年)

PA 熱熔膠黏劑市場:趨勢、預測、競爭分析(~2030 年) PA熱熔膠黏劑全球市場:趨勢、預測與競爭分析(~2030年)

PA熱熔膠黏劑全球市場:趨勢、預測與競爭分析(~2030年) 反應型熱熔膠市場報告:2030 年黏劑、預測與競爭分析

反應型熱熔膠市場報告:2030 年黏劑、預測與競爭分析 PU系反應性熱熔膠黏劑的全球市場:類型·基材·用途·不同地區的預測 (~2030年)

PU系反應性熱熔膠黏劑的全球市場:類型·基材·用途·不同地區的預測 (~2030年)