|

市場調查報告書

商品編碼

1536943

地工織物:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029)Geotextile - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

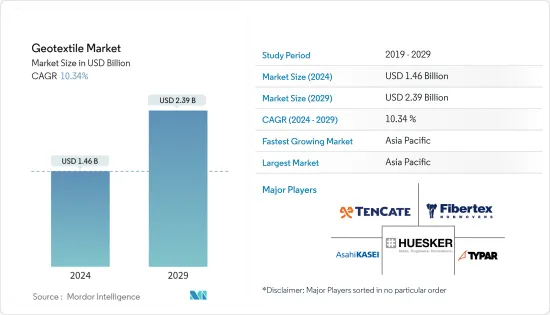

地工織物市場規模預計到 2024 年為 14.6 億美元,預計到 2029 年將達到 23.9 億美元,在預測期內(2024-2029 年)複合年成長率為 10.34%。

由於封鎖、社交距離和貿易制裁對全球供應鏈網路造成重大干擾,COVID-19 大流行阻礙了市場。由於活動停止,道路建設產業出現下滑。然而,這種情況預計將在 2021 年恢復,並在預測期內使市場受益。

主要亮點

- 推動市場的主要因素是地工織物在建設產業和採礦活動中的使用不斷增加,以及嚴格的環境保護法規結構。

- 原物料價格的波動預計將阻礙市場成長。

- 製造業節水意識的增強預計將成為未來市場的機會。

- 預計亞太地區將主導全球市場,政府投資建設公路和鐵路計劃將導致中國、日本和印度等國家對地工織物的巨大需求。

地工織物市場趨勢

道路建設需求增加

- 地工織物主要由聚丙烯、聚酯和聚乙烯等合成聚合物製成,具有極強的抗生物和化學過程腐爛能力。

- 這項特性使得地工織物適用於道路建設和維護。在過去的十年中,地工織物在全球建設產業的使用大幅成長。

- 根據歐洲一次性不織布協會(EDANA)的資料,每年生產和銷售的地工織物不織布約750公里,其中60%用於道路建設。

- 這些材料具有透水性編織結構,主要用於建築應用。地工織物在建築領域的可能應用已成功開發。地工織物在經濟性、性能和耐用性方面具有顯著的優勢。

- 此外,全球建築支出和建築活動的增加可能會導致對地工織物的需求增加。例如,在 2024 會計年度,聯邦公路管理局將向 12 個官方項目投資 610 億美元,以支持道路、橋樑、隧道、碳排放和安全改進等關鍵基礎設施的投資。基礎設施投資和就業法案 (IIJA) 資金分配給所有 50 個美國、哥倫比亞特區和波多黎各。

- 此外,預計2024年美國公路橋樑建設額將與前一年同期比較增23%,達1,471億美元。此外,到2024年,該國交通建設工程總價值可能達到2,140億美元,成長14%。

- 大多數可用的地工織物由聚丙烯或聚酯製成。聚丙烯材料堅固、耐用且比水輕。據全球領先材料製造商之一的HUBS稱,聚丙烯佔全球產量的35-40%,其次是聚乙烯(15%)、ABS(25%)和聚苯乙烯(10%)等其他材料。

- 多家公司正在投資建造聚丙烯 (PP) 製造廠,以增加 PP 材料的產量,這些材料擴大用於建設活動。例如,2022年7月,加拿大Heartland Polymers公司位於加拿大亞伯達Heartland石化聯合體的聚丙烯(PP)裝置運作全面營運,規劃年產聚丙烯產能52.5萬噸。

- 這些材料用於道路、高速公路、土壩、鐵路、土壤穩定、排水控制、隧道施工等建設。

- 因此,預計上述因素將在預測期內推動地工織物市場的發展。

亞太地區主導市場

- 在全球地工織物整體市場中,亞太地區佔據最大的市場佔有率。建設產業的持續市場開拓是該地區地工織物市場的主要促進因素。

- 由於中國全年承接大型基礎設施計劃,預計中國將成為該地區地工織物的主要市場。例如,中國政府的目標是到2025年將高鐵網路擴展至5萬公里。

- 中國國家統計局數據顯示,2023年全國基礎建設投資較2022年成長5.9%。

- 據印度品牌股權基金會稱,由於政府不斷舉措改善該國的交通基礎設施,印度公路和高速公路市場預計到 2025 年複合年成長率將達到 36.16%。

- 根據印度國家投資促進和便利化局統計,公路網總長度為637萬公里,包括所有類別的公路(國道、邦道、城市和鄉村公路),是世界第二大公路網。此外,該國於2020年推出了國家基礎設施管道(NIP),預計2020年至2025年將投資13,380億美元。

- 其他亞太國家的建築業也與前一年同期比較成長。例如,根據韓國央行的數據,2023年韓國建築業將累計約671億美元,較2022年成長4%。

- 因此,上述因素可能會在預測期內推動亞太地區對地工織物的需求。

地工織物行業概況

地工織物市場部分分散。主要企業(排名不分先後)包括 Fibertex Non-fabric AS (Schouw &Co.)、HUESKER、TYPAR Geosynthetics、Tencate Geosynthetics 和 Asahi Kasei Advance。

其他好處:

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 調查先決條件

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 促進因素

- 擴大地工織物在建築業的使用

- 採礦業中地工織物的使用增加

- 嚴格的環境保護法規結構

- 抑制因素

- 原物料價格波動

- 其他阻礙因素

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章 市場區隔(以金額為準的市場規模)

- 按材質

- 聚丙烯

- 聚酯纖維

- 聚乙烯

- 其他材料

- 按類型

- 織物

- 不織布

- 針織

- 其他類型

- 按用途

- 道路建設與路面修復

- 侵蝕

- 引流

- 鐵路建設

- 農業

- 其他用途

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 泰國

- 馬來西亞

- 印尼

- 越南

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 義大利

- 法國

- 俄羅斯

- 北歐的

- 西班牙

- 土耳其

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 哥倫比亞

- 南美洲其他地區

- 中東/非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 卡達

- 奈及利亞

- 埃及

- 其他中東/非洲

- 亞太地區

第6章 競爭狀況

- 併購、合資、聯盟、協議

- 市場佔有率(%)**/排名分析

- 主要企業策略

- 公司簡介

- AFITEXINOV

- AGRU AMERICA INC.

- Asahi Kasei Advance Corporation.

- Carthage Mills Inc.

- Fibertex Nonwovens AS(Schouw & Co.)

- GSE Environmental

- HUESKER

- Kaytech

- Low & Bonar

- Mattex Geosynthetics

- Naue GmbH & Co. KG

- Officine Maccaferri SpA

- Owens Corning

- Swicofil AG

- Tencate Geosynthetics

- Thrace Group

- TYPAR Geosynthetics

第7章 市場機會及未來趨勢

- 製造業節水意識增強

- 其他機會

The Geotextile Market size is estimated at USD 1.46 billion in 2024, and is expected to reach USD 2.39 billion by 2029, growing at a CAGR of 10.34% during the forecast period (2024-2029).

The COVID-19 pandemic hindered the market because lockdowns, social distancing, and trade sanctions caused significant disruptions to global supply chain networks. The road construction industry witnessed a decline due to the halt in activities. However, the condition recovered in 2021, which is expected to benefit the market during the forecast period.

Key Highlights

- Major factors driving the market are the increasing use of geotextiles in the construction industry and mining activities and the stringent regulatory framework for environmental protection.

- The fluctuating prices of raw materials are expected to hinder the market's growth.

- Rising awareness about water conservation in the manufacturing sector is expected to act as an opportunity for the market in the future.

- Asia-Pacific is expected to dominate the global market due to government investments in the construction of roads and rail projects, leading to a huge demand for geotextiles from countries such as China, Japan, and India.

Geotextile Market Trends

Increasing Demand in Road Construction

- Geotextiles are made from synthetic polymers, mainly polypropylene, polyester, polyethylene, and others, that are very unlikely to decay under biological and chemical processes.

- This feature makes geotextiles suitable for the construction and maintenance of roads. In the past decade, there has been considerable growth in the usage of geotextiles in the construction industry worldwide.

- According to data from the European Disposables and Non-wovens Association (EDANA), around 750 km of geotextile non-wovens are manufactured and sold every year, of which 60% is used for the construction of roads.

- These materials have permeable textile structures and are used primarily in construction applications. The possible applications of geotextiles in the construction sector have been successfully developed. They offer significant benefits in terms of financial feasibility, performance, and durability.

- Moreover, the increase in construction spending and work worldwide may lead to increased demand for geotextiles. For instance, the Federal Highway Administration for the fiscal year 2024 allocated USD 61 billion for 12 formula programs to aid investment in critical infrastructure, including roads, bridges, tunnels, carbon-emission reduction, and safety improvements. This funding from the IIJA (Infrastructure Investment and Jobs Act) was allocated for all 50 US states, the District of Columbia, and Puerto Rico.

- Furthermore, highway and bridge construction in the United States is expected to increase by 23% to USD 147.1 billion in 2024 over the previous year. Additionally, the country's total value of transportation construction work may grow by 14% to USD 214 billion in 2024.

- Most of the available geotextiles are made of polypropylene or polyester. Polypropylene material is strong and durable and is lighter than water. According to a globally leading material manufacturing company, HUBS polypropylene accounts for 35% to 40% of worldwide output, followed by other materials like polyethylene (15%), ABS (25%), and polystyrene (10%).

- Various companies are investing in their polypropylene (PP) manufacturing plants to increase the output of PP material that will be used more in construction activities. For instance, in July 2022, the Canadian company Heartland Polymers fully commissioned its polypropylene (PP) plant with a planned production capacity of 525,000 tons of polypropylene per year at the Heartland Petrochemical Complex in Alberta, Canada.

- These materials are used in the construction of roads, highways, earth dams, and railroads, in the stabilization of soil, control of drainage, tunnel construction, etc.

- Thus, the above-mentioned factors are expected to drive the geotextile market during the forecast period.

Asia-Pacific to Dominate the Market

- Asia-Pacific held the largest market share in the overall geotextile market worldwide. The ongoing developments in the construction industry are the main drivers of the geotextile market in the area.

- China is expected to be the major market for geotextiles in the region as the country has mega-scale infrastructure projects year-round. For instance, the Chinese government is working to expand its high-speed railway network to 50,000 km by 2025.

- According to the National Bureau of Statistics of China, the country's infrastructure investment in 2023 increased 5.9% in value compared to 2022.

- According to the India Brand Equity Foundation, the Indian roads and highways market is projected to register a CAGR of 36.16% in 2025 on account of growing government initiatives to improve transportation infrastructure in the country.

- According to the National Investment Promotion and Facilitation Agency, India, the total road network is 6.37 million km, comprising all categories of roads (national and state highways, urban and rural roads), which is the second largest in the world. Furthermore, the country launched the National Infrastructure Pipeline (NIP) in 2020, which envisages an investment of USD 1,338 billion between 2020 and 2025.

- The construction sector of other Asia-Pacific countries is also growing Y-o-Y. For instance, according to the Bank of Korea, South Korea's construction sector accounted for approximately USD 67.1 billion in 2023, representing a 4% growth rate over 2022.

- Therefore, the aforementioned factors may fuel the demand for geotextiles in Asia-Pacific during the forecast period.

Geotextile Industry Overview

The geotextile market is partially fragmented in nature. The major companies (not in any particular order) include Fibertex Non-woven AS (Schouw & Co.), HUESKER, TYPAR Geosynthetics, Tencate Geosynthetics, and Asahi Kasei Advance Corporation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Usage of Geotextiles in Construction Industry

- 4.1.2 Increase Usage of Geotextiles in Mining Activities

- 4.1.3 Stringent Regulatory Framework for Environmental Protection

- 4.2 Restraints

- 4.2.1 Fluctuating Raw Material Prices

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 By Material

- 5.1.1 Polypropylene

- 5.1.2 Polyester

- 5.1.3 Polyethylene

- 5.1.4 Other Materials

- 5.2 By Type

- 5.2.1 Woven

- 5.2.2 Non-woven

- 5.2.3 Knitted

- 5.2.4 Other Types

- 5.3 By Application

- 5.3.1 Road Construction and Pavement Repair

- 5.3.2 Erosion

- 5.3.3 Drainage

- 5.3.4 Railworks

- 5.3.5 Agriculture

- 5.3.6 Other Applications

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Thailand

- 5.4.1.6 Malaysia

- 5.4.1.7 Indonesia

- 5.4.1.8 Vietnam

- 5.4.1.9 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 Italy

- 5.4.3.4 France

- 5.4.3.5 Russia

- 5.4.3.6 NORDIC

- 5.4.3.7 Spain

- 5.4.3.8 Turkey

- 5.4.3.9 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 United Arab Emirates

- 5.4.5.4 Qatar

- 5.4.5.5 Nigeria

- 5.4.5.6 Egypt

- 5.4.5.7 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 AFITEXINOV

- 6.4.2 AGRU AMERICA INC.

- 6.4.3 Asahi Kasei Advance Corporation.

- 6.4.4 Carthage Mills Inc.

- 6.4.5 Fibertex Nonwovens AS (Schouw & Co.)

- 6.4.6 GSE Environmental

- 6.4.7 HUESKER

- 6.4.8 Kaytech

- 6.4.9 Low & Bonar

- 6.4.10 Mattex Geosynthetics

- 6.4.11 Naue GmbH & Co. KG

- 6.4.12 Officine Maccaferri SpA

- 6.4.13 Owens Corning

- 6.4.14 Swicofil AG

- 6.4.15 Tencate Geosynthetics

- 6.4.16 Thrace Group

- 6.4.17 TYPAR Geosynthetics

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Rising Awareness about Water Conservation in the Manufacturing Sector

- 7.2 Other Opportunities

地工織物市場規模、佔有率及成長分析(按材料類型、技術類型、應用和地區)-2025-2032 年產業預測

地工織物市場規模、佔有率及成長分析(按材料類型、技術類型、應用和地區)-2025-2032 年產業預測 北美地工織物市場:市場規模、佔有率、趨勢分析(按材料、產品、應用和國家)、細分市場預測(2025-2030 年)

北美地工織物市場:市場規模、佔有率、趨勢分析(按材料、產品、應用和國家)、細分市場預測(2025-2030 年) 美國地工織物市場:市場規模、佔有率、趨勢分析(按材料、產品和應用)、細分市場預測(2025-2030 年)

美國地工織物市場:市場規模、佔有率、趨勢分析(按材料、產品和應用)、細分市場預測(2025-2030 年) 地工織物的全球市場:市場規模·佔有率·趨勢,產業分析 (各技術·各材料·各用途·各地區),未來預測 (2025年~2034年)

地工織物的全球市場:市場規模·佔有率·趨勢,產業分析 (各技術·各材料·各用途·各地區),未來預測 (2025年~2034年) 2024 年 Sabo 與沉積物控制全球市場報告

2024 年 Sabo 與沉積物控制全球市場報告 地工織物市場規模、佔有率和成長分析(按材料、產品、應用、最終用途、地區):產業預測(2024-2031)

地工織物市場規模、佔有率和成長分析(按材料、產品、應用、最終用途、地區):產業預測(2024-2031) 地工織物市場:按材料、產品和應用分類 - 2025-2030 年全球預測

地工織物市場:按材料、產品和應用分類 - 2025-2030 年全球預測 地工織物的市場規模,佔有率,預測,趨勢分析:各材料,各產品類型,各用途,各部門,各地區-2031年前的世界預測

地工織物的市場規模,佔有率,預測,趨勢分析:各材料,各產品類型,各用途,各部門,各地區-2031年前的世界預測 全球土工織物市場評估:依材料類型、產品類型、應用、最終用戶、地區、機會、預測(2016-2030)

全球土工織物市場評估:依材料類型、產品類型、應用、最終用戶、地區、機會、預測(2016-2030) 到 2030 年的 Geotube 市場預測:按材料、應用和地區進行的全球分析

到 2030 年的 Geotube 市場預測:按材料、應用和地區進行的全球分析