|

市場調查報告書

商品編碼

1537632

選礦設備:市場佔有率分析、產業趨勢/統計、成長預測(2024-2029)Mineral Processing Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

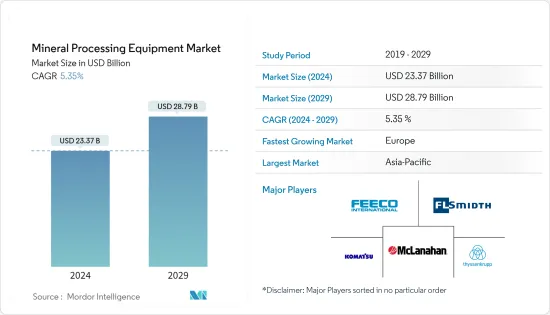

選礦設備市場規模預計到 2024 年為 233.7 億美元,預計到 2029 年將達到 287.9 億美元,在預測期內(2024-2029 年)複合年成長率為 5.35%。

從中期來看,全球採礦機械和設備的進步正在增加鐵、銅和其他礦石等礦物的產量。這種成長體現在重大的擴張和計劃。隨著基礎設施和製造業的增加,對採礦設備的需求也增加,導致各地區的採礦活動增加。

基礎設施領域對鋼、鐵和鋁等金屬的需求增加可能會增加預測期內對選礦設備的需求。此外,採礦業嚴格的安全法規正在刺激自主採礦機械的創新。此外,減少通風有限和礦工呼吸風險的封閉礦井的排放氣體勢在必行,這正在推動電動式和混合採礦機械的進步。

採礦設備製造商優先考慮使用者體驗,致力於創建直覺且使用者友好的介面,以最佳化遠端監控和控制大型採礦設備的便利性和滿意度。這些因素的結合確保採礦設備符合不斷變化的操作要求,其中安全性和用戶滿意度至關重要。然而,開發和擴大採礦活動的困難、環境問題等嚴格的政府法規、採礦成本的增加和安全標準等挑戰可能會限制市場的成長。

選礦設備市場趨勢

鋼鐵預計將成為預測期內成長最快的領域

鋼鐵對於建設業和其他製造業至關重要。在建設產業,90%的提煉金屬是鋼材。然而,礦石品位下降和生產成本上升正在阻礙世界某些地區的生產。

- 2023年,全球可用鐵礦石總產量預計將達25億噸。當年最大的鐵礦石生產國是澳大利亞,生產了9.6億噸可用鐵礦石。

巴西和澳洲的鐵產量大幅成長,企業投資新礦取代舊礦。例如,必和必拓已核准40億美元用於西澳大利亞鐵礦石相關計劃,顯示鐵礦石加工設備的成長。

- 2023年,英美資源集團在南非的昆巴礦場生產了約3,600萬噸(濕基)鐵礦石。英美資源集團是一家跨國礦業公司,總部位於約翰尼斯堡和倫敦。

由於世界各地對鐵礦石的需求不斷增加,多家選礦設備公司正在爭取各種鐵加工設備計劃,以保持在競爭的前沿。例如

- 2024年1月,採礦業最尖端科技解決方案的知名供應商TAKRAF為毛里塔尼亞F'Derick計劃安裝了綜合鐵礦石加工設施,包括破碎、篩分、物料輸送設備和火車裝載站- 成功贏得了與法國國家工業與礦業公司(SNIM) 的一份重要契約,提供搬運系統。

對這些金屬的需求增加將導致採礦活動增加,這可能有助於推動預測期內對新選礦設備的需求。

亞太地區預計將佔據主要市場佔有率

亞太地區是選礦設備的主要市場,以中國、澳洲、印度和日本等國家為首,其中僅中國就佔2023年市場需求的50%以上。這一優勢是由於該地區擁有豐富的活躍礦山,以及將未使用的採礦土地重新用於出口的趨勢不斷成長。此外,在工業和基礎設施發展措施的推動下,該地區對金屬和礦物的需求正在增加。例如

- 印度2024年2月礦產生產指數升至139.6,較2023年2月的水準上漲8%。該指數4月至2月11個月累積年增率為8.2%。

- 鐵礦石產量從2023年4月的2.3億噸增加至2024年2月的2.52億噸,成長9.6%。

- 2023年,中國估計開採了280 MMT的鐵礦石。中國是世界第三大鐵礦石生產國。鋰蘊藏量對於電動車中使用的鋰離子電池至關重要,這刺激了採礦作業的增加,並需要引進先進的選礦機械來進行高效、安全的加工。此外,對煤、銅、礬土、金、鈾和鎳等各種礦物和貴金屬的需求不斷成長,正在推動採用先進加工設備來提高採礦能力。

全部區域礦山產量的增加可能會增加預測期內對選礦設備的需求。

選礦設備產業概況

選礦設備市場由以下全球公司組成: FLSmidth & Co. A/S、Komatsu Ltd、Metso Oyj、FEECO International, Inc. 和Multotec Pty Ltd. 多家設備製造商正在建立合資企業和合作夥伴關係,並推出採用先進技術的新產品,以比競爭對手較具優勢。

- 2023 年 6 月,Epiroc AB 完成了對領先的反循環 (RC) 鑽井產品製造商 Schramm Australia 的主要資產的收購。這些資產包括智慧財產權、珀斯附近的兩個生產設施以及昆士蘭州和南澳大利亞州的兩個服務中心。安百拓僱用 Schramm Australia 員工。

- 2023年4月,FLSmidth贏得中東某金礦價值5,085萬美元的選礦設備訂單。 FLSmidth交付的設備是世界上最高效的設備之一。這項技術使礦山能夠在對環境影響較小的情況下提取黃金。

- 2022 年 5 月,山特維克 AB 收購了 Schenck Process Group (SP Mining) 的採礦業務。透過此次收購,SP Mining 被納入山特維克岩石加工解決方案 (SRP) 旗下定置型破碎和篩檢部門。

其他好處:

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章 簡介

- 調查先決條件

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 市場促進因素

- 對金屬和礦物的需求增加振興了市場

- 市場限制因素

- 嚴格的環境法規和社區擔憂可能會阻礙市場

- 波特五力分析

- 新進入者的威脅

- 買家/消費者的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭公司之間敵對關係的強度

第5章市場區隔

- 按採礦業分類

- 礬土

- 鐵

- 鋰

- 其他

- 按設備分類

- 破碎機

- 餵食器

- 輸送帶

- 鑽頭和破碎機

- 其他

- 按地區

- 北美洲

- 美國

- 加拿大

- 北美其他地區

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 其他歐洲國家

- 亞太地區

- 印度

- 中國

- 日本

- 韓國

- 其他亞太地區

- 世界其他地區

- 南美洲

- 中東/非洲

- 北美洲

第6章 競爭狀況

- 供應商市場佔有率

- 公司簡介

- FLSmidth A/S

- Komatsu Ltd

- Metso Outotec

- FEECO International Inc.

- Multotec Pty Ltd

- McLanahan Corporation

- Sandvik AB

- ThyssenKrupp AG

- TAKRAF GmbH

- McCloskey International

- Sotecma

- Wirtgen Group

- Nordberg Manufacturing Company

- Terex Corporation

第7章 市場機會及未來趨勢

The Mineral Processing Equipment Market size is estimated at USD 23.37 billion in 2024, and is expected to reach USD 28.79 billion by 2029, growing at a CAGR of 5.35% during the forecast period (2024-2029).

Over the medium term, globally, advancements in mining machinery and equipment have increased the production of minerals such as iron, copper, and other ores. This growth has seen large-scale expansions and projects. With the increase in infrastructure and manufacturing sectors, the demand for mining equipment has increased, resulting in an augmented level of mining activity in various regions.

Rising demand for metals such as steel, iron, and aluminum across infrastructure sectors is likely to increase the demand for mineral processing equipment during the forecast period. Moreover, stringent safety regulations in mining sectors have spurred the innovation of autonomous mining machinery. Furthermore, the imperative to mitigate emissions in enclosed mines, where ventilation is limited and poses respiratory risks to miners, has propelled the advancement of electric and hybrid mineral equipment.

Prioritizing user experience, manufacturers of mineral processing machinery are dedicated to crafting intuitive and user-friendly interfaces that optimize convenience and satisfaction for remotely overseeing and controlling large-scale mining equipment. These combined factors ensure that mineral machinery aligns with evolving operational requirements while placing the utmost emphasis on safety and user satisfaction. However, challenges like the difficulty involved in developing and expanding mining activity, strict government regulations such as environmental concerns, an increase in the cost of mining, and safety standards can restrain the market's growth.

Mineral Processing Equipment Market Trends

Iron is Poised to be the Fastest-growing Segment Over the Forecast Period

Iron is critically essential for the construction and other manufacturing industries. In the construction industry, 90% of all refined metal is accounted for by steel. However, falling ore grades and high production costs are hindering production in some parts of the world.

- In 2023, the total volume of usable iron ore produced worldwide amounted to an estimated 2.5 billion metric tons. The leading iron ore-producing country that year was Australia, which produced 960 million metric tons of usable iron ore.

Iron production in Brazil and Australia witnessed a massive increase, with companies investing in new mines to replace older ones. For instance, BHP approved USD 4 billion for iron ore-related projects in Western Australia, indicating growth for iron ore processing equipment.

- In 2023, Anglo American produced around 36 million metric tons (wet basis) of iron ore in the Kumba mine, South Africa. Anglo-American is a multinational mining company headquartered in Johannesburg and London.

Owing to the growing demand for iron ore across the world, several mineral processing equipment companies are securing various iron processing equipment projects to remain at the forefront of the competitive race. For instance,

- In January 2024, TAKRAF, a renowned provider of cutting-edge technological solutions for the mining sector, successfully secured a significant contract with Societe Nationale Industrielle et Miniere (SNIM) for the provision of a comprehensive iron ore processing and handling system, including crushing, screening, and material handling facilities, as well as a train loading station for the F'Derick project in Mauritania.

The increasing demand for these metals will lead to rising mining activity, which may help drive the demand for new mineral processing equipment over the forecast period.

Asia-Pacific is Expected to Hold a Significant Market Share

Asia-Pacific stands as the primary market for mineral processing equipment, led by countries such as China, Australia, India, and Japan, with China alone accounting for over 50% of the market demand in 2023. This dominance is attributed to the region's abundance of active mines and the growing trend of repurposing unused mine sites for exportation. In addition, the region is experiencing heightened demand for metals and minerals driven by industrial and infrastructure development initiatives. For instance,

- In February 2024, India's index of mineral production rose to 139.6, 8% higher than the level recorded in February 2023. The cumulative growth of this index for the 11 months from April to February of FY24 over the corresponding period of the previous year was 8.2%.

- Iron ore production in the country increased from 230 MMT during the 11-month period from April to February of FY23 to 252 MMT during the corresponding period of FY24, at a 9.6% growth rate.

- In 2023, an estimated 280 MMT of iron ore was extracted in China. China is the third-largest producer of iron ore in the world. China's significant reserves of lithium, essential for lithium-ion batteries used in electric vehicles, have spurred increased extraction efforts, necessitating the adoption of advanced mineral processing machinery for efficient and safe processing. Moreover, the escalating demand for various minerals and precious metals like coal, copper, bauxite, gold, uranium, and nickel has prompted the adoption of sophisticated processing equipment to enhance extraction capabilities.

The rise in production of minerls across the region is likely to increase the demand for mineral processing equipment during the forecast period.

Mineral Processing Equipment Industry Overview

The mineral processing equipment market comprises global players such as FLSmidth & Co. A/S, Komatsu Ltd, Metso Oyj, FEECO International, Inc., and Multotec Pty Ltd. Several equipment manufacturers are making joint ventures and partnerships and launching new products with advanced technology to have an edge over their competitors. For instance,

- In June 2023, Epiroc AB completed the purchase of the key assets of Schramm Australia, a major manufacturer of products for reverse circulation (RC) mining drilling. The assets include intellectual property, two production facilities near Perth, and two service centers located in Queensland and South Australia. Epiroc will employ Schramm Australia's employees.

- In April 2023, FLSmidth secured an order worth USD 50.85 million for mineral processing equipment for a gold mine in the Middle East. The equipment delivered by FLSmidth is among the most efficient in the world. When installed, the technology allows the mine to extract gold with reduced impact on the environment.

- In May 2022, Sandvik AB acquired the mining-related business of Schenck Process Group (SP Mining). Through this acquisition, SP Mining reported in Stationary Crushing and Screening, a division of Sandvik Rock Processing Solutions (SRP).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Increasing Demand for Metals and Minerals to Fuel the Market

- 4.2 Market Restraints

- 4.2.1 Stringent Environmental Regulations and Community Concerns may Hinder the Market

- 4.3 Porters Five Force Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD Billion)

- 5.1 By Mineral Mining Sector

- 5.1.1 Bauxite

- 5.1.2 Iron

- 5.1.3 Lithium

- 5.1.4 Others

- 5.2 By Equipment

- 5.2.1 Crushers

- 5.2.2 Feeders

- 5.2.3 Conveyors

- 5.2.4 Drills and Breakers

- 5.2.5 Others

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 India

- 5.3.3.2 China

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 Rest of the World

- 5.3.4.1 South America

- 5.3.4.2 Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles*

- 6.2.1 FLSmidth A/S

- 6.2.2 Komatsu Ltd

- 6.2.3 Metso Outotec

- 6.2.4 FEECO International Inc.

- 6.2.5 Multotec Pty Ltd

- 6.2.6 McLanahan Corporation

- 6.2.7 Sandvik AB

- 6.2.8 ThyssenKrupp AG

- 6.2.9 TAKRAF GmbH

- 6.2.10 McCloskey International

- 6.2.11 Sotecma

- 6.2.12 Wirtgen Group

- 6.2.13 Nordberg Manufacturing Company

- 6.2.14 Terex Corporation

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

全球破碎機、分類機和濃縮機市場(2025 年)

全球破碎機、分類機和濃縮機市場(2025 年) 2025-2033 年按類型、移動性、應用和地區分類的破碎、篩選和選礦設備市場報告

2025-2033 年按類型、移動性、應用和地區分類的破碎、篩選和選礦設備市場報告 ASIC礦機全球市場(2024-2028)

ASIC礦機全球市場(2024-2028) 全球選礦設備市場

全球選礦設備市場 全球選礦設備市場,2024-2028

全球選礦設備市場,2024-2028 碾碎、分選和選礦設備市場:按類型、按應用、按移動性、按銷售類型:2023-2032 年全球機會分析和產業預測

碾碎、分選和選礦設備市場:按類型、按應用、按移動性、按銷售類型:2023-2032 年全球機會分析和產業預測 選礦設備市場規模 - 按設備類型(破碎機、給料機、輸送機、分離器)、按應用(金屬礦石加工、工業選礦、稀土選礦)、移動性、最終用途和預測,2023 - 2032 年

選礦設備市場規模 - 按設備類型(破碎機、給料機、輸送機、分離器)、按應用(金屬礦石加工、工業選礦、稀土選礦)、移動性、最終用途和預測,2023 - 2032 年 溶劑冶金的全球市場(2024年~2034年)

溶劑冶金的全球市場(2024年~2034年)