|

市場調查報告書

商品編碼

1537636

鍶:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029)Strontium - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

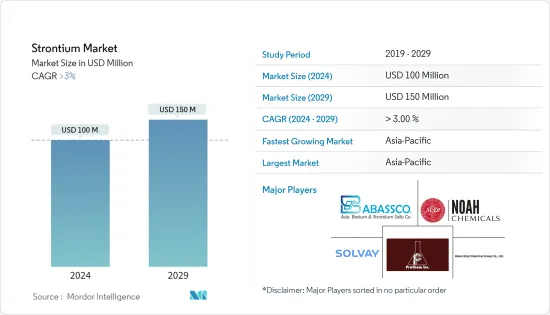

鍶市場規模預計到2024年將達到1億美元,預計到2029年將達到1.5億美元,在預測期內(2024-2029年)複合年成長率將超過3%。

COVID-19大流行對鍶市場產生了負面影響。疫情擾亂了鍶的開採、加工和運輸活動,影響了鍶原料和中間產品的供應。然而,隨著封鎖的解除,各行業的經濟活動逐漸恢復,包括汽車和電子產品,它們是鍶基產品的主要消費者。市場復甦是由產品需求增加所推動的,導致含鍶產品增加。

主要亮點

- 預計推動鍶市場的因素包括油漆和被覆劑對鍶的需求增加以及新興國家建設活動對鍶的需求增加。

- 另一方面,與鍶相關的爆炸和火災風險預計將阻礙市場成長。

- 硝酸鍶預計將主要用於化學、海洋和國防工業。醫療領域的日益成長的使用預計將為市場相關人員提供有利可圖的機會。

- 由於中國、印度和日本等國家的消費增加,預計亞太地區在預測期內將保持其市場主導地位。

鍶市場趨勢

油漆和被覆劑領域佔據市場主導地位

- 硫酸鍶作為硫酸鍶用於油漆和塗料工業。硫酸鍶是一種白色、無味、無害、化學惰性的粉末。它透過充當顏料增量劑(填料)來提高液體和粉末塗料的性能。

- 它還在更高的塗層覆蓋率、更好的機械性能、耐鹽、防霧、抗紫外線等方面表現出優越的性能。主要用於塑膠、液體塗料、粉末塗料等。

- 根據美國塗料協會2023年8月發布的預計,2022年美國油漆塗料市場規模將達318.5億美元,2023年將達335.5億美元。預計到2024年這筆金額將達到357.2億美元。

- 根據美國塗料協會的年度報告,2023年美國油漆和塗料產量達到約13.1億加侖。預計到 2024 年將超過 13.4 億加侖。

- 歐洲有多家大型塗裝企業,其中四大經濟體分別是德國、法國、義大利和西班牙:德國、法國、義大利和西班牙。德國是歐洲重要的油漆和塗料供應商和市場。德國在油漆、清漆和印表機油墨領域擁有 300 多家製造公司。

- 世界油漆和塗料協會 (WPCIA) 報告中納入的油漆和塗料行業主要企業包括宣偉 (Sherwin Williams)、PPG Industries Inc.、阿克蘇諾貝爾 (Akzo Nobel NV) 和日本塗料控股公司 (Nippon Paint Holdings)。

- 這將使資金注入各個行業,增加世界各地對油漆和被覆劑的需求,並支持鍶市場。

亞太地區主導市場

- 由於生產和消費各種鍶基最終產品,包括油漆和被覆劑、化妝品以及電氣和電子設備,亞太地區是最重要的鍶市場。

- 印度商務部工業和內貿促進部發布的報告顯示,2022會計年度印度塗料產業貿易額超過600億印度盧比。該國塗料及相關產品的出口額約為229.6億印度盧比,而進口額則超過377億印度盧比。

- 此外,中國的建設產業預計將在亞太地區成長最快,其次是印度。為了滿足日益成長的住宅需求,中國政府正在提供更多資金建造保障性住宅。基礎設施領域已成為印度政府重點關注領域之一。

- 中國的建設產業正在快速擴張。根據中國國家統計局預計,中國建築業產值年終約為31.2兆元(4.31兆美元),2023年將達31.59兆元人民幣(4.37兆美元)。

- 所有這些建設活動和政府措施預計將增加該國的建築計劃數量,從而導致對油漆和清漆的需求增加。

- 隨著亞太地區許多產業尋求成長,預計未來五年對鍶的需求也將增加。

鍶行業概況

鍶市場本質上高度分散。市場主要參與者有(排名不分先後)索爾維、Abassco、河北辛集化工集團、諾亞化學、ProChem Inc.等。

其他好處:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第1章 簡介

- 調查先決條件

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 促進因素

- 塗料產業需求增加

- 亞太新興經濟體建設活動增加

- 抑制因素

- 與鍶相關的爆炸和火災風險

- 其他阻礙因素

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 買方議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

- 價格趨勢

第5章市場區隔

- 依產品

- 碳酸鍶

- 硫酸鍶

- 硝酸鍶

- 其他產品(氫氧化鍶)

- 按用途

- 電力/電子

- 醫療/牙科

- 油漆/塗料

- 個人護理

- 焰火

- 其他用途(玻璃、陶瓷)

- 按地區

- 生產分析

- 中國

- 西班牙

- 土耳其

- 墨西哥

- 伊朗

- 阿根廷

- 世界其他地區

- 按消費分析

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 泰國

- 馬來西亞

- 印尼

- 越南

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 義大利

- 法國

- 西班牙

- 土耳其

- 俄羅斯

- 北歐的

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 哥倫比亞

- 南美洲其他地區

- 中東/非洲

- 沙烏地阿拉伯

- 南非

- 奈及利亞

- 埃及

- 卡達

- 阿拉伯聯合大公國

- 其他中東和非洲

- 生產分析

第6章 競爭狀況

- 併購、合資、聯盟、協議

- 市場佔有率(%)/排名分析

- 主要企業策略

- 公司簡介

- Abassco

- Barium & Chemicals Inc.

- Chongqing Yuanhe Fine Chemicals Inc.

- Fertiberia

- Hebei Xinji Chemical Group Co. Ltd

- Joyieng Chemical Limited

- KBM Affilips

- Nanjing Jinyan Strontium Industry Co. Ltd

- Noah Chemicals

- ProChem Inc.

- SAKAI CHEMICAL INDUSTRY CO. LTD

- Shenzhou Jiaxin Chemical Co. Ltd

- Shijiazhuang Zhengding JINSHI Chemical Co. Ltd

- Solvay

第7章 市場機會及未來趨勢

- 增加硝酸鍶在化學、海洋和國防領域的使用

- 醫療領域的使用增加

The Strontium Market size is estimated at USD 100 million in 2024, and is expected to reach USD 150 million by 2029, growing at a CAGR of greater than 3% during the forecast period (2024-2029).

The COVID-19 pandemic negatively impacted the strontium market. The pandemic disrupted strontium mining, processing, and transportation activities, affecting the availability of strontium raw materials and intermediate products. However, as lockdowns were lifted, economic activities gradually resumed across industries, including automotive and electronics, which are significant consumers of strontium-based products. The market recovery was driven by increased demand for goods, which led to a rise in strontium-content products.

Key Highlights

- The factors that are expected to drive the strontium market are the rising demand for strontium from paints and coatings and the increasing demand for strontium from construction activities in developing countries.

- On the flip side, the risk of explosion and fire hazards that are associated with strontium is expected to hinder the growth of the market.

- It is expected that strontium nitrate will be used majorly in the chemical, marine, and defense industries. The increasing usage in the medical field is expected to provide lucrative opportunities for the market players.

- Due to increasing consumption in countries such as China, India, and Japan, the Asia-Pacific is expected to maintain its dominance of the market during the forecast period.

Strontium Market Trends

Paints and Coatings Segment to Dominate the Market

- Strontium sulfate is used in the paint and coating industry as strontium sulfate. Strontium sulfate is a white, odorless, and unhazardous chemical inert powder. It improves the performance of liquid paint and powder coatings by acting as a pigment extender (filler).

- In addition, it provides higher film coverage, more extraordinary mechanical properties, and excellent performance in the areas of salt, fog, or UV resistance. It's mainly used in plastics, liquid paints, powder coats, and so on.

- According to the estimate released by the American Coatings Association in August 2023, the market value of paints and coatings in the United States was USD 31.85 billion in 2022 and USD 33.55 billion in 2023. This value is expected to reach USD 35.72 billion in 2024.

- The volume of paint and coating production in the United States reached about 1.31 billion gallons in 2023, according to an annual report from the American Coatings Association. It is forecasted that the industry's production will surpass 1.34 billion gallons in 2024.

- Europe is home to a multitude of large painting companies, with its four largest mainland economies: Germany, France, Italy, and Spain. Germany is a significant provider and market of paints and coatings in Europe. It is home to over 300 production companies in the field of paint, varnish, and printer ink.

- Some of the key firms in the paints and coatings sector included in the World's Paints and Coatings Association (WPCIA) report are Sherwin Williams, PPG Industries Inc., Akzo Nobel NV, and Nippon Paint Holdings Co. Ltd.

- This will make it possible to invest more money in different sectors, which will increase demand for paints and coatings from all over the world and help the strontium market.

Asia-Pacific Region to Dominate the Market

- Due to the production and consumption of a wide range of end products made from strontium, including paints and coatings, cosmetics, electrical and electronic equipment, and others, the Asia Pacific region is the most critical market for strontium.

- According to the report published by the Department of Commerce (India), Department for Promotion of Industry and Internal Trade (India), in fiscal year 2022, the trade value of India's paint sector was over INR 60 billion. The value of exported paint and associated products in the country stood at around INR 22.96 billion, compared to more than INR 37.7 billion for imports.

- In addition, Asia-Pacific is likely to grow fastest in Chinese construction, followed by India. In order to meet the increasing demand for housing, the Chinese government has provided more funds so that affordable houses can be built. The infrastructure sector has become one of the main focus areas of the government in India.

- The Chinese building and construction industry is expanding at a rapid pace. Construction output in China was estimated to be worth about CNY 31.2 trillion (USD 4.31 trillion) at the end of 2022, reaching CNY 31.59 trillion by 2023 (USD 4.37 trillion), according to an estimate released by the Chinese National Statistics Office.

- The number of building projects in this country is expected to increase due to all these construction activities and government measures, which are expected to lead to a higher demand for paints and varnishes.

- The demand for strontium is also expected to increase over the next five years, as many industries in Asia-Pacific are looking for growth.

Strontium Industry Overview

The strontium market is highly fragmented in nature. The major players in the market include (not in any particular order) Solvay, Abassco, Hebei Xinji Chemical Group Co. Ltd, Noah Chemicals, and ProChem Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increased Demand from the Paints and Coatings Segment

- 4.1.2 Increasing Construction Activities in Emerging Economies of Asia-Pacific

- 4.2 Restraints

- 4.2.1 Risk of Explosion and Fire Hazards Associated with Strontium

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

- 4.5 Price trends

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 By Product

- 5.1.1 Strontium Carbonate

- 5.1.2 Strontium Sulfate

- 5.1.3 Strontium Nitrate

- 5.1.4 Other Products (Strontium Hydroxide)

- 5.2 By Application

- 5.2.1 Electrical and electronics

- 5.2.2 Medical and Dental

- 5.2.3 Paints and Coatings

- 5.2.4 Personal Care

- 5.2.5 Pyrotechnic

- 5.2.6 Other Applications (Glass and Ceramics)

- 5.3 By Geography

- 5.3.1 Production Analysis

- 5.3.1.1 China

- 5.3.1.2 Spain

- 5.3.1.3 Turkey

- 5.3.1.4 Mexico

- 5.3.1.5 Iran

- 5.3.1.6 Argentina

- 5.3.1.7 Rest of the World

- 5.3.2 By Consumption Analysis

- 5.3.2.1 Asia-Pacific

- 5.3.2.1.1 China

- 5.3.2.1.2 India

- 5.3.2.1.3 Japan

- 5.3.2.1.4 South Korea

- 5.3.2.1.5 Thailand

- 5.3.2.1.6 Malaysia

- 5.3.2.1.7 Indonesia

- 5.3.2.1.8 Vietnam

- 5.3.2.1.9 Rest of Asia-Pacific

- 5.3.2.2 North America

- 5.3.2.2.1 United States

- 5.3.2.2.2 Canada

- 5.3.2.2.3 Mexico

- 5.3.2.3 Europe

- 5.3.2.3.1 Germany

- 5.3.2.3.2 United Kingdom

- 5.3.2.3.3 Italy

- 5.3.2.3.4 France

- 5.3.2.3.5 Spain

- 5.3.2.3.6 Turkey

- 5.3.2.3.7 Russia

- 5.3.2.3.8 NORDIC

- 5.3.2.3.9 Rest of Europe

- 5.3.2.4 South America

- 5.3.2.4.1 Brazil

- 5.3.2.4.2 Argentina

- 5.3.2.4.3 Colombia

- 5.3.2.4.4 Rest of South America

- 5.3.2.5 Middle East and Africa

- 5.3.2.5.1 Saudi Arabia

- 5.3.2.5.2 South Africa

- 5.3.2.5.3 Nigeria

- 5.3.2.5.4 Egypt

- 5.3.2.5.5 Qatar

- 5.3.2.5.6 United Arab Emirates

- 5.3.2.5.7 Rest of Middle East and Africa

- 5.3.1 Production Analysis

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/ Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Abassco

- 6.4.2 Barium & Chemicals Inc.

- 6.4.3 Chongqing Yuanhe Fine Chemicals Inc.

- 6.4.4 Fertiberia

- 6.4.5 Hebei Xinji Chemical Group Co. Ltd

- 6.4.6 Joyieng Chemical Limited

- 6.4.7 KBM Affilips

- 6.4.8 Nanjing Jinyan Strontium Industry Co. Ltd

- 6.4.9 Noah Chemicals

- 6.4.10 ProChem Inc.

- 6.4.11 SAKAI CHEMICAL INDUSTRY CO. LTD

- 6.4.12 Shenzhou Jiaxin Chemical Co. Ltd

- 6.4.13 Shijiazhuang Zhengding JINSHI Chemical Co. Ltd

- 6.4.14 Solvay

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Use of Strontium Nitrate in the Chemical, Marine, and Defense Sectors

- 7.2 Increasing Usage in Medical Field