|

市場調查報告書

商品編碼

1537609

聚異丁烯(PIB):市場佔有率分析、產業趨勢/統計、成長預測(2024-2029)Polyisobutylene (PIB) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

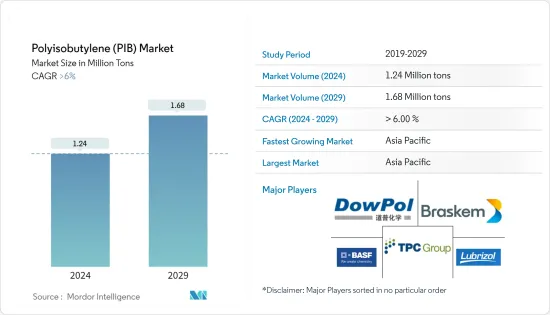

預計2024年全球聚異丁烯(PIB)市場規模將達到124萬噸,2029年將達到168萬噸,2024-2029年的複合年成長率將超過6%。

主要亮點

- 由於遏制措施和經濟中斷,黏劑、密封劑和潤滑劑等行業被迫推遲生產,導致生產和運輸放緩,市場受到了 COVID-19 大流行的負面影響。目前市場正從疫情中恢復。預計2022年市場將達到疫情前水準並持續穩定成長。

- 推動所研究市場的主要因素是黏劑和密封劑行業需求的不斷成長。

- 另一方面,聚異丁烯(PIB)由於缺乏抗紫外線能力而不穩定,阻礙了市場成長。

- 聚異丁烯(PIB)有望作為皮革製造人員編制中羊毛脂的替代,為市場成長提供各種機會。

- 亞太地區主導全球市場,最大的消費來自中國、日本、韓國和印度等國家。

聚異丁烯(PIB)市場趨勢

對黏劑和密封劑產業的需求增加

- 預計黏劑和密封劑產業在預測期內將出現巨大需求。聚異丁烯(PIB)在黏劑和密封劑行業的主要用途包括密封接縫、密封和保護電線以及防潮車身腔體。

- 聚異丁烯(PIB)以壓敏黏著劑和熱熔黏劑的形式用於黏劑系統。由於其黏性、柔韌性和低內聚力,主要用於膠合劑和黏劑。

- 2023年6月,漢高宣佈在中國增設一座新的黏劑製造工廠。漢高黏合劑技術公司的新製造工廠位於中國山東省煙台化學工業園區。新工廠「鯕鵬」的建設成本預計約為8.7億元人民幣(1.19億美元)。新廠增加了漢高在中國高抗衝黏劑產品的產能,並進一步最佳化其供應鏈,以滿足國內外市場不斷成長的需求。

- 2023年5月,黏劑製造商喬瓦特宣布將在中國建立自己的黏劑中心,擴大在亞太地區的業務。位於亞洲的新黏劑中心佔地超過11,000平方公尺,預計於2023年完工。

- 亞太地區住宅的成長預計將受到壓敏黏著劑和熱熔黏劑的推動。聚異丁烯 (PIB) 密封劑用於防潮、橡膠屋頂修復和屋頂薄膜維護。

- 亞太地區是全球最大的辦公大樓市場。根據高緯環球 (Cushman & Wakefield) 的報告,預計到 2030 年,亞太地區平均每年將有 1.2 億平方英尺的辦公建築面積。因此,隨著辦公活動的增加,辦公用品中聚異丁烯(PIB)的需求也預計將大幅增加。

- 各建設公司都認為歐洲辦公空間有著長遠的未來。此外,多家公司正在投資商業領域的建設計劃,推動了對聚異丁烯(PIB)的需求。

- 中國是辦公空間建設的領先國家之一。中國武漢復星外灘中心T1等辦公空間的建設預計將推動所研究的市場的發展。該計劃的建設工作預計將於2021年第三季開始,並於2025年第四季完工。

- 此外,根據中國國家統計局的數據,2022年中國建築業產值達到高峰約4.11兆美元。結果,這些因素往往會增加市場需求。

- 預計黏劑和密封劑產業將在預測期內主導全球聚異丁烯(PIB)市場。

亞太地區主導市場

- 在預測期內,聚異丁烯(PIB)市場預計將由亞太地區主導。這是因為該地區主導著黏劑、密封劑、潤滑劑和燃料添加劑等應用市場。

- 2023年3月,Pidilite宣佈在印度生產Jowat黏劑。黏劑將在 Pidilite 位於古吉拉突邦皮的製造工廠生產。該公司進一步宣布,黏劑將以 Pidilite 品牌生產。

- 聚異丁烯(PIB)廣泛用於潤滑油中,調節和提高潤滑油的黏度至所需的最終黏度。由於更好和改進的性能,例如降低可燃性、減少齒輪磨損和延長使用壽命,潤滑油市場目前對高性能潤滑油的需求不斷增加。

- 聚異丁烯(PIB)被添加到燃料中以改善其黏彈性。聚異丁烯 (PIB) 衍生物用作無灰分散劑(例如 PIBSA),以最大限度地減少沉積物並防止油稠化和油泥形成。

- 因此,汽車行業的成長預計將拉動市場需求。中國是世界上最大的汽車製造國。由於對環境問題的日益關注,該國的汽車行業正在專注於製造在確保燃油效率的同時最大限度地減少排放氣體的產品,並正在努力改進其產品。

- 根據OICA(國際汽車構造組織)統計,2022年汽車產量達2,702.1萬輛,汽車銷售量達2,686.4萬輛,與前一年同期比較同期成長3.4%及2.1%。

- 因此,上述聚異丁烯(PIB)應用需求的成長預計將推動亞太地區的市場成長。

聚異丁烯(PIB)產業概況

聚異丁烯(PIB)市場較為分散。研究市場的主要企業包括(排名不分先後)BASF股份公司、Braskem、Dowpol Corporation、TPC Group 和 The Lubrizol Corporation。

其他好處

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 調查先決條件

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 促進因素

- 對黏劑和密封劑的需求增加

- 交通運輸領域對 PIB 的需求不斷增加

- 其他司機

- 抑制因素

- 聚異丁烯 (PIB) 不穩定,不具備抗紫外線能力

- 其他限制因素

- 價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 買方議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章市場區隔(市場規模:基於數量)

- 目的

- 輪胎內胎

- 黏劑/密封劑

- 潤滑劑

- 塑化劑

- 燃料添加劑

- 電絕緣

- 其他用途

- 地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 義大利

- 法國

- 歐洲其他地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東/非洲

- 沙烏地阿拉伯

- 南非

- 其他中東/非洲

- 亞太地區

第6章 競爭狀況

- 併購、合資、聯盟和協議

- 市場佔有率(%)/排名分析

- 主要企業策略

- 公司簡介

- BASF SE

- Braskem

- Dowpol Corporation

- TPC Group

- The Lubrizol Corporation

- Exxon Mobil Corporation

- JX Nippon Oil & Gas Exploration Corporation

- Kemipex

- SABIC

- Zhejiang Shunda New Material Co., Ltd.

第7章 市場機會及未來趨勢

- 聚異丁烯作為皮革生產人員編制中羊毛脂的替代

- 其他機會

簡介目錄

Product Code: 69511

The Polyisobutylene Market size is estimated at 1.24 Million tons in 2024, and is expected to reach 1.68 Million tons by 2029, growing at a CAGR of greater than 6% during the forecast period (2024-2029).

Key Highlights

- The market was negatively impacted by the COVID-19 pandemic as there was a slowdown in production and mobility wherein industries, such as adhesives and sealants, lubricants, etc., were forced to delay their production due to containment measures and economic disruptions. Currently, the market has recovered from the pandemic. The market reached pre-pandemic levels in 2022 and is expected to grow steadily in the future.

- The major factor driving the market studied is increasing demand from the adhesives and sealants industry.

- On the flip side, the instability of polyisobutylene, being non-UV resistant, is hindering the growth of the market.

- Polyisobutylene, as a substitute for wool fat in stuffing agents for the production of leather, is expected to offer various opportunities for the growth of the market.

- Asia-Pacific region dominates the market globally, with the most substantial consumption from countries like China, Japan, South Korea, and India.

Polyisobutylene (PIB) Market Trends

Increasing Demand from Adhesives and Sealants Industry

- The adhesive and sealant industry is anticipated to witness significant demand during the forecast period. Major applications of polyisobutylene in the adhesive and sealant industry are to seal joints, to seal and protect electrical wirings, and to protect body cavities from moisture.

- Polyisobutylene is used in adhesive systems in the form of pressure-sensitive and hot-melt adhesives. It is used due to its tackiness, flexibility, and low cohesive strength, mainly in PSAs and hot-melt adhesives.

- In June 2023, Henkel announced the addition of a new adhesive manufacturing facility in China. The new manufacturing facility of Henkel Adhesive Technologies in the Yantai chemical industry park in Shandong province, China. The new plant, 'Kunpeng,' will cost approximately CNY 870 million (USD 119 Million). The new plant will increase Henkel's production capacity of high-impact adhesive products in China and further optimize the supply chain to meet the increasing demand from domestic and foreign markets.

- In May 2023, Jowat, the adhesive manufacturer, announced to expand its presence in Asia-Pacific with the establishment of its own adhesive center in China. The new adhesive center in Asia will have a surface area of more than 11,000 sq meters and is planned to be finished by 2023.

- Growth in residential construction in the Asia-Pacific region is expected to act as a driver for pressure-sensitive and hot melt adhesives. Polyisobutylene sealant is used for damp proofing, rubber roof repair, and maintenance of roof membranes.

- The Asia-Pacific accounted for the largest market for office construction across the globe. The reports by Cushman & Wakefield state the Asia-Pacific region is likely to incorporate office construction at an average of 120 million square feet annually till 2030. Thus, with the increasing number of office activities, the demand for polyisobutylene in office supplies will also significantly increase.

- Various construction firms consider Europe's long future for office spaces. Also, several companies have invested in construction projects in the commercial sector, driving the demand for polyisobutylene.

- China is one of the leading countries in office space construction. The construction of office spaces such as Wuhan Fosun Bund Center T1 in China is expected to boost the market studied. Construction work for the project started in Q3 2021 and is forecasted to complete in Q4 2025.

- Also, according to the National Bureau of Statistics of China, China's construction output peaked in 2022 at a value of about USD 4.11 trillion. As a result, these factors tend to increase the market demand.

- The adhesives and sealants industry is expected to dominate the global polyisobutylene market over the forecast period.

Asia-Pacific Region to Dominate the Market

- Asia-Pacific is expected to be the dominant market for polyisobutylene during the forecast period. This is because the region dominates the market for applications such as adhesives and sealants, lubricants, fuel additives, and among others.

- In March 2023, Pidilite announced the manufacture of Jowat's hot melt adhesive in India. The adhesives will be produced at Pidilite's manufacturing plant in Vapi, Gujarat. The company further announced that the adhesive will be manufactured under the Pidilite brand.

- Polyisobutylene is widely used in lubricants for modifying or improving the viscosity of the lubricant formulations to the desired final viscosity. The lubricants market is currently witnessing an increasing demand for high-performance lubricants owing to their better and improved properties, such as reduced flammability, reduced gear wear, and increased service life.

- Polyisobutylene is added to fuel to improve the viscoelastic property. Derivatives of polyisobutylene are used as ash-less dispersants (such as PIBSA) to minimize deposits and prevent oil thickening and formation of sludge.

- Thus, the growing automotive industry is expected to boost the market demand. China is the largest manufacturer of automobiles in the world. The country's automotive sector has been shaping up for product evolution, with the country focusing on manufacturing products to ensure fuel economy while minimizing emissions, owing to the growing environmental concerns.

- According to OICA (The Organisation Internationale des Constructeurs d'Automobiles), automobile production and sales reached 27.021 million and 26.864 million, respectively, in 2022, up 3.4% and 2.1% from the previous year.

- Thus, rising demands from the polyisobutylene applications mentioned above are expected to drive the growth of the market in the Asia-Pacific region.

Polyisobutylene (PIB) Industry Overview

The polyisobutylene market is fragmented in nature. The major players in the studied market (not in any particular order) include BASF SE, Braskem, Dowpol Corporation, TPC Group, and The Lubrizol Corporation, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand from Adhesives and Sealants

- 4.1.2 Rising Demand for PIB from Transportation Sector

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Instability of Polyisobutylene being Non-UV Resistant

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Application

- 5.1.1 Tire Tubes

- 5.1.2 Adhesive and Sealants

- 5.1.3 Lubricants

- 5.1.4 Plasticizers

- 5.1.5 Fuel Additives

- 5.1.6 Electrical Insulation

- 5.1.7 Other Applications (Lube Additives, Etc.)

- 5.2 Geography

- 5.2.1 Asia-Pacific

- 5.2.1.1 China

- 5.2.1.2 India

- 5.2.1.3 Japan

- 5.2.1.4 South Korea

- 5.2.1.5 Rest of Asia-Pacific

- 5.2.2 North America

- 5.2.2.1 United States

- 5.2.2.2 Canada

- 5.2.2.3 Mexico

- 5.2.3 Europe

- 5.2.3.1 Germany

- 5.2.3.2 United Kingdom

- 5.2.3.3 Italy

- 5.2.3.4 France

- 5.2.3.5 Rest of Europe

- 5.2.4 South America

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 Rest of South America

- 5.2.5 Middle East and Africa

- 5.2.5.1 Saudi Arabia

- 5.2.5.2 South Africa

- 5.2.5.3 Rest of Middle East and Africa

- 5.2.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 BASF SE

- 6.4.2 Braskem

- 6.4.3 Dowpol Corporation

- 6.4.4 TPC Group

- 6.4.5 The Lubrizol Corporation

- 6.4.6 Exxon Mobil Corporation

- 6.4.7 JX Nippon Oil & Gas Exploration Corporation

- 6.4.8 Kemipex

- 6.4.9 SABIC

- 6.4.10 Zhejiang Shunda New Material Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Polyisobutylene as Substitute for Wool Fat in Stuffing Agents for the Production of Leather

- 7.2 Other Opportunities

02-2729-4219

+886-2-2729-4219

2025 年聚異丁烯全球市場報告

2025 年聚異丁烯全球市場報告 聚異丁烯市場規模、佔有率和成長分析(按產品類型、分子量、應用、最終用途產業和地區)- 2025-2032 年產業預測氫化聚異丁烯市場按產品類型、最終用途產業和地區分類2030 年異丁烯市場預測:按產品類型、等級、製造流程、應用、最終用戶和地區進行的全球分析

聚異丁烯市場規模、佔有率和成長分析(按產品類型、分子量、應用、最終用途產業和地區)- 2025-2032 年產業預測氫化聚異丁烯市場按產品類型、最終用途產業和地區分類2030 年異丁烯市場預測:按產品類型、等級、製造流程、應用、最終用戶和地區進行的全球分析 聚異丁烯市場規模、佔有率、趨勢分析報告:按產品、最終用途、地區、細分市場預測,2025-2030 年

聚異丁烯市場規模、佔有率、趨勢分析報告:按產品、最終用途、地區、細分市場預測,2025-2030 年 聚異丁烯市場:全球產業分析、市場規模、佔有率、成長、趨勢與未來預測(2025-2032)全球異丁烯市場(2018-2034)

聚異丁烯市場:全球產業分析、市場規模、佔有率、成長、趨勢與未來預測(2025-2032)全球異丁烯市場(2018-2034) 多異丁烯的全球市場 - 全球產業分析,規模,佔有率,成長,趨勢,預測(2031年)2025 - 2034 年聚丁烯-1 市場機會、成長動力、產業趨勢分析與預測

多異丁烯的全球市場 - 全球產業分析,規模,佔有率,成長,趨勢,預測(2031年)2025 - 2034 年聚丁烯-1 市場機會、成長動力、產業趨勢分析與預測 聚異丁烯市場:按等級、分子量、應用和最終用途 - 2025-2030 年全球預測

聚異丁烯市場:按等級、分子量、應用和最終用途 - 2025-2030 年全球預測

▼