|

市場調查報告書

商品編碼

1537608

滑爽添加劑:市場佔有率分析、產業趨勢/統計、成長預測(2024-2029)Slip Additives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

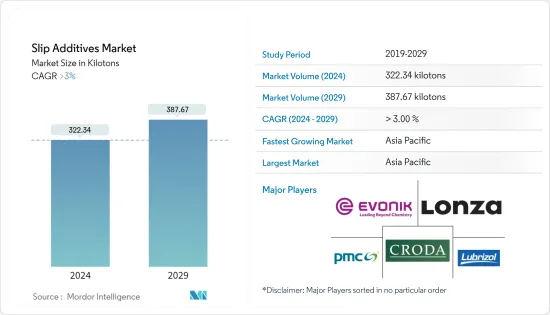

預計2024年全球滑爽添加劑市場規模將達322.34千噸,2029年將達到387.67千噸,2024-2029年預測期間複合年成長率將超過3%。

COVID-19 大流行對滑爽添加劑市場產生了正面影響。封鎖期間,消費品、藥品、食品和飲料等網路銷售增加了對包裝產品的需求,而滑爽添加劑的市場前景樂觀。 COVID-19大流行後,由於包裝和非包裝應用的需求增加,市場進一步成長。

食品和飲料包裝行業需求的增加以及與替代品相比價格更低的供應預計將推動矽膠塗料市場的發展。

有關塑膠使用的嚴格環境法規預計將阻礙市場成長。

生物基滑爽添加劑的市場開拓以及醫療應用中塑膠薄膜需求的增加預計將在預測期內為市場創造機會。

預計亞太地區將主導市場。此外,包裝和非包裝應用中對滑爽添加劑的需求不斷成長,預計在預測期內仍將保持最高複合年成長率。

滑爽添加劑市場趨勢

包裝應用主導市場

- 推動滑爽添加劑需求增加的主要因素是其在食品和飲料行業中的使用量增加。塑膠包裝有助於延長包裝產品的保存期限並減少食品洩漏。

- 包裝產業的一個重要趨勢是禁止使用一次性塑膠,以在不影響產品安全和衛生的情況下減少包裝廢棄物。這些因素預計將增加對聚烯塑膠包裝薄膜的需求。滑爽添加劑用於減少摩擦,似乎有助於賦予包裝材料所需的性能。

- 包裝行業預計將是滑爽添加劑應用最廣泛的領域。聚合物薄膜主要用於包裝和標籤。滑爽添加劑在聚乙烯薄膜和鑄膜生產中的重要作用是賦予薄膜表面滑爽性能。

- 食品包裝市場在未來幾年可能會出現顯著的成長。根據食品服務包裝協會預測,2022年全球食品包裝市場銷售額預計將達3.638億美元,2026年將達到4.583億美元。因此,食品包裝市場的成長預計將推動當前的研究市場。

- 在製藥業,聚乙烯和聚丙烯包裝被廣泛用作初級包裝材料。這些包裝材料用途廣泛、性能優異,可用於醫療和製藥應用。塑膠薄膜可保護藥品免受氧氣、異味、濕氣、水蒸氣傳輸、污染和細菌的影響。塑膠薄膜用於各種塑膠包裝產品,例如滴管和注射器。近年來,全球醫藥市場顯著成長。 2022年,全球醫藥市場規模達1.48兆美元,與前一年同期比較同期成長4.2%。

- 因此,對食品和飲料包裝以及藥品包裝應用的需求不斷增加將推動對滑爽添加劑的需求。

亞太地區主導市場

- 亞太地區是全球最大的滑爽添加劑市場。中國、印度和日本是該地區最大的滑爽添加劑市場。

- 在亞太地區,不斷成長的中階人口、快速工業化以及包裝產品使用量的增加等因素預計將推動包裝行業的發展,導致滑爽添加劑市場的成長前景各不相同。

- 中國和印度是該地區最大的食品和飲料市場。根據中國國家輕工業委員會統計,年銷售額超過280萬美元的主要食品生產企業2022年收益超過1.53兆美元。與2021年相比,總收入年與前一年同期比較5.6%,顯示食品業成長強勁。因此,食品和飲料行業的成長預計將增加食品和飲料包裝應用中使用的滑爽添加劑的需求。

- 同樣,藥品包裝應用中對滑爽添加劑的需求也在增加。印度是世界製藥中心,向 200 多個國家出口藥品。 2023年上半年,流入醫藥產業的外商直接投資成長25%。根據IBEF預測,到2024年,製藥業的收益預計將達到650億美元。因此,醫藥市場的擴大將帶動目前的研究市場。

- 日本目前是世界第三大電子商務市場。預計2023年,日本電子商務市場收益將達到2,322億美元,到2027年將進一步達到3,554億美元。消費者在日本化妝品市場購買產品時也變得更加挑剔和注重價值。因此,電商市場的擴大將促進日本的包裝應用,帶動滑爽添加劑市場。

- 由於上述因素,亞太滑爽添加劑市場預計在預測期內將顯著成長。

滑爽添加劑產業概況

滑爽添加劑市場因其性質而部分分散。該市場的主要企業包括(排名不分先後)Croda International Plc、Evonik Industries AG、Lonza、PMC Group, Inc. 和 The Lubrizol Corporation。

其他好處:

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 調查先決條件

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 促進因素

- 食品和飲料包裝產業需求增加

- 與替代品相比,價格較低

- 其他司機

- 抑制因素

- 關於塑膠使用的嚴格環境法規

- 其他限制因素

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 買方議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章市場區隔(市場規模:基於數量)

- 載體樹脂

- 聚乙烯

- 聚丙烯

- 其他載體樹脂

- 類型

- 脂肪醯胺

- 蠟聚矽氧烷

- 其他類型

- 目的

- 包裝

- 食品/飲料

- 消費品

- 衛生保健

- 展開的

- 包裝

- 地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 義大利

- 法國

- 歐洲其他地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東/非洲

- 沙烏地阿拉伯

- 南非

- 其他中東/非洲

- 亞太地區

第6章 競爭狀況

- 併購、合資、聯盟和協議

- 市場佔有率(%)/排名分析

- 主要企業策略

- 公司簡介

- Afron

- ALTANA

- BASF SE

- Croda International Inc.

- Emery Oleochemicals

- Evonik Industries AG

- Fine Organics

- Honeywell International

- Lonza

- The Lubrizol Corporation

- PMC Group, Inc.

第7章市場機會與未來趨勢

- 生物基滑爽添加劑的開發

- 醫療應用對塑膠薄膜的需求增加

The Slip Additives Market size is estimated at 322.34 kilotons in 2024, and is expected to reach 387.67 kilotons by 2029, growing at a CAGR of greater than 3% during the forecast period (2024-2029).

The COVID-19 pandemic had a positive impact on the slip additives market. During the lockdown, the online sales of consumer goods, pharmaceuticals, food, and beverage products increased the demand for packaged products, thus creating a positive market outlook for slip additives. Post-COVID-19 pandemic, the market further registered a growth rate due to rising demand from packaging and non-packaging applications.

Increasing demand from the food and beverage packaging industry and the availability at low prices compared to substitutes are expected to drive the market for silicone coatings.

The stringent environmental regulations on the use of plastics are expected to hinder the market's growth.

The development of bio-based slip additives and the increasing demand for plastic films in medical applications are expected to create opportunities for the market during the forecast period.

The Asia-Pacific region is expected to dominate the market. It is also expected to register the highest CAGR during the forecast period due to rising demand for slip additives in packaging and non-packaging applications.

Slip Additives Market Trends

Packaging Application to Dominate the Market

- The increasing demand for slip additives is majorly attributed to the growing usage in the food & beverage industry. Plastic packaging helps increase the shelf life of the products packed and reduces leakages of food products.

- One of the significant trends in the packaging industry is the ban on the usage of single-use plastic to reduce packaging waste without compromising the safety and hygiene of the products. These factors will increase the demand for polyolefin plastic packaging films. The slip additives are used to decrease friction and will likely help to get the desired properties in the packaging material.

- The packaging segment is anticipated to be the most extensive application of slip additives. Polymer films are mainly preferred in the packaging industry for packing and labeling. The critical function of slip additives in the production of polyethylene and cast film is to deliver slip properties to the film surface.

- The food packaging market is likely to register a significant growth rate in the coming years. According to the Foodservice Packaging Association, the global food packaging market revenue is recorded at USD 363.8 million in 2022, and it is projected to reach USD 458.3 million by 2026. Thus, the growth in the food packaging market will drive the current studied market.

- In the pharmaceutical industry, polyethylene and polypropylene packaging are widely used as primary packaging materials. These packaging materials are versatile, high-performance, and used in medical and pharmaceutical applications. The plastic films protect the pharmaceutical product against oxygen and odor, moisture, water vapor transmission, contamination, and bacteria. They are used in various plastic packaging products, including eyedroppers, syringes, and others. The global pharmaceutical market has grown significantly in recent years. In 2022, the global pharmaceutical market registered at USD 1.48 trillion, at a growth rate of 4.2% compared to the previous year.

- Thus, the growing demand for food and beverage packaging and pharmaceutical packaging applications will drive the demand for slip additives.

Asia-Pacific Region to Dominate the Market

- The Asia-Pacific is the largest market for slip additives in the world. China, India, and Japan are the largest markets for slip additives in the region.

- In the Asia-Pacific region, factors such as the growing middle-class population, rapid industrialization, and the increasing usage of packed products are expected to drive the packaging industry, providing various growth prospects to the slip additives market.

- China and India are the largest food and beverage markets in the region. According to the China National Light Industry Council, major food manufacturing companies with an annual turnover of over USD 2.8 million reported revenues of over USD 1.53 trillion in 2022. Compared to 2021, the total revenue registered a year-on-year growth of 5.6%, indicating strong growth in the food industry. Thus, the growth of the food and beverage industries is expected to increase the demand for slip additives used in food and beverage packaging applications.

- Similarly, the demand for slip additives is increasing in pharmaceutical packaging applications. India is a global pharmaceutical hub, exporting pharmaceuticals to over 200 countries. In the first half of FY 2023, foreign direct investment inflows into the pharmaceutical industry increased by 25%. According to IBEF, the pharmaceutical industry revenue is expected to reach USD 65 billion by 2024. Thus, the increasing market for pharmaceuticals will drive the current studied market.

- Japan is currently the world's third most prominent e-commerce market in the world. Revenue in the e-commerce market in Japan was expected to generate USD 232.20 billion by 2023 and is further expected to reach USD 355.40 billion by 2027. Also, consumers purchasing goods within the cosmetics market in Japan are becoming more selective and value-conscious. Thus, the increasing e-commerce market will drive the packaging application in the country, thereby driving the market for slip additives.

- Owing to the factors mentioned above, the slip additives market in the Asia-Pacific is projected to grow significantly during the forecast period.

Slip Additives Industry Overview

The slip additives market is partially fragmented in nature. Some of the major players in the market include (not in any particular order) Croda International Plc, Evonik Industries AG, Lonza, PMC Group, Inc., and The Lubrizol Corporation, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand from Food & Beverage Packaging Industry

- 4.1.2 Availability at Low Price Compared to Substitutes

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Stringent Environmental Regulations on The Use of Plastics

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Carrier Resin

- 5.1.1 Polyethylene

- 5.1.2 Polypropylene

- 5.1.3 Other Carrier Resins (Polyvinyl Chloride, Polyamide,etc.)

- 5.2 Type

- 5.2.1 Fatty Amides

- 5.2.2 Waxes and Polysiloxanes

- 5.2.3 Other Types (Esters, Salts, etc.)

- 5.3 Application

- 5.3.1 Packaging

- 5.3.1.1 Food and Beverage

- 5.3.1.2 Consumer Goods

- 5.3.1.3 Healthcare

- 5.3.2 Non-Packaging

- 5.3.1 Packaging

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 Italy

- 5.4.3.4 France

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Afron

- 6.4.2 ALTANA

- 6.4.3 BASF SE

- 6.4.4 Croda International Inc.

- 6.4.5 Emery Oleochemicals

- 6.4.6 Evonik Industries AG

- 6.4.7 Fine Organics

- 6.4.8 Honeywell International

- 6.4.9 Lonza

- 6.4.10 The Lubrizol Corporation

- 6.4.11 PMC Group, Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Development of Bio-based Slip Additives

- 7.2 The Increasing Demand for Plastic Films in Medical Applications

全球潤滑添加劑市場研究報告 - 產業分析、規模、佔有率、成長、趨勢和預測 2025 年至 2033 年

全球潤滑添加劑市場研究報告 - 產業分析、規模、佔有率、成長、趨勢和預測 2025 年至 2033 年 潤滑添加劑市場規模、佔有率和成長分析(按載體樹脂、類型、應用和地區)- 產業預測,2025-2032 年

潤滑添加劑市場規模、佔有率和成長分析(按載體樹脂、類型、應用和地區)- 產業預測,2025-2032 年 滑爽添加劑市場:按類型、載體樹脂、應用分類 - 2025-2030 年全球預測

滑爽添加劑市場:按類型、載體樹脂、應用分類 - 2025-2030 年全球預測 全球滑爽添加劑市場 - 2024-2031

全球滑爽添加劑市場 - 2024-2031 滑爽添加劑市場規模、佔有率、趨勢分析報告:按類型、按載體樹脂、按最終應用、按地區、細分市場預測,2024-2030 年全球滑爽添加劑市場研究報告 - 2024 年至 2032 年產業分析、規模、佔有率、成長、趨勢與預測滑爽添加劑市場- 按類型(脂肪醯胺、蠟和聚矽氧烷、硬脂酸鹽)、按載體樹脂、按應用(包裝薄膜、消費品、汽車、農用薄膜、建築、製藥)及預測,2024 - 2032 年全球滑爽添加劑市場

滑爽添加劑市場規模、佔有率、趨勢分析報告:按類型、按載體樹脂、按最終應用、按地區、細分市場預測,2024-2030 年全球滑爽添加劑市場研究報告 - 2024 年至 2032 年產業分析、規模、佔有率、成長、趨勢與預測滑爽添加劑市場- 按類型(脂肪醯胺、蠟和聚矽氧烷、硬脂酸鹽)、按載體樹脂、按應用(包裝薄膜、消費品、汽車、農用薄膜、建築、製藥)及預測,2024 - 2032 年全球滑爽添加劑市場 滑爽添加劑市場——2023年至2028年預測

滑爽添加劑市場——2023年至2028年預測