|

市場調查報告書

商品編碼

1537645

同調雷達:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029)Coherent Radar - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

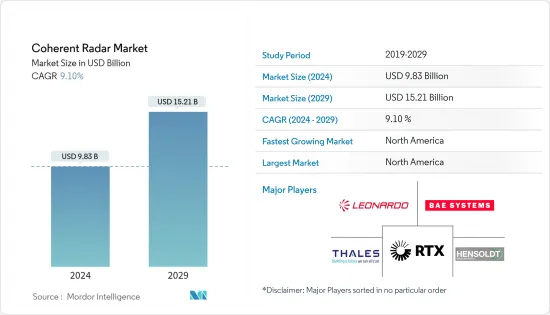

同調雷達市場規模預計到 2024 年為 98.3 億美元,預計到 2029 年將達到 152.1 億美元,在預測期內(2024-2029 年)複合年成長率為 9.10%。

同調雷達在軍事領域有多種應用。 同調雷達可以偵測和追蹤快速移動的隱形目標,並提供地形和物體的高解析度影像。由於中東和亞太地區等某些地區的恐怖主義不斷加劇以及地緣政治緊張局勢,預計未來幾年軍事領域對同調雷達的需求將會成長。這一因素增加了用於現代化監視技術(例如用於檢測任何潛在威脅的同調雷達)的國防支出。

戰場的快速數位化促進了C4ISR系統的採用,以獲得針對敵方部隊的戰術性優勢。其中包括同化來自各種資訊來源的資料,包括透過使用同調雷達進行被動感測和監視,從而為在戰場上採用這些系統創造機會。

然而,先進的同調雷達系統的採用僅限於技術先進的國家。因此,如果採購和研發資金被轉移到其他領域,可能會對市場成長產生負面影響。儘管存在這些因素,由於地緣政治緊張局勢加劇和世界各國國防開支增加導致的需求,預計市場在預測期內將出現正成長。

雷達技術的不斷進步,例如固體雷達系統的開發和人工智慧的整合,預計將推動該市場的成長,因為它們可以提高雷達系統的性能和效率。

同調雷達市場趨勢

空降同調雷達領域呈現最高成長率

機載同調雷達在軍事上有多種應用,包括防空、飛彈防禦以及情報、監視和偵察 (ISR)。因此,世界各國都在大幅增加軍事開支,以開發和採購配備先進光電/紅外線系統、預警系統和全天候雷達系統的多用途隱形戰鬥機。

由於世界主要國家的軍事開支增加和各種現代化努力,預計該領域的成長將會增加。例如,2022年全球軍費開支達2.24兆美元,較2021年成長6%。隨著國防費用的增加,美國、法國、德國、俄羅斯、英國和日本等國家目前都致力於開發隱形戰鬥機技術。例如,2022年11月,法國、德國和西班牙簽署了一項協議,根據未來作戰空中系統計畫開始下一階段的新型戰鬥機開發工作。該國防計劃預計耗資超過1,034億美元。根據該計劃,這些國家預計將更換 F-18 和颱風戰鬥機等較舊的戰鬥機機隊。

同樣,2023 年 12 月,英國與日本和義大利簽署了一項協議,開發下一代隱形戰鬥機,作為未來作戰空中計畫的一部分。該戰鬥機預計將具有超音速能力,並配備此類軍用飛機的最新技術,包括連貫機載雷達。

印度、以色列和土耳其等國也正在投資無人機的開發和採購,以增強其情監偵力量。例如,2023年11月,印度與IAI簽署契約,採購六架非武裝Hermes 900無人機,以增強該國的監視能力。總體而言,一些國家國防軍採用隱形技術同調雷達相干雷達能夠穿透敵方防空系統,以靜默方式監視目標並在需要時摧毀它們。預計這將在預測期內推動該細分市場的需求。

北美地區成長率最高

美國是北美同調雷達等先進雷達技術的熱衷開發者與使用者。軍事領域這一市場的需求是由美國龐大的軍事開支所推動的,這支持了包括同調雷達技術在內的各種雷達技術的開發和採購。例如,2022年美國軍事國防費用達8,770億美元,比2021年成長9%。對技術先進武器的投資增加是由於中國和俄羅斯在戰場上的能力增強所構成的威脅越來越大,這一因素極大地推動了該國對同調雷達系統的需求。

隨著國防支出的增加,美國正在積極訂購大型軍機以增強其防禦能力,這正在提振美國市場的需求。例如,截至2022年12月,美國已訂購約2,000架F-35A/B/C飛機。諾斯羅普·格魯曼公司為這些 F-35 提供主動電子掃描陣列 (AESA) 雷達,這些 AESA 雷達系統包括許多單獨的輻射元件,每個輻射元件都有一個發射器和接收器模組。這些模組協同工作,形成同調雷達波束,以偵測潛在的空中威脅。

北美也是主要國防技術公司的所在地,這些公司不斷投資開發先進的情境察覺增強系統。例如,Raven Industries Inc. 是透過其 HiPointer 100同調雷達系統解決方案向同調雷達市場提供解決方案的OEM之一。該公司的 HiPointer 100 提高了持續監視能力,並增強了各種有人和無人平台的全面情境察覺,為陸地、海上和空中的最終用戶和決策者提供極低的誤報,使您能夠在動態情報、監視、和偵察(ISR)任務。

同調雷達行業概覽

同調雷達系統市場由 HENSOLDT AG、RTX Corporation、BAE Systems PLC、Leonardo SpA 和 Thales 等主要參與者主導,佔據了大部分市場佔有率。

國防部門嚴格的安全和監管政策預計將限制新進入者。隨著敵方航空平台和武器擴大採用隱形技術,市場開發商正在專注於開發先進的雷達系統,以有效探測小型雷達截面的目標。為了確保與最終用戶國家的長期合作夥伴關係並促進與各種軍事資產的整合,這些公司正在投入資源來開發尖端雷達技術。

其他好處:

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章 簡介

- 調查先決條件

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 市場概況

- 市場促進因素

- 市場限制因素

- 波特五力分析

- 新進入者的威脅

- 買家/消費者的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭公司之間敵對關係的強度

第5章市場區隔

- 按平台

- 海軍

- 地上

- 海軍

- 按地區

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 印度

- 中國

- 日本

- 韓國

- 其他亞太地區

- 世界其他地區

- 拉丁美洲

- 中東/非洲

- 北美洲

第6章 競爭狀況

- 供應商市場佔有率

- 公司簡介

- HENSOLDT AG

- BAE Systems PLC

- IAI

- Leonardo SpA

- RTX Corporation

- Lockheed Martin Corporation

- Thales

- Saab AB

- L3 Harris Technologies Inc.

- Indra Sistemas SA

第7章 市場機會及未來趨勢

The Coherent Radar Market size is estimated at USD 9.83 billion in 2024, and is expected to reach USD 15.21 billion by 2029, growing at a CAGR of 9.10% during the forecast period (2024-2029).

Coherent radar has various applications in the military. It can detect and track fast-moving and stealthy targets and provide high-resolution images of the terrain and objects of interest. The demand for coherent radar in the military is expected to grow in the coming years due to the rise in terrorism and geopolitical tensions in certain regions like the Middle East and Asia-Pacific. This factor has led to a rise in defense expenditure on modernizing surveillance technology, such as coherent radar, to detect any potential threat.

The rapid digitization of the battlefield has fostered the adoption of C4ISR systems to gain a tactical edge over hostile forces. These include the assimilation of data from various sources, including passive detection and monitoring through the use of coherent radars, thereby creating an opportunity for adopting these systems on the battlefield.

However, adopting advanced coherent radar systems is limited to technologically advanced countries. Hence, the diversion of procurement and R&D funds toward other sectors can deleteriously affect market growth. Despite this factor, the market is expected to grow positively during the forecast period due to the demand driven by rising geopolitical tensions and increasing defense expenditures in various economies worldwide.

Continuous advancements in radar technologies, such as the development of solid-state radar systems and the integration of artificial intelligence, are expected to drive the growth of this market as these technological advancements enable improved performance and increased efficiency of radar systems.

Coherent Radar Market Trends

Airborne Coherent Radar Segment to Exhibit the Highest Growth Rate

Airborne coherent radar has various applications in the military, such as air and missile defense, intelligence, surveillance, and reconnaissance (ISR). Hence, various countries worldwide are significantly increasing their military spending in developing and procuring multirole and stealth fighter aircraft equipped with advanced EO/IR systems, early warning systems, and all-weather radar systems.

The growth of this segment is expected to increase due to rising military expenditure and various modernization efforts by major global powers. For instance, in 2022, the global military expenditure reached USD 2,240 billion, a growth of 6% from 2021. With this increased defense expenditure, various countries, such as the United States, France, Germany, Russia, the United Kingdom, and Japan, are currently working on the development of stealth fighter jet technology. For instance, in November 2022, France, Germany, and Spain signed an agreement to start the next phase of development of a new fighter jet under the Future Combat Air System program. The defense project is estimated to cost more than USD 103.4 billion. Under the program, these countries are expected to replace older fighter aircraft fleets such as the F-18 and Typhoon.

Similarly, in December 2023, the United Kingdom entered an agreement with Japan and Italy to create a next-generation stealth fighter as part of the future combat air program. The fighter is expected to have supersonic capabilities and be equipped with the latest technology in these military aircraft, such as coherent airborne radars.

Countries such as India, Israel, and Turkey are also investing in developing and procuring unmanned air vehicles to boost their ISR strength. For instance, in November 2023, India awarded a contract to IAI to procure six Hermes 900 unarmed drones to augment the country's surveillance capabilities. Overall, the adoption of stealth technology by the defense forces of several countries necessitates the integration of coherent radar systems on board the aircraft to silently monitor the target and penetrate enemy air defenses to neutralize them if the need arises. This is expected to drive the demand for this segment during the forecast period.

North America to Exhibit the Highest Growth Rate

The United States is an avid developer and user of sophisticated radar technologies such as coherent radar in North America. The demand for this market in the military is driven by the large military spending of the United States, which, in turn, supports the development and procurement of various radar technologies, including coherent radar technologies. For instance, in 2022, the US military defense expenditure rose to USD 877 billion, a growth of 9% compared to 2021. The increased investments toward technologically advanced weaponry are due to the growing threat to the country from the enhanced capabilities of China and Russia on the battlefield, and this factor is heavily driving the demand for coherent radar systems in the country.

With this increased defense spending, the United States is actively ordering huge military aircraft to enhance its defense capabilities, which is driving the demand for this market in the United States. For instance, as of December 2022, the US military had placed orders for around 2,000 F-35A/B/C aircraft variants. For these F-35s, Northrop Grumman provides its active electronically scanned array (AESA) radar, and these AESA radar systems involve numerous individual radiating elements, each with its own transmit and receive module. These modules work harmoniously to form a coherent radar beam to detect potential airborne threats.

North America is also home to leading defense technology firms that are constantly investing in developing advanced situational awareness enhancement systems. For instance, Raven Industries Inc. is one of the OEMs that provides its solutions in the coherent radar market with its HiPointer 100 coherent radar system solution. The company's HiPointer 100 increases persistent surveillance capabilities, enhances total situational awareness from a diverse set of manned and unmanned platforms with extremely low false alarms, and enables end users and decision-makers to achieve success in dynamic intelligence, surveillance, and reconnaissance (ISR) missions spanning land, sea, and air.

Coherent Radar Industry Overview

The coherent radar systems market is consolidated with leading players, such as HENSOLDT AG, RTX Corporation, BAE Systems PLC, Leonardo SpA, and Thales, accounting for a majority of the market share.

The stringent safety and regulatory policies in the defense segment are expected to restrict the entry of new players. With the growing implementation of stealth technologies in adversary aerial platforms and weapons, market players are focusing on the development of sophisticated radar systems that can effectively detect targets with lower radar cross-sections. To ensure long-term partnerships with end-user countries and easy integration with a broad spectrum of military assets, these companies are dedicating their resources to the development of cutting-edge radar technology.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Platform

- 5.1.1 Airborne

- 5.1.2 Terrestrial

- 5.1.3 Naval

- 5.2 Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.2 Europe

- 5.2.2.1 Germany

- 5.2.2.2 United Kingdom

- 5.2.2.3 France

- 5.2.2.4 Russia

- 5.2.2.5 Rest of Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 India

- 5.2.3.2 China

- 5.2.3.3 Japan

- 5.2.3.4 South Korea

- 5.2.3.5 Rest of Asia-Pacific

- 5.2.4 Rest of the World

- 5.2.4.1 Latin America

- 5.2.4.2 Middle East and Africa

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 HENSOLDT AG

- 6.2.2 BAE Systems PLC

- 6.2.3 IAI

- 6.2.4 Leonardo SpA

- 6.2.5 RTX Corporation

- 6.2.6 Lockheed Martin Corporation

- 6.2.7 Thales

- 6.2.8 Saab AB

- 6.2.9 L3 Harris Technologies Inc.

- 6.2.10 Indra Sistemas SA